The stock market has been on an absolute tear this year with the S&P 500 up 19% and the Nasdaq 100 up a whopping 42.6% YTD.

Stock Strength Nearing Exhaustion

Now, while I have no interest in trying to call a top in this market, the indexes have clearly moved into overbought territory, at least in the near-term. The mega-cap technology stocks in particular have accounted for much of the market’s returns, so a rotation out of the sector wouldn’t be unreasonable at this time.

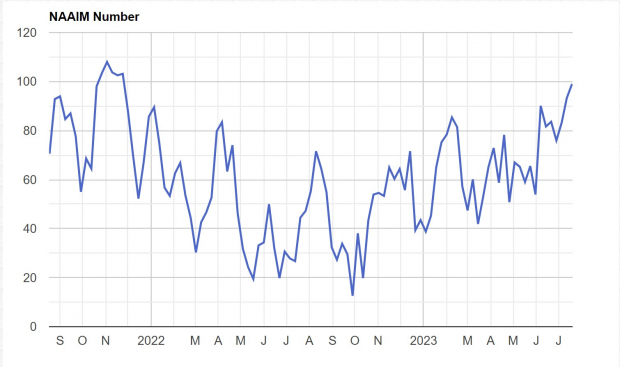

As measured by the NAAIM Exposure Index, which shows the average exposure to US equities reported by the survey members, active fund managers are very long stocks. The index is now above 99%, the highest reading since 2021, and all while markets are near YTD highs. This indicator is not predictive, so is not a sell signal, but is worth considering when making trading decisions.

Image Source: NAAIM

Image Source: NAAIM

Dividend Growth Stocks

If you are concerned about the massive rallies in tech leading to sharp corrections, then taking profits or adding other positions would be a prudent move. One place to look for solace when the broader stock market corrects is dividend stocks, even better when they have a long history of raising their payments.

Companies that have raised their dividend yield for many consecutive years often provide additional degrees of security and can function almost similar to a bond, while offering the upside of a stock.

In this article, I will cover three dividend aristocrats that have raised their dividends for a minimum of 29 years consecutively, and have high Zacks Ranks, further improving their near-term expectations. T. Rowe Price (TROW), Roper Technologies (ROP), and West Pharmaceutical Services (WST) all have the potential to be appealing investments if the markets take a turn lower.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

West Pharmaceutical Services

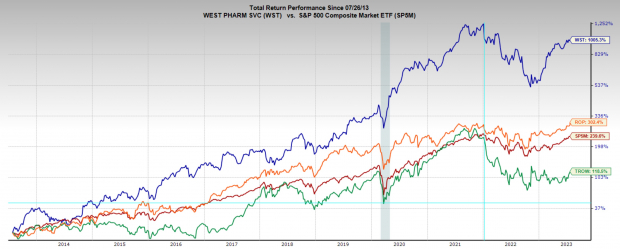

West Pharmaceutical Services has been an exceptional stock to own over the last decade, compounding at annual rate of 27.1% over that period.

WST is a global healthcare company that specializes in the design, development, and manufacturing of innovative pharmaceutical packaging and delivery systems. They offer a wide range of products, including vial seals, stoppers, prefillable syringe systems, and self-injection devices, catering to the pharmaceutical, biotechnology, and medical device industries.

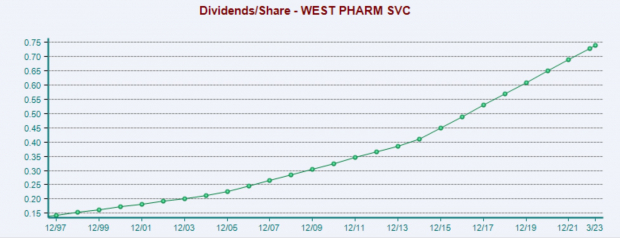

WST has raised the dividend payment for 29 years consecutively. Over the last five years the dividend has been increased by an average of 6.2% annually. Although the dividend yield is on the smaller side at 0.2% you can almost guarantee that it will continue to rise for years to come.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

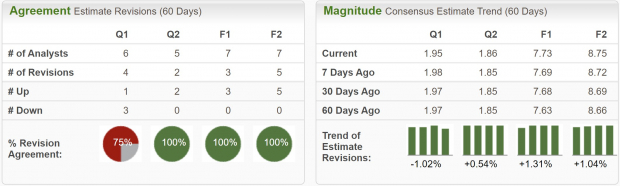

Though current quarter earnings estimates have been revised lower over the last two months, estimates have been upgraded unanimously across all forward timelines. FY23 earnings estimates have been revised higher by 1.3%. FY24 earnings have been revised higher by 1% and are projected to grow 13.1% YoY.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

T. Rowe Price

T. Rowe Price is a renowned global investment management firm based in the United States. With a history spanning several decades, the company provides a wide range of investment products and services to individual and institutional investors.

TROW is known for its expertise in actively managed mutual funds and has expanded its offerings to include other investment vehicles like exchange-traded funds (ETFs) and separately managed accounts. The firm is recognized for its commitment to research-driven investment strategies and has established a strong reputation within the financial industry.

T. Rowe Price has a hefty dividend yield of 4.1% and has raised the payment by an average of 14.4% annually over the last five years. Additionally, management has raised dividends for 36 consecutive years. Additionally, demonstrating upward trending earnings revisions, TROW currently has a Zacks Rank #2 (Buy) Rating.

TROW is trading at a one-year forward earnings multiple of 17.8x, which is below the market average of 21.3x, and just above its 10-year median of 16x.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Roper Technologies

Roper Technologies is a diversified technology company with a global presence. It operates in various industries, including healthcare, transportation, energy, and water, providing specialized software, equipment, and solutions to its customers.

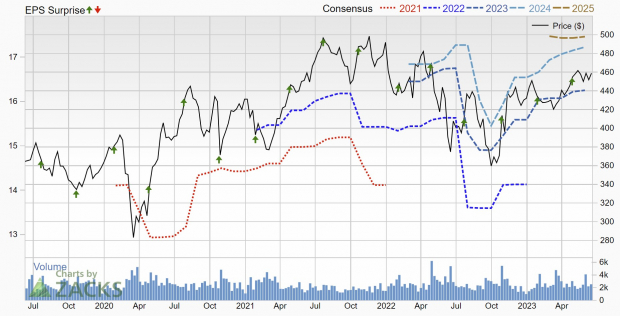

Roper Technologies has quite a stranglehold on the industries it makes products for, and just reported better than expected earnings Friday, July 21. EPS of $4.12 beat estimates of $3.99 and sales of $1.53 billion beat estimates of $1.5 billion.

Shares are rocketing nearly 4% higher in trading Friday, and the stock is now just 1% below its all-time high. Roper Technologies earnings call was highlighted by 17% growth in FCF in the year, significantly expanded recurring revenue customer base, and raising of FY23 earnings guidance to $16.36 – $16.50.

Roper Technologies currently has a Zacks Rank #2 (Buy), indicating upward trending earnings revisions.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The company has a 29-year track record of raising dividends and currently offers a yield of 0.6%. Additionally, ROP has raised its dividend payment by an average of 10.7% annually over the last five years.

Roper Technologies is trading at a one-year forward earnings multiple of 29.7x, which is below the industry average of 34.4x, and above its 10-year median of 26.1x.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Bottom Line

Given the extended state of the stock market, I wouldn’t blame any investors for looking to peel off their more profitable positions. However, if you are looking for places to put that money to work, I would recommend looking at dividend growth stocks like those listed above, as they can perform better than the broad market during selloffs.

— Ethan Feller

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks