Were you able to refi your home when rates were low? I hope so.

Don’t tell my wife, but we almost missed the low-rate era. My better half kept asking about refinancing. “Yeah, yeah,” I said. “We will when rates bottom.”

In early 2021, they took off right under my nose. I stare at the bond market all day and nearly missed this thing!

Fortunately, we got a pullback in rates. I called my buddy, a mortgage broker, who dialed me in with a sweet 2.2% rate on our remaining balance. Two point two!

Had we missed that deal, I’d never live it down. I may as well have slept in my office for a while.

Well, this current situation in dividends is like that. Yields are sky high for the first time since, really, the 1990s. Don’t miss the opportunity to “lock in” these retirement income streams today!

Now Is Our Chance to “Refi” Our Dividends

As I write this, there are hundreds of dividend payers out there boasting higher yields than they have in years—and they’re plenty safe, too. We can thank the Federal Reserve for that.

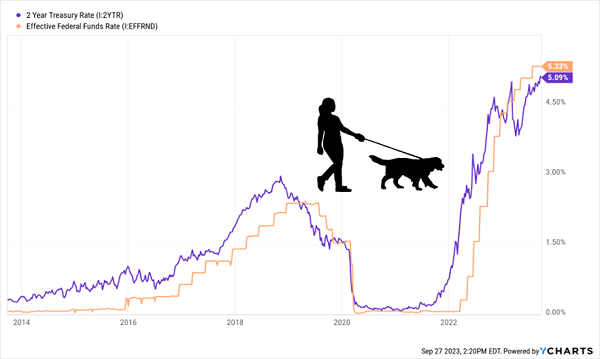

Jay Powell and Co. have driven rates through the roof—to the point they nearly broke the banks! But the Fed only controls the “short” end of the yield curve, which is why the 2-year Treasury yield closely lines up with the Fed funds rate:

The 2-Year Has the Fed on a Leash—or Is It the Other Way Around?

A 5.1%-paying 2-year means a lot more “yield competition” for our favorite high-yield plays, like utilities, real estate investment trusts (REITs) and closed-end funds (CEFs). As I’m sure you’ve noticed, they’ve all been washed out in response.

A 5.1%-paying 2-year means a lot more “yield competition” for our favorite high-yield plays, like utilities, real estate investment trusts (REITs) and closed-end funds (CEFs). As I’m sure you’ve noticed, they’ve all been washed out in response.

But here’s the upshot: their dividend yields have gone through the roof!

Heck, even “first-level” utility plays like Verizon Communications (VZ) yield big: VZ pays 8.2% today. And that’s just what the mainstream crowd is getting; by digging a bit deeper, we contrarians can grab even higher payouts—often paid monthly, too.

It really is a rich hunting ground of big dividends out there right now. But it won’t be for long—which is where our chance to “refi” our dividends comes in. As the economy slows, rates will fall. Investors will move out of Treasuries—and into high-yielding stocks and funds, sending their prices up, and their yields back down.

In other words, now is the time to lock in the big payouts on carefully selected REITs, utilities and CEFs—then ride along as these dividend plays’ prices return to “normal”!

Here are two tickers that are worth your consideration now. And I’ve got plenty of timely buys waiting for you in the portfolio of my Contrarian Income Report high-yield investing service.

“Dividend Refi” Play No. 1: A “Double Discounted” 9.5% Payer

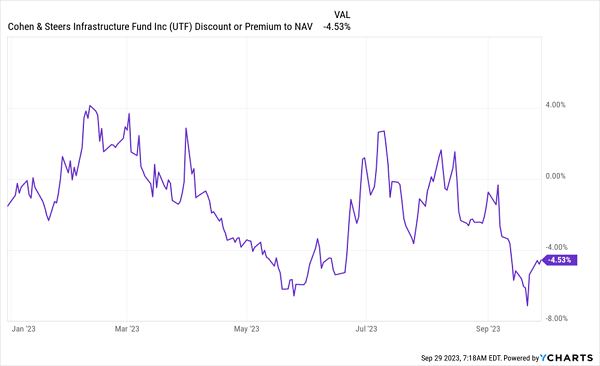

The Cohen & Steers Infrastructure Fund (UTF) is giving us a nice “dividend refi” opportunity now, thanks to the “double discount” it’s throwing us.

The first is the one every mainstream investor who buys utilities on the open market gets: the chance to buy washed-out stalwarts, like NextEra Energy (NEE), Southern Company (SO) and Canadian natural gas provider Enbridge (ENB)—all top UTF holdings—cheap.

The second is only available to those of us in the CEF “VIP lounge,” and comes from UTF’s own discount to NAV, which, at 4.5%, is the best deal we’ve seen on this classic “recession-resistant” play since Silicon Valley Bank et al hit the skids last spring.

UTF’s “Double Dip” Discount

And as we discussed last week, it’s not the current discount to NAV that matters with CEF, but the discount as it compares to history.

And as we discussed last week, it’s not the current discount to NAV that matters with CEF, but the discount as it compares to history.

We’ve already got good news about that in the chart above. But the longer-term average is breaking our way, too: in the past five years, UTF has traded at a 0.8% average discount—or basically par. That gives us some nice “snap back” upside as the current 4.5% discount disappears, to accompany the fund’s monthly payout, which yields 9.5% on a yearly basis.

“Dividend Refi” Play No. 2: A 4.5% Payout That’s Movin’ On Up

Since we’re talking refis, we’d be remiss not to mention a residential REIT—as today’s high mortgage rates push more folks into the rental market. That’s a big profit driver for Equity Residential (EQR), owner of some 80,000 apartment units around major metros like New York, Boston, Seattle and Washington, DC.

EQR is a net beneficiary of rising rates, with rental rates from its existing buildings rising 3.5% in August and occupancy sitting at basically fully booked 96%. Its balance sheet is also healthy with its debt measuring in at 27% of assets.

Moreover, EQR has just 11.8% of its debt maturing this year, dropping to a mere 0.1% next year and 7% in 2025, and its loans carry a weighted average rate of around 4%—far less than you and I would pay at the bank!

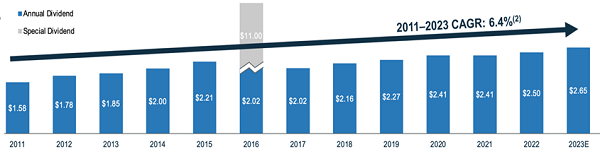

Dividend coverage is also solid for a REIT, at around 70% of adjusted funds from operations (AFFO, the main REIT profitability metric.). And payout growth is strong and steady, too:

EQR’s Payout Takes the Elevator

Source: Equity Residential May 2023 investor presentation

Source: Equity Residential May 2023 investor presentation

That leaves us with a 4.5% “starter yield” that’s higher than it’s been since 2020. By buying now, we lock that yield in and start to build up the yield on our original buy thanks to EQR’s steady payout growth.

— Brett Owens

Your Best Play for the 2023 “Dividend Refi Boom”? 8%+ Yields (Paid Monthly) [sponsor]

This temporary “rates-up, yields-up” window is a terrific time to lock in high monthly payouts for decades to come.

Of course, we income seekers love monthly payouts because they let us reinvest our cash faster—and they line up nicely with our bills. No more managing stocks with “lumpy” quarterly income streams!

To help you take full advantage of this short-term buy window, I’ve assembled a unique portfolio of monthly dividend stocks throwing off a rich 8% average dividend today. And thanks to Jay Powell, they’re trading at big discounts, too!

You do not want to miss this, and end up like the folks who missed the bargain rates of 2020. Click here to get the full backstory on this monthly paying portfolio and the opportunity to download a free Special Report naming my favorite 8%+ paying stocks and funds inside.

Source: Contrarian Outlook