Not many people realize it, but there’s a way you can actually get paid to own stocks.

I’m not talking pennies, either. The fund I’m about to show you is capable of generating $64,000 in dividends per year on a $500,000 investment, thanks to its 12.8% yield, as of this writing.

This gives us three things:

- A large, reliable income stream with a lower risk of principal loss (unlike many annuity products and other income funds out there, where loss of principal is guaranteed).

- Diversification across over a hundred companies in one of the most oversold sectors today: technology—including firms driving the AI revolution, like Nvidia (NVDA).

- The opportunity to own this diversified portfolio essentially for free.

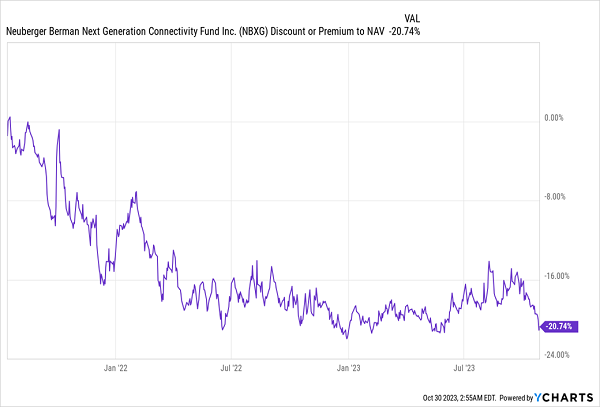

That third part is the trickiest to get our heads around, so let me explain. The Neuberger Berman Next Generation Connectivity Fund (NBXG) is a closed-end fund (CEF) that trades at a 20.7% discount as of this writing, around its 52-week low of a few days ago, which is also its all-time low:

NBXG’s Sale Gets Extreme

Let’s break this down further: as I write this, NBXG has about $934 million in assets and 78,761,496 shares outstanding. That means each share is really worth about $11.86. However, any brokerage or financial website would show that its actual stock price is much lower.

Let’s break this down further: as I write this, NBXG has about $934 million in assets and 78,761,496 shares outstanding. That means each share is really worth about $11.86. However, any brokerage or financial website would show that its actual stock price is much lower.

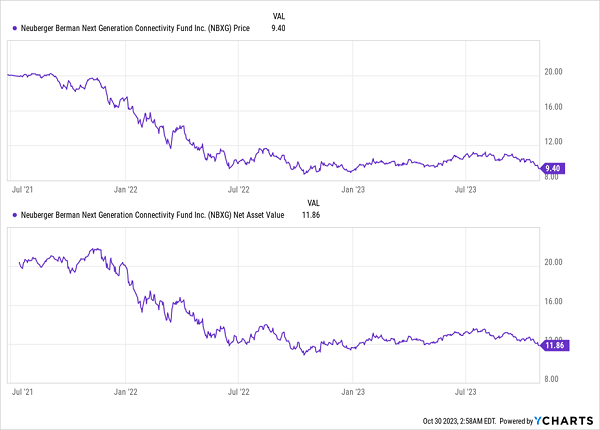

NBXG’s Price and Value

As with all CEFs, it’s good to think of NBXG in terms of value and price. NBXG’s value is the total of its assets divided by the number of shares outstanding, which is $11.86 (the technical term for this is the “net asset value” or “NAV”). Its market price, however, is $9.40, meaning it’s on sale by a margin of about 20.7%. This is also the biggest discount available for a CEF focusing on mostly larger US tech stocks.

As with all CEFs, it’s good to think of NBXG in terms of value and price. NBXG’s value is the total of its assets divided by the number of shares outstanding, which is $11.86 (the technical term for this is the “net asset value” or “NAV”). Its market price, however, is $9.40, meaning it’s on sale by a margin of about 20.7%. This is also the biggest discount available for a CEF focusing on mostly larger US tech stocks.

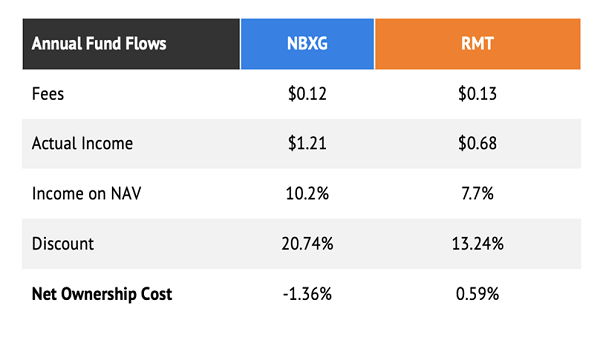

Compare that to the microcap stock–focused Royce Micro-Cap Trust (RMT), the third-most-discounted CEF out there, with a smaller 13.2% discount, despite its focus on much riskier assets.

RMT’s biggest equity holding, Transcat Inc. (TRNS), has an $807-million market cap, while NBXG’s biggest, fiber-optic supplier Amphenol (APH), has a $47-billion market cap and revenues of $12 billion that grew over 15% in 2022. TRNS, on the other hand, had just $230 million in revenue in 2022, up 12.5%.

Given its lower risk, it makes no sense for NBXG to be priced this low, which is a good reason to buy on its own. But beyond that, there’s the fact that NBXG will effectively pay you to own it.

This isn’t something unique to NBXG; many CEFs give investors an opportunity in which, in the words of Forbes staff writer William Baldwin, “You are being paid to let someone select securities for your portfolio.”

How does that formula work? Let’s say we have a hypothetical fund with a per-share NAV of $100 and a market price of $85. Suppose the fund makes annual cash distributions equal to 10% of its asset value. Every $10 check you get in the mail is something you bought for $8.50. So you have an instant $1.50 gain.

Now suppose the fund runs up annual overhead of 1%. That’s $1 out of your pocket. But then there’s the $1.50 windfall more than offsetting the expenses. The annual holding cost of a share with a net asset value of $100 is negative 50 cents. Your effective expense ratio is -0.5%.

In other words, the bigger the discount, the more you’re being paid to own this portfolio. Instead of a hypothetical, let’s plug NBXG into this formula. As I write this, NBXG trades at $9.40 but its assets are $11.86. Factoring in its dividend yield, fees and discount, it has a negative ownership cost (and a big one: -1.36%!).

So far, we’ve uncovered three facts that make NBXG compelling:

So far, we’ve uncovered three facts that make NBXG compelling:

- NBXG has better assets than RMT.

- NBXG yields more than RMT.

- NBXG effectively pays shareholders to invest in it.

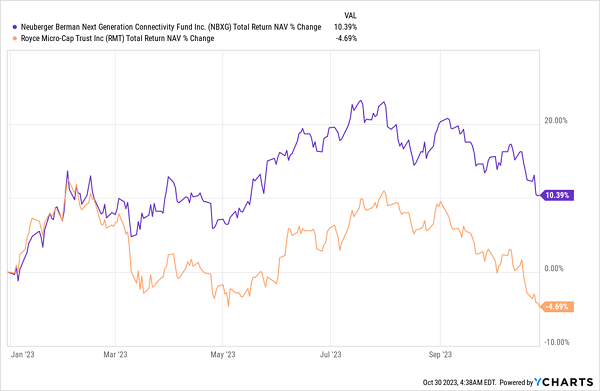

It’s no surprise, then, that NBXG has been outperforming RMT when we look at the fundamental value of the portfolio:

NBXG Pays You to Own It and Beats the Competition

A safer portfolio, higher income stream and better performance, yet NBXG is much cheaper than RMT. This is not just a market inefficiency, it’s an illogical mispricing. In fact, it’s just the kind of inefficiency we love to exploit when we invest in CEFs, all while collecting big income streams like NBXG’s 12.8% payout.

A safer portfolio, higher income stream and better performance, yet NBXG is much cheaper than RMT. This is not just a market inefficiency, it’s an illogical mispricing. In fact, it’s just the kind of inefficiency we love to exploit when we invest in CEFs, all while collecting big income streams like NBXG’s 12.8% payout.

— Michael Foster

It’s Not Just NBXG—Our Buy Window on These 4 Big Dividends Is Open, Too [sponsor]

When it comes to CEFs, we ALWAYS demand big discounts and big dividends. And I’ve got 4 other picks with dividends and discounts that will be shiny lures to income seekers as rates top out this year and “roll over” in 2024.

I’m pounding the table on these 4 dynamic income plays because now is the time to buy them—and start enjoying their Treasury-crushing income streams.

This quartet yields 9.9% between them and sport discounts so deep I see them primed for 20% price gains in the next 12 months.

I’m ready to share my research on all four of them. Click here to learn more and get an opportunity to download a free Special Report naming all 4 of these cash-spinning funds, including their names, tickers, discounts, current yields and more.

Source: Contrarian Outlook