With insurance coverage and services being somewhat vital in today’s society, Aflac (AFL) and Brown & Brown (BRO) are two insurance stocks that are worthy of investors’ consideration.

After hitting 52-week highs last week both stocks looked poised to keep rising in correlation with the trend of positive earnings estimate revisions.

Recent Performance Overview

Voluntary supplemental and life insurance behemoth Aflac has seen its stock rise +15% for the year while Brown & Brown shares have soared +30% YTD with the company also providing a variety of insurance products including commercial packages, group medical, and workers’ compensation.

Their strong price performances could continue with Aflac’s Zacks Insurance-Accident and Health Industry currently in the top 18% of over 250 Zacks industries while Brown & Brown’s Zacks Insurance-Brokerage Industry is in the top 4%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Attractive EPS Growth

Benefitting from the essentiality and strengthening outlook of their business industries, Aflac and Brown & Brown are experiencing stellar EPS growth this year.

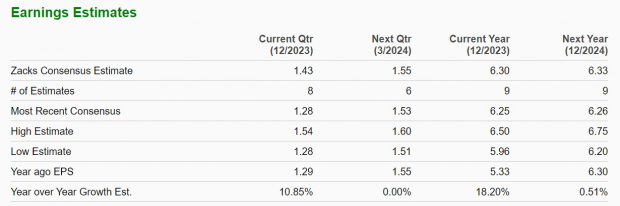

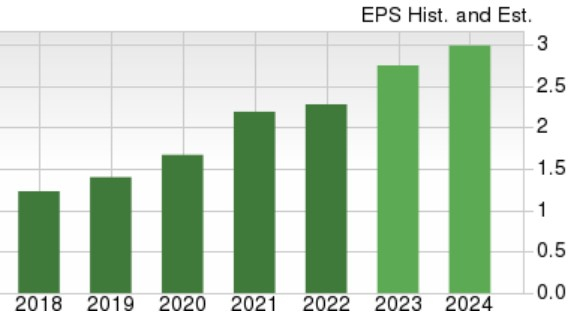

Aflac’s fiscal 2023 earnings are now expected to be up 18% to $6.30 per share compared to $5.33 a share last year. Fiscal 2024 earnings are projected to slightly edge up to $6.33 per share and this would represent 27% EPS growth over the last five years with earnings at $4.96 a share in 2020.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Turning to Brown & Brown, annual earnings are forecasted to climb 21% this year to $2.76 per share versus $2.28 a share in 2022. Plus, FY24 earnings are projected to jump another 9% to $3.02 per share and this would be an 80% increase over the last five years with 2020 earnings at $1.67 a share.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Reasonable P/E Valuations

In regards to their P/E valuations, Aflac trades at a very reasonable 13.1X forward earnings multiple and near the Zacks Insurance-Accident and Health Industry’s 11.1X. Furthermore, Aflac is one of the leaders in its space and trades at an attractive discount to the S&P 500’s 21.3X.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

While Brown & Brown trades above the benchmark at 26.9X forward earnings, this is not a stretched premium considering the company’s expansive bottom line as it is also near its own industry average of 22.7X.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Bottom Line

Over the last 60 days, annual earnings estimates have continued to rise for both Aflac’s and Brown & Brown’s fiscal 2023 and FY24. In correlation with such they share the commonality of a Zacks Rank #2 (Buy). The trend of positive earnings estimate revisions is also supportive of their reasonable P/E valuations and as these two insurance companies benefit from strong business industries their stocks may be in store for higher highs in December.

— Shaun Pruitt

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks