[Recently], I told you about the best way to invest in the natural resource sector.

Instead of mining metals or producing oil or natural gas, royalty companies generate cash by earning revenue streams on the production of natural resources.

[ad#Google Adsense 336×280-IA]This business model means royalty companies don’t have the same risks and expenses producers have.

Because they don’t spend money to explore or produce, royalty companies are also shielded from swings in the prices of commodities… and they generate massive profit margins.

In short, royalty companies allow investors to participate in the natural resource sector with far less risk than buying producers and they have big upside potential.

To show you just how powerful the royalty model is, let’s take a look at the oil sector…

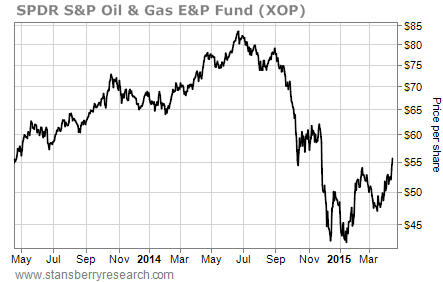

As regular Growth Stock Wire readers know, the price of oil has tumbled over the past few months. The benchmark West Texas Intermediate (WTI) crude oil price fell 60% from July 2014 to March 2015.

With the big drop in the price of oil, it was impossible for most producers to earn profits. And their share prices suffered. The SPDR S&P Oil & Gas Exploration & Production Fund (XOP), which holds shares of exploration and production companies, fell 49% from its June 2014 high to its January 2015 low.

Thanks to a modest recent rally, XOP is now trading for around the same price it was two years ago. That means investors who bought the stock in April 2013 and held it have made 0% on their investment.

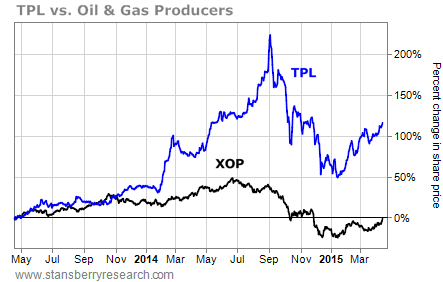

But there’s one oil stock that has soared over the past two years… even with the oil-price collapse.

I’m talking about Texas Pacific Land Trust (TPL). TPL is an oil and gas royalty trust. So it doesn’t drill wells or look for new fields. Its main job is to collect income from its oil and gas properties.

The trust owns about 889,000 acres of land in West Texas (including in the Permian Basin). It owns the mineral rights to 459,000 of those acres. The trust receives a 6% royalty on any oil and gas production on most of those 459,000 acres.

Because TPL doesn’t have to explore and drill, it has almost zero expenses. Besides income taxes, TPL’s expenses are just 6% of its total revenue. So the company has a massive profit margin. In 2014, its profit margin was 63%. For comparison, two big shale producers – Devon Energy and Chesapeake Energy – had 9% profit margins. Both companies work extensively in the Permian Basin. But the cost of drilling those wells, falling oil prices, and expensive leases eat up the profits.

That’s why collecting royalties is such a better business model. And it has allowed TPL to head higher over the past two years – despite recent low oil prices. As you can see in the chart below, TPL has easily outperformed oil and gas producers.

In short, $1 invested in XOP two years ago is worth $1 today. However, $1 invested in Texas Pacific Land Trust two years ago is worth about $2.12 today. That’s a 112% gain compared with 0% for oil and gas producers.

So even with the oil-price decline, TPL has doubled investors’ money. And when oil prices eventually rebound, TPL shares should perform even better.

That’s why royalty companies are by far the best way to invest in natural resources. If you’re looking to invest in the oil sector – or any natural resource sector – start with royalty stocks.

Good investing,

Matt Badiali

[ad#stansberry-ps]

Source: Growth Stock Wire