There’s a strong buying opportunity unfolding in an ignored corner of the market right now. Steady dividends of 5.8% (and higher) are waiting for savvy contrarians who jump on it.

And the corner of the market I’m referring to is municipal bonds.

If you’ve been following the muni-bond saga over the last two months, you might find my enthusiasm a bit unfounded.

After all, the coronavirus is hammering the finances of cities and states across the country and driving up the risk of muni-bond defaults—right?

Not so fast.

Your Muni Default Risk? 0.042%

To cut through all the hype surrounding munis these days, we need to zoom out a bit. According to rating-agency Moody’s, over the last 10 years, 0.042% of municipal bonds have defaulted. In other words, you’d have had to own 2,380 municipal bonds before one of them would default, statistically speaking.

I think you’ll agree that this is very safe. By comparison, junk bonds had a 3.3% default rate in 2019, meaning you’d have to own just 30 junk bonds to have a default. That makes them nearly 80 times riskier than munis.

Some investors are willing to tolerate corporate bonds’ higher risk for the yield, however. The benchmark SPDR Barclays Capital High-Yield Bond ETF (JNK) yields 6.1% today, a payout few individual muni bonds can compete with.

But you can get a payout in that range if you buy munis through a closed-end fund (CEF) like the BlackRock Taxable Municipal Bond Trust (BBN). This fund yields just a bit less than JNK, at 5.8%, but more than makes up for that tiny gap by exposing you to much less risk than the junk-bond ETF—while delivering much bigger returns.

If you invested $100,000 in BBN today, you’d collect $483 per month. And check out how BBN has also trounced JNK, with dividends included, since its IPO:

BBN Delivers Bigger Returns and Greater Safety

But are munis still a safe bet if defaults are on the rise? To answer that, let’s do some math.

Muni-Bond Risk Broken Down

If you put $100,000 in a single muni bond and that bond happened to be the one that defaults, you’d be out some cash just for having bad luck. This would be much likelier than the 0.042% default rate for municipal bonds would have you believe, for one simple reason: market access.

Muni bonds aren’t like stocks in that the best ones aren’t offered to everyone at the same time. In fact, the best municipal bonds are usually reserved for banks’ top clients—the companies that manage billions, or even trillions, of dollars. So buying a muni bond on your own means you’ll get whatever those big players passed over.

But if you buy muni bonds through those big players’ CEFs, you’re buying into their ability to choose the best munis on the market. And that’s why I introduced you to BBN above.

This actively managed fund is offered by BlackRock, which has $7 trillion in assets under management. BlackRock is the firm entire countries call, begging it to buy their bonds. And that’s why BlackRock’s funds crush the index.

BlackRock Laps the Muni-Bond Market

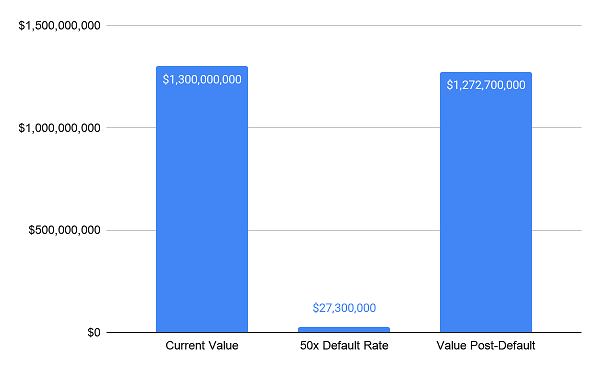

But what if defaults rise by a lot? Not to worry—in such a scenario, you’re still pretty safe.

BBN Would Easily Weather a Default Spike

Source: CEF Insider

Source: CEF Insider

Let’s imagine a world where the muni-bond default rate jumps to 50 times the 2019 rate. This would be unprecedented; such a spike didn’t even happen during the Great Depression. But let’s be really negative and imagine it does this time around.

In that instance, BBN’s portfolio value would fall from $1.3 billion to $1.272 billion. That’s hardly noticeable! Plus, remember that BBN’s active management means it’s far less exposed to the kinds of bonds that are likely to default, which makes an investment in this CEF even safer.

— Michael Foster

Yours Now: 4 Incredible Funds That Crush BBN, Pay You 9.4% [sponsor]

A 5.8% dividend is a very nice income stream to have in your back pocket these days, of course. But that payout doesn’t come close to the tidal wave of cash you get from the 4 high-paying CEFs I’ll show you here.

These 4 stout income plays pay you 9.4% on average—and that’s just the average! You’ll find monster payouts up to 10.8% among this bunch.

Better still, all 4 of these funds are trading at ridiculous discounts. Here’s what that means in a crisis like the one we’re facing now:

- If the market falls from here, these 4 funds should easily outperform: after all, it’s hard for a fund that’s already ridiculously cheap to get a whole lot cheaper!

- If the market regains its footing, these funds are primed to gap higher—and fast!

Either way, we’ll continue to collect our safe (and massive) payouts.

Don’t miss your chance to drastically increase your income stream and set yourself up for massive price gains as the rebound kicks in. Click here for full details on these 4 stout high-income plays: names, tickers, buy-under prices, dividend histories and my complete analysis.

Source: Contrarian Outlook