I’m usually a “let the winners run” kind of investor, so it shouldn’t be any surprise that I’ve decided to saddle up the winner of a little investing horse race I created a few years back.

In April 2020, I decided that our Income Builder Portfolio would buy equal dollar amounts of credit-card giants Mastercard (MA) and Visa (V). My article about the buys featured the phrase: “Let’s Have A Contest!”

We followed with three more buys over the years, and although Visa cut ever so slightly into Mastercard’s lead since the beginning of 2023, the fact is that MA has a comfortable advantage in the “contest.”

SimplySafeDividends.com

After my fourth buy of each stock on Aug. 19, 2022, I wrote:

The IBP’s Mastercard position has fared much better than Visa overall. That continues the pattern of the last 7 years, during which Mastercard has outperformed its larger rival 331% to 242%. … Going forward, if V continues to be a relative laggard, I will stop dividing the IBP’s investments evenly between the companies and instead will favor Mastercard. So I guess you could say the contest is really on now.

Which brings us to now.

As any parent will tell you, if you’re going to issue a warning to kids, you’d darn well better follow through if the situation continues. And so, as the IBP’s “daddy,” I’m following through.

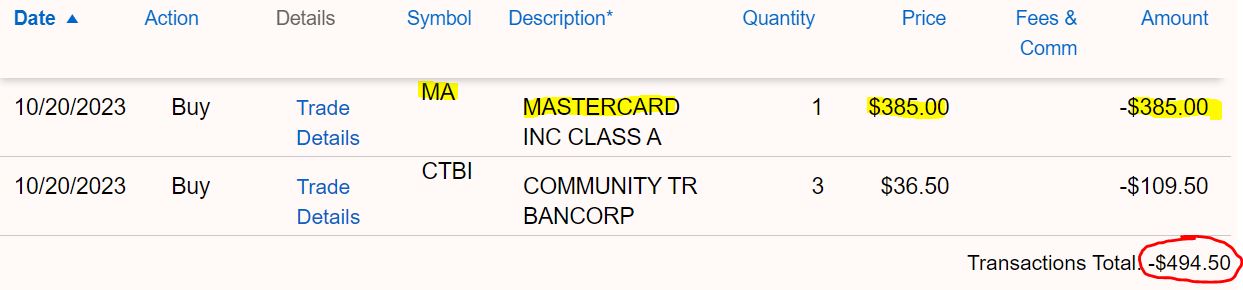

On Friday, Oct. 20, I executed a purchase order for another share of Mastercard stock on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

As you can see, I used the rest of Greg’s $500 monthly allocation to add a few shares to the portfolio’s existing position in Community Trust Bancorp (CTBI). I’ll talk a little about that regional bank later, but not until after I focus on our main October buy.

Master Of Its Domain

Simply stated, Mastercard is one of the highest-quality companies out there.

Here’s a nice synopsis of Mastercard’s dominance from Morningstar analyst Brett Horn:

First, despite the evolution in the payment space, we think a wide moat surrounds the business and view Mastercard’s position in the current global electronic payment infrastructure as essentially unassailable. Second, Mastercard benefits from the ongoing shift toward electronic payments, which provides plenty of opportunities to utilize its wide moat to create value over the long term. Digital payments, on a global basis, surpassed cash payments just a few years ago, suggesting that this trend still has a lot of room to run, and we think emerging markets could offer a further leg of growth even as growth in developed markets starts to slow. Finally, Mastercard is something of a tollbooth business, and the company is relatively agnostic to smaller shifts in the electronic payment space, as it earns fees regardless of whether payment is credit, debit, or mobile.

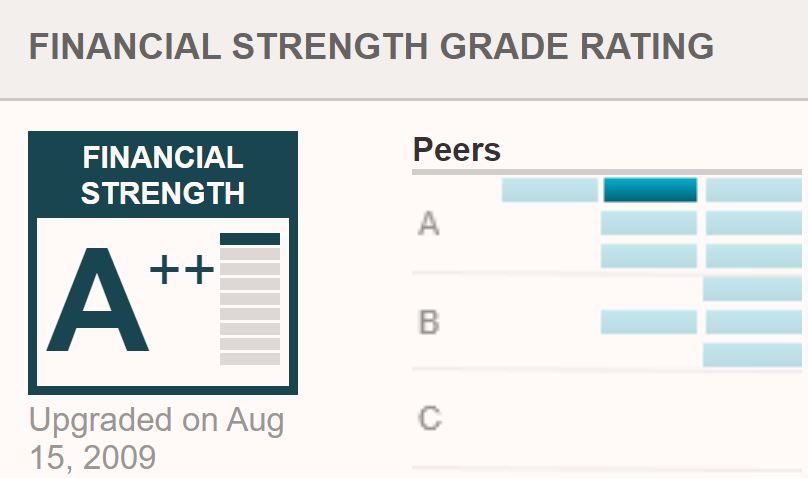

In addition to Morningstar’s wide moat designation, Mastercard gets an outstanding A+ credit rating from Standard & Poor’s, as well as Value Line’s top grades for both relative safety and financial strength.

valueline.com

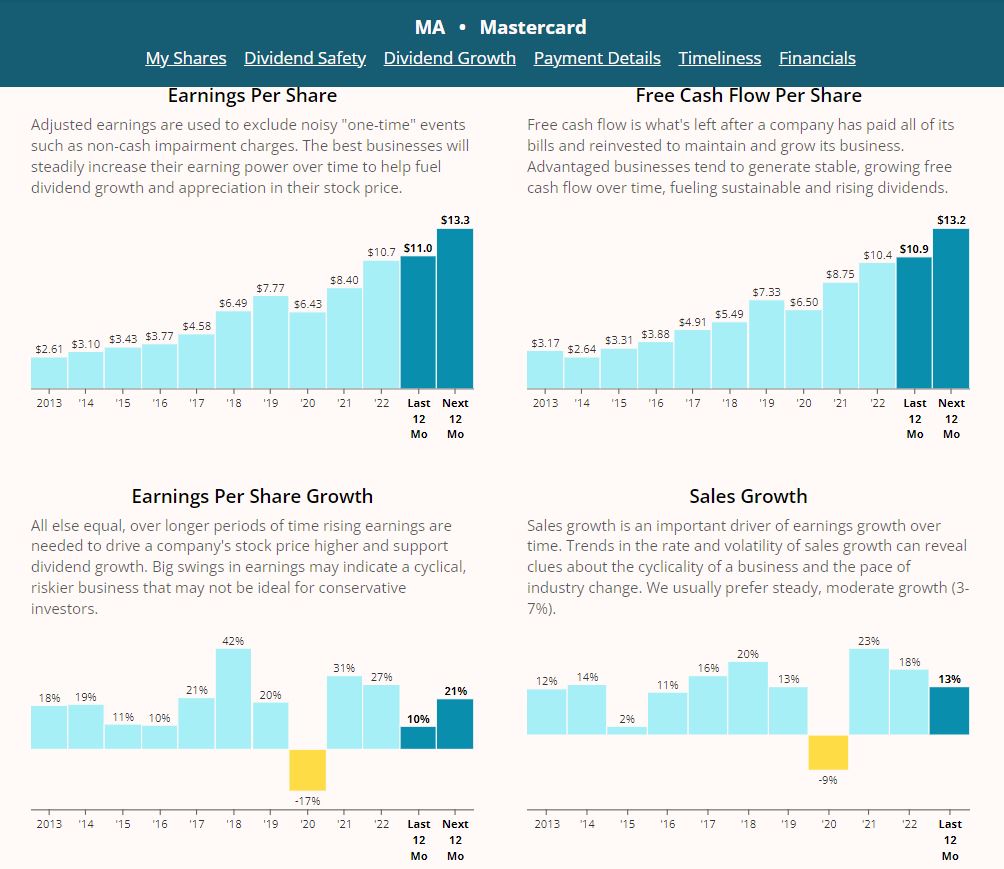

The reason for all those high marks from various analytical and rating agencies: a sterling balance sheet, with ever-growing earnings, sales and free cash flow.

In the charts below, you can see that the only blemish in every category was the downward trend from the depths of Covid-19 pandemic, followed by incredibly quick recoveries:

SimplySafeDividends.com

Mastercard is due to release third-quarter earnings information on Oct. 26, and I usually don’t like to buy shares of a company that close to its report.

However, with only one quarterly earnings miss in the last 10 years, Mastercard is a company whose management consistently under-promises and over-delivers. So I think it’s reasonable to expect another earnings and sales beat, and a favorable reaction from Mr. Market.

That we bought only a single share also mitigates risk against a negative earnings surprise. For those interested in investing thousands of dollars, I certainly wouldn’t blame them for waiting until after the report.

Valuation Station

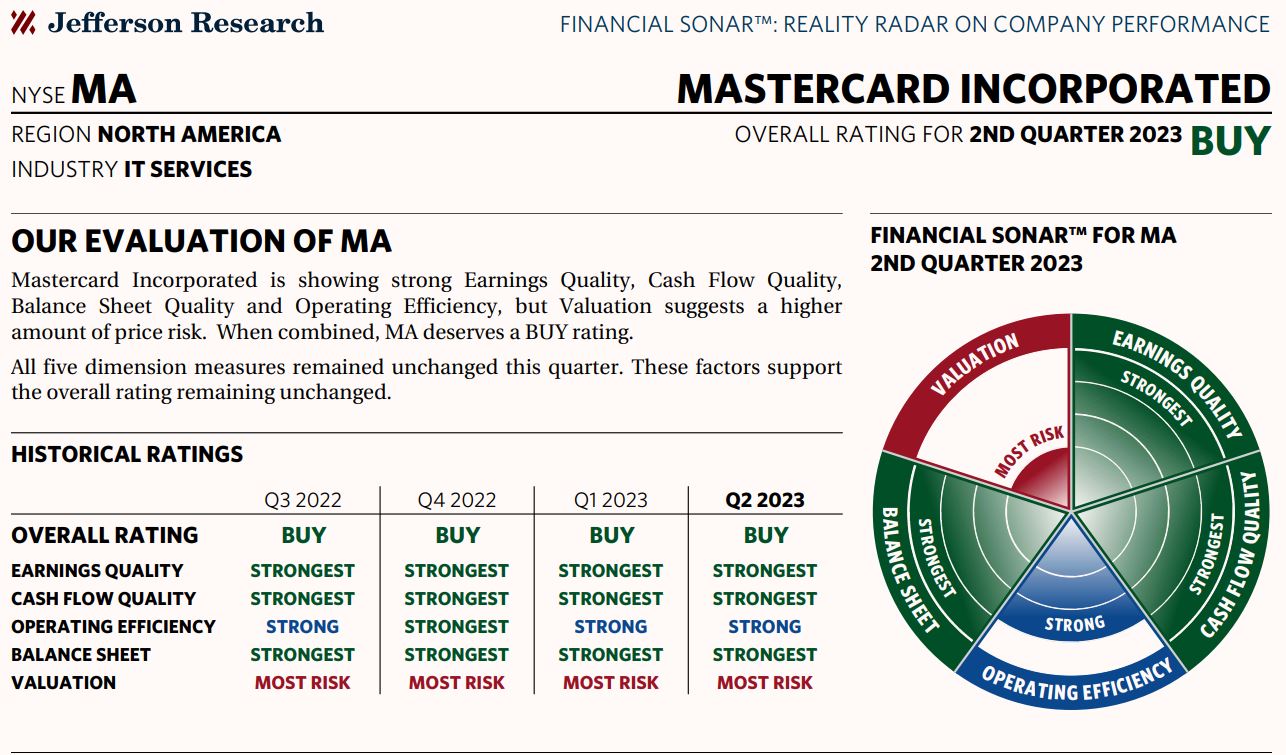

Here’s one more quality-related item — the “Financial Sonar” from Jefferson Research:

Jefferson Research, via fidelity.com

That consistently excellent performance across the board, quarter after quarter, does come with a caveat: rich valuation.

But what else is new? MA is a growth stock that has appeared to be overvalued for years and years.

You might have noticed that despite that “Most Risk” designation, Jefferson Research still calls Mastercard a “Buy.” And JR has plenty of company there.

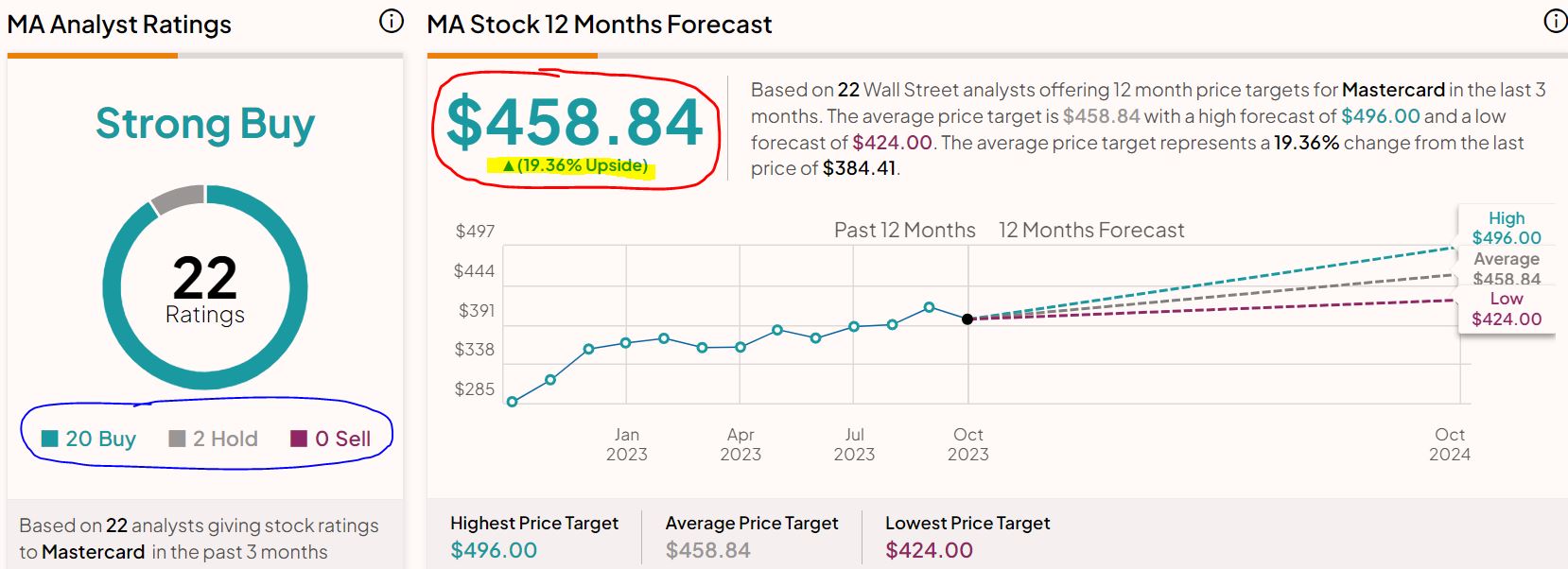

Twenty of the 22 analysts monitored by TipRanks say Mastercard is a buy, with an average 12-month target price that suggests nearly 20% upside.

tipranks.com

A similar story can be found from the 39 analysts tracked by Refinitiv, with 34 calling MA either a strong buy or buy. Their mean 12-month target price is $455.

Refinitiv, via fidelity.com

CFRA couldn’t be much more bullish, with a target price suggesting 25% upside.

CFRA, via schwab.com

In explaining CFRA’s view, analyst Alexander Yokum said:

MA is positioned to perform in a variety of economic conditions, as its multi-pronged growth model helps buffer rapidly changing purchase types (discretionary or nondiscretionary) and/or payment category (card-present or card-not-present). Moreover, sizable inroads into tech-heavy growth levers (remittances, commercial point of sale, and B2B accounts payable) and more cyclical areas (cross-border travel) should allow MA to handily outgrow PCE, leading to revenues outstripping expenses, and compounding per-share earnings at an above-average rate. In the short term, we expect MA to benefit from elevated crossborder volume, given momentum in Asia-Pacific and a rebound of travel into China. … We remain bullish on MA’s ability to modulate spending and generate healthy operating leverage, leading to an attractive ROIC (35%+).

Even though Mastercard is trading at about 30 times expected 2024 earnings, Morningstar says the stock’s fair value is $406 — suggesting slight undervaluation.

After raising MA’s target price from $430 to $440 in July, Argus analyst Stephen Biggar said: “We like Mastercard’s long-term growth story, particularly relative to the broad market. In our view, the company will continue to benefit from the secular shift from cash to credit cards, driven by the rapid growth of online shopping, the security and convenience of cards, and the opportunity to take advantage of rewards programs.”

Value Line’s 3-5 year projection isn’t that impressive, but its 18-month target midpoint of $498 suggests a 30% upside.

valueline.com

Mastercard is one of only 11 companies on Value Line’s list of 100 “Highest Growth Stocks” to receive a 1 for relative safety, and analyst Sharif Abdou said: “Conservative investors seeking upside potential in the coming 18 months should take another look at top-quality Mastercard stock.”

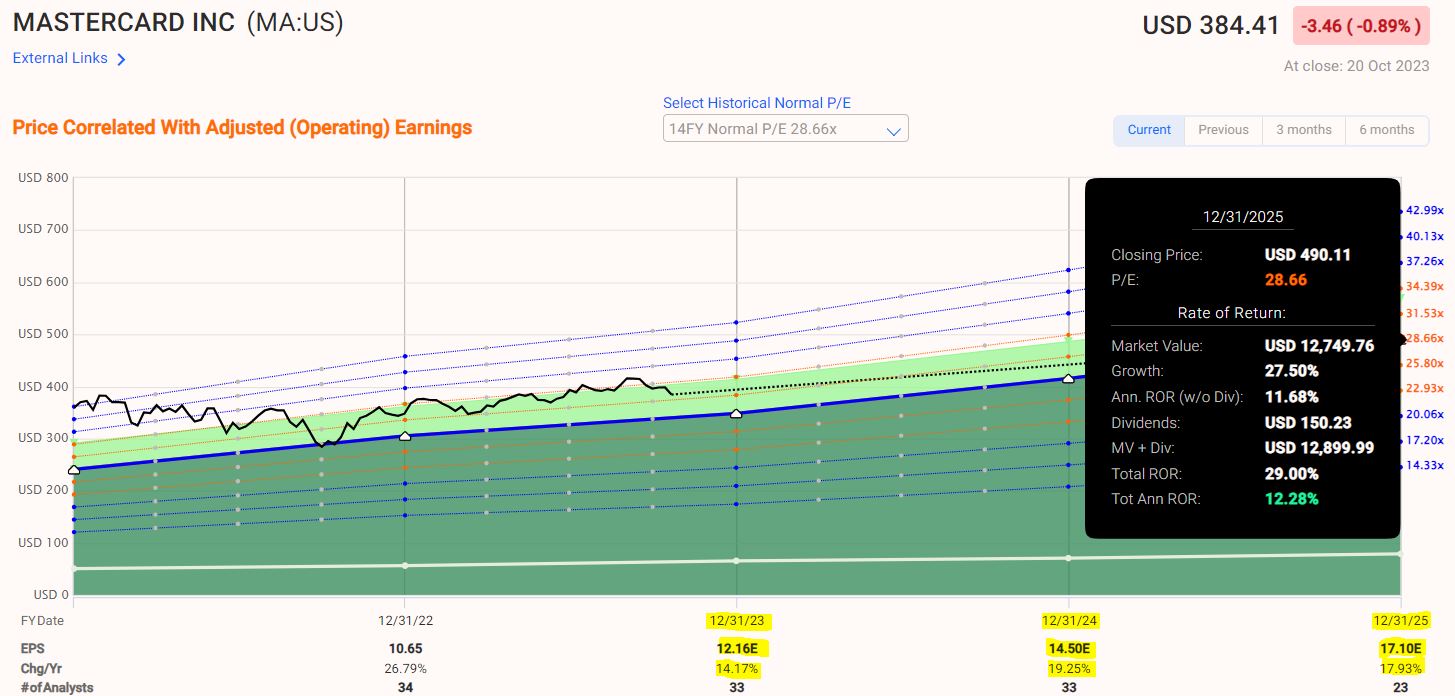

Since the future matters most to investors, I used the FAST Graphs forecasting calculator to produce the following image:

fastgraphs.com

Note the black box to the right of the graph indicating that if MA manages even a 29-ish P/E ratio — which would be its lowest since the Great Recession — its annual rate of return through 2025 would be 12.3%.

Also note the yellow-highlighted areas at the bottom of the image, showing expected earnings growth of about 14% for full-year 2023, 19% for 2024 and 18% for 2025. Gotta love that!

Income Report

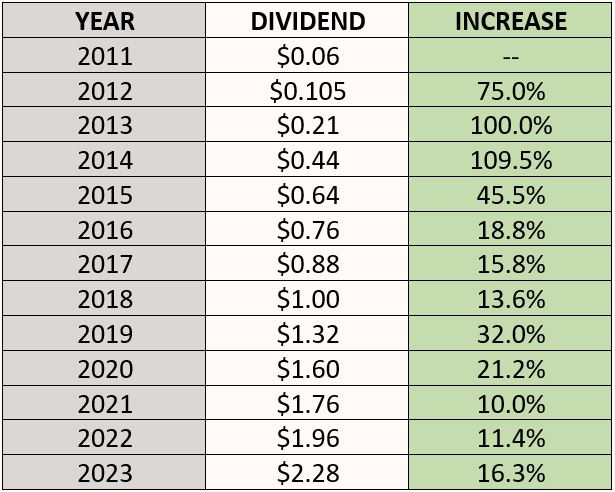

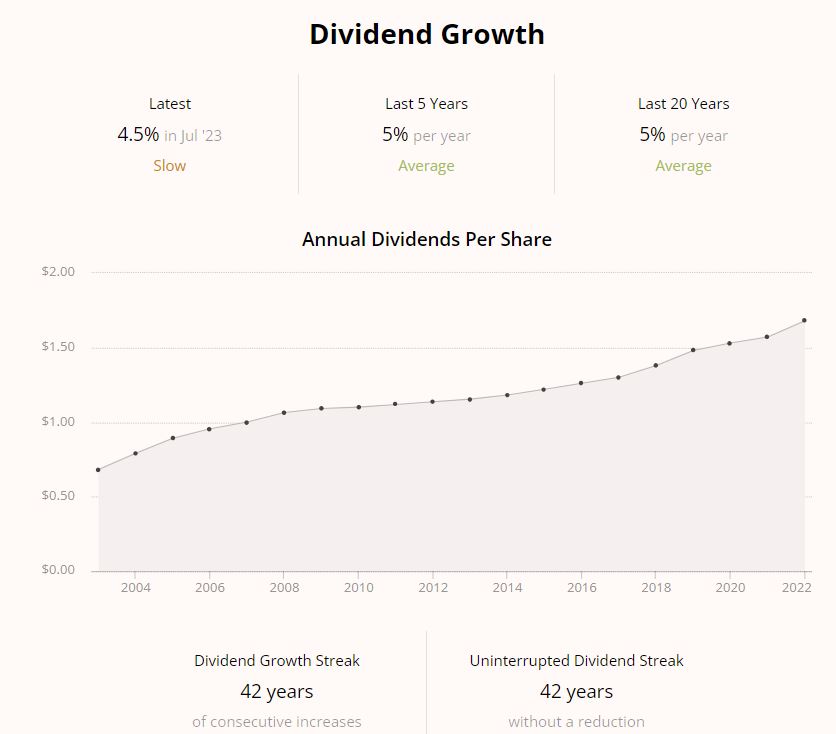

Mastercard has raised its dividend by double-digit percentages for 12 consecutive years, most recently 16.3% from 2022 to 2023.

Given that track record, I’d be surprised if the company didn’t announce yet another large increase in December for 2024.

MA also receives a perfect 99 “dividend safety” score from Simply Safe Dividends, meaning the firm is highly unlikely to reduce its payout.

At 0.59%, Mastercard is the Income Builder Portfolio’s second-lowest yielder, ahead of only the 0.56% of Apple (AAPL). So I consider the dividend just a little bonus, not really a reason to buy the stock.

And speaking of dividends … that brings us to Community Trust Bancorp (CTBI), our other October buy. CTBI yields 5% and has been growing dividends for more than four decades, so I thought it would nicely complement a low-yielder such as Mastercard.

SimplySafeDividends.com

And unlike several regional banks that are struggling these days, this little outfit from Kentucky just released a very good earnings report.

One of our more recent additions to the portfolio, CTBI’s full write-up can be read HERE.

Three stocks in the IBP have announced dividend raises in October: McDonald’s (MCD), 10%; Lockheed Martin (LMT), 5%; and Pinnacle West (PNW), 2%. Those increases — combined with several dividend reinvestments and our October buys — have lifted the IBP’s projected annual income stream to $5,248.

The Income Builder Portfolio home page — HERE — has data on all 52 positions, as well as links to every IBP-related article.

Wrapping Things Up

With its sub-1% yield, how does Mastercard fit into a portfolio that has “Income” right in its name?

Well, while I definitely get that MA won’t be attractive to some DGI practitioners — especially those who have a minimum-yield requirement for every holding — I happen to believe that a Dividend Growth Investing portfolio has room for a few low-yielding, super-high-quality, “growthier” names.

I’m definitely a DGI guy, and yet my personal portfolio includes several low-yielders, and even a few stocks that pay no dividends at all.

I look forward to more years of growth from Mastercard — a well-run corporation, and a stock that has been a better investment than its main competitor for well over a decade.

I also have Mastercard in my Growth & Income Portfolio, another real-money project I run for this site. Check out all GIP-related information HERE.

— Mike Nadel

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: Dividends & Income