The run in Nvidia (NASDAQ:NVDA) has been stunning, and deservedly so. With NVDA stock up 183% from the March lows, many investors are beginning to wonder just how high this name can go.

That’s a fair question at this point, even from those that have been long. However, investors also need to realize the underlying mechanics of the market.

Understanding Demand

Hindsight is obviously 20/20 right? It’s easy to sit here now at the end of August and pound our chest about being long stocks.

Now that everything has resolved to the upside, it’s easy to be the bull. But understanding the underlying mechanics is necessary to learn for the future.

NVDA stock was a steal below $200 per share. At that time, it was a value play. In the months since though, it was a momentum play.

That’s as large cap tech was clearly in demand. That’s shown by how much faster the Nasdaq hit new highs before the S&P 500. Simply put, there was more demand for tech than other sectors.

That was a plus for Nvidia.

But the other big positive? Nvidia has growth — and not only growth, but accelerating growth. It’s the kind of thing I like to see with the stocks I pick for my 5G Highway Super Portfolio.

Put simply, the pandemic has been good for business. That has made Nvidia among a smaller cohort of stocks that are now growing even faster, while a larger group of stocks have little or negative year-over-year growth.

That creates even more demand for a stock like Nvidia. I have been talking about this concept — that growth stocks accelerating their growth deserve a higher premium — for months now.

So next time, analyze what part of the market is in demand, then what stocks in that group are in even higher demand.

Breaking Down NVDA Stock

When the company reported earnings in May, upside guidance really blew Wall Street away. However, despite elevated expectations coming into the most recent earnings result, Nvidia again delivered.

Earnings and revenue topped expectations, with the latter growing 50% year-over-year. Gross margins also came in ahead of estimates. But on top of all that, management said it expects fiscal third-quarter revenue of $4.4 billion, well ahead of consensus estimates at the time for $3.97 billion in sales.

Friends, there’s no other way to say this: Nvidia’s products are in robust demand. Its data center business just had its best quarter. Gaming — as we know from our prior coverage — has been robust as well. Demand for A.I. and cloud applications is through the roof. Those two catalysts are also what makes it a promising 5G stock to consider.

Nvidia isn’t just a 5G “road builder” like some companies investors like to hype up. It’s going to be a driver on what I call the “5G Highway.” It’s going to lead some of the greatest innovations as we step into a future that brings our biggest sci-fi dreams into reality.

While the Mellanox deal took longer than expected to close, it has immediately added to Nvidia’s business. This is no surprise, as management told us it would be accretive to cash flow, margins and earnings from day one.

Admittedly, some areas of its business are struggling as the sectors that it caters too — for instance, automotive — are in a tough spot due to the novel coronavirus. But as a whole, Nvidia’s businesses are booming and thus, NVDA stock has been on fire.

This rally is deserved, even if the stock is getting stretched.

Bottom Line on Nvidia

Some investors are becoming concerned about the move, asking “just how far can Nvidia go?”

Some investors are becoming concerned about the move, asking “just how far can Nvidia go?”

While the valuation is becoming stretched — now at 46 times next year’s earnings estimates — realize that price-to-earnings ratios are not the all-encompassing deciding factor in the stock market.

Otherwise, this latest rally in the market would have never occurred. Valuation isn’t irrelevant, but there are more factors in play than just that.

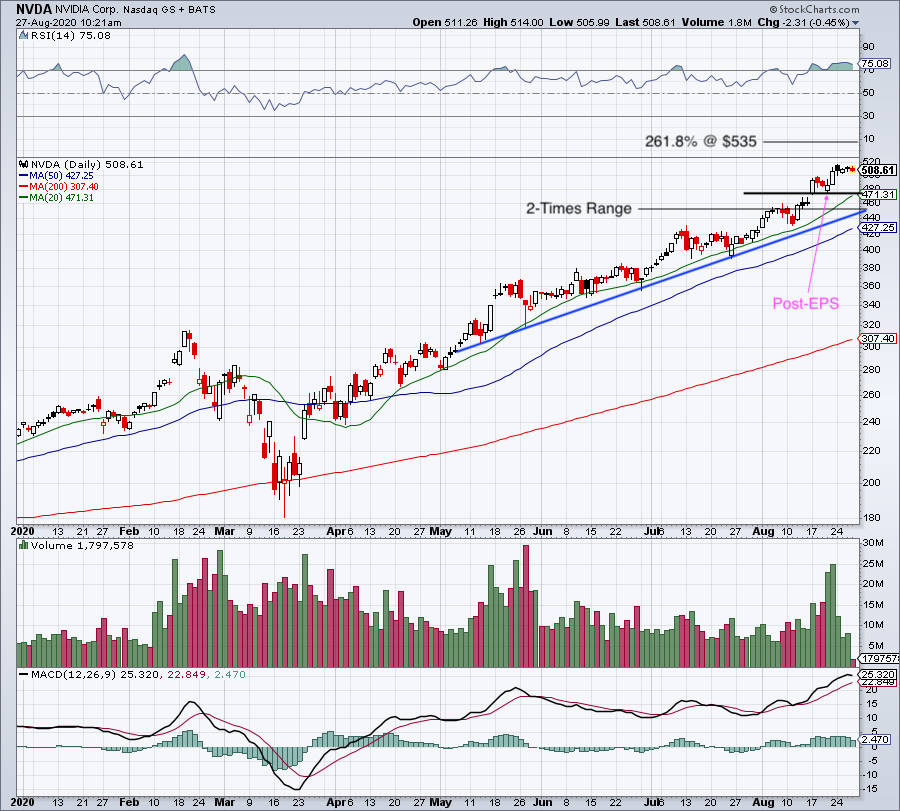

There was clear hesitation by investors after earnings.

Despite a strong quarter, the stock stalled, ending flat on the day after it reported. That said, it only took a day for buyers to come back to NVDA stock. Shares soon cleared $500 and continue to hold above that mark now.

On the upside, look for a rotation over the current high at $516.50. Above that puts the 261.8% extension in play up near $535. Above that mark and shares can again start to push higher. While the run seems extreme, investors have to realize that Nvidia is a backbone in the tech sector. It’s not just a component that can be swapped with others; in many cases it’s a critical pillar that makes it possible.

For this reason, not only does Nvidia stock deserve a premium, but it will also continue to fuel growth. Regardless of what the share price does, NVDA stock has great fundamentals and that will continue to drive this stock higher for the long term.

— Matt McCall

Silicon Valley venture capitalist Luke Lango says this little-known Apple project could be 10X bigger than the iPhone, MacBook, and iPad COMBINED! Investing in Apple today would be a smart move... but he’s discovered a bigger opportunity lying under Wall Street’s radar -one that could give early investors a shot at 40X gains! Click here for more details.

Source: Investor Place