The stock market is my favorite store. And high-quality dividend growth stocks are my favorite merchandise. But this merchandise is just like any other in one specific way.

We all want value for money. We want a good deal.

Stock prices are changing constantly, but business value? Not so much. And so buying when there’s a favorable disconnect between price and value can do wonders for your ability to build wealth.

When dealing with dividend growth stocks, a lower price can do more than just that. Price and yield are inversely correlated. All else equal, lower prices result in higher yields.

That means more passive dividend income on the same invested dollar. So it’s more dividend income being collected while you build more wealth over the long run. I call that a win-win.

Today, I want to tell you about five dividend growth stocks that are down more than 20% from their recent highs.

Ready? Let’s dig in.

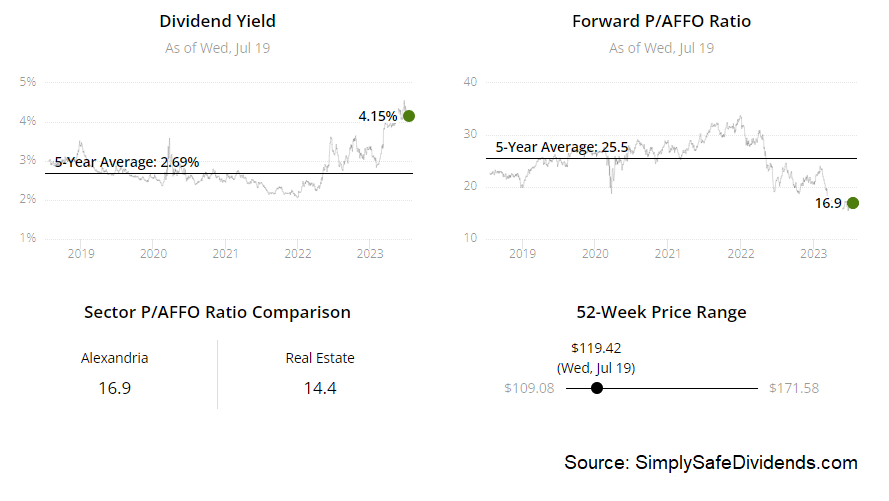

The first dividend growth stock we have to talk about is Alexandria Real Estate Equities (ARE). Alexandria Real Estate is life science and technology real estate investment trust.

This is a really interesting situation. REITs, in general, are unpopular right now. That’ll happen when rates are higher, which increases interest expenses and creates competition for yield on the equity side. But office building REITs, in particular, are extremely unpopular right now. With remote/hybrid work showing real legs, many office-focused REITs are struggling.

But Alexandria Real Estate is not a typical office operator. Its properties are built-for-purpose laboratories. It’s pretty tough to do medical research in your spare bedroom. That explains the high occupancy rate of almost 94% and rent collection rate of just under 100%. These solid fundamentals underpin the solid, growing dividend.

The REIT has increased its dividend for 13 consecutive years. The 10-year DGR of 8.7% is actually quite strong for a REIT. Many REITs have low-single-digit dividend growth rates. But not Alexandria Real Estate. These are prime properties in prime locations. And you get to pair that high-single-digit dividend growth rate with the stock’s market-smashing yield of 4.2%.

Based on midpoint guidance for this year’s adjusted FFO/share, the payout ratio is 55.4%. Many of the REITs that I’ve seen out there have payout ratios of 70% or 80%… or even higher, so this payout ratio stands out – in a good way. But none of this seems to matter to the market. This stock is down 31% from its 52-week high.

When there’s a herd rushing for the exits, there’s no time to be discriminating. With the problems facing traditional offices, anything that even smells like an office REIT is a baby getting thrown out with the bathwater. But, again, these buildings aren’t traditional offices.

When there’s a herd rushing for the exits, there’s no time to be discriminating. With the problems facing traditional offices, anything that even smells like an office REIT is a baby getting thrown out with the bathwater. But, again, these buildings aren’t traditional offices.

These laboratories continue to be in demand from some of the biggest companies in healthcare that require research facilities for continued R&D. This stock’s 52-week high of $172.65 is long gone. The stock’s pricing is now trending around $120, which isn’t far from the 52-week low. Its P/CF ratio of 14 is nearly half of its own five-year average of 24.5. Take a look at this one.

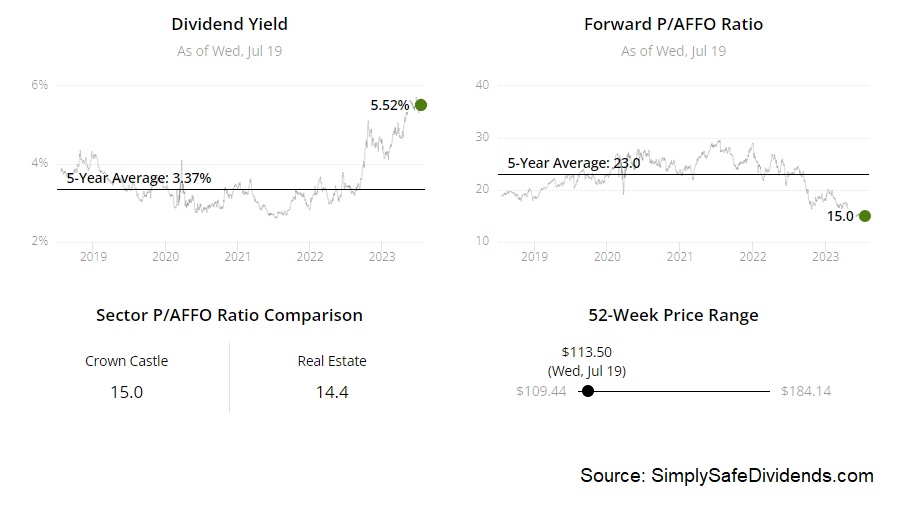

The second dividend growth stock that I have to highlight is Crown Castle (CCI). Crown Castle is a communications infrastructure real estate investment trust.

Yep. Another REIT. And why not? They’ve been absolutely hammered. Now, I do think you have to be careful with REITs. Plenty of debt. And growth isn’t as amazing as other areas of the market, like tech. Plus, many REITs could be in terminal decline. Think traditional office buildings. Or indoor shopping malls. But Crown Castle is none of that. It’s not even “real estate”, really.

This REIT owns infrastructure like communications towers and fiber. With mobile communications becoming more common, necessary, and important than ever before, this company’s infrastructure is more valuable than ever before. By the way, its dividend might be more valuable than ever before.

This REIT has increased its dividend for nine consecutive years. And with a five-year DGR of 8.9%, we have another REIT that bucks the slow-growth trend. And, circling back around to the point I just made about the value of this dividend, the stock’s current yield is 5.4%. That is as high as I’ve ever seen it. For perspective, that’s 200 basis points higher than its own five-year average. Incredible.

Now, one area of minor concern is the payout ratio. Based on this year’s AFFO/share guidance, at the midpoint, the payout ratio is 82%. That’s elevated. Not an emergency. But I do suspect very modest dividend growth in the near term, which will alleviate some of the pressure.

Speaking of pressure, this stock has had it. And I mean downward pressure. As in 37% lower than its 52-week high. The 52-week high is $184.92. Current pricing? A bit under $116. Growth isn’t what it once was. The market is a bit saturated. So I understand the need for a correction to what was a premium valuation. Has it been overdone, though? Perhaps.

Speaking of pressure, this stock has had it. And I mean downward pressure. As in 37% lower than its 52-week high. The 52-week high is $184.92. Current pricing? A bit under $116. Growth isn’t what it once was. The market is a bit saturated. So I understand the need for a correction to what was a premium valuation. Has it been overdone, though? Perhaps.

The P/CF ratio of 17.2 is significantly lower than its own five-year average of 23.3. Anyone who bought this stock at, or around, its 52-week high is suffering. And that’s unfortunate. But it’s important to never egregiously overpay. With the near-40% drop in pricing, I think the valuation has come down to a pretty reasonable level.

The third dividend growth stock we should go over is Fifth Third Bancorp (FITB). Fifth Third is a diversified regional bank holding company.

Out of the frying pan, into the fire. REITs have been pretty tough. Some of the banks have been worse. What’s odd is that, unlike REITs, banks should be flourishing in the current interest rate environment. Indeed, many banks are flourishing.

But a few idiosyncratic bank failures, mostly caused by mismanagement, spread fear and panic across the whole industry, taking down one stock after another. This regional bank, however, has no such management issues. It’s been reporting really, really good results, like clockwork, for years now. Speaking of clockwork, the dividend gets paid and raised like clockwork.

The regional bank has increased its dividend for 12 consecutive years. A 10-year DGR of 13.1%, which is great, clues you in to just how sneakily well this bank has been rewarding its shareholders. And what’s really crazy here is that you’re able to pair the double-digit dividend growth rate with the stock’s current yield of 4.8%.

That yield, by the way, is 130 basis points higher than its own five-year average. So this stock often offers a pretty nice yield. But it’s way higher than usual. That might imply some danger. But the payout ratio is only 38.3%. I don’t see any danger at all. The only thing that has seemed to have any danger at all here is the stock, which is 28% off of its 52-week high.

That yield, by the way, is 130 basis points higher than its own five-year average. So this stock often offers a pretty nice yield. But it’s way higher than usual. That might imply some danger. But the payout ratio is only 38.3%. I don’t see any danger at all. The only thing that has seemed to have any danger at all here is the stock, which is 28% off of its 52-week high.

That’s despite no apparent danger with the business or its dividend. But that’s the stock market for you. If you’re looking for perfect efficiency and rationality, you’re looking in the wrong place. The market is made of human beings with many differences of opinion. But business results are facts. Another area of facts is pricing. The 52-week high is $38.06.

The stock’s current pricing is sitting at about $27. Unfortunate if you bought at the highs. But interesting if you didn’t and have room for a regional bank in your portfolio. We analyzed and valued this bank late last year, estimating fair value for the business at almost $42/share. Make sure this bank is on your radar.

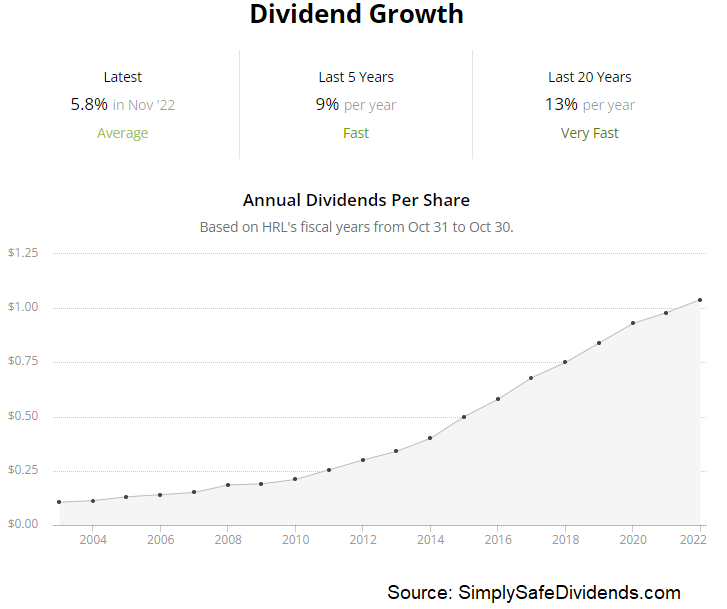

The fourth dividend growth stock we have to talk about is Hormel Foods (HRL). Hormel is an American food processing company.

This is one of the largest processors of meats in the world. Hormel also owns a variety of non-meat brands, such as Skippy peanut butter. And the thing is, we’ve all gotta eat. Hormel has been around since 1891. How has it been so enduring?

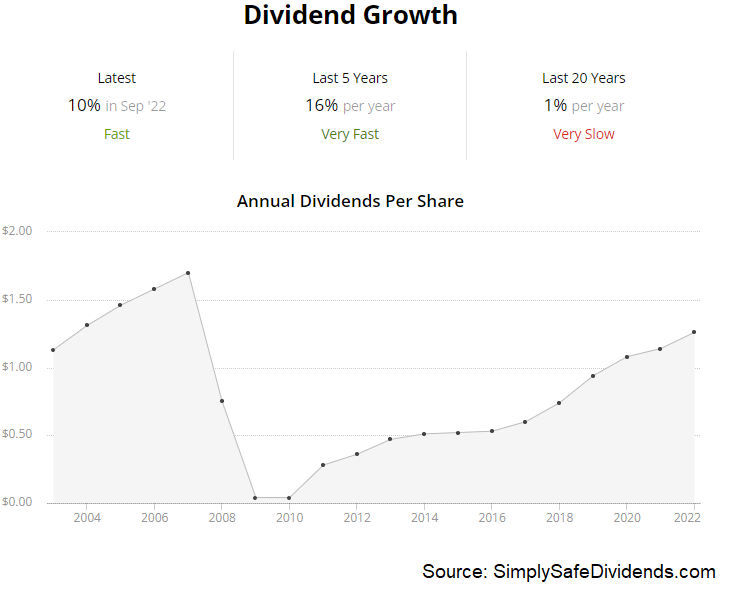

Well, I think selling basic food staples is a pretty good way to last a long time. And while stock in Hormel won’t make you rich tomorrow, it’s also tough to go broke by owning the shares. The risk is low. But the dividend is not. The food processing company has increased its dividend for 57 consecutive years.

Well, I think selling basic food staples is a pretty good way to last a long time. And while stock in Hormel won’t make you rich tomorrow, it’s also tough to go broke by owning the shares. The risk is low. But the dividend is not. The food processing company has increased its dividend for 57 consecutive years.

Talk about endurance. Nearly 60 consecutive years of ever-higher dividend payments to shareholders. Awesome. This is a Dividend Aristocrat and a Dividend King. The 10-year DGR is 13.2%, although more recent dividend growth has been in the mid-single-digit range.

Still, the stock offers a 2.8% yield. That’s 80 basis points higher than its own five-year average, so the market has been adjusting the yield higher in order to compensate for slower growth. And that’s a good call, in my view. Meantime, the payout ratio is 64.7%. A bit elevated. But the Dividend King status looks very secure. This stock’s 24% decline from its 52-week high may be a great opportunity to buy a Dividend Aristocrat while it’s weak.

Still, the stock offers a 2.8% yield. That’s 80 basis points higher than its own five-year average, so the market has been adjusting the yield higher in order to compensate for slower growth. And that’s a good call, in my view. Meantime, the payout ratio is 64.7%. A bit elevated. But the Dividend King status looks very secure. This stock’s 24% decline from its 52-week high may be a great opportunity to buy a Dividend Aristocrat while it’s weak.

If you wait until it’s all sunshine, you’re going to pay a high price. The deals tend to come when the skies are gray. That’s just how it is. Well, Hormel’s skies have lacked sunshine for some time now. The stock’s current pricing of about $39 is well off of its 52-week high of $51.69.

Every basic valuation metric I look at is indicating pretty decent undervaluation here. The sales multiple of 1.8 is quite a bit lower than its own five-year average of 2.4. Same goes for the P/E ratio of 23.2, which comes in much less demanding than its own five-year average of 26.1. Hormel isn’t my favorite business. Not the cheapest stock out there. But it’s a Dividend King that has been weak. It’s at least worth a look.

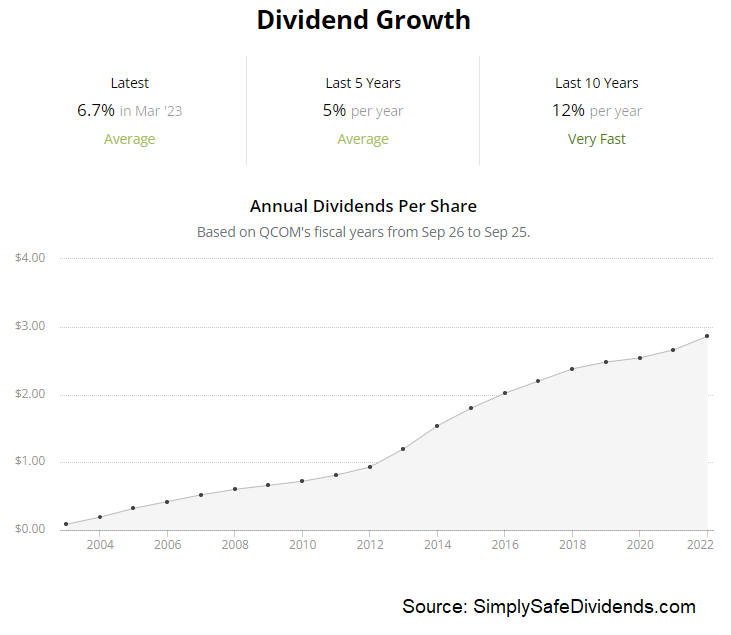

The fifth dividend growth stock that I want to highlight today is Qualcomm (QCOM). Qualcomm is a multinational technology corporation.

Qualcomm creates semiconductors, software, and services related to wireless technology and connectivity. This company has long been a leader in the wireless space. It holds virtually all essential patents used in 3G, 4G, and 5G networks.

Because of this, Qualcomm collects royalty income on the majority of 3G, 4G, and 5G handsets sold worldwide. Smartly, Qualcomm parlayed this success into a diversified business model that offers a suite of technologies and services across an entire IoT ecosystem. The company is now exposed to some of the biggest trends in all of technology, such 5G, broadband, modern RF systems, gaming, IoT, self-driving autos, AI, and AR/VR. That should mean lots of revenue and profit growth, which is translating right to the dividend.

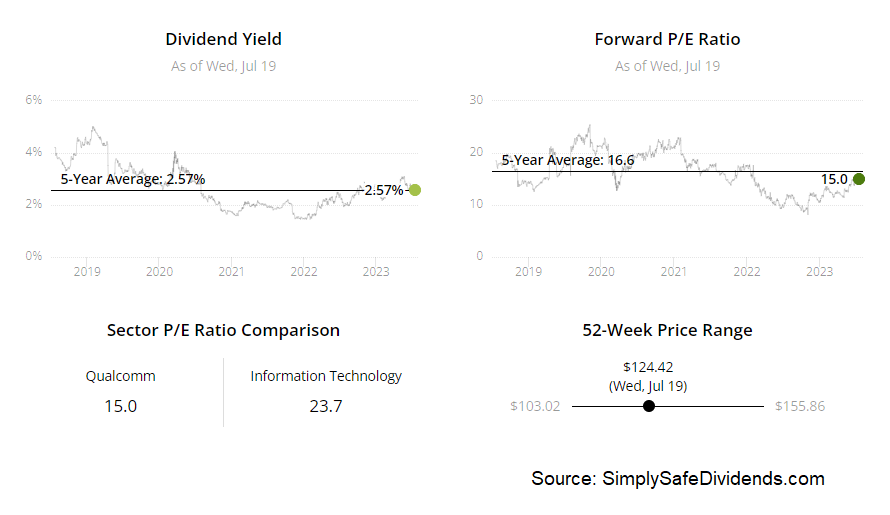

The technology corporation has increased its dividend for 21 consecutive years. Qualcomm has the makings of an upcoming Dividend Aristocrat. The 10-year DGR of 11.7% is very nice, although dividend raises have been a bit lumpy. Some of that is due to litigation around patents and royalties, but Qualcomm is sitting better than ever right now. The stock yields a market-beating 2.6%. And the low payout ratio of only 34.4% indicates no troubles whatsoever with the commitment to shareholders.

The technology corporation has increased its dividend for 21 consecutive years. Qualcomm has the makings of an upcoming Dividend Aristocrat. The 10-year DGR of 11.7% is very nice, although dividend raises have been a bit lumpy. Some of that is due to litigation around patents and royalties, but Qualcomm is sitting better than ever right now. The stock yields a market-beating 2.6%. And the low payout ratio of only 34.4% indicates no troubles whatsoever with the commitment to shareholders.

This stock is down 21% from its 52-week high. Could be a rare deal in technology. Tech stocks left and right have taken off to all-time highs on the back of AI excitement. Are there some bubbles out there? Maybe. But Qualcomm certainly isn’t in one. Its nowhere near all-time highs.

In fact, the current price of about $123 on the stock isn’t even close to its own 52-week high of $156.66. We analyzed and valued Qualcomm recently, estimating fair value for the business at a bit over $139/share. I think Qualcomm is a very interesting idea for long-term dividend growth investors.

In fact, the current price of about $123 on the stock isn’t even close to its own 52-week high of $156.66. We analyzed and valued Qualcomm recently, estimating fair value for the business at a bit over $139/share. I think Qualcomm is a very interesting idea for long-term dividend growth investors.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income