As an investor, it sometimes can feel as if you’re on a treadmill to nowhere.

Whether you’re buying individual stocks in a brokerage account or contributing to mutual funds through an employer’s 401(k) plan, the market can be on such a downer that you don’t even want to look at your account statements.

The S&P 500 Index plunged 5% in September — by far its worst month of the year — as investors were spooked by the combination of high interest rates, inflation, Russia’s invasion of Ukraine, China’s economic woes, and a toxic political environment in the United States.

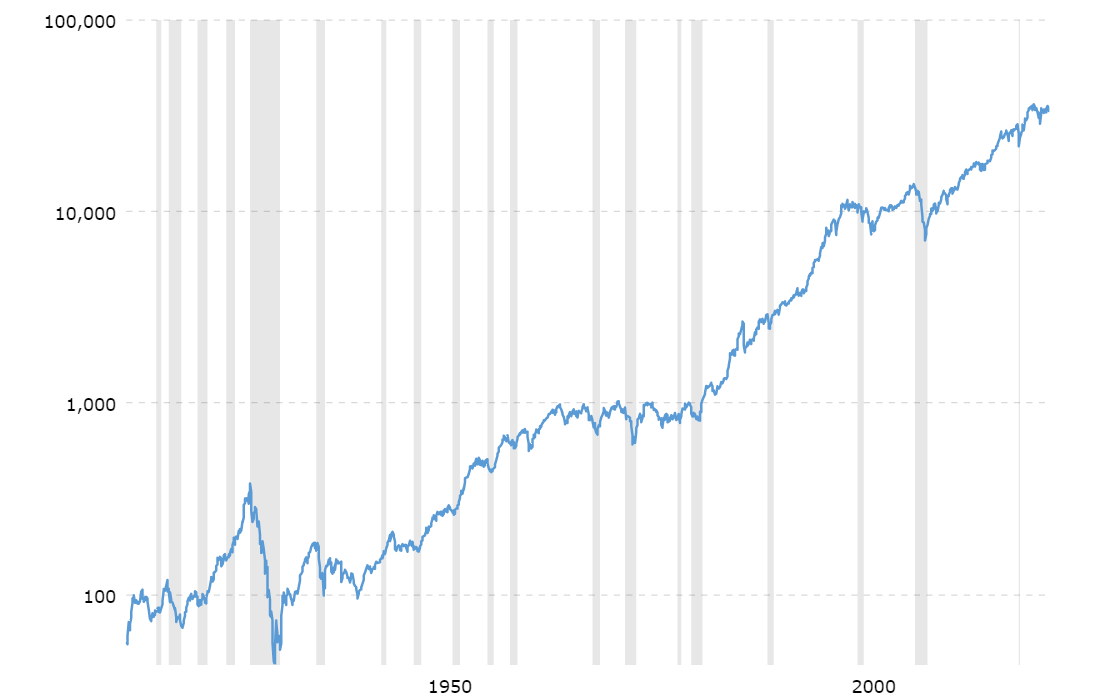

But here’s something to remember: Eventually, the market goes up.

Through recessions (the gray-shaded vertical lines on the Dow Jones Industrial Average chart below) and wars and terrorist attacks and droughts and any number of other calamities, stock prices of publicly traded companies have risen and fallen … but, collectively, they’ve always done a lot more rising than falling.

macrotrends.com

My real-money Growth & Income Portfolio — which also serves as the college fund I’m building for grandkids Jack, Logan, Noah, Owen and Piper — offers a more personalized (and recent) example.

When I last wrote about the portfolio on Oct. 5, 2022 (HERE), the S&P 500 Index had been down some 25% year-to-date. The GIP was not immune; it gave up what had been robust gains and showed a paltry total return of 0.3% since it debuted in June 2020 as the Grand-Twins College Fund.

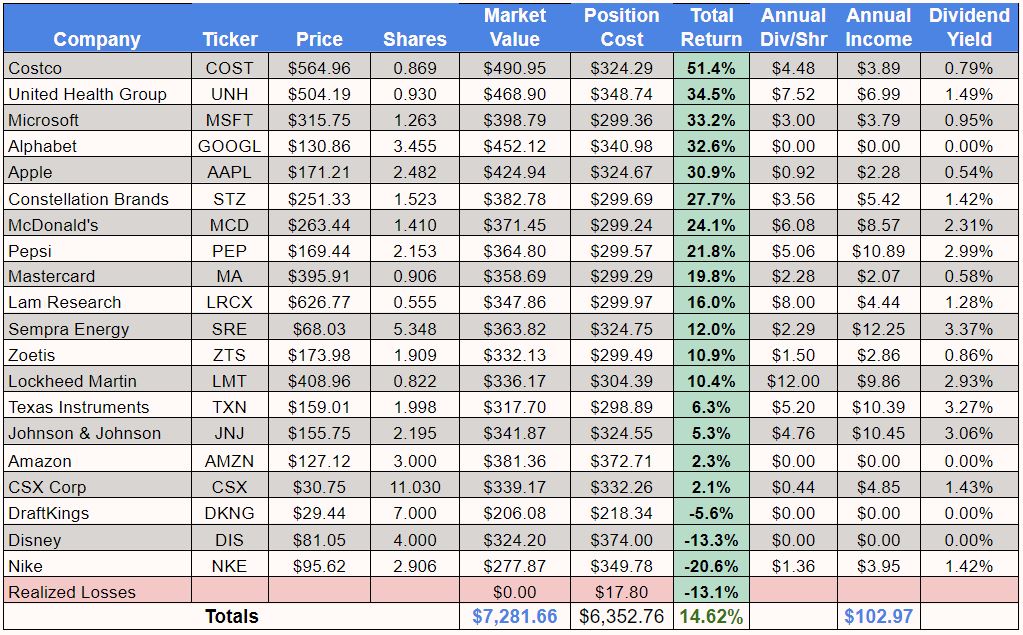

Now, a year later — despite the market’s September doldrums — the GIP’s total return is a healthy 14.6%. Here’s the data through Sept. 30:

Costco (COST), UnitedHealth Group (UNH) and tech giants Microsoft (MSFT), Alphabet (GOOGL) and Apple (AAPL) have been the leaders, but even gambling company DraftKings (DKNG) has had a great turnaround after being down 61% a year ago.

In the portion of the portfolio earmarked for my daughter and son-in-law’s kids, 3-year-old Owen and 19-month-old Piper, the return a year ago was minus-21%. Though still not exactly robust, it’s now at least showing improvement.

I mostly kept adding to the stocks I already had — month after month, a little at a time — though I also opened new positions in major North American freight railroads CSX Corp. (CSX) and Canadian National Railway (CNI). More on those shortly.

Little Big Man

Before I go any further, let me introduce the newest member of the family, Noah, who was born Sept. 5. As you can see, my son and daughter-in-law’s 4-year-old twins, Logan and Jack, love their baby brother.

My wife and I have been contributing $100/month to each set of grandkids, but we soon will be increasing the Jack/Logan/Noah portion by 50 bucks.

In all, we’ll be contributing $250 a month to the college fund. That might not sound like much, but the combined holdings are already worth about $9,000, and it’s only been about 3 years since we started.

All Aboard!

Kids love trains … as Owen, Logan and Jack are demonstrating here.

So I figured, why not buy a railroad stock for each set of grandkids?

When they get older and can understand a little something about what investing means, I can explain to them that railroads have “wide moats” — significant economic advantages — because nobody is about to build any new train lines. And, despite the rare headline-grabbing wrecks, rail is an efficient way to transport goods.

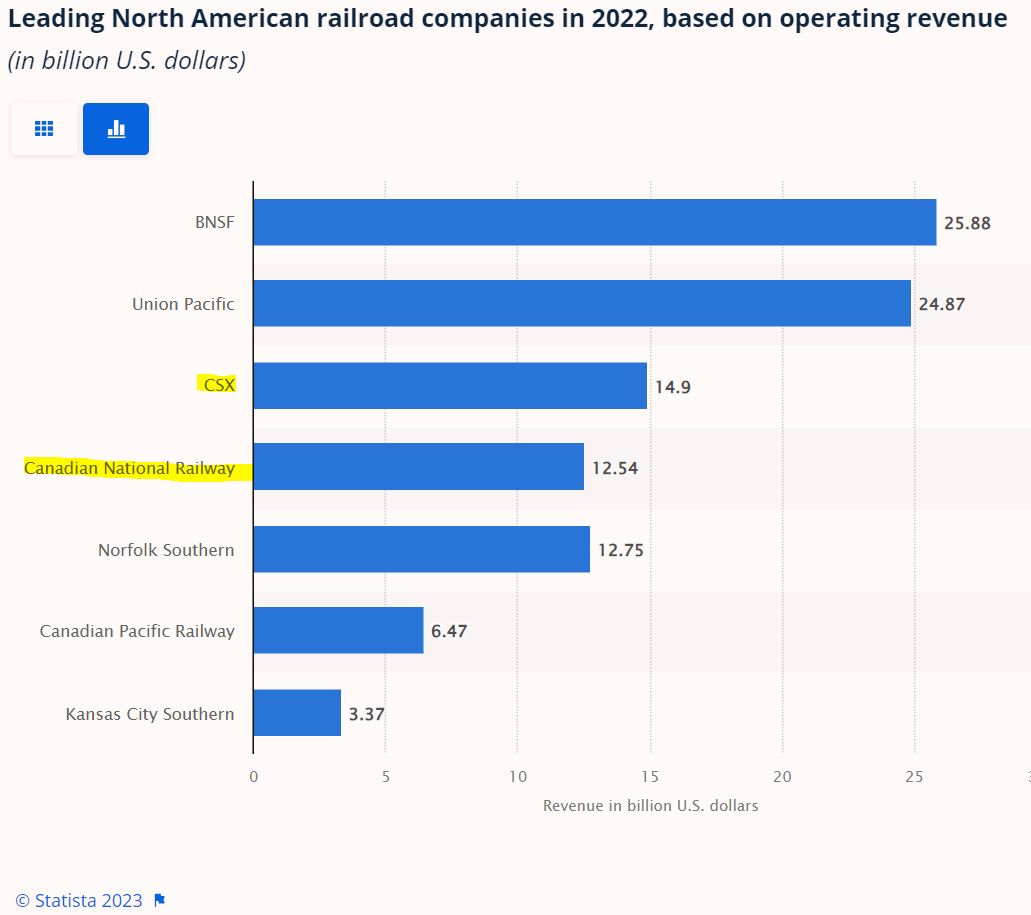

Six Class I freight railroads operate in the United States. There were seven, but Canadian Pacific and Kansas City Southern merged earlier this year.

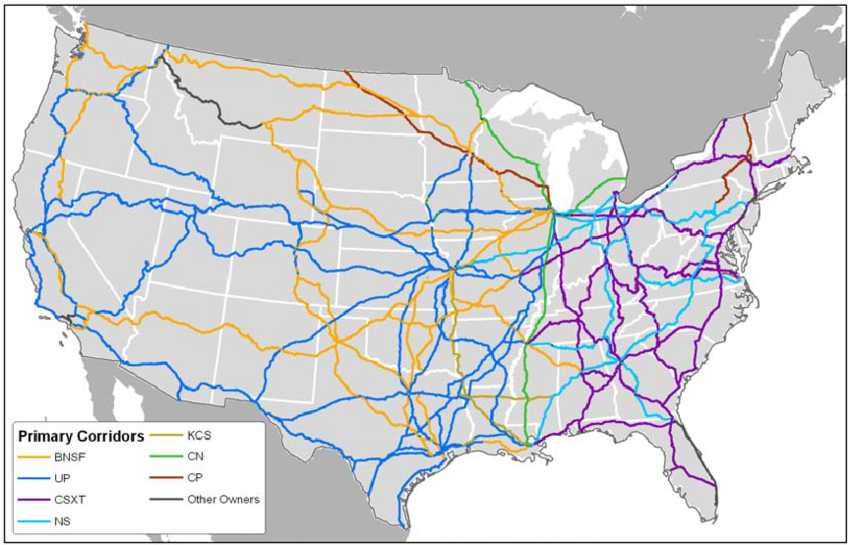

researchgate.net

CSX, represented by the purple line on the above map, operates mostly in the eastern third of the United States. CNI (green line) is by far Canada’s largest railroad but it runs through middle America, too.

Only BNSF, which Warren Buffett took private more than a decade ago, and Union Pacific (UNP) raised more operating revenue last year than CSX and CNI did. (The other public portfolio I manage, the Income Builder Portfolio, owns shares of Union Pacific.)

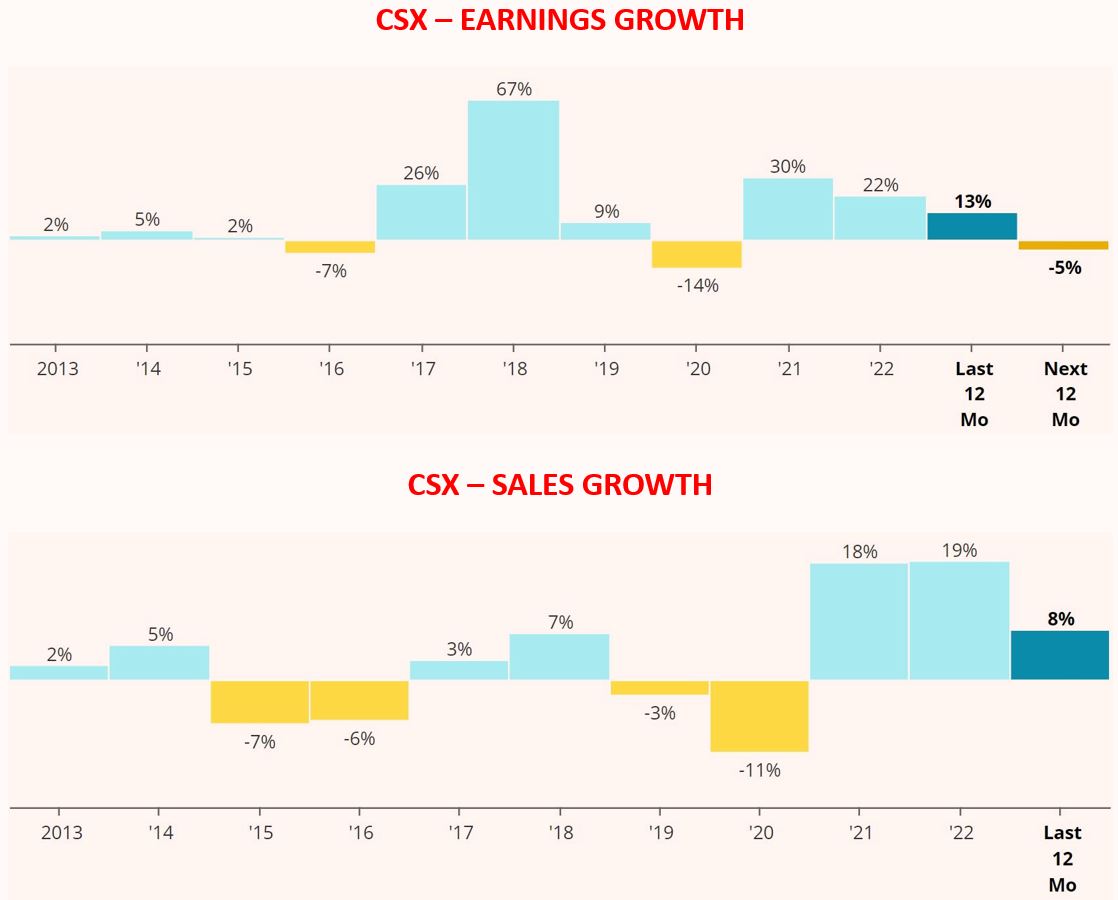

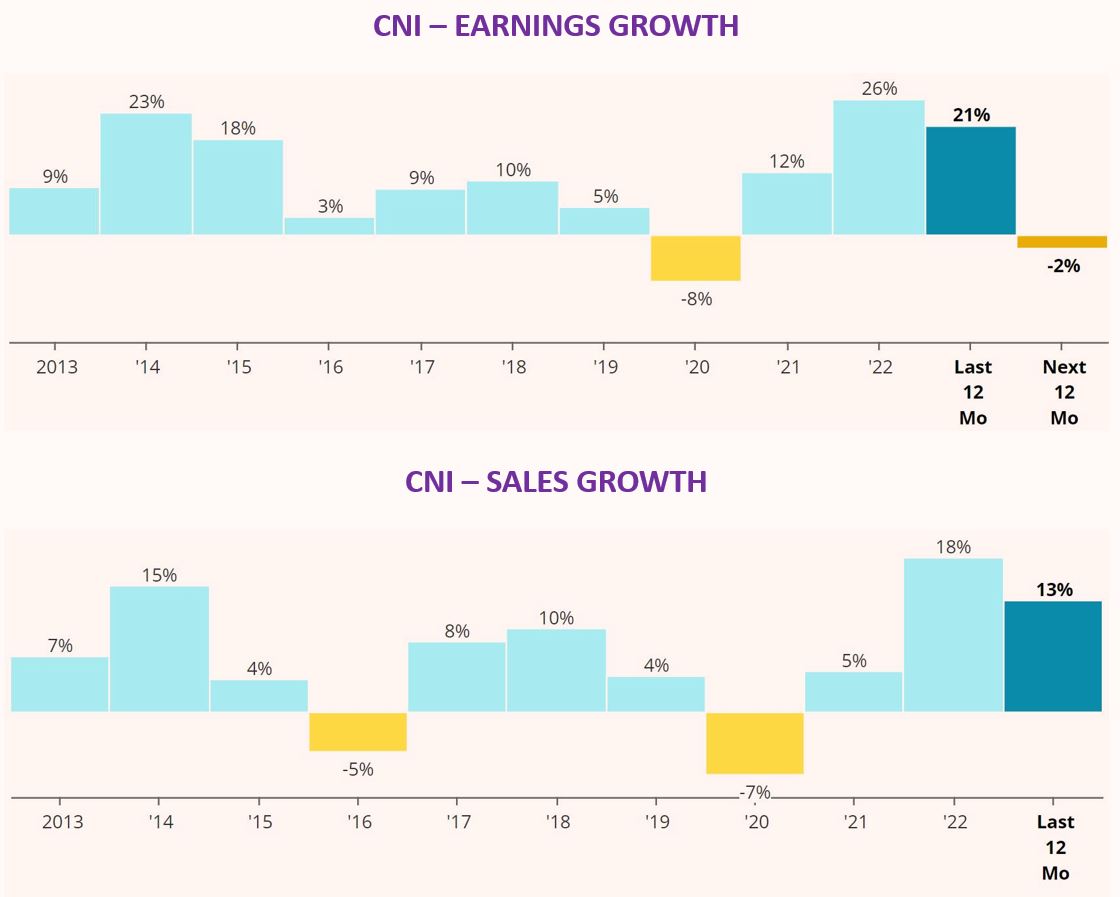

Both CSX and CNI have seen some contraction in what Morningstar analyst Matthew Young called “intermodal volume declines rooted in retail-sector inventory destocking and sluggish imports.”

CNI also has been hurt by business slowdowns due to the wildfires that swept through Canada, as well as on-again, off-again labor strikes.

The following charts from Simply Safe Dividends show how earnings growth and sales growth have declined for both companies.

However, earnings are forecast to grow 9% for CSX and 12% for CNI in 2024, and 10% for CSX and 13% for CNI in 2025. As an investor, I find such guidance to be encouraging.

These well-run businesses receive high quality scores from various rating services and agencies.

Valuation Station

In general, analysts consider both stocks to be in the range of fairly valued to somewhat undervalued.

Of the 27 analysts tracked by Refinitiv, 18 give CSX either a Strong Buy or Buy rating.

Refinitiv, via fidelity.com

At Tip Ranks, 20 analysts monitored have a 12-month target price that suggests a 16% upside for Canadian National.

tipranks.com

Of CSX, Value Line analyst Michael Collins said: “The railroad is heavily exposed to the macroeconomic environment but retains healthy pricing power owing to its strong competitive advantages. On a risk-adjusted basis, the equity holds worthwhile capital appreciation potential over the 3- to 5-year investment horizon.”

And he said this about CNI: “There is less downside to estimates than the other railroads. … We believe there is a good opportunity … “

The following graphic gives valuation-related data from several outlets, and the two Value Line columns reflect Collins’ relative bullishness.

On the down side, CFRA analyst Nasseff Mitsch is much less enthusiastic about the Canadian stock’s prospects.

Citing the labor issues, Mitsch called for a “softer volume environment, combined with supply chain issues.” He also said the merger between Canadian Pacific and Kansas City Southern could increase competition and cut into CNI’s profits.

Income Report

CNI and CSX are relatively low-yielders, but both have very nice income profiles and history, as the following table shows. (I’ve included information on Union Pacific for comparison’s sake.)

SimplySafeDividends.com

CNI has increased its dividend for 28 consecutive years, and average growth over the past 3, 5 and 10 years has been around 12%. Simply Safe Dividends says CNI has the “safest” — least likely to be cut — dividend in the industry.

It’s worth noting that because of currency-exchange rates, there can be years in which the company raises the dividend in Canadian dollars but it looks like a cut in USD.

CSX has a 19-year streak, with 5-year average dividend growth of 9%. Like CNI, it increased its dividend during the Great Recession.

“Growth” is the first word in this portfolio’s name, but “Income” is in there, too. Even though the GIP isn’t cranking out big-time dividends today, I believe it will produce material income before I start making disbursements for college costs in the late 2030s.

Recently announced dividend raises by GIP holdings include a 16% hike by Lam Research (LRCX), a 10% increase by Microsoft, and a 5% raise by Texas Instruments (TXN).

Since my previous GIP article a year ago, the portfolio’s annual income production has increased by 31%. That’s enough to make anybody happy — including Grandma and Grandpa!

Wrapping Things Up

I’ll report back on the Growth & Income Portfolio’s progress in a few months. Until then, check out the home page HERE; I update it regularly, and it includes links to every GIP-related article I’ve written.

For those even more into dividends, our Income Builder Portfolio home page can be found HERE.

— Mike Nadel

Buy this small group of unique stocks... never sell them... and make all the money you need... No matter what happens in the market. Revealed here: the name and ticker of the #1 stock.

Source: Dividends & Income