August and early September were busier than usual in my Dividend Growth Portfolio (DGP). Activities included:

- Making September’s dividend reinvestment

- Recording three dividend increases from the portfolio’s 29 companies

- Selling out of T. Rowe Price (TROW) and replacing it with more Prudential (PRU)

- Exchanging a couple shares of Johnson & Johnson (JNJ) for a stake in its spinoff Kenvue (KVUE)

Let’s review the action.

September’s Dividend Reinvestment

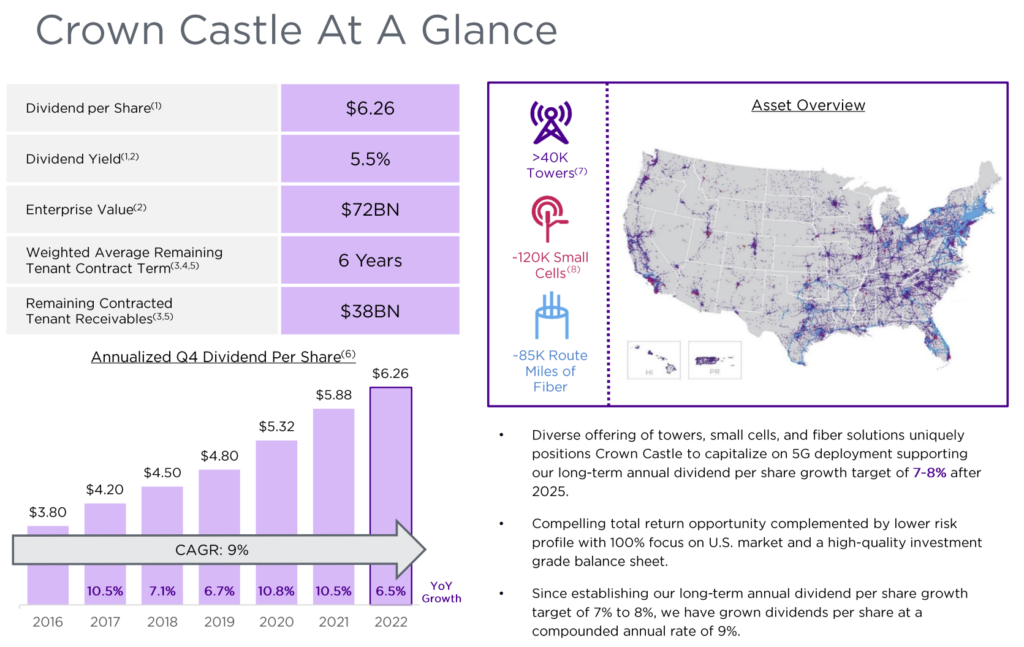

I have been building a position in Crown Castle (CCI) since early 2022, with the intent of making it a “non-small” position, meaning more than 3% of the portfolio.

My interest in CCI is based on its role in telecommunication infrastructure.

Source: CCI Investor Presentation

Source: CCI Investor Presentation

CCI has an extensive domestic network of cell towers (purple in the diagram above), fiber optic cables (blue), and small cells.

Small cells bolster telecom capacity where demand is heaviest. They are attached to city light posts and utility poles, up and down busy streets.

Telecom infrastructure is important, because the generation of electronic data has been increasing at exponential rates for years and will continue to do so. The long-term growth opportunities for CCI appear extensive, as the infrastructure needed to transmit all of the data will continue to grow.

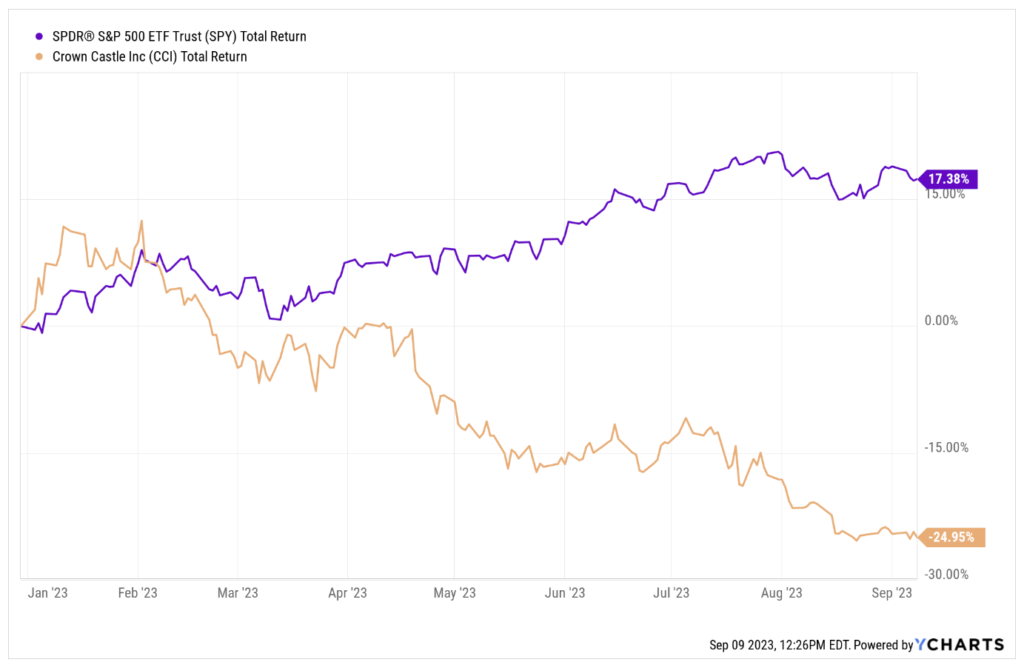

CCI is a REIT (real estate investment trust), and it is among the REITs that have gotten hammered by the market this year. CCI’s total returns (orange below) are down 25% year to date compared to the S&P 500’s gain of 17% (purple).

The good news is that the hammering has put CCI’s shares “on sale.”

The good news is that the hammering has put CCI’s shares “on sale.”

Source: Simply Safe Dividends

Source: Simply Safe Dividends

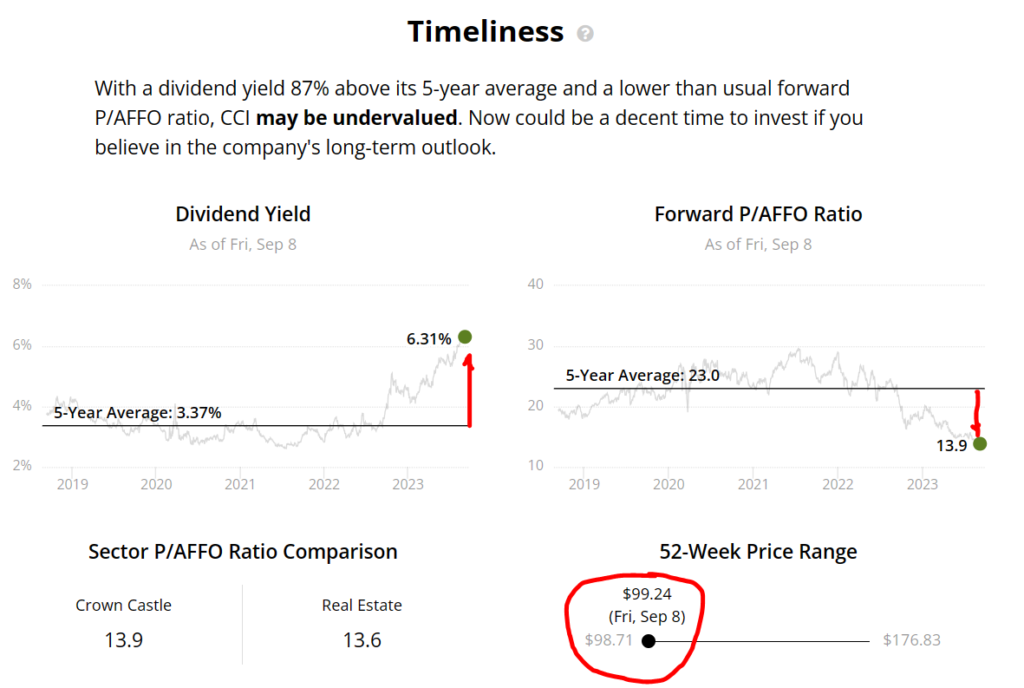

The display shows four metrics, and three of them illustrate CCI’s price attractiveness:

- CCI’s dividend yield is 85% above its 5-year average. Yield moves inversely to price, so the current high level of CCI’s yield suggests that its price is historically low.

- CCI’s Forward Price/AFFO ratio is 40% under its 5-year average. AFFO stands for adjusted funds from operations, which are how profits are measured for REITs. The Price/AFFO ratio is like the P/E ratio for most stocks: A basic measure of valuation. Lower is better, assuming the company is OK.

- The share price for CCI is near its 52-week low. “Buy on dips,” they say.

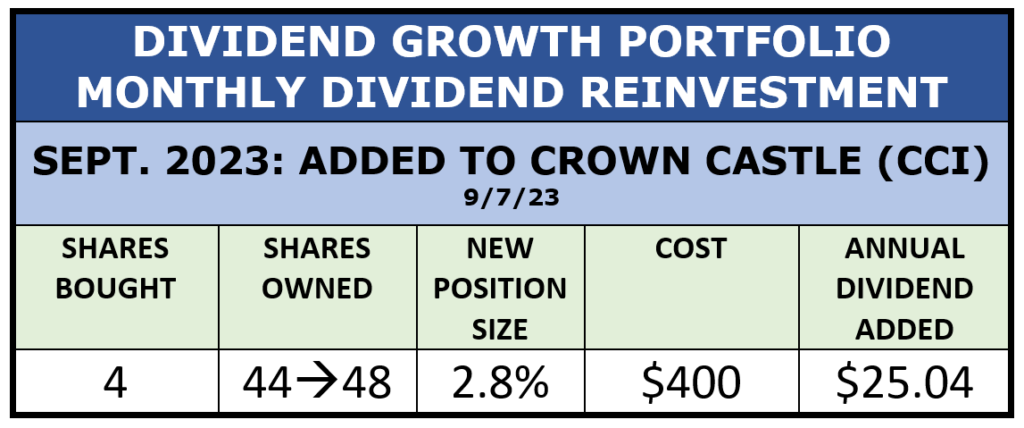

So, for the third time this year, I selected CCI for my monthly dividend reinvestment. Each time I buy the stock, it is more undervalued than last time, so I get the shares at higher yields.

In addition to 2023’s three dividend-reinvestment purchases of CCI, I also bought shares in July using proceeds from a sale of another stock. So altogether, I have purchased CCI four times this year.

Here is the summary of this month’s purchase.

Source: Author

Source: Author

The next ex-dividend date for CCI is about a week after my purchase, so I will collect the Q3 dividend on the new shares as well as all of the preceding ones.

Dividend Increases

The dividends in a dividend-growth portfolio go up for the three reasons shown here:

Source: Author

Source: Author

The DGP has received 23 dividend-increase announcements so far this year. On the following display, I pinched the first 6 months onto one line to save space. The highlighted lines are new increase announcements since last month.

Source: Author

Source: Author

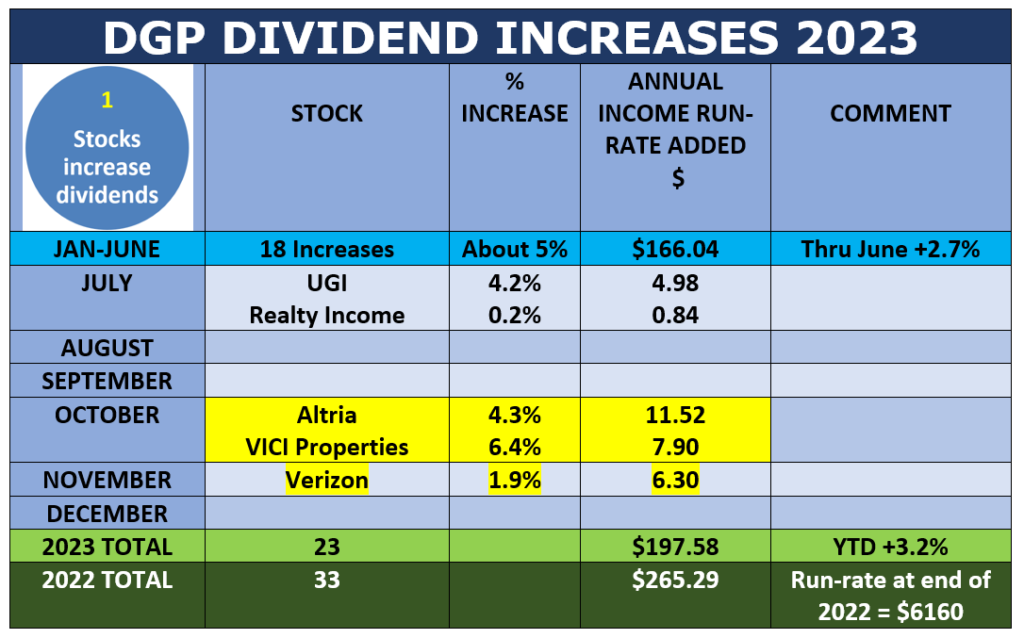

I expect to receive about 8 more increases by the end of the year. The total number of increases will be smaller this year than in 2022, because there are fewer stocks in the portfolio now.

By the end of the year, I expect that dividend increases, by themselves, will account for about a 4% annual income increase for the portfolio.

Dividend Reinvestments

I have already discussed September’s reinvestment that added to Crown Castle.

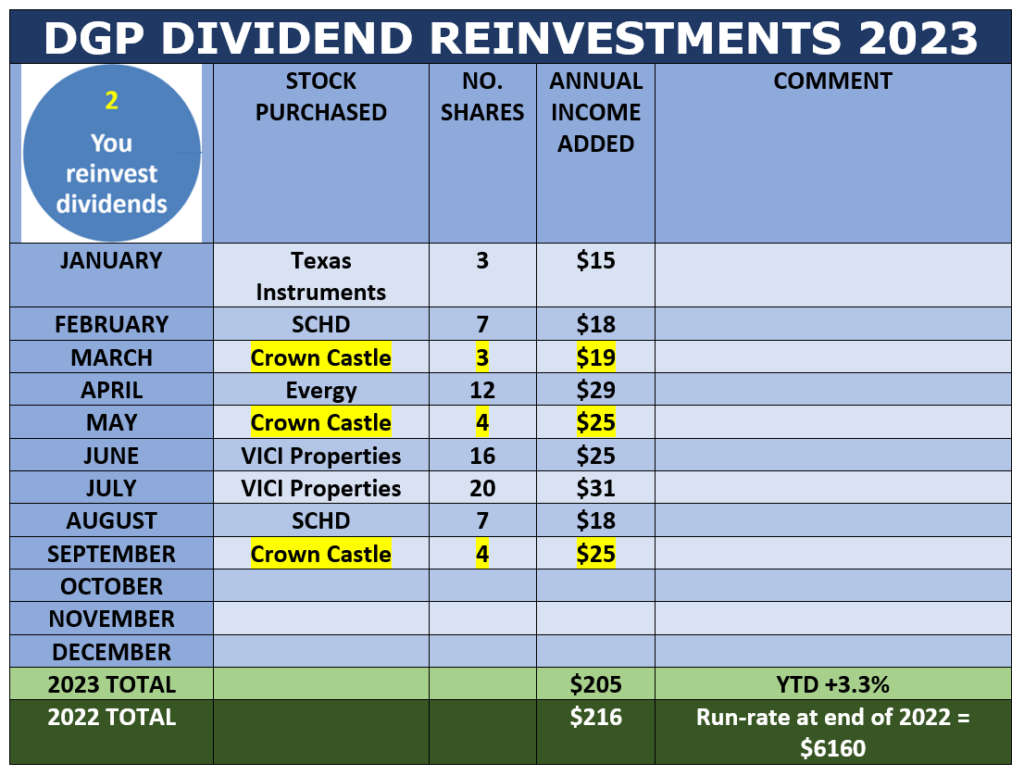

Reinvesting dividends is the second reason the DG portfolio’s income steadily goes up. I collect the dividends in cash, then reinvest them once each month.

Since dividends are paid per share, each additional share purchased with reinvested dividends causes the portfolio’s income to compound. The compounding results from making money (future dividends) on money already earned (collected in the prior month).

The table below shows how my dividend reinvestment program is going so far this year, with the three purchases of Crown Castle highlighted.

Source: Author

Source: Author

Note that 2023’s monthly reinvestments are increasing the portfolio’s income faster than last year. With three months left in 2023, I have already added 95% of last year’s reinvestment income ($205 so far this year vs. $216 in 2022).

At the YTD pace, this year’s reinvestments will, by themselves, add upwards of 4% to the portfolio’s annual dividend income.

Portfolio Management

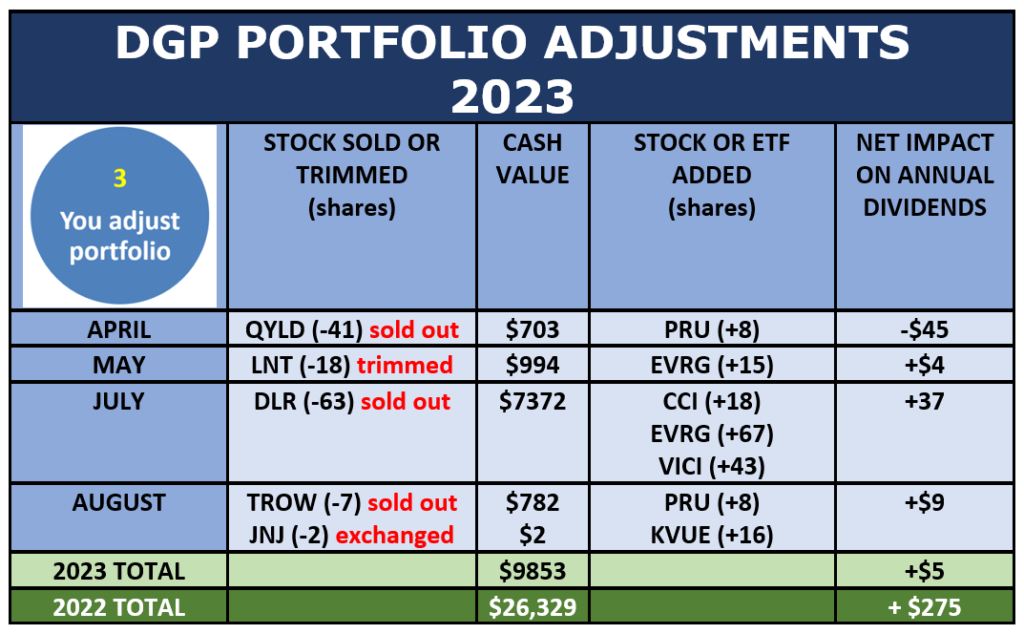

The third reason that dividends go up in this portfolio is that, from time to time, I adjust the portfolio. The reasons might be to trim or sell a disappointing stock, trim a position that has become oversized, and so on.

Some individual trades and adjustments reduce the income stream for a short time, but overall, my portfolio adjustments tend to increase the income stream on a long-term basis.

In August, I made two adjustments. One was routine, while the other was unusual.

Routine adjustment: Replace one stock with another

A sell-stop I placed earlier in the year under T. Towe Price (TROW) hit on August 2, and my shares sold out. I used the proceeds to add to Prudential (PRU), which was already a position in the portfolio.

Annual income increased $6 from this straightforward swap.

Source: Author

Source: Author

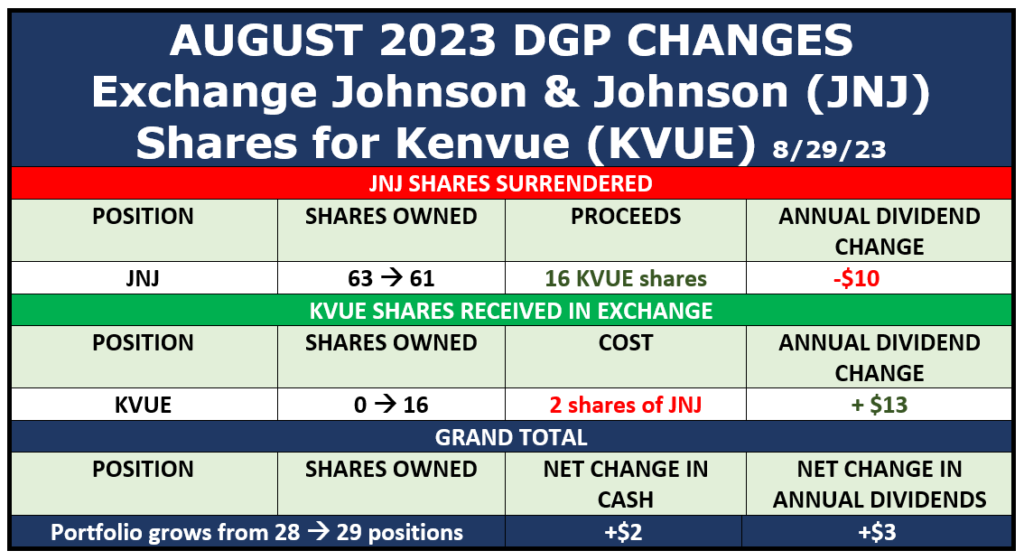

Unusual adjustment: Johnson & Johnson spinoff

Some months ago, healthcare giant Johnson & Johnson (JNJ) spun off its consumer products into a new company called Kenvue (KVUE).

Often in spinoff situations, shareholders in the parent company are simply given shares in the new company. JNJ chose a different route, called a “split off.” JNJ’s shareholders were given the option to exchange JNJ shares for shares in the new company, with the exchange offered at a discount to Kenvvue’s current price.

I signed up for the exchange, but due to the popularity of the offer, only two of the JNJ shares that I offered were accepted. In exchange for them, I received 16 shares of KVUE, which became a new position in the portfolio. (There was also a minor cash adjustment to avoid fractional shares.)

This exchange resulted in a small ($3/year) increase in the portfolio’s dividend stream, as well as one more company in the portfolio.

Here is a summary of all of my portfolio management activities so far this year.

Here is a summary of all of my portfolio management activities so far this year.

Source: Author

Source: Author

Historically, the DGP is a low-turnover operation. In some years, there has been no turnover at all.

This year’s activity, as measured by the money involved, has amounted to about a 6% turnover rate, which would be considered light. The net impact on dividends has been positive by a few bucks.

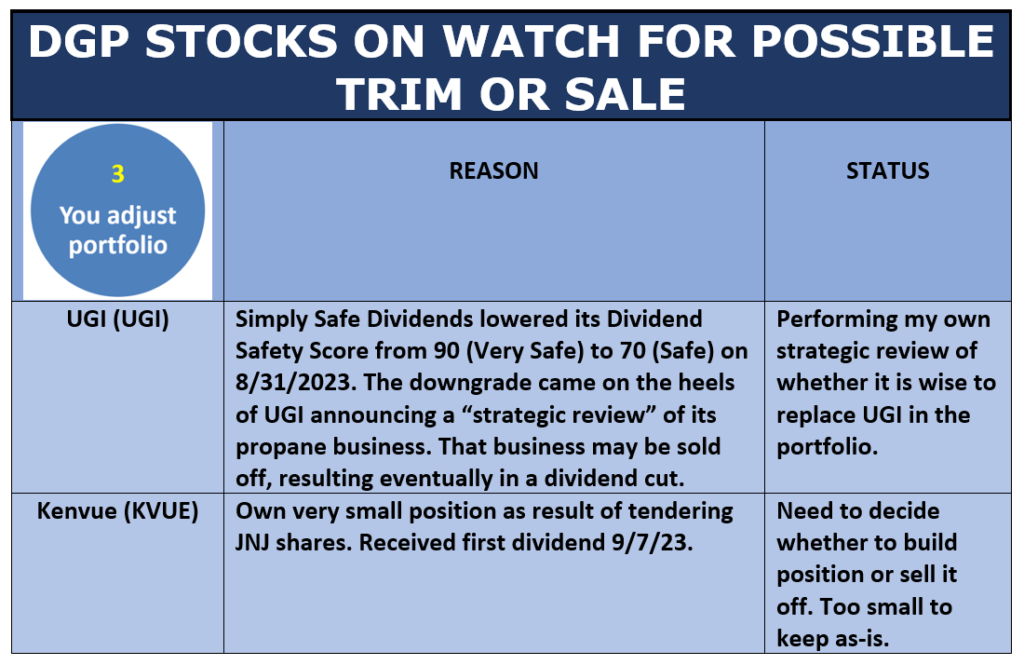

I maintain a watch list of potential future portfolio adjustments. Two new ones hit the radar screen for possible action later this year.

First new item: UGI

On August 30, the utility UGI (UGI) announced that it will undertake a strategic review of its non-regulated propane business.

Simply Safe Dividends has downgraded UGI’s dividend safety score twice this year, from 99 to 90 in May and from 90 to 70 upon the strategic review announcement.

When companies announce strategic reviews, they usually end up selling the business under review. That reduces the size of the company, which means that it also reduces the pool of money from which dividends can be paid. In UGI’s case, the propane business provides about 40% of its earnings.

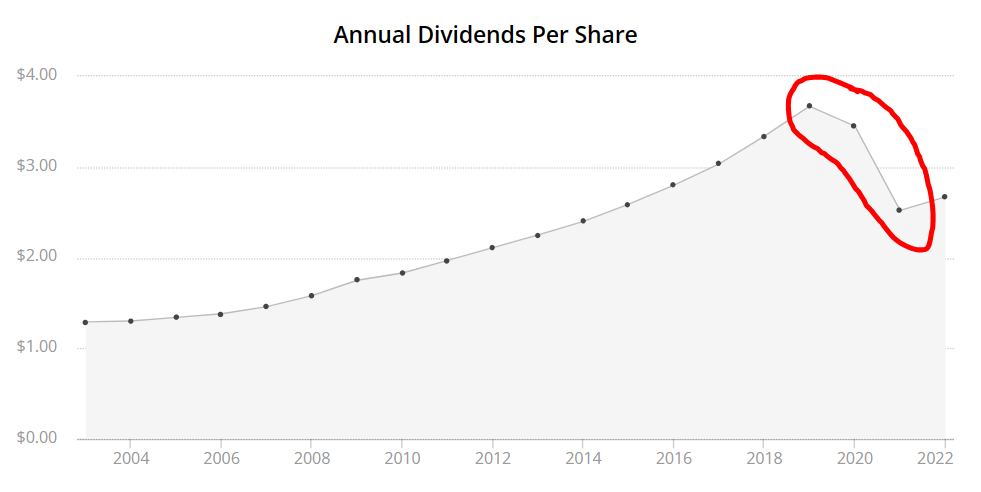

The UGI situation has, perhaps, an instructive precedent. Dominion Energy (D), like UGI, is a utility with historical roots back into the 1800s. In July, 2020, Dominion announced that it was selling a substantial portion of its natural gas transmission and storage assets. The resulting downsizing of the company made a dividend cut inevitable. In fact, two cuts followed:

Source: Simply Safe Dividends

Source: Simply Safe Dividends

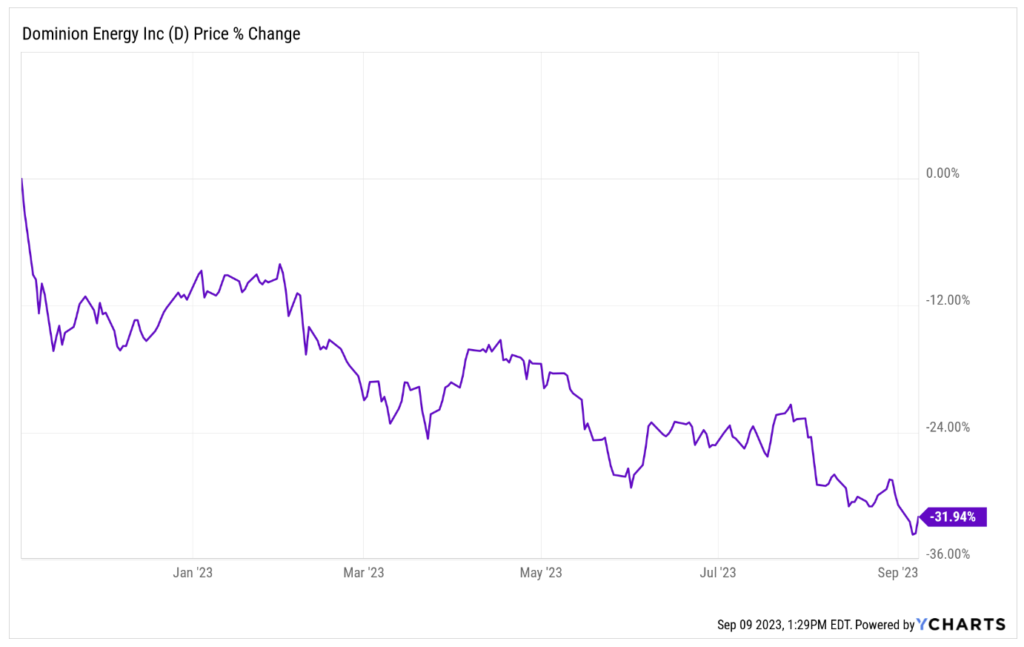

Then, last November, Dominion announced that it was undertaking a “top to bottom” review of its entire business. That announcement induced uncertainty among Dominion’s shareholders, with negative effects on the stock’s price. This chart covers the period after the announcement.

Dominion’s price has dropped 32% since it announced the review.

Dominion’s price has dropped 32% since it announced the review.

The Dominion and UGI situations are not identical, but they both involve utilities, unregulated gas (propane) businesses, and strategic reviews. The market’s initial reaction to UGI’s August 30th announcement was positive (price up 3%), but it has only been a few days.

For all of the reasons above, I have put UGI on watch for possible sale. Over the next year or two, its story may turn out to be like Dominion’s: dividend cuts and price drops. I consider the announcement to not only create an immediate uncertainty, but also to stand as a long-range heads-up about possible trouble for UGI down the road. Therefore, the situation bears watching.

Second new item: Kenvue

Now that I own a handful of Kenvue shares, I need to decide what to do with them: Grow the position, sell it, or simply leave it alone? The latter seems unlikely, since right now Kenvue is such a small position that it’s sort of a nuisance.

That said, KVUE has great DNA, and its yield (3.8%) is actually higher than JNJ’s (3.0%). Its dividend growth rate has yet to be established, but given its parentage, I expect it to become a dividend-growth company. S&P has already added KVUE to its Dividend Aristocrats – companies that have 25+ years of dividend increases – even though the company has only been around a few months.

Here is the current watch list for possible portfolio management actions.

Source: Author

Source: Author

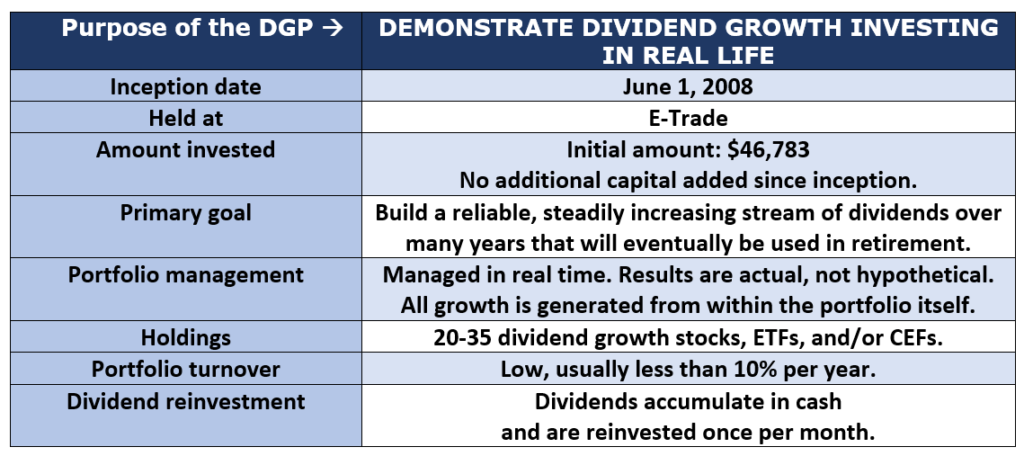

Quick Update of Full Portfolio

My Dividend Growth Portfolio (DGP) is now in its 16th year. The DGP is real, meaning that it is not a hypothetical, “model,” or back-test. All decisions about managing it have been made in real time with real money.

This display describes the DGP in a nutshell.

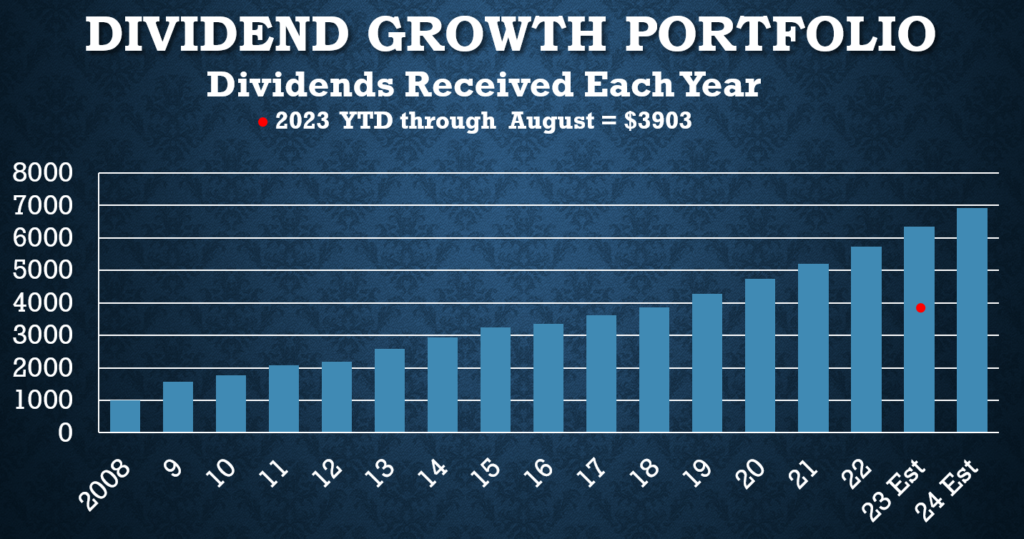

The primary goal – to build a reliable, steadily increasing stream of dividends over the long term – has been, and continues to be, achieved, as shown here:

Source: Author

Source: Author

The full-year 2023 estimate is the sum of the dividends already collected through August ($3903) plus future dividends expected over the remainder of the year (not counting changes in the holdings or their payout rates).

The portfolio is well on it way to hitting the year-end estimate for annual dividend increase. Through the end of August, dividends collected in 2023 are 10.2% more than the dividends collected last year through August.

If you want to see the positions in the portfolio at any time, its status as of the end of the previous month is always available here. That link also has an archive of all the articles and videos that I have published about the portfolio.

Thanks for reading!

-–Dave Van Knapp

According to one of the world's top AI scientists, there's a major event coming as soon as three months from today that could cause expensive tech stocks like Microsoft, Google, and NVIDIA to double or triple in price in the months ahead... but whatever you do, don't go all in on big tech before you have all the details. Click here.

Source: Dividends & Income