Founded in 1849, Pfizer (PFE) is one of the world’s largest drugmakers, with medications sold in over 125 countries. The company’s annual sales exceed $50 billion and are grouped into three business segments:

This unit drives Pfizer’s overall growth because it produces all of the company’s largest sellers, including a number of medications with more than $1 billion in annual sales.

Compared to other pharma and biotech companies, Pfizer’s portfolio is nicely diversified by treatment area and drug type, reducing its risk profile.

Pfizer’s largest drugs in this segment are:

- The Prevnar family of therapeutics (10.8% of company-wide sales; pneumococcal vaccines)

- Lyrica (8.6%; epilepsy)

- Ibrance (7.7%; breast cancer)

- Eliquis (6.4%; blood thinner to reduce risk of strokes)

- Enbrel (3.9%; arthritis)

- Xeljanz (3.3%; arthritis)

This unit also produces and markets biosimilars (1% of sales; fast-growing generic versions of biological drugs) and sterile injectable products.

Upjohn (37% of sales): markets Pfizer’s legacy medications that have lost patent protection, such as Lipitor (3.6% of company-wide sales; cholesterol), Norvasc (1.8%; high blood pressure), the Premarin family (1.8%; menopause), and Celebrex (1.5%; arthritis). This segment sells certain generic drugs as well.

Consumer Healthcare (7% of sales): consists of dietary supplements, pain management, gastrointestinal, and respiratory and personal care products marketed under some of industry’s most trusted names.

Pfizer plans to merge this business with GlaxoSmithKline’s consumer healthcare division to become the world’s largest maker of over-the-counter products. The deal is expected to close in the second half of 2019, with plans to eventually spin off the company within five years. Pfizer will own 32% of the joint venture.

In total, Pfizer’s sales are split about equally between the U.S. and the rest of the world (16% Europe and 13% developed non-European countries), with emerging markets accounting for just over 20% of company-wide revenue.

Pfizer’s dividend track record is stained by a 2009 dividend cut associated with its $68 billion purchase of Wyeth. Pfizer’s purchase was made necessary by a large patent cliff (most notably cholesterol drug Lipitor losing patent protection in 2011) that the firm desired to overcome by acquiring a strong collection of existing drugs on the market as well as new development pipeline candidates.

Business Analysis

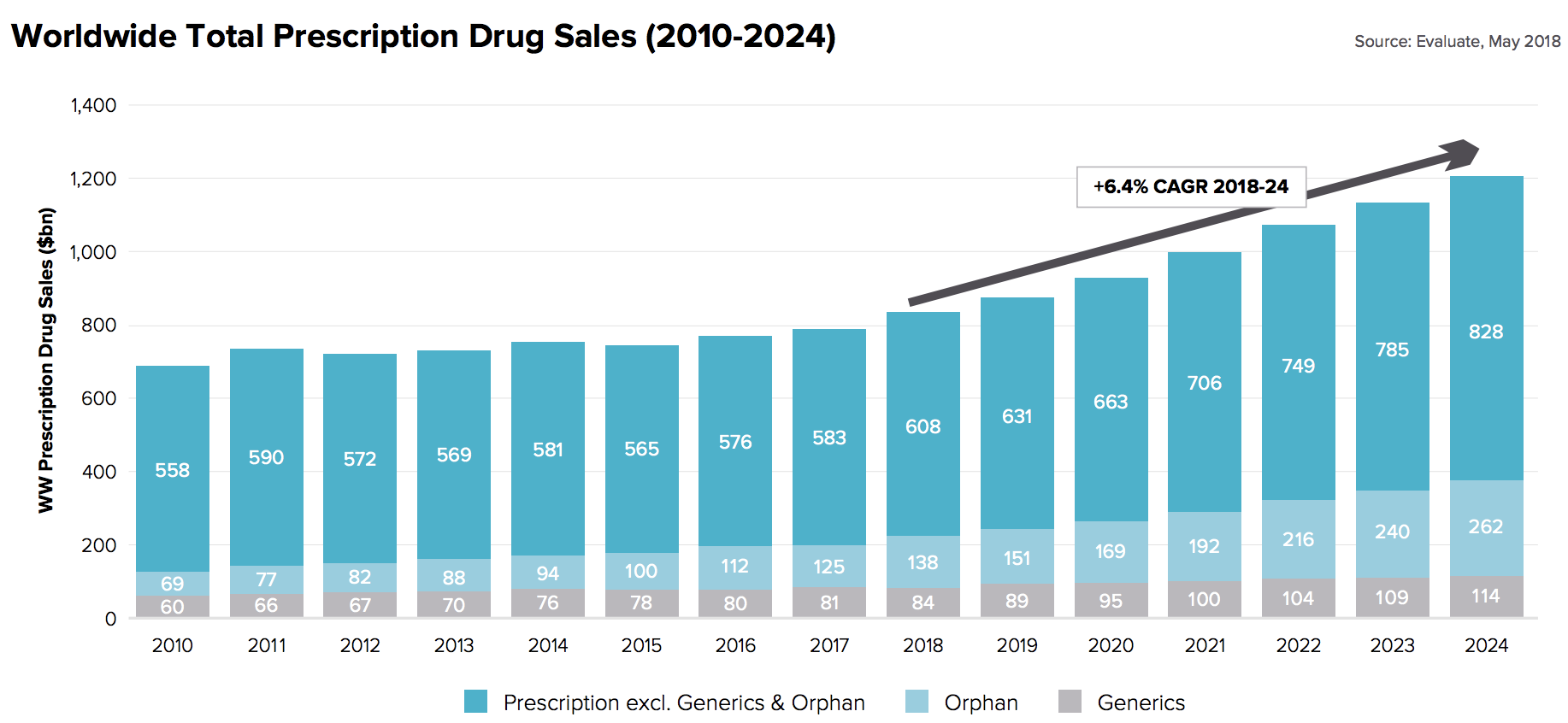

In theory, blue-chip drugmakers are dependable dividend stocks because the demand for their products is stable and recession resistant. And with the strong growth in demand for healthcare products, courtesy of an aging global population, overall drug sales are expected to continue increasing over time. In fact, worldwide prescription drug sales are projected to grow 6.4% annually through 2024, according to research firm EvaluatePharma.

Source: EvaluatePharma

Source: EvaluatePharma

While it is very expensive to research, develop, and ultimately commercialize a new drug, these companies can enjoy years of monopoly-like profits and strong growth with a successful product launch. However, drug companies actually face many challenges when it comes to generating sustainable growth.

Patent expirations, strong competition from similar products (launched by rivals), and the fast growth of cheaper generic drugs mean that pharmaceutical companies such as Pfizer face an uphill battle when it comes to growing their sales and earnings.

Drugs that lose market exclusivity often fade quickly, so their revenue must be replaced by new drugs that find success. Combined with the steep cost of developing new drugs, this is why Pfizer routinely spends about 15% of its sales on R&D each year. As a result, the company’s fixed costs are relatively high, so its margins can be somewhat volatile if a major chunk of drug revenue is lost any given year due to patent expirations.

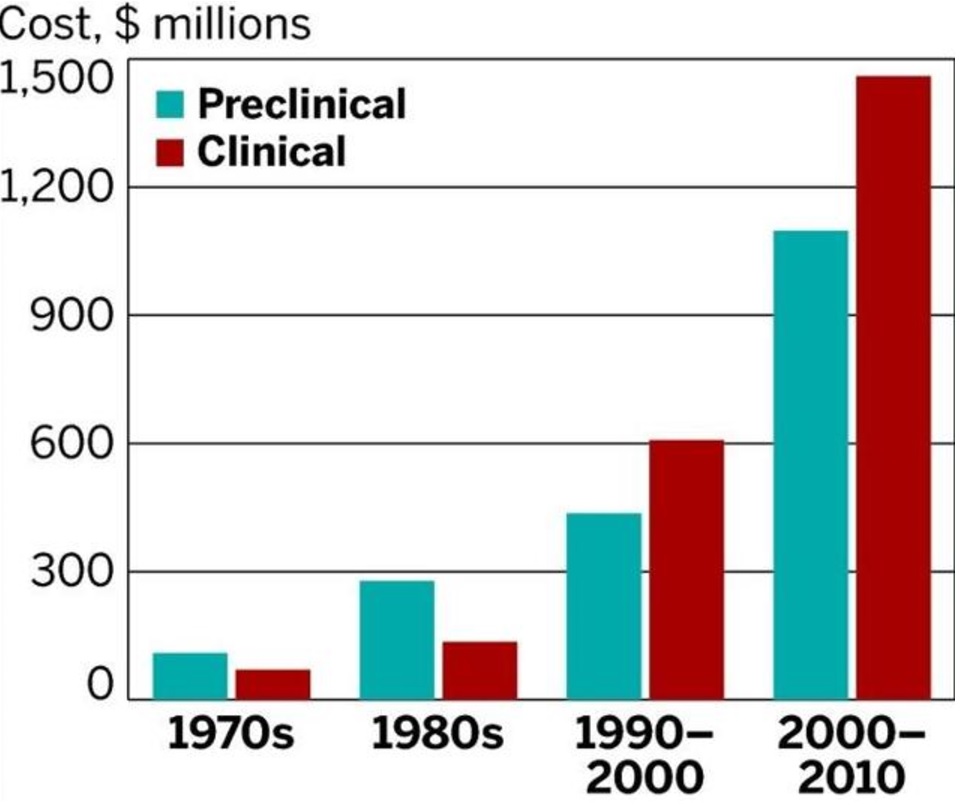

With that said, Pfizer enjoys meaningful competitive advantages, driven in part by the high development costs and complex regulatory hurdles required to bring a new drug to market (a process that can cost over one billion dollars and take as long as 15 years).

Few companies in the world can match Pfizer’s enormous resources and technical know-how. While it’s true that patents are temporary, they allow for very high margins on drugs while they are in effect, making Pfizer a free cash flow generating machine (free cash flow margin over 30% in 2018). The firm’s substantial cash flow allows it to be generous with buybacks and dividends.

Another competitive advantage Pfizer has is its very large, globally distributed sales force, which has had much success in growing the firm’s drug sales in emerging markets, such as Brazil, Russia, India, and China. Developing nations are where the majority of future long-term growth is likely to come as many developed nations struggle with flat or even declining population growth rates.

Besides international expansion, part of Pfizer’s strategy consists of diversifying its business from pure patented drugs into two major growth areas, biosimilars and sterile injectables.

There are two kinds of drugs, chemical-based (derived from organic compounds, such as various proteins) and biological (enzymes derived from biological sources). When a chemical drug goes off patent, the formula is known and can be easily replicated in any manufacturing facility around the world, resulting in margins falling off a cliff.

However, biosimilars have a distinct advantage in that after a biosimilar goes off patent, any rival attempting to recreate it must go through the same regulatory hurdles that the original biological drug had to pass through to achieve initial approval. In other words, while generic drugs are cheap and easy to make, biosimilars are far more complex, expensive, and time-consuming to bring to market, even if a drug’s patent expires.

This creates a wider moat around such drugs, and because biosimilar drugs are already proven market winners (the original biological drug was a blockbuster), there is less risk to developing them than with brand new medications.

Not surprisingly, pharmaceutical companies are racing to get into this fast-growing and highly profitable space. In fact, there are over 200 biosimilars currently in development, according to EvaluatePharma and PharmaCompass.

Pfizer got into with biosimilars in 2015 with its $16 billion acquisition of Hospira, which had a strong biosimilar development portfolio ($20 billion global market expected by 2020), as well as a platform in the fast-growing injectables market ($70 billion global market expected by 2020).

Pfizer is known as a serial acquirer (like most big drugmakers), having made 29 notable M&A deals over the decades. The firm’s last big purchase was Medivation which Pfizer bought for $14 billion in August 2016. Medivation gave Pfizer the prostate cancer drug Xtandi, which saw nearly 20% sales growth in 2018 and management believes can generate over $1 billion in U.S. sales alone by 2020 (versus $590 million global sales in 2018).

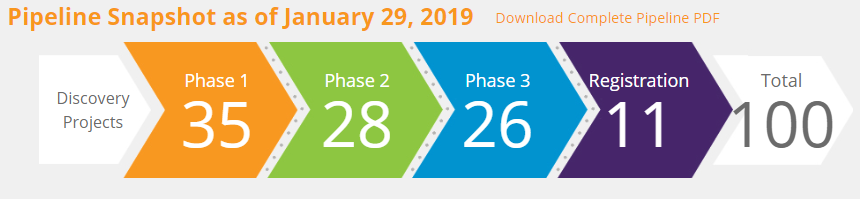

These deals have helped grow the company’s development pipeline to an industry leading 100 products/indications in development, including 15 blockbusters that could be approved for sale by regulators by 2022.

Management believes each of these blockbuster drugs in the pipeline has potential to generate $1 billion or more in annual sales, and half of them could receive approval by 2020.

In recent years Pfizer has transitioned its business to combat declining sales from key products losing market exclusivity, such as Lipitor in 2011 and Viagra in 2017, and increased generic competition. Moves to spin-off its animal health business for more than $2 billion in early 2013 and the company’s plans to combine its consumer healthcare unit with GlaxoSmithKline all point to a future in which Pfizer’s business is completely dominated by prescription drugs.

Fortunately, the company believes it is nearing an inflection point where new product launches (including the 15 potential blockbusters previously mentioned) and fewer losses from major drugs coming off patent protection will drive revenue higher over the coming years.

Here’s what former CEO Ian Read stated in late 2017:

“We expect the full-year year-over-year impact of [loss of exclusivity] to continue to be significantly lower than our recent past. We’re forecasting the impact to be approximately $2 billion in each of the next three years, about $1 billion in 2021, and then $500 million or less from 2022 through 2025. At the same time, we expect a steady flow of new products to begin to emerge from our pipeline.”

Pfizer’s only notable loss of patent protection for the foreseeable future is for its drug Lyrica (8.6% of sales), which is expected to come under pressure in late 2019 and 2020. However, starting in 2021, Pfizer believes it can start generating mid-single-digit sales growth and even faster earnings growth.

“Once we get past the Lyrica [loss of exclusivity], beginning at 2021 with 2020 as a base, we expect that top line to grow into mid-single-digit. And we will make sure, we leverage that relative to the bottom line, get operating leverage margin and margin expansion, so that revenues are growing at a rate that’s more than the expenses.” – CFO Frank D’Amelio

While mid-single-digit top lien growth may not sound like much, Pfizer’s annual revenue has grown by 2% of less in seven of the last eight years. Thanks to a strong focus on oncology and immunology, which are two of the largest and fastest parts of the drug market, Pfizer’s strong drug pipeline (which Pfizer’s CEO calls its “greatest pipeline ever”) seems likely to help it to overcome its upcoming patent losses.

Overall, Pfizer has significant competitive advantages, including substantial economies of scale, access to vast amounts cheap capital (an “AA” credit rating from S&P), a well-diversified drug portfolio (no drug greater than 11% of total sales), and a business model that generates significant free cash flow each year. These factors have made the stock a popular holding in conservative retirement portfolios.

However, as with most major drugmakers, Pfizer has a somewhat complex risk profile.

Key Risks

It’s important to realize that the pharma industry is one that is capital intensive and, thanks to the periodic expiration of patents, also cyclical. The path to long-term growth is not linear, with a giant company like Pfizer sometimes experiencing years of flat sales followed by an acceleration later.

According to CFO Frank D’Amelio, in 2019 Pfizer faces a $2.6 billion sales headwind due to declining revenue from drugs that are now off patent. For context, in 2018 patent sales were just $1.7 billion, or 3.1% of full-year revenue.

Replacing 3-5% of revenue in a single year is not easy for a company of Pfizer’s size, which is a major reason why the firm is guiding for basically flat sales growth in 2019. Simply put, achieving consistent top line growth is difficult in this industry.

The biggest headwind for Pfizer in 2019 will be the loss of patent protection on blockbuster epilepsy drug Lyrica ($4.6 billion in 2018 sales, or 8.6% of total revenue) in the middle of the year.

According to CEO Albert Bourla, 2020 is also going to be a tough year for Pfizer, again owing to the patent loss on Lyrica. That’s a sentiment shared by CFO D’Amelio who put it bluntly on the firm’s fourth-quarter 2018 conference call saying that Pfizer will “need to work our way through 2020” and that next year will be “a challenging year.”

Mr. Bourla told analysts on the conference call that “the pivotal moment” in terms of a return to positive top and bottom line growth will be “after June-July of 2020”. An inflection point is expected here thanks to the end of Pfizer’s major patent cliff in 2021 and the anticipated launches of new drugs, as well as expanded indications on existing blockbusters.

Of course, such optimism about strong growth in sales and cash flow beyond 2021 is predicated on Pfizer’s pipeline getting approved, and then winning market share. Neither is guaranteed to happen.

What about large acquisitions, which are common in this industry due to high drug development costs and risks of trial failures?

Pfizer’s track record is a mixed bag when it comes to making deals, including its:

- $68 billion acquisition of Wyeth in 2009 to offset the upcoming large patent cliff in 2011, which resulted in a large dividend cut.

- Failed $100 billion acquisition of AstraZeneca in 2014.

- Failed tax inversion deal to acquire Allergan for $160 billion in 2015.

Looking forward, Pfizer’s new CEO told analysts that when it comes to M&A “we never say never, so we are examining all opportunities.” For now, Pfizer is focused on its drug pipeline, and not anticipating major deals. But just remember that at some point Pfizer will buy another company again, and acquisitions carry numerous risks.

Companies frequently overpay for assets, use too much debt to buy a prized business, and struggle to mesh different corporate cultures. Factor in the uncertainty baked into future drug approvals and peak sales, and pharma M&A is not an easy task.

What’s the risk of Pfizer having to cut its dividend again due to another big acquisition like the Wyeth deal? In fairness to Pfizer, acquiring Wyeth was ultimately a good long-term move because it gave the company Prevnar 13, the company’s best-selling product.

Dividend cuts like the one caused by Pfizer’s Wyeth acquisition are difficult to predict because they have more to do with management’s capital allocation decisions rather than their underlying payout ratios, business fundamentals, and balance sheet.

That being said, back in 2009 Pfizer was a smaller and less diversified company. Lipitor is also the best selling drug in the company’s history, racking up nearly $150 billion in revenue between 1996 and 2016. In 2009, Lipitor sales were $11.4 billion and accounted for 23% of total company revenue. Thus the 2011 patent cliff (59% decline in Lipitor revenue in 2012) was a far bigger risk than the one posed by Lyrica today, since that drug represents less than 9% of Pfizer’s overall revenue.

Even though Pfizer isn’t likely to face another 2009-style dividend cut in the future, its business model still faces other risks similar to those of any drugmaker.

Thanks to increasing regulatory hurdles, for example, the cost of bringing new drugs to market has been steadily rising over the decades up to $2 billion to $3 billion for just one medication.

As a result, drugmakers have increasingly turned to joint ventures to help spread the risk/cost of new R&D (now about $800 million per drug per company according to Morningstar).

The pharma industry faces never-ending regulatory risk as well since high drug prices are a favorite punching bag for politicians on both sides of the aisle.

In fact, on January 31, 2019, the Department of Health and Human Services, per the request of the Trump Administration, proposed a new rule that could potentially ban (or at least severely limit) drug rebates to pharmacy benefit managers, Part D plans and Medicaid managed care organizations.

Drugmakers have used such rebates, including bundles of them for several drugs, to maintain market share and minimize how fast drug sales fall when a medication loses patent protection. If this rule change occurs, then it could make steadier top and bottom line growth harder for all pharma companies.

Congress could always try to amend current laws that prohibit Medicare and Medicaid from negotiating bulk drug purchases, putting downward pressure on drug costs.

The risk of bulk government drug purchases would spike if the proposed “Medicare-for-all” ever becomes reality.

That single-payer idea, in which Medicare would effectively cover all Americans, was proposed by Bernie Sanders during his run for president in 2016 but has become adopted by almost all 2020 Democratic Presidential hopefuls.

Of course, given the complexity and expense of that legislation (healthcare is about 20% of the U.S. economy), there isn’t a big risk of single-payer healthcare actually happening anytime soon. However, the point is that any dividend investor interested in healthcare companies, but especially drugmakers, needs to keep various regulatory risks in mind.

Closing Thoughts on Pfizer

The pharma industry’s complexity is enough to scare off many conservative investors, and rightly so. From industry pricing concerns to patent cliffs and blockbuster flops, there is no shortage of murky issues that can cause surprises.

With that said, Pfizer is one of the few companies that seems worth considering for income in this space. It appears that the worst of its drug-exclusivity losses will be behind it starting in mid-2020, and the company’s portfolio of medicines is nicely diversified. Pfizer’s drug pipeline offers a lot of potential across many different therapeutic areas, and its balance sheet remains in great shape, minimizing the risk of another 2009-style dividend cut ever being necessary.

All in all, Pfizer appears to be recovering well from the 2011 patent cliff by investing significant capital in R&D and acquisitions to rebuild its pipeline. With its diversified drug pipeline drawing closer to delivering meaningful results, the business has strong potential to return to stronger organic growth after years of struggling.

While Pfizer may have its challenges, as do all drugmakers, ultimately the company looks like an above-average choice with a well-covered dividend in a highly defensive sector.

— Brian Bollinger

Simply Safe Dividends provides a monthly newsletter and a comprehensive, easy-to-use suite of online research tools to help dividend investors increase current income, make better investment decisions, and avoid risk. Whether you are looking to find safe dividend stocks for retirement, track your dividend portfolio’s income, or receive guidance on potential stocks to buy, Simply Safe Dividends has you covered. Our service is rooted in integrity and filled with objective analysis. We are your one-stop shop for safe dividend investing. Brian Bollinger, CPA, runs Simply Safe Dividends and previously worked as an equity research analyst at a multibillion-dollar investment firm. Check us out today, with your free 10-day trial (no credit card required).

Source: Simply Safe Dividends