When planning for retirement, most investors try to split their assets between stocks (higher risk, higher return) and federal U.S. government bonds (lower risk, and these days, much lower return).

Problem is, stocks are enjoying an overextended winning streak. The S&P 500 is up over 7% year-to-date:

S&P 500 Moves Up and To the Right

That’s quite nice, especially after the 1.4% return that the same index had last year. But when we consider its performance in 2014 (13.5%), 2013 (32.2%), and 2012 (15.9%), investors are right to give pause. Has the market outperformed for too many years in a row?

That’s quite nice, especially after the 1.4% return that the same index had last year. But when we consider its performance in 2014 (13.5%), 2013 (32.2%), and 2012 (15.9%), investors are right to give pause. Has the market outperformed for too many years in a row?

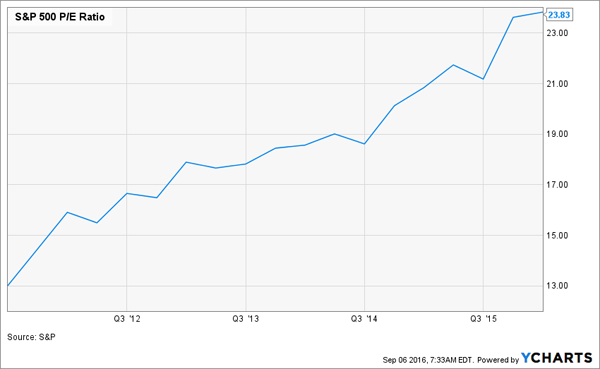

Perhaps. The S&P’s price-to-earnings ratio (P/E ratio) shows that the index is roughly twice as expensive now as it was 5 years ago:

Earnings at Twice the Price

In fact, the S&P is roughly 54% more expensive than its historical average. This means that you’re roughly paying 54 cents more for every dollar you put into the stock market to get the same amount of earnings that you would’ve received if you’d invested in the market in the past.

In fact, the S&P is roughly 54% more expensive than its historical average. This means that you’re roughly paying 54 cents more for every dollar you put into the stock market to get the same amount of earnings that you would’ve received if you’d invested in the market in the past.

[ad#Google Adsense 336×280-IA]This is the point where most new investors get terrified and simply run away.

“The market’s too expensive,” they think, and instead put their money in bonds (low yields) or cash (no yields).

Or they invest in real estate (which historically underperforms the stock market by a huge margin).

Any of these options would be a big mistake.

Instead, we need to think more creatively about the stock market. If it’s pricey now, that doesn’t mean we need to avoid stocks—it means we need a new strategy.

First, let’s consider bonds. We will want to buy some long-term U.S. Treasury bonds to diversify and have a cash cushion in case the stock market falls (in which case we’ll rebalance our Treasuries into stocks). To do this, we can buy the iShares Barclays 20+ Year Treasury Bond ETF (TLT), which currently pays a 2.2% dividend.

We can juice our income even more and diversify away from stocks by buying junk bonds. One way to do this is to get the iShares iBoxx High Yield Corporate Bond Fund (HYG), which is now paying a 5.5% dividend. There are better options than HYG—but I’ll get to that in a moment.

First let me show you how well HYG and TLT have done over the last year—a buy and hold investor saw some turbulence with HYG stabilized by steady growth with TLT:

A 2-Fund Bond Portfolio Trends Up

Even better: The income stream has stayed constant:

Even better: The income stream has stayed constant:

Yields Averaging Almost 4%

But 4% alone won’t get it done – we need to add stocks and their tremendous growth potential. So let’s do what billionaires do and hedge our holdings. We can do this with a fund like the Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV), which has recovered nicely after the big market turmoil earlier this year:

But 4% alone won’t get it done – we need to add stocks and their tremendous growth potential. So let’s do what billionaires do and hedge our holdings. We can do this with a fund like the Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV), which has recovered nicely after the big market turmoil earlier this year:

Buy-Write Still the Right Buy

Note that the fund’s price, besides the big crash, has been pretty stable—between $15.10 and $14.25. That’s a range of just 5.6%.

Note that the fund’s price, besides the big crash, has been pretty stable—between $15.10 and $14.25. That’s a range of just 5.6%.

There are a few fundamental reasons why the fund is so stable. One is that it invests in many of the big stocks of the S&P 500. Its biggest holdings are Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Google (GOOG), Facebook (FB) and Comcast (CMCSA)—the biggest companies renowned for having stable, reliable, durable business models.

But another reason its price is so steady is its hedging strategy.

The fund uses a covered-call strategy that combines owning shares and selling insurance on those shares to other investors in the market. Its insurance sales provide the fund with cash flow on top of its equity holdings.

That brings us to the best part of ETV. The fund’s dividend yield is 8.8%—much more than the corporate bond ETF and nearly 4 times as much as the U.S. government bond fund. And we’re not only getting cash dividends every month—we’re also getting stock exposure and upside in case the rally continues.

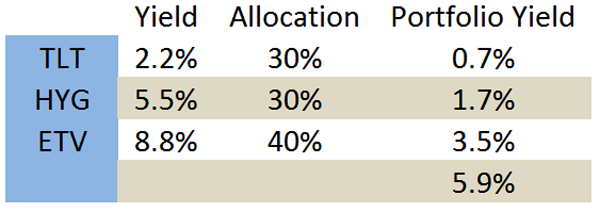

Now let’s talk asset allocations. If we are aggressive and we want 30% bonds and 70% stocks, we might decide on splitting that 70% between HYG and ETV, putting 40% in ETV and 30% in HYG. Combine that with our 30% in TLT, we get a portfolio yielding 5.9%:

Keep in mind that this is a portfolio that limits our stock exposure and keeps some cash available for rebalancing. Our stock holdings essentially are partly insured. This is a high income stream for such a diversified, secure portfolio that includes U.S. Treasuries.

Keep in mind that this is a portfolio that limits our stock exposure and keeps some cash available for rebalancing. Our stock holdings essentially are partly insured. This is a high income stream for such a diversified, secure portfolio that includes U.S. Treasuries.

But it still isn’t ideal. My main concern is with HYG. Like SPY, this ETF essentially mimics an index to provide a return that largely correlates with the market as a whole. With corporate bond defaults skyrocketing, HYG is higher risk than some other actively managed funds.

— Brett Owens

Sponsored Link: I’d personally replace HYG with three “hidden gem” bond funds are trading at a steep discount to their net asset value. There’s a reason billionaire investor Bond God Jeffrey Gundlach has been so high on these types of issues, even while he is bearish on the market as a whole. They pay 8%, with upside thanks to their discount – and they are uncorrelated from the market at large.

What’s even better—you and I are actually better suited to buy these funds than Gundlach himself, because we don’t have to deploy $80+ billion!

Worse case, he said a few months back, these investments will trade flat and we’ll collect a fat 8-11% dividend. Best case, they’ll add 20% in price appreciation. Put the two together and we’re talking about gains of 8-31% over the next twelve months!

His usually prescient advice is looking dead-on once again, as these funds are already starting to tick up. So I wouldn’t waste any time moving on this tip from the top fixed income guru on the planet – I’d buy these three issues today. Click here and I’ll share [more information] and buy prices for these “slam dunk” income plays.

Source: Contrarian Outlook