If you always wanted a free lunch but thought they don’t exist, well, they kind of do, in the form of the Fidelity group of ZERO index funds, like the Fidelity ZERO Total Market Index Fund (FZROX).

After all, its 0% fees mean it should easily beat a closed-end fund (CEF) with a high expense ratio, right? Well, not so fast.

0% Fees Do Not Equal Outperformance

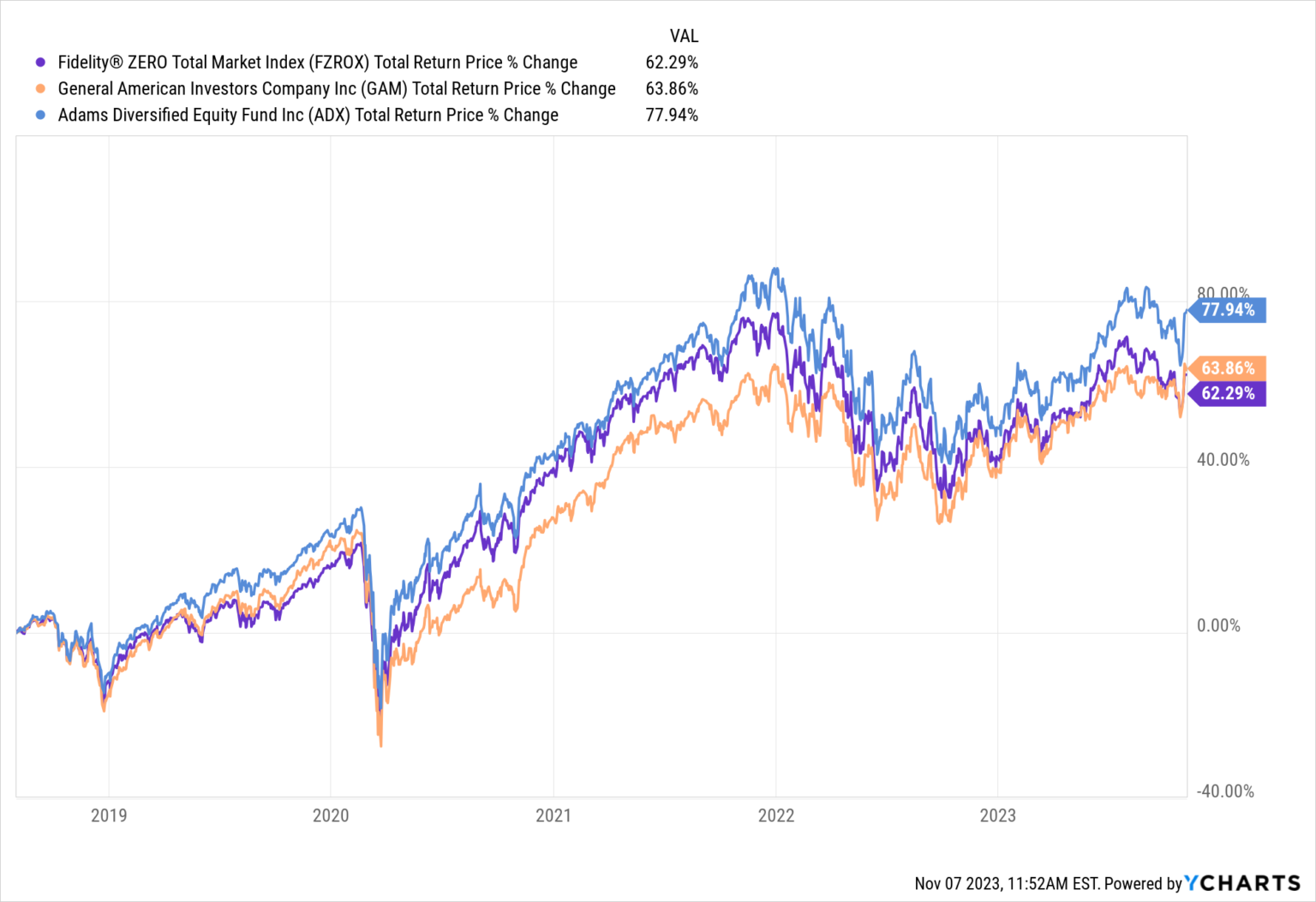

FZROX—in purple above—may levy no management fee, but it’s underperformed many equity CEFs over a long period. Since inception, it’s trailed the Adams Diversified Equity Fund (ADX), in blue, and the General American Investors Co. (GAM) fund, in orange, in total returns.

FZROX—in purple above—may levy no management fee, but it’s underperformed many equity CEFs over a long period. Since inception, it’s trailed the Adams Diversified Equity Fund (ADX), in blue, and the General American Investors Co. (GAM) fund, in orange, in total returns.

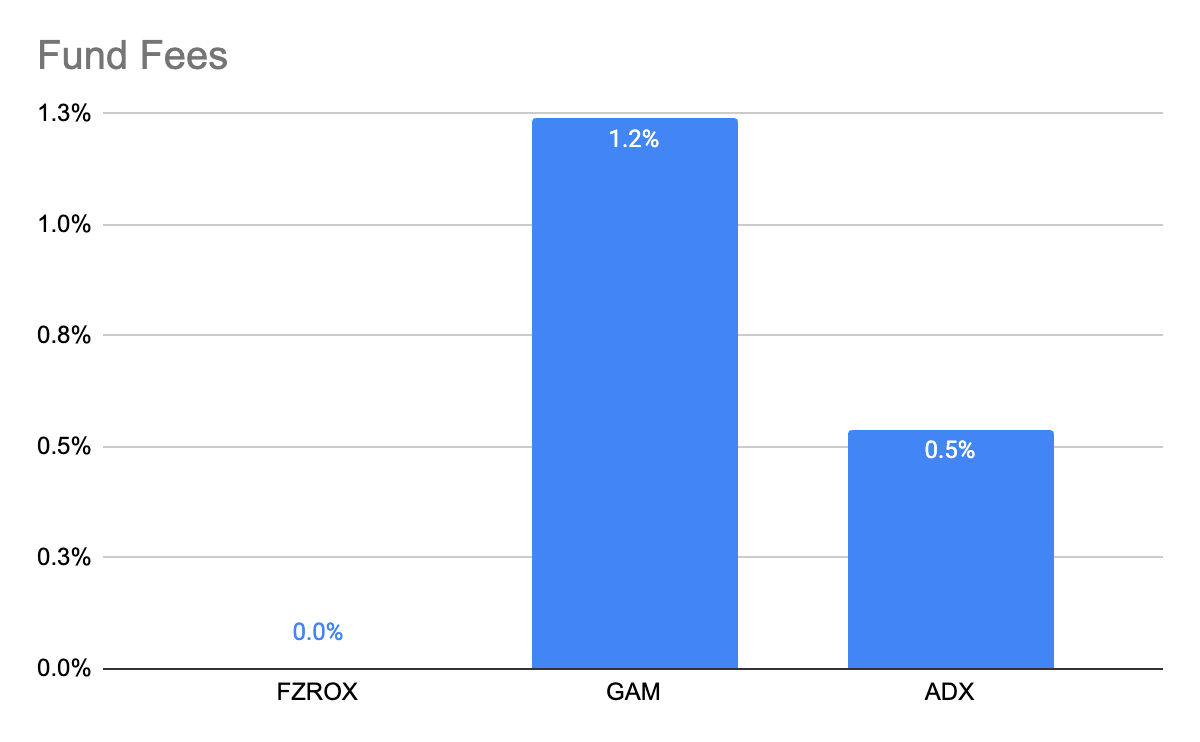

Meantime, that duo yielded about 8% each, versus FZROX’s 1.2%.That’s despite much bigger management fees at ADX and GAM.

Source: CEF Insider

Source: CEF Insider

These aren’t even the most expensive CEFs on a fee basis. But since these fees are taken out of the fund periodically as managers invest their capital (no, you don’t have to send a check to your CEF to pay the fee), the fees don’t really matter if the fund is providing a larger total return than the free fund. And it is.

That’s not the only reason CEF managers earn their higher fund fees. There’s also the income issue.

CEFs = More Income

Source: CEF Insider

Source: CEF Insider

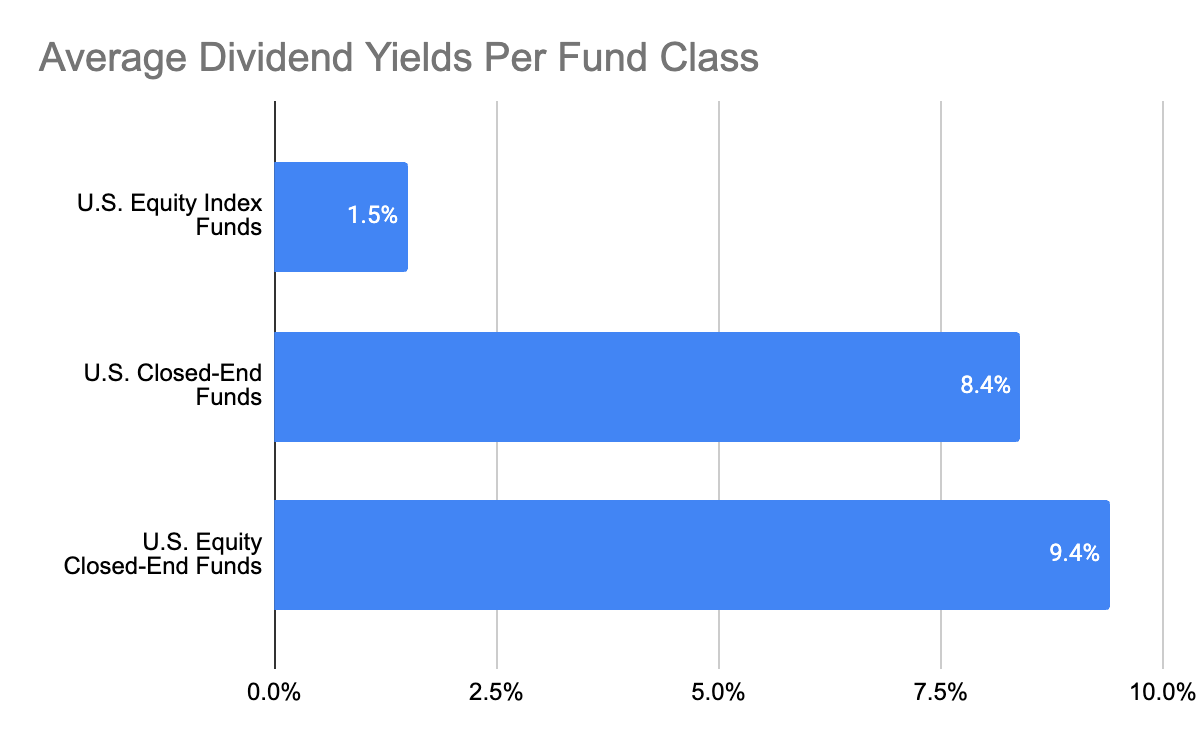

CEFs are perhaps best known for their bond funds, which assemble a portfolio of bonds and hand the income it generates over to investors. But many are surprised to find that, actually, equity CEFs yield more on average: 9.4%, as the chart above shows.

That’s $783 a month in income on average per $100k invested. For equity index funds, that same investment yields a puny $125 a month, over six times less!

But aren’t high yields unsustainable? Many of us have been told that, and it’s true for a lot of assets, but not CEFs. Here’s why.

How CEF Managers Earn Their Fees

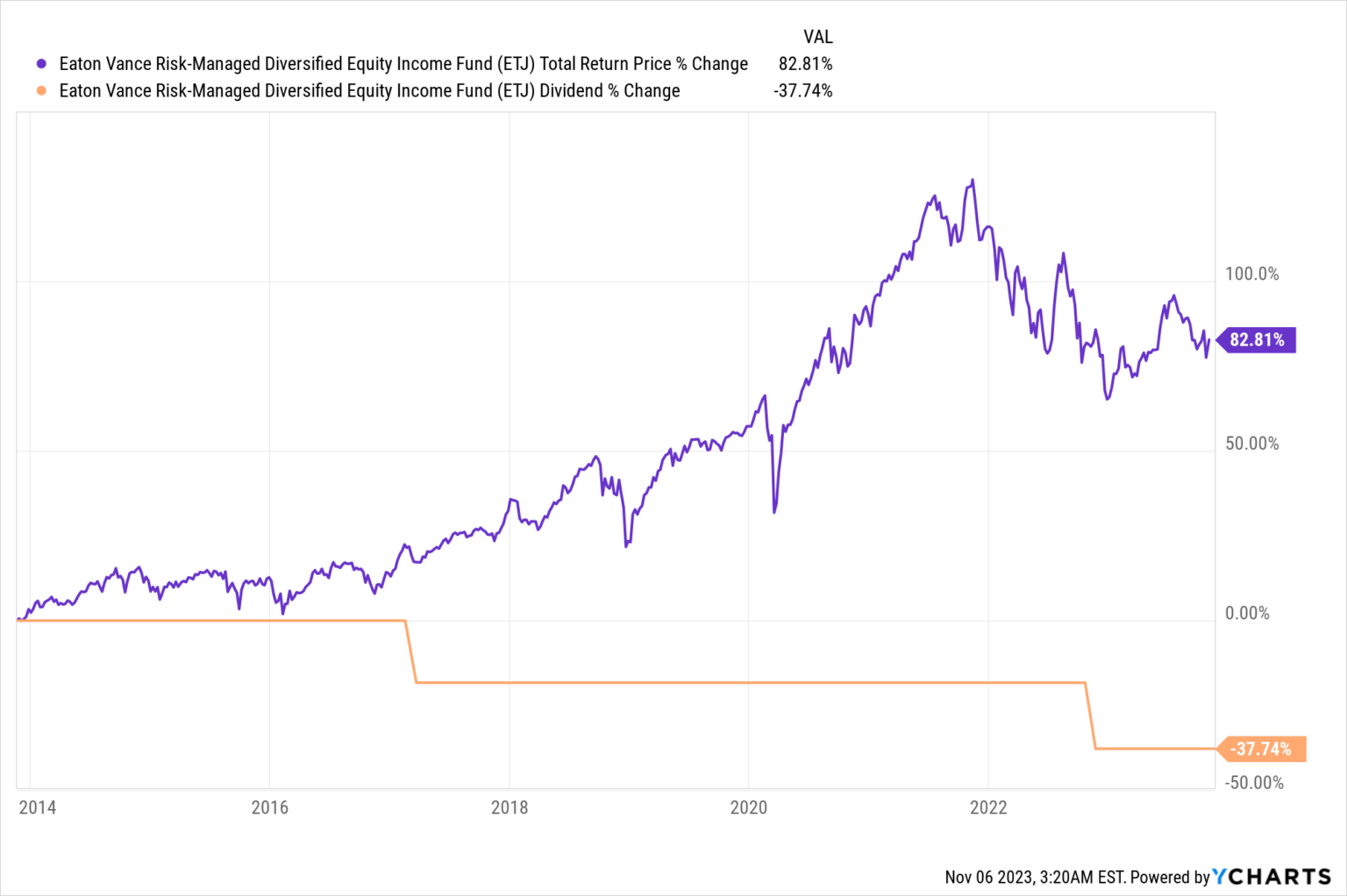

For an example, let’s take the Eaton Vance Risk-Managed Diversified Equity Income Fund (ETJ), a 9%-yielding equity fund that holds the usual suspects: Microsoft (MSFT), Apple (AAPL) and Amazon (AMZN) are its top three holdings, with Eli Lilly (LLY), Walmart (WMT) and Caterpillar (CAT) also being top-20 positions.

ETJ’s Profit and Income Story

ETJ wasn’t the greatest fund then (or now), but even it got investors big profits and an 8.4% yield for a decade. Not just any decade, either, but the 2010s, when interest rates were near zero for years!

ETJ wasn’t the greatest fund then (or now), but even it got investors big profits and an 8.4% yield for a decade. Not just any decade, either, but the 2010s, when interest rates were near zero for years!

This is what CEF investors pay those fund fees for: fund managers have the responsibility to maintain payouts as best as possible while not letting the fund’s net asset value (NAV) fall, not lowering distributions, and providing a big total return. ETJ didn’t succeed—it cut dividends twice—but that means this “failure” of a fund still yielded 8.4% over 10 years and got investors an 82.8% total return at the same time! All the while, ETJ was charging about a 1.12% fund fee per year.

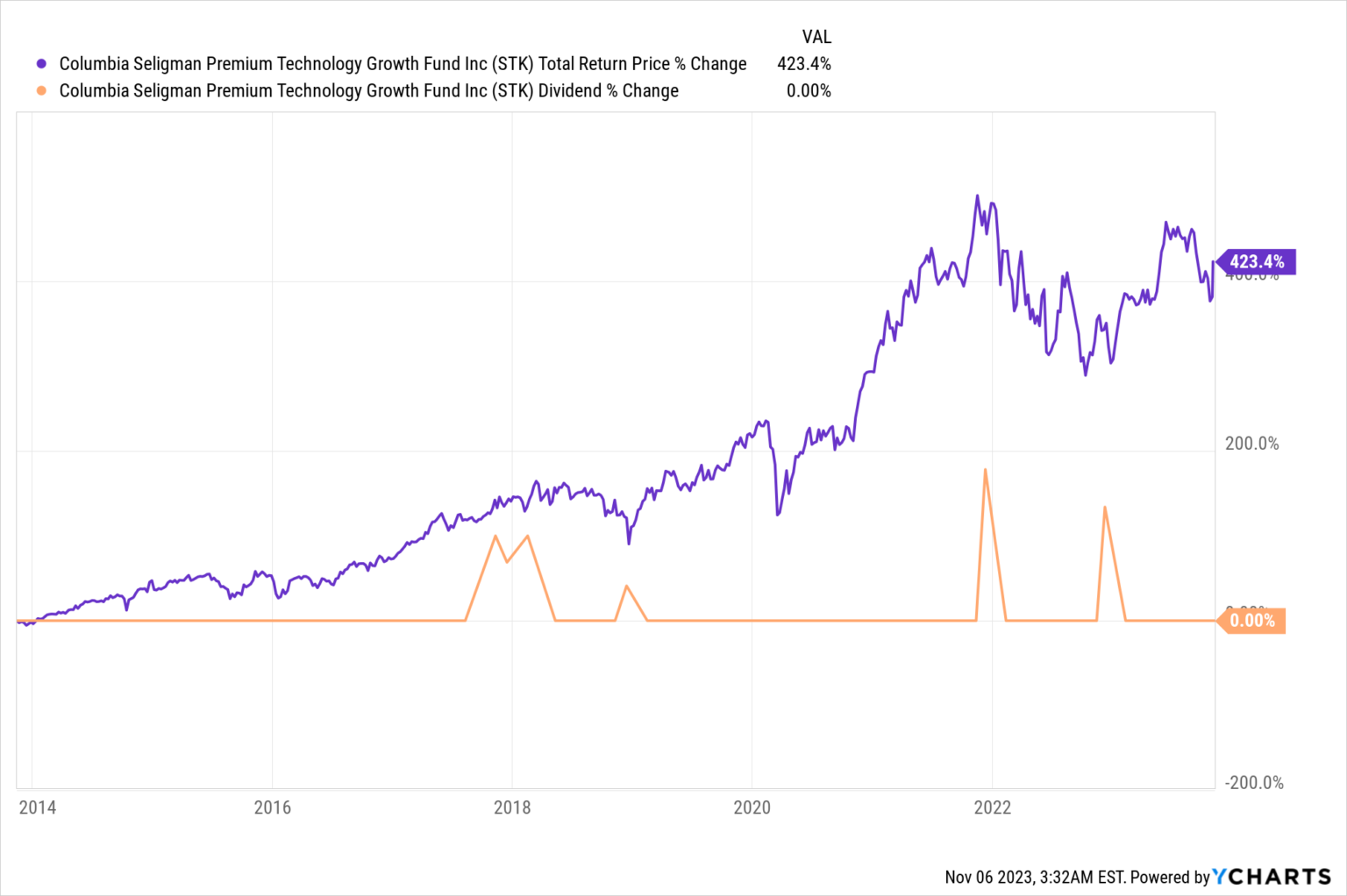

Want more profits and no dividend cuts? Well, CEF investors got that from the Columbia Seligman Premium Technology Growth Fund (STK), whose 1.13% fund fee is nearly identical to that of ETG, but whose returns are much better.

Don’t ignore that orange line: those are the dividends, which remained unchanged throughout all the madness of the last decade and included some special payouts along the way, as well (shown by the spikes). STK’s 7% dividend has been secure for years and years, and it looks likely to stay that way.

Don’t ignore that orange line: those are the dividends, which remained unchanged throughout all the madness of the last decade and included some special payouts along the way, as well (shown by the spikes). STK’s 7% dividend has been secure for years and years, and it looks likely to stay that way.

This is powerful stuff: a big, sustainable income stream, exposure to stocks (or bonds, or real estate) and a diversified portfolio. That’s what CEF investors pay those fees for, and if you value cash in hand over the promise of cash in the future, you can see why they are happy to pay them.

The Future of CEF Fees

The magic in a good closed-end fund is turning market returns into income, and there’s no correlation between fees and total returns in CEFs (trust me, I’ve studied this stuff for over a decade). This has meant CEF fund managers haven’t had much motivation to cut fees, and few investors have campaigned successfully on the issue of fees.

That is changing for a lot of reasons.

First, asset management is declining. That’s why Prudential, which manages over $1 trillion, cut 243 employees this year; Charles Schwab is cutting 2,000, and BlackRock’s Invesco has announced it is reducing its head count and will continue to do so. Also, just based on what I’m hearing, asset managers are seeing pay cuts.

Some asset-management firms see an opportunity in this shift, and they’ve been buying smaller asset-management firms. In CEFs, the British asset manager abrdn is taking over many smaller funds, snapping up their management teams and companies. Meanwhile, other firms have been merging funds, with many more likely in the next couple of years).

This consolidation is happening for the simple reason that it reduces costs: fewer people managing fewer funds means lower salaries, filing fees, and just generally lower fees overall.

That means CEF fees are set to fall, so if you hate CEF fees (despite these funds’ 8%+ income streams, diversification and history of long-term profits), you might want to take this world of funds now.

— Michael Foster

5 Ways to Build a Sturdy Monthly Payer Portfolio (With a Huge 9.2% Yield) [sponsor]

Another benefit of PDI is that its income stream rolls our way monthly—another bonus of investing through CEFs! Few people know it, but most CEFs kick out dividends every 30 (or 31) days, instead of every quarter, like pretty well all stocks.

That makes CEFs a terrific way to build a regular income stream. To help you do just that, I’ve assembled a 5-CEF portfolio yielding a sky-high 9.2%. It gives us everything we want in a collection of monthly payers: diversification, big discounts and, of course, a high yield!

Source: Contrarian Outlook