What a year it’s been for oil!

Oil Takes Off

With a 43.5% climb in just a year, oil prices have blown by several technical levels to breach $70, and $80 is on the table by the end of the year.

With a 43.5% climb in just a year, oil prices have blown by several technical levels to breach $70, and $80 is on the table by the end of the year.

This is the highest price since 2014, and it’s a very good sign for stocks—which is why you should consider buying 2 funds paying massive dividends and boasting top-notch energy-sector exposure.

Before I show you my 2 energy funds, though, let’s talk a bit about what isn’t happening with oil.

First, oil is nowhere near the $100 range it maintained in the early 2010s.

And since the economy is much stronger now than it was back then, we know that oil can easily get back to that $100 range without being a big drain on consumer spending.

That alone is a great reason to bet on oil.

You can see this in the fact that even though gas prices are high these days, we’re not seeing a huge uproar from consumers.

Of course, some people are grumbling, but it isn’t the kind of nationwide upset we saw in 2010 and 2011, when a mix of higher gas prices, high unemployment and stagnant wages crushed demand and squeezed American families.

Gas Climbing—But Not Peaking Yet

In part, rising wages and higher inflation outside of oil are causing Americans to be less shocked by gas prices. And while that may change, it isn’t changing now, which means demand for gas (and thus oil) is by no means going to slow down.

In part, rising wages and higher inflation outside of oil are causing Americans to be less shocked by gas prices. And while that may change, it isn’t changing now, which means demand for gas (and thus oil) is by no means going to slow down.

And that’s why energy stocks are a terrific place for you to invest right now.

The Opportunity

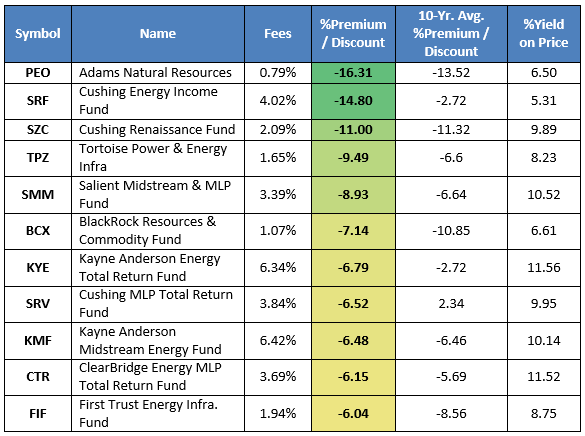

Of the over 40 energy closed-end funds (CEFs) out there, 25 boast discounts to their net asset values (NAVs) and 11 have huge markdowns (wider than 5%).

Here they are:

Out of all these CEFs, several are appealing, for different reasons.

Out of all these CEFs, several are appealing, for different reasons.

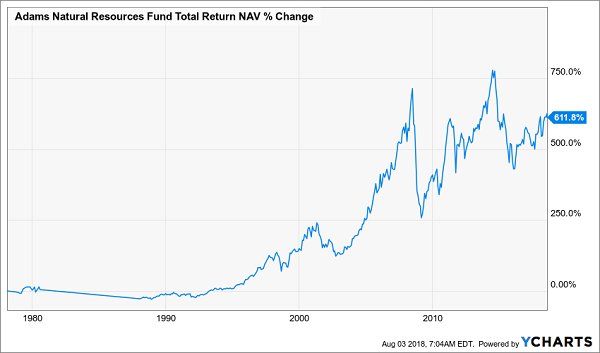

Take the first one I want to tell you about today: the 6.5%-yielding Adams Natural Resources Fund (PEO), which has the widest discount of all these CEFs and is also one of the oldest energy funds, with a tremendous long-term total return:

PEO Has a Great History

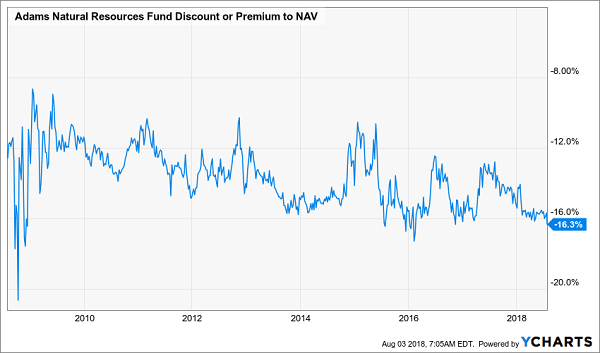

But over the last decade, this fund has traded at about a 13.5% discount to NAV, which isn’t much different from its current pricing.

But over the last decade, this fund has traded at about a 13.5% discount to NAV, which isn’t much different from its current pricing.

That means the discount probably won’t close completely anytime soon. But it will likely get smaller—enough to bring the price up by around 7.1% from today’s levels, since the discount was around 10% just three years ago (and that doesn’t include any additional upside from oil’s continued rise):

Smaller Discount—and Upside—on the Way

Since PEO’s discount has been widening lately, this could be a great contrarian play for short-term gains.

Since PEO’s discount has been widening lately, this could be a great contrarian play for short-term gains.

That brings me to my second pick—the Cushing Energy Income Fund (SRF), which is also one of the most expensive energy funds out there on a fee basis—4% expenses, compared to PEO’s 0.8%. But remember, fees come out of NAV, so you won’t get a bill for management here. Plus, this chart points to huge price upside ahead for SRF:

SRF’s Mispricing Is an Opportunity

While SRF has been benefiting from the improvement in oil prices, the market seems to be ignoring that fact, resulting in SRF’s total NAV return exceeding its total price return by a wide—and growing—margin.

While SRF has been benefiting from the improvement in oil prices, the market seems to be ignoring that fact, resulting in SRF’s total NAV return exceeding its total price return by a wide—and growing—margin.

As a result, SRF’s discount has exploded from its 2.7% average over the last decade to over 14%, despite the tremendous bull run we can expect in energy, thanks to the rise in oil.

In other words, we’re talking 12.8% in capital gains just from the discount closing alone—which you can get on top of SRF’s 5.3% dividends.

— Michael Foster

4 Cash-Loaded CEFs—With Payouts Up to 7.8%—Set to Rip Higher [sponsor]

As I’ve just shown you, a CEF’s discount to NAV is a surefire indicator that it’s on the launch pad for some serious price upside.

And remember that many CEFs pay dividends 3 or 4 TIMES higher than your typical stock—upwards of 8.0%! So you’re getting paid very handsomely while you wait for these funds’ discount windows to slam shut.

Right now, I’ve got 4 CEFs on my radar that are ALL trading at ridiculously wide discounts to NAV. When these absurd discount windows evaporate, we’ll be in line for massive 20%+ upside in the next 12 months.

Here’s a quick look at each of them:

- The real estate mogul: This fund has DOUBLED the market’s return since inception—including during the financial crisis—by investing in real estate, the very thing that caused the meltdown in the first place! It pays you 7.8% in cash today, and its silly discount points to a shockingly big price rise ahead.

- The bond play with a fat 7.2% payout: This one trades at a totally unusual 14.9% discount to NAV. And it has something I love in a CEF: management with skin in the game. The team at the top includes a Wall Street vet with $250,000 of his own cash in the fund, so you can bet he’ll be working for you.

- The perfect buy for rising rates: This one holds floating-rate loans, whose rates adjust higher with interest rates. If you want to hedge your portfolio against the Fed’s next move (and collect 6.4% in cash while you do) this fund is for you.

- The preferred-stock player: Preferred stocks trade around a par value, like a bond, but pay outsized dividends, fueling this fund’s amazing 6.9% payout. Better yet, preferreds have gone on sale in the last few months, driving this fund to a rare discount—and giving us our in.

I can’t wait to show you all 4 of these high-powered CEFs close up. All you have to do is CLICK HERE to get the full story (names, tickers, buy-under prices and everything you need to know) right now!

Source: Contrarian Outlook