We’re facing a “2016-like” moment in bonds these days, meaning anyone who buys now has a shot at locking in 10%+ dividends for decades—and a shot at price upside, too.

I mention 2016 now because, back then, something truly unusual happened: interest rates on bonds jumped in a short period of time, driving the payouts on high-yield corporate bonds to nearly 10% at their peak:

Rates Drop, Soar, Drop, Soar Again

As you can see above, anyone who bought a high-yield bond in 2016 locked in a 10% cash flow. Many of these bonds continued paying out interest without a hitch, even through the pandemic, a time when yields spiked again, giving investors another chance to buy bonds at another huge interest rate.

As you can see above, anyone who bought a high-yield bond in 2016 locked in a 10% cash flow. Many of these bonds continued paying out interest without a hitch, even through the pandemic, a time when yields spiked again, giving investors another chance to buy bonds at another huge interest rate.

Both times, something magical happened: bond markets effectively brought down the cost of retirement. Think of it this way: back in 2013, when yields were low, you could have funded a $100,000-per-year retirement by buying $1.9 million worth of high-yield corporates.

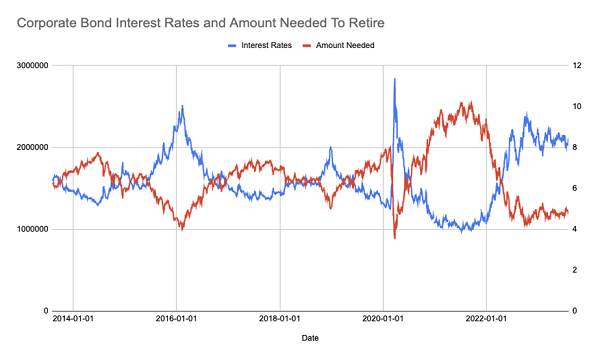

We can even see when retirement got cheaper because the yield—the interest payments corporate bonds pay out to investors—on bonds fluctuates daily. So as bond prices fluctuate, the amount of money it takes to use the bond market alone to retire changes daily. Here’s a chart of how much it took to net $100,000 per year in passive income for every day over the last decade.

Source: CEF Insider

Source: CEF Insider

The red line shows the balance required to retire with $100,000 in interest on a daily basis, starting at $1.56 million in August 2013 and falling to $1,183,431.95 as I write this in the first week of August 2023.

That’s a big range! It means someone today would need over $400,000 less to retire with corporate bonds than they would’ve needed a decade ago, and it’s over a million dollars less than the peak of over $2.5 million in mid-2021.

Now there’s a reason why we shouldn’t just rely heavily on corporate bonds, take all the interest payments and call it a day. Or at least there was a good reason for a long time—now I’m not so sure.

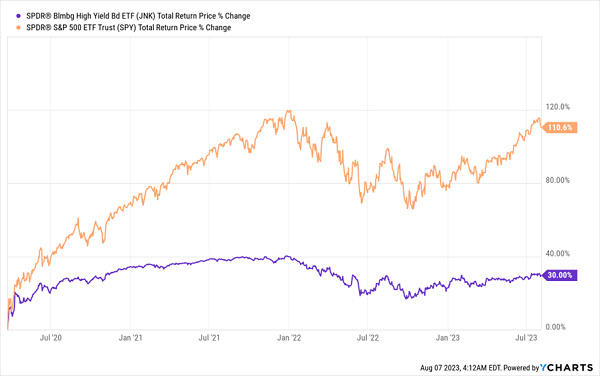

Back in 2020, when the pandemic hit, corporate-bond yields soared, and suddenly $100,000 annual income could be bought by investing just $878,734 in high-yield bonds (because yields and prices move in opposite directions). And while that is a cheap retirement, stocks were still the better option.

Stocks Beat Bonds Following the March 2020 Mess …

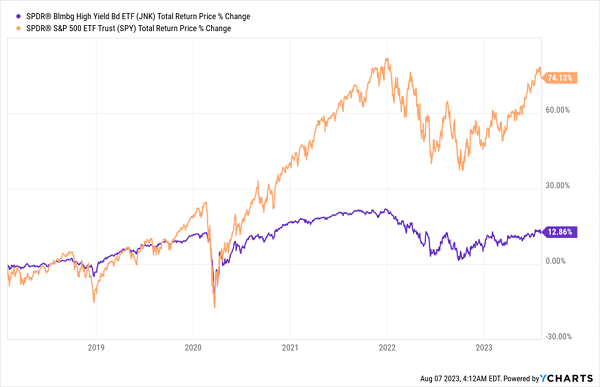

Similarly, the 2018 spike was because of another market panic that was a buying opportunity for stocks.

Similarly, the 2018 spike was because of another market panic that was a buying opportunity for stocks.

… And Again After the 2018 Panic

It makes sense that stock returns were better from the pandemic to now versus from the 2018 selloff to now (which, like 2022’s selloff, was due to interest rates rising) because the pandemic was a particularly difficult time to be a contrarian and buy, like we did at CEF Insider (and did again in 2022, locking in safe 8%+ yields in the process).

It makes sense that stock returns were better from the pandemic to now versus from the 2018 selloff to now (which, like 2022’s selloff, was due to interest rates rising) because the pandemic was a particularly difficult time to be a contrarian and buy, like we did at CEF Insider (and did again in 2022, locking in safe 8%+ yields in the process).

It also makes sense that stocks would do better than bonds, even taking into account bond-interest payments, as the charts throughout this article do.

The reason is simple: because stocks don’t pay out steady payments like bonds and fluctuate more in value, they provide higher returns over the long term; bankers call this a liquidity premium. When bond yields peaked in 2020 and 2018, buying stocks ended up earning you more money than buying bonds for this reason.

This time is different. That’s always a dangerous thing to say in finance, but we know it’s different because in 2018 and 2020, the market organically caused interest rates to rise as it sold off bonds, and in 2022, the interest-rate hikes were inorganic, caused, as they were, by Jay Powell and the Fed.

Back in 2018, markets panicked because investors thought a small (and, at the time, good for the economy) increase in the Fed’s benchmark rate would cause a pullback. Then they realized they were overreacting.

This time, the Fed has hiked interest rates over 2,000% in a year and a half, the most aggressive and extreme interest-rate hiking in the central bank’s history.

As a result, the Fed’s interest rate rose to 5.5%. That means that you will get 5.5% if you lend money to a bank overnight. Longer-term rates should be higher, and riskier rates should be higher, too. Which is why corporate bonds are now yielding over 8.3%.

In other words, buying corporate bonds today basically locks in an 8.3% return.

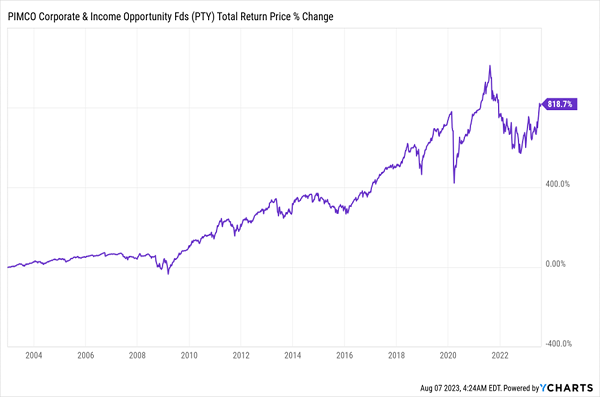

This is for a few reasons. First, if bond interest rates go up or down, the yield on a buy made today will keep paying that same amount, and you can diversify through a corporate-bond closed-end fund (CEF) like the PIMCO Corporate Opportunity Income Fund (PTY). Since only around 2% to 3% of all corporate bonds default, and these funds diversify into hundreds of bonds, your risks go toward zero.

Decades of Strong Returns

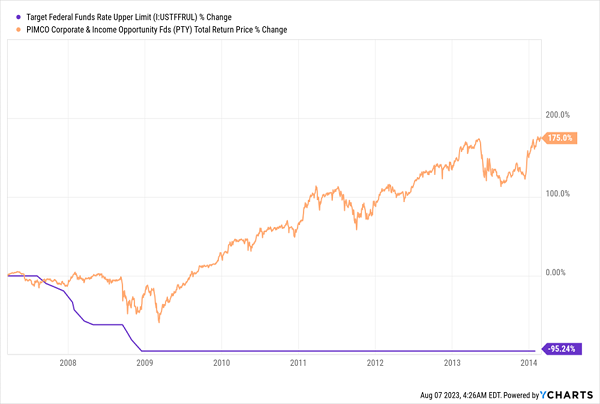

If bond interest rates go down (like if the Fed cuts rates due to a recession), these bonds are likely to go up in value as investors seek higher-yielding alternatives. That would raise PTY’s net asset value (NAV, or the value of its underlying portfolio). This is what happened in 2008–2009, during the Great Recession: PTY’s asset value actually rose over the next few years as its higher-yielding bonds became more valuable.

If bond interest rates go down (like if the Fed cuts rates due to a recession), these bonds are likely to go up in value as investors seek higher-yielding alternatives. That would raise PTY’s net asset value (NAV, or the value of its underlying portfolio). This is what happened in 2008–2009, during the Great Recession: PTY’s asset value actually rose over the next few years as its higher-yielding bonds became more valuable.

A Rising NAV as Rates Collapse

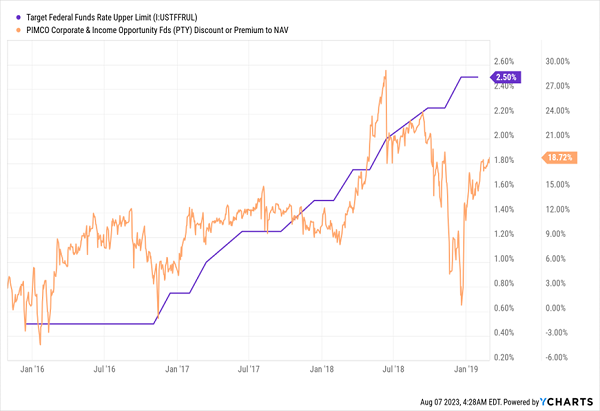

Higher rates will benefit PTY, too, as it means more demand for the fund; again we saw this when interest rates rose at a (what was then) historically unprecedented rate in the mid-2010s, causing PTY’s market price to go from a small discount to NAV to a huge premium.

Higher rates will benefit PTY, too, as it means more demand for the fund; again we saw this when interest rates rose at a (what was then) historically unprecedented rate in the mid-2010s, causing PTY’s market price to go from a small discount to NAV to a huge premium.

Market Demand for Bonds Soars

In other words, if bond yields go up or down, a fund like PTY will keep providing a high income stream (it’s at 9.8% now, thanks to PIMCO’s ability to get access to higher-quality bonds than most people can), and you’re getting the potential for strong price gains, too.

In other words, if bond yields go up or down, a fund like PTY will keep providing a high income stream (it’s at 9.8% now, thanks to PIMCO’s ability to get access to higher-quality bonds than most people can), and you’re getting the potential for strong price gains, too.

— Michael Foster

4 MORE “Financial Independence” Buys Investors Are Sleepwalking Right By [sponsor]

PTY is a great bond pick, but its 34.6% premium to NAV is far too high for my liking right now.

Better yet, my favorite high-yield pays kick out a 9.5% average dividend now, while trading at discounts so unreal I expect them to vanish fast.

End result: a forecast 20% price gain from these 4 picks, to go along with their 9.5% payout.

Click here to learn all about these secure, income-spinning 9.5% yielders now, including a powerful “buy signal” they give off when they’re about to surge (hint: they’re delivering this signal, loud and clear, right now).

Source: Contrarian Outlook