Live below your means. Intelligently invest your capital for the long run.

It’s such a simple recipe for financial success. But it just plain works.

So what is intelligent investing? Well, dividend growth investing comes to mind right away. This is a strategy whereby you buy and hold shares in high-quality businesses that pay safe, growing dividends to shareholders.

You buy these shares when undervaluation is present. And then you hold for decades, reinvesting those growing dividends along the way.

High-quality dividend growth stocks are some of the best stocks in the world. That’s because they represent equity in some of the best businesses in the world. After all, the only way to fund ever-rising dividends is to produce the ever-rising profits necessary to afford that behavior. And only truly great businesses can produce ever-rising profits.

That said, you should be considering your age. Investing in your 50s isn’t exactly like investing in your 20s, 30s, 70s, etc. There are differences in aspects like time horizon, risk tolerance, income needs, etc.

If you’re in your 50s, yield and income is probably becoming an important consideration. Knowing that your dividends could start to cover your expenses is a great feeling. But you also need some growth in order to protect your future purchasing power. And that focus on safe yield without totally giving up growth is what we’re diving into.

Today, I want to tell you about 3 dividend growth stocks to consider buying if you’re in your 50s.

Ready? Let’s dig in.

The first dividend growth stock I have to highlight today is Enbridge (ENB). Enbridge is a North American energy distribution and transportation company.

After merging with Spectra Energy Corp. in 2017, Canada-based Enbridge became the largest energy infrastructure company in North America. Enbridge operates the world’s longest and most complex crude oil and liquids transportation system. You might think energy commodities are too volatile to rely on. But that’s not what’s happening here. Enbridge is basically an energy toll road, collecting fees no matter what.

Clients have to move their products, and pipelines offer a cost-effective way to do that. If you use these pipelines, Enbridge is going to collect those juicy fees – no matter what the price of energy commodities are at any given time. Indeed, the company estimates that ~98% of its cash flow is predictable through regulated operations, take or pay contracts, or fixed fees.

It’s been a successful model for decades already, and I don’t see that changing. Enbridge was founded in 1949. I think the staying power is partially owed to the fact that Enbridge is mostly insulated from volatile pricing. It’s a steady-eddy business that investors have been able to rely on for decades.

And while the world is slowly moving toward more sustainable forms of energy that are friendlier to the environment, society’s non-negotiable need for consistent energy means that oil & gas products will be necessary for decades to come.

That’s what sets up Enbridge to continue paying and growing its reliable dividend for decades to come.

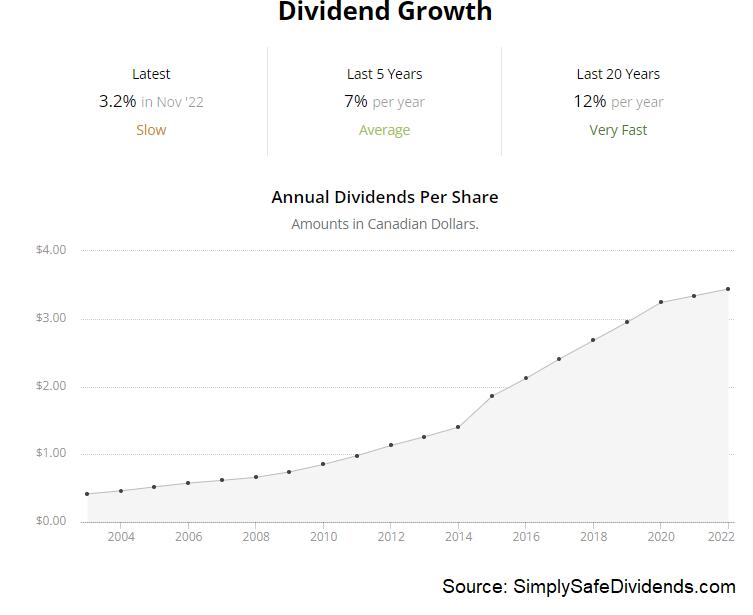

Already, Enbridge has increased its dividend for 28 consecutive years. That’s in its native currency, which is Canadian dollars. Even more amazing, the dividend’s CAGR over that period is 10%. Recent dividend raises have been in the low-single-digit range, however.

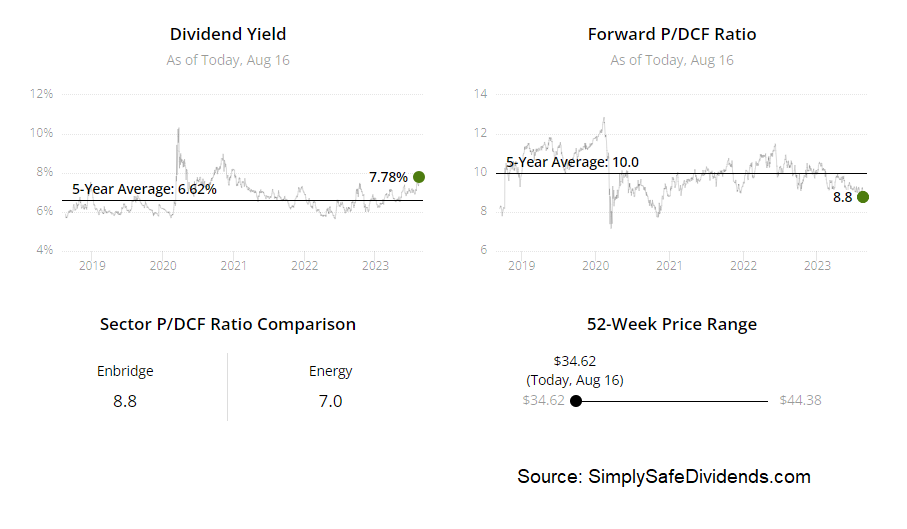

But with the stock currently yielding 7.3%, you just don’t need much dividend growth in order to make sense of the investment. For someone in their 50s and looking for income to start covering the bills and offering the ability to slow down and live off of dividends, that kind of yield goes a long way. This yield, by the way, is high – even by Enbridge’s lofty standards. It’s 70 basis points higher than its own five-year average. With the payout ratio at 65.1%, based on midpoint guidance for this year’s DCF/share, Enbridge’s dividend looks to be as dependable as ever.

But with the stock currently yielding 7.3%, you just don’t need much dividend growth in order to make sense of the investment. For someone in their 50s and looking for income to start covering the bills and offering the ability to slow down and live off of dividends, that kind of yield goes a long way. This yield, by the way, is high – even by Enbridge’s lofty standards. It’s 70 basis points higher than its own five-year average. With the payout ratio at 65.1%, based on midpoint guidance for this year’s DCF/share, Enbridge’s dividend looks to be as dependable as ever.

I’m surprised at how cheap this stock has gotten. It’s been totally ignored by the market this year. Of course, when you’re running a boring pipeline business focused on consistent cash flow, and the rest of the market is infatuated with artificial intelligence, maybe we shouldn’t be too surprised.

The stock’s 5% YTD decline against the market’s near-20% rise may have created a great long-term investment opportunity, especially for older, income-oriented dividend growth investors. Since you want to value a pipeline business like this based on cash flow, the current P/CF ratio of 7.7 is well below its own five-year average of 9.7. Enbridge is never terribly expensive. It’s mature. Growth is limited. On the other hand, it’s a cash cow. And that cash cow is unusually cheap right now. Take a look.

The stock’s 5% YTD decline against the market’s near-20% rise may have created a great long-term investment opportunity, especially for older, income-oriented dividend growth investors. Since you want to value a pipeline business like this based on cash flow, the current P/CF ratio of 7.7 is well below its own five-year average of 9.7. Enbridge is never terribly expensive. It’s mature. Growth is limited. On the other hand, it’s a cash cow. And that cash cow is unusually cheap right now. Take a look.

The second dividend growth stock to go over today is Main Street Capital (MAIN). Main Street Capital is a business development company.

A BDC like Main Street Capital is a financing/investment platform. Main Street Capital provides flexible private equity and debt capital solutions to smaller privately-held businesses that, for whatever reason, can’t get, or don’t want, traditional financing options, such as those available from a bank.

I think of a BDC as a way for regular investors like us to get exposure to something that acts like private equity.

After all, what do PE firms do? They primarily invest in private companies. That’s what a BDC does. So if you have a portfolio that has plenty of defensive blue-chips that are tried and true, a BDC like this one adds a little bit of spice to the mix. Main Street Capital goes out and makes investments in all of these small private businesses that you’d never know of or profit from. And profiting from these moves is all Main Street Capital seems to do.

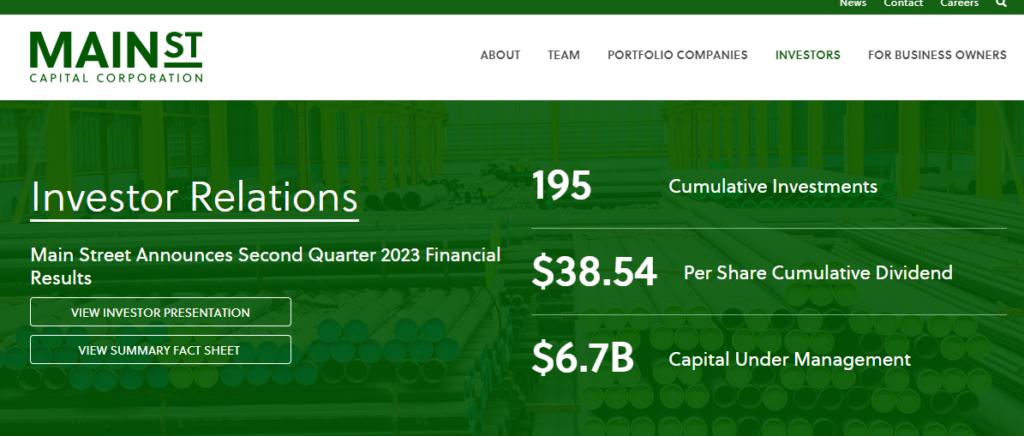

The BDC has net asset value – NAV – per share growth of 115% since its 2007 IPO. The company has almost $7 billion in capital under management. Investments have been made all over the US, in all kinds of industries. The investment portfolio of nearly 200 companies is diversified across dozens of industries. An average investment size of $18.4 million protects the overall firm from any one investment going sour.

There’s nothing sour about this dividend. The stock offers a monstrous yield of 6.8%. And that’s before factoring in the supplemental dividends, which are aplenty.

There’s nothing sour about this dividend. The stock offers a monstrous yield of 6.8%. And that’s before factoring in the supplemental dividends, which are aplenty.

Main Street Capital typically pays multiple supplemental dividends per year. If we take the totality of all dividends paid thus far this year, the yield on the stock rises to 8.4%. And we’re not even done with 2023 yet! Also, this dividend is paid monthly. Not bad, right?

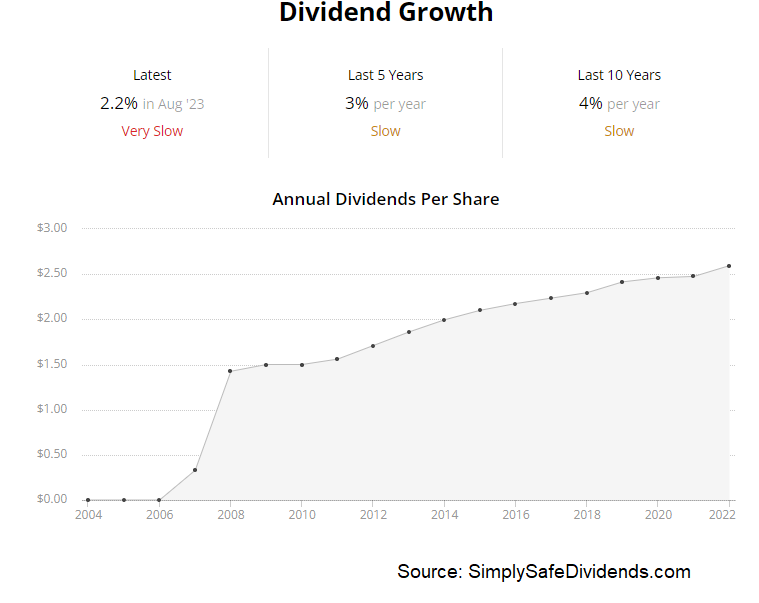

Certainly makes budgeting for expenses easier. Main Street Capital also routinely grows the dividend. The dividend has been increased for 13 consecutive years, with a 10-year DGR of 4.3%. If we run-rate the most recent net investment income numbers, the dividend payout ratio is 62.9% on the regular dividend, before factoring in supplementals. For someone in their 50s, this is a nice income producer with a decent growth kicker.

The stock is currently at a premium to NAV, but it’s been that way for years. When trying to value a BDC like this, you’ll want to look at net investment income – NII – or NAV. NAV is $27.69/share, as I write this article. The stock’s pricing in the market is slightly above $40.

The stock is currently at a premium to NAV, but it’s been that way for years. When trying to value a BDC like this, you’ll want to look at net investment income – NII – or NAV. NAV is $27.69/share, as I write this article. The stock’s pricing in the market is slightly above $40.

So that’s a pretty big premium. However, I’ve never seen Main Street Capital not get a premium to NAV. And that’s been the right call. It’s been such a steady performer across the board. Even though this is an income play, not a high-quality compounder, the stock has a CAGR of almost 12% over the last 10 years, thanks to that massive monthly dividend with supplementals. For someone in their 50s thinking about getting the bills paid with dividends, Main Street Capital could make a lot of sense.

The third dividend growth stock I have to tell you about is W.P. Carey (WPC).

W.P. Carey is a net lease real estate investment trust. With a market cap of $14 billion, W.P. Carey is one of the largest net lease real estate investment trusts in the world. But this REIT isn’t just about size. It’s also about quality and diversification. The diversification, in particular, is really something.

The property portfolio here is somewhat unique. Nearly 1,500 properties leased to almost 400 different tenants. Nothing unique about that, right? Well, where W.P. Carey starts to separate itself from the rest of the pack is in type and location. W.P. Carey doesn’t specialize in one type of real estate.

Instead, its portfolio has industrial, retail, education, self-storage, and even government properties. Regarding geographic diversification, W.P. Carey is truly global. About 61% of properties are located in the US. The rest are worldwide, although largely in Europe. W.P. Carey ranges from self-storage properties in the US to warehouses in Croatia.

I think this diversification has engendered immense staying power for W.P. Carey. Real estate is a tough nut to crack. It’s taken down a lot of pretty smart people over the years. However, W.P. Carey is currently celebrating its 50-year anniversary.

I think this diversification has engendered immense staying power for W.P. Carey. Real estate is a tough nut to crack. It’s taken down a lot of pretty smart people over the years. However, W.P. Carey is currently celebrating its 50-year anniversary.

It was founded in 1973. You simply cannot last for fifty years in the real estate game without running a quality operation. W.P. Carey’s portfolio is currently 99% occupied. And almost every property has built-in rent escalations, with many of them tied to CPI. This REIT is built to last. And that’s why the dividend is built to last.

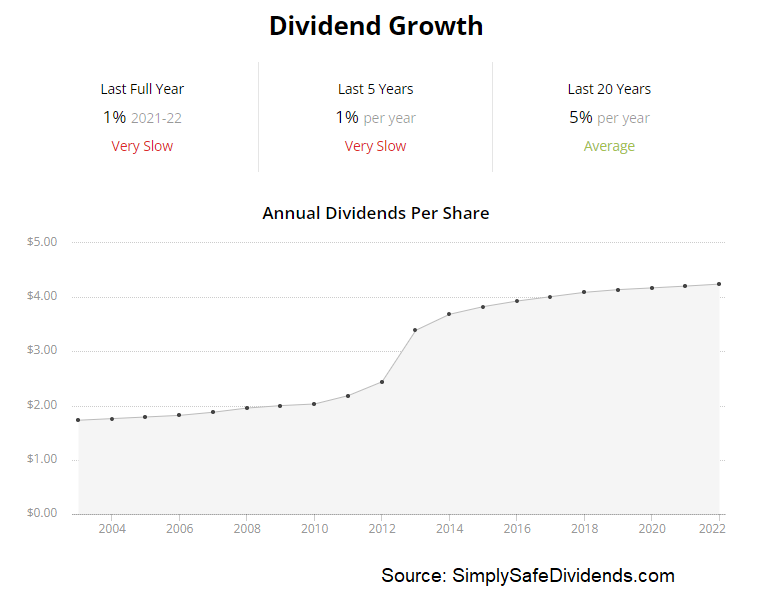

W.P. Carey has increased its dividend for 26 consecutive years. That’s Dividend Aristocrat territory. Now, the dividend has been growing very slowly of late. Recent dividend increases have been in the 1% range. So it’s not moving much. Even when inflation normalizes, that’s not much growth.

However, the stock yields a juicy 6.5%. If you’re in your 50s and thinking about getting bills paid via dividends, that kind of yield is appealing. The payout ratio is 79.9%, based on midpoint guidance for this year’s adjusted funds from operations per share. Pretty much in line with what I’d expect from a REIT. It’s not growing super fast. But it’s a big, safe dividend.

However, the stock yields a juicy 6.5%. If you’re in your 50s and thinking about getting bills paid via dividends, that kind of yield is appealing. The payout ratio is 79.9%, based on midpoint guidance for this year’s adjusted funds from operations per share. Pretty much in line with what I’d expect from a REIT. It’s not growing super fast. But it’s a big, safe dividend.

The valuation also seems to be indicating safety, as in a margin of safety. Outside of the pandemic crash of early 2020, this is the cheapest that W.P. Carey’s stock has been in five years. Every single multiple is significantly off of its respective recent historical average.

Take the P/CF ratio of 12.7, for example. If you’re familiar at all with REITs, you’ll right away know how low that is. This stock’s own five-year average cash flow multiple is 16, which, in and of itself, is not high. W.P. Carey is a bit boring. It’s not flashy.

But it’s been paying a very large and steadily growing dividend for almost three straight decades. For dividend growth investors in their 50s who are, perhaps, sensitive to income, W.P. Carey is a strong candidate for long-term investment consideration.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income