Closed-end funds (CEFs) are ready to climb after a two-month decline. In preparation for this pop, select vanilla investors are buying this 11.1% dividend with its 14% downside.

Wait, what?!

Everyone hates bonds today. Yet, somehow, these bonds are selling for $1.14 on the dollar.

I sure wouldn’t do it. I’d favor the fixed income that everyone hates. (More on these discounted dividends in a moment.)

Who is this “I’ll pay a premium” belle of the basic income ball? Convertible bonds. Convertibles pay regular interest. In this way, they act like bonds. You buy them and “lock in” regular coupon payments.

But convertibles are also like stock options in that they can be “converted” from a bond to a share of stock by the holder. So, you can think of them as bonds with some stock-like upside.

You may think few people are paying up for equity upside today. If so, well, you’d be mistaken. Fear dominates the financial markets today, but convertibles are (for whatever reason) still drawing quite the crowd!

Let’s start with the SPDR Barclays Capital Convertible Bond ETF (CWB), the most popular mainstream (read: widely marketed) vehicle to purchase convertibles. CWB yields just 2.2%, but many investors and money managers choose it because it’s easy.

But that 2.2% really insults true convertible connoisseurs. So, these guys and gals are piling into the closed-end fund (CEF) Calamos Convertible and High Income Fund (CHY). CHY has a headline yield of 11.1% and also boasts “convertible” in its name, so why not!

This dividend “alpha” over CWB, however, is about all we have on the resume. CHY and CWB have performed in-line over the past 10 years, so they’re the same, right?

Unfortunately, no. Not today, at least. CHY is fetching a 14% premium to the value of its underlying holdings. Investors are paying $1.14 for a dollar of its convertibles (while CWB buyers pay only $1).

It wasn’t always this way. Just three years ago, we discussed CHY because it was trading at an 11% discount to its net asset value (NAV). It was selling for just 89 cents on the dollar!

That was a good deal. Over the next year, CHY soared by 54% including dividends. Reminding us contrarians, once again, why we always demand discounts.

With CHY trading at a premium, it’s now poised to underperform. Avoid.

A better bet is Nuveen AMT-Free Municipal Credit (NVG). Next to US Treasuries, muni bonds are the safest bonds in America. And lately, munis have been comparative darlings! No debt drama for these boring payers.

When it comes to bonds, boring is good.

Munis are usually so mundane and reliable that they rarely go on sale. And here’s a great thing about municipalities, at least for us investors: when they need money, they issue bonds. The writers of muni bonds are not interest rate sensitive.

(Taxpayers, cover your ears!)

Which means muni funds are the place to be right now. Or at least soon. But you wouldn’t know it from their valuations. In contrast to convertible-powered CHY, boring ‘ol NVG trades at a 16% discount to its NAV today.

A 16% Discount Window, Wide Open

Yup! This well-run muni fund is on sale for 84 cents on the dollar. Buy the stock for under $10, receive $1.85 in NAV for free.

Yup! This well-run muni fund is on sale for 84 cents on the dollar. Buy the stock for under $10, receive $1.85 in NAV for free.

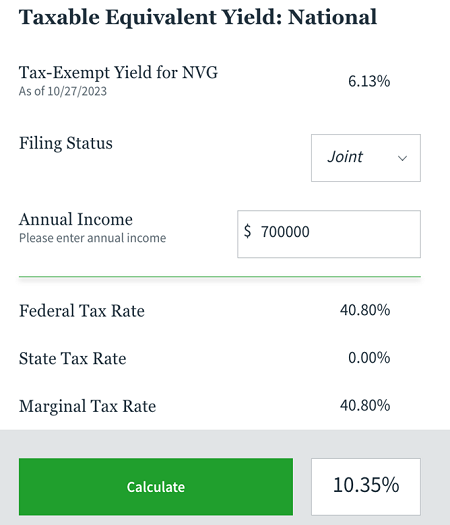

And oh by the way, the fund just raised its monthly payout by 19%! The fund dishes 6.1% and on a tax-exempt basis—they are tax exempt, remember—it’s even better. For my top tax-bracket ballers, this is a tax equivalent yield of nearly 10.4%:

Meanwhile, this tax-advantaged dividend comes with not one but two margins of safety:

Meanwhile, this tax-advantaged dividend comes with not one but two margins of safety:

The 16% markdown. As this discount narrows, the fund will enjoy price upside.

Plus, NAV gains are likely when interest rates settle down.

Yes, NVG is positioned to be a special taxpayer trifecta. The US economy is slowing down en route to an eventual recession. Which means long rates will eventually trend lower.

That move will push cheap munis like these much higher. Not bad for supposedly boring bonds! It’s a great time to hop aboard the slow, steady and dirt-cheap muni train—before our income friends park their high-flying, overpriced convertibles and head this way.

— Brett Owens

Don’t Miss Your Chance to Lock in “Forever” 10%+ Payouts Now. Here’s How. [sponsor]

In just a few months, we’ll likely look back at this pullback and realize it was a once-in-a-generation chance to “lock in” huge dividend yields at massive bargains.

Imagine booking yourself a 10% payout essentially forever! That’s what’s on the table here. And when Treasury yields (inevitably) decline, stocks (and CEFs) will soar, driving their dividend yields down. By then it will be too late!

That’s why I’m inviting you to try my CEF Insider service for 60 days. As I write this, our portfolio yields a stout 9.8%, with many funds paying much more. This powerful income portfolio gives you instant diversification, too, with CEFs holding corporate bonds, US stocks, international stocks, real estate investment trusts and more.

Simply click here and I’ll share my full CEF-investing strategy with you and give you the opportunity to download a free Special Report naming my top 4 CEFs to buy now. Plus you’ll get your chance to kick off your no-risk 60-day trial to CEF Insider, too.

Source: Contrarian Outlook