This entire market meltdown has been based off of a flawed premise. We income investors must take advantage of it, before sanity returns to the markets.

The 10-year Treasury yield soared above 5%. On its journey to the stars the higher 10-year has clipped equities severely along the way. A high benchmark rate upsets every applecart in finance.

But here’s the thing. This is not a sustainable move.

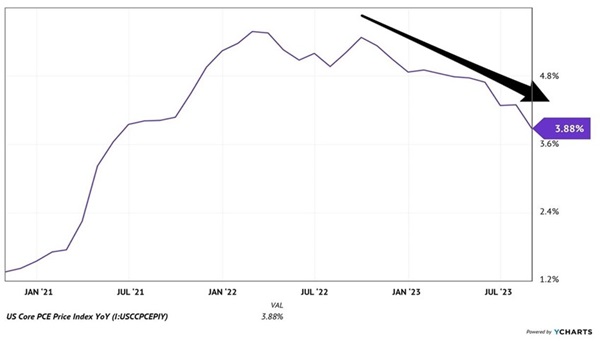

Inflation isn’t really in a spiral higher. In fact, it’s the opposite. Core PCE (personal consumer expenditures)—the Federal Reserve’s preferred measure of inflation—is dropping like a rock:

Fed’s Preferred Inflation Measure is Dropping Fast

Note, this excludes food and energy prices. Which, some argue, is not appropriate because oil prices are high again.

Note, this excludes food and energy prices. Which, some argue, is not appropriate because oil prices are high again.

I’ve been an oil bull for years now—and I disagree that high oil is worrisome for inflation. Future inflation, that is.

High oil prices are a tax on the consumer. Yes, another drag on the economy, as are high interest rates.

High crude slows the economy. It likely already has. And the Fed’s rate hiking mission will bring a recession.

Then, when the economy slows, Jay Powell’s Fed will ease rates.

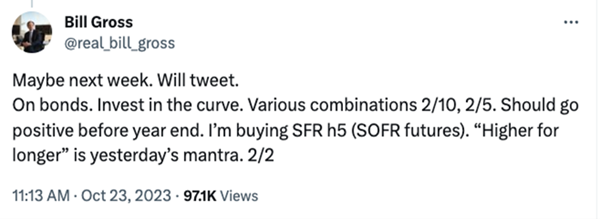

The “Bond King,” Bill Gross, agrees:

So do more bond market participants. They are seeing what we’ve been saying… that this move to 5% is overdone.

So do more bond market participants. They are seeing what we’ve been saying… that this move to 5% is overdone.

The 10-Year Yield Finally Reverses Lower

Source: Google Finance

Source: Google Finance

If rates drop, what does that mean for rate-sensitive stocks?

It means they’ll rip off of their lows.

The first potential ripper yields 12.2%. That’s right—we’ll collect a twelve-point-two percent payout while we watch this fund pop as rates ease!

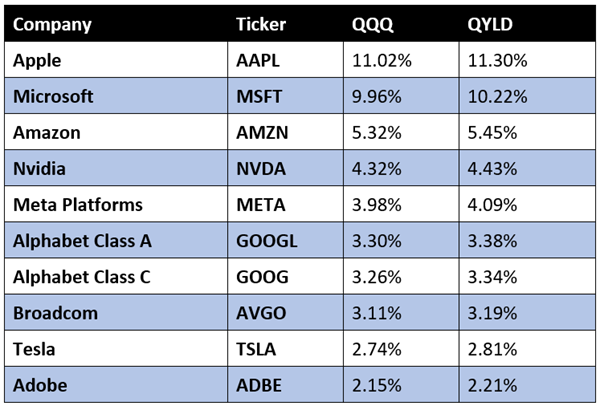

Global X Nasdaq 100 Covered Call ETF (QYLD)

Dividend Yield: 12.2%

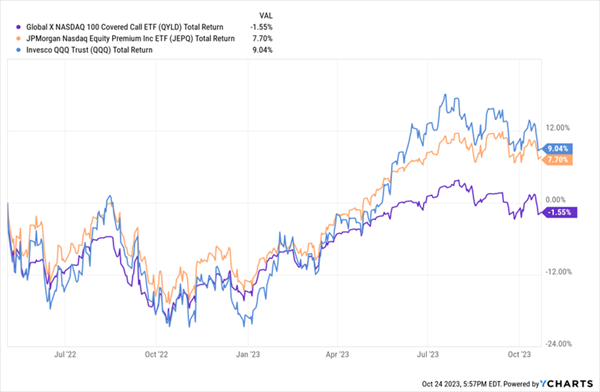

Technology stocks are particularly attractive plays here because they act like “long duration” assets. When rates rise, tech drops. We’ve seen that over the past two years as the QQQs sank lower and lower.

But a top in rates means a potential bottom in tech stocks. At least for a period of time here. Here we’ll focus on the dividend payers because, well, why not double dip our gains with some big yields.

Among alternative-style ETFs, the Global X Nasdaq 100 Covered Call ETF (QYLD) is one of the oldest—it will celebrate its 10th birthday this December.

The Global X Nasdaq 100 Covered Call ETF is an index fund that does exactly what the name suggests:

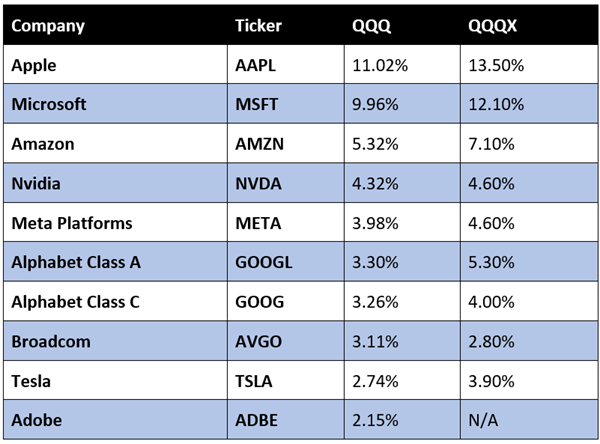

First, it buys all of the stocks in the technology-heavy Nasdaq-100 Index (in roughly the same weights they enjoy in the index). Indeed, the top 10 holdings exemplifies how similar its equity holdings are to the Invesco QQQ (QQQ).

Of course, Apple (AAPL) yields a mere 0.6%, while Microsoft (MSFT) isn’t much better, at 1%. So how is QYLD throwing off all that income?

Of course, Apple (AAPL) yields a mere 0.6%, while Microsoft (MSFT) isn’t much better, at 1%. So how is QYLD throwing off all that income?

It creates a “synthetic yield” by selling at-the-money call options on the Nasdaq-100 Index itself.

This kind of strategy is an absolute grind, which is why I don’t recommend sitting around and trying to sell covered calls on 100 stocks all by yourself. And you don’t have to—you can save yourself the time by outsourcing it to Global X.

The idea behind this strategy is to enjoy some of the performance of the Nasdaq-100, but with less volatility and with most of the returns coming from generous monthly distributions. It’ll lag during up markets but protect your backside during downturns.

QYLD: A Smoother Ride

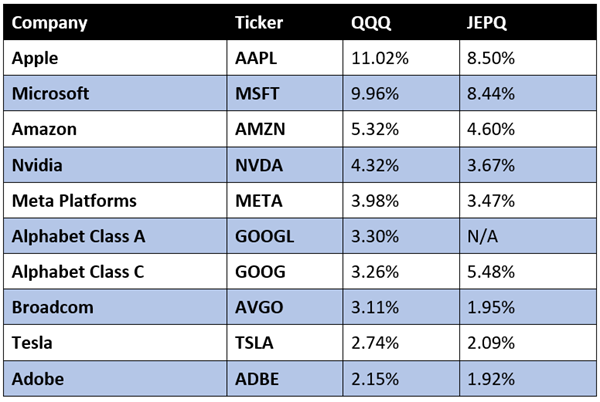

JPMorgan Nasdaq Equity Premium Income ETF (JEPQ)

JPMorgan Nasdaq Equity Premium Income ETF (JEPQ)

Dividend Yield: 11.1%

The JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) is an ETF that has roughly the same thrust as QYLD, but with three meaningful differences.

JEPQ buys Nasdaq-100 stocks, but not all of them—for instance, it only holds one Alphabet (GOOG) share class—and not at the same weights as the QQQ.

While it sells one-month covered calls, it does so with out-of-the-money options.

While it sells one-month covered calls, it does so with out-of-the-money options.

And whereas QYLD is tethered to an index, JEPQ is actively managed (though interestingly, much cheaper, at 0.35% annually versus QYLD’s 0.60%.

The fund has only been around since May 2022, but so far, its results compared to QYLD are promising.

Jamie Dimon’s Managers Are Proving Their Worth

Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX)

Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX)

Dividend Yield: 8.4%

Another actively managed fund with a similar bent is the Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX). The fund also buys Nasdaq-100 stocks, then sells covered calls on 35% to 75% of the notional value of the fund’s equity portfolio.

Again, there are some differences on the long portion of the portfolio:

What makes QQQX stick out is that it’s a closed-end fund, which gives it a significant advantage.

What makes QQQX stick out is that it’s a closed-end fund, which gives it a significant advantage.

One drawback of selling covered calls is that it can weigh on returns over the long haul because the fund’s best performers rise to the option-selling price and get sold, or “called away.” But pushing against that is the fact that QQQX is trading for a significant discount to its net asset value (NAV)—something ETFs don’t do.

Right now, QQQX is trading for an 8%-plus discount, whereas the fund has, on average, traded at a slight premium over the past five years.

What’s also nice is that if volatility continues, the covered-call strategy will make the dividend even safer. That’s because QQQX’s options are likely to expire worthless, letting the fund keep its holdings and the premium it sells option buyers, too.

— Brett Owens

Give Me 4 Minutes, I’ll Show You How to 4X Your Retirement Income [sponsor]

The point behind these covered-call strategies is to reduce portfolio drama and deliver a high, regular income stream.

And if you think that sounds eerily similar to the point of a high-yield retirement portfolio … you’re right!

We want holdings that will let us sleep through existential crises—bear markets, economic slumps, yet another Jerome Powell press conference.

Those are the kind of investments I stash away in my “Perfect Income” portfolio.

My “Perfect Income” portfolio attacks retirement investing from a different angle. Rather than trying to time the market and chase trends, we target high-yield holdings (roughly 4x the S&P!) that walk their own path, no matter what the Fed, Congress or the rest of the world throws their way.

So, what makes these dividends “perfect”? Well, they have to have a few things in common:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Source: Contrarian Outlook