Last month, I opened a new position in my Dividend Growth Portfolio when I purchased shares of VICI Properties. They own a whole lot of the Las Vegas Strip.

Then a couple weeks later, I went to Vegas to inspect my new holdings. Here is me in one of my numerous casinos, surrounded by thousands of my closest friends at the World Series of Poker:

The inspection trip convinced me that VICI’s tenants are not in danger of failing to pay their rent anytime soon.

The inspection trip convinced me that VICI’s tenants are not in danger of failing to pay their rent anytime soon.

In this article, after I tell you about purchasing more VICI shares this month, I will update the entire portfolio. Spoiler alert: The DGP continues to do great. It now sports a new all-time record high yield on cost (YOC).

Dividend Reinvestment for July, 2023: VICI Properties (VICI)

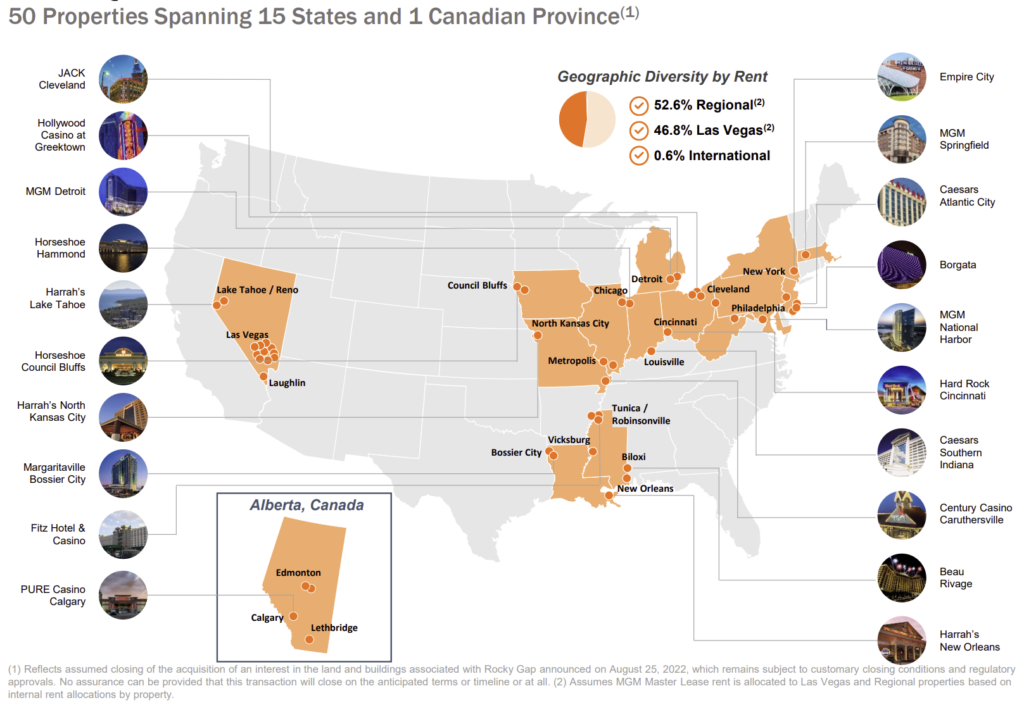

VICI Properties (VICI) is a real-estate investment trust (REIT) that invests in gaming and “experiential” properties. While headquartered in NYC, VICI has a giant presence in Las Vegas (which provides 47% of its revenue), while also owning properties across the USA and in Canada.

Source: Investor presentation

Source: Investor presentation

Please see last month’s article for a broad overview of VICI. Rather than repeat that information here, I am going to list Top 10 facts about VICI that I gleaned from its website and recent investor presentations.

- 100% of VICI’s properties follow the triple-net-lease model. That means that the tenants (not VICI) promise to pay all the expenses of the property, including property taxes, building insurance, and maintenance. These expenses are in addition to the cost of rent and utilities. (Triple-net leases are a common form of commercial real estate ownership.)

- At $51B enterprise value, VICI is the largest net lease REIT in the “experiential properties” niche.

- The weighted average lease term of VICI’s tenants is 42 years, which is much longer than typical triple-net arrangements.

- 76% of VICI’s annual cash rental income comes from two industry giants: Caesar’s Entertainment (40%) and MGM Resorts (36%). This includes those companies’ holdings not only in Vegas, but elsewhere.

- Despite Morningstar awarding an economic moat of “None” to VICI, the barriers to entry of possible competitors are enormous. VICI owns highly differentiated, non-commoditized, iconic properties along the Las Vegas Strip and elsewhere.

- VICI has experienced no cash flow volatility since it was formed in 2017. It has collected 100% of rents from all of its tenants, including during 2020 (the Covid year).

- VICI’s leases typically contain annual rent escalators. While the average of these is low (around 2% per year), many leases have CPI protection built in, and that proportion is growing. Currently at 50% of VICI’s rent-roll, CPI-protected leases are projected to rise to 85% of rent-roll over the next 10 years.

- VICI’s tenants’ businesses are not restricted to gaming. They also own large hotels, and they have massive investments in meeting and convention space, restaurants, entertainment venues, retail, and golf courses.

- VICI has raised its dividend every year since formation, with a target to pay out 75% of AFFO (adjusted funds from operations) each year. It has been right around that target every year.

- VICI has investment-grade credit ratings from all three major agencies (S&P, Fitch, Moody’s), all currently designated with “stable” outlooks.

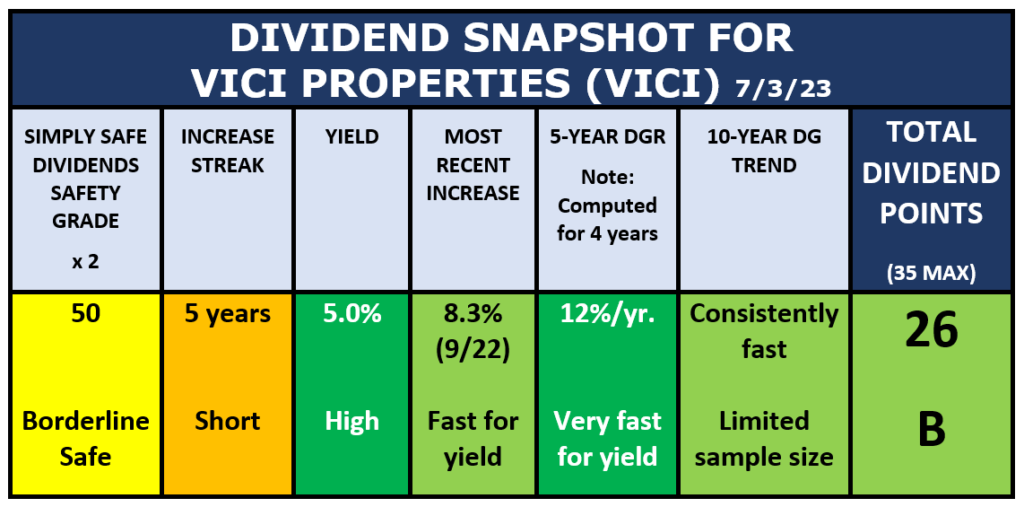

Here is VICI’s Dividend Snapshot:

Source: Author

Source: Author

Using E-Trade as a source of analyst research, 9 analysts covering VICI all have “Buy” ratings on the stock, as depicted by the green data points in the following display.

Source: E-Trade

Source: E-Trade

The research summary (above) suggests that now is a good time to buy VICI. The average price target (shown by the blue dashed line) suggests that VICI is 16% undervalued at this time. The fair-value computational service Alpha Spread posits that VICI is 27% undervalued.

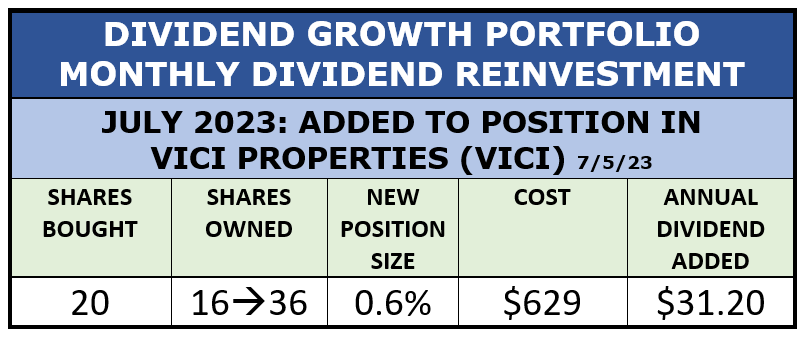

So, taking all of the data about VICI into account, and adding my positive hunch about Las Vegas into the mix, I decided to buy more shares in VICI Properties (VICI) as this month’s dividend reinvestment.

Here is what I did:

Source: Author

Source: Author

The net effect of opening the new position in VICI:

- More than doubles the size of my VICI position.

- Adds $31 to the portfolio’s annual dividend run-rate.

- Leaves $153 in the dividend kitty to put towards next month’s reinvestment.

Update of Full Portfolio

Now let’s review the portfolio as a whole.

I started the DGP in 2008 to demonstrate dividend-growth investing. The portfolio is real, the holdings are actual, and all decisions about managing the portfolio have been made in real time. This is not a hypothetical or “model,” nor is it a back-test.

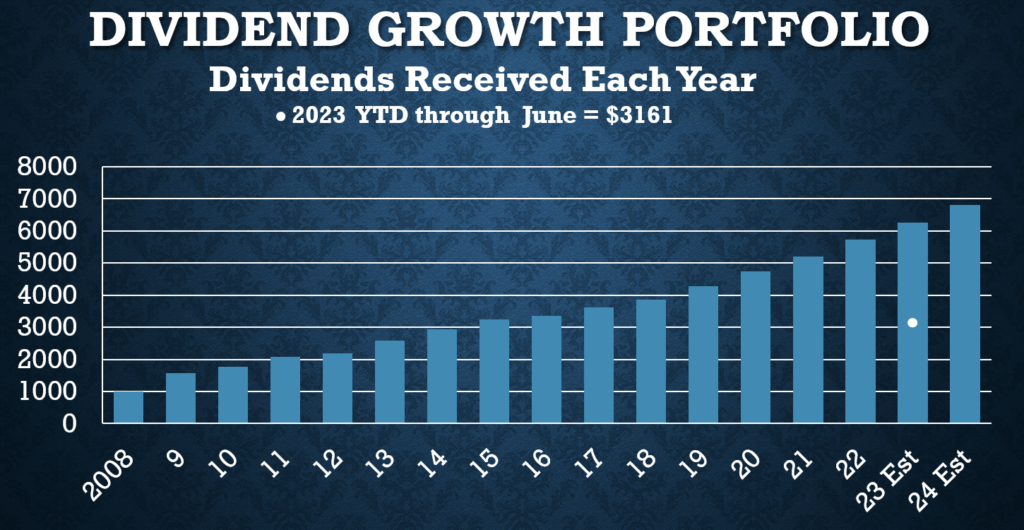

The main financial goal of the portfolio is to generate a reliable, ever-increasing stream of dividends in meaningful amounts, which it has done:

Source: Author

Source: Author

In the display above, I have added my first projection for 2024’s dividends. The estimate is modest: A 9% increase over my estimate for 2023.

The 2023 estimate, in turn, is simply the sum of dividends already collected this year ($3161) plus dividends expected over the remainder of the year. The actual total collected should be higher than that, because dividend increases to be announced through the rest of the year are not included yet, nor are “new” dividends to be collected from shares bought via dividend reinvestments in the last five months of 2023.

As a directional indicator, the dividends collected so far (through the end of June) in 2023 have been about 10% more than the dividends collected last year in the same time.

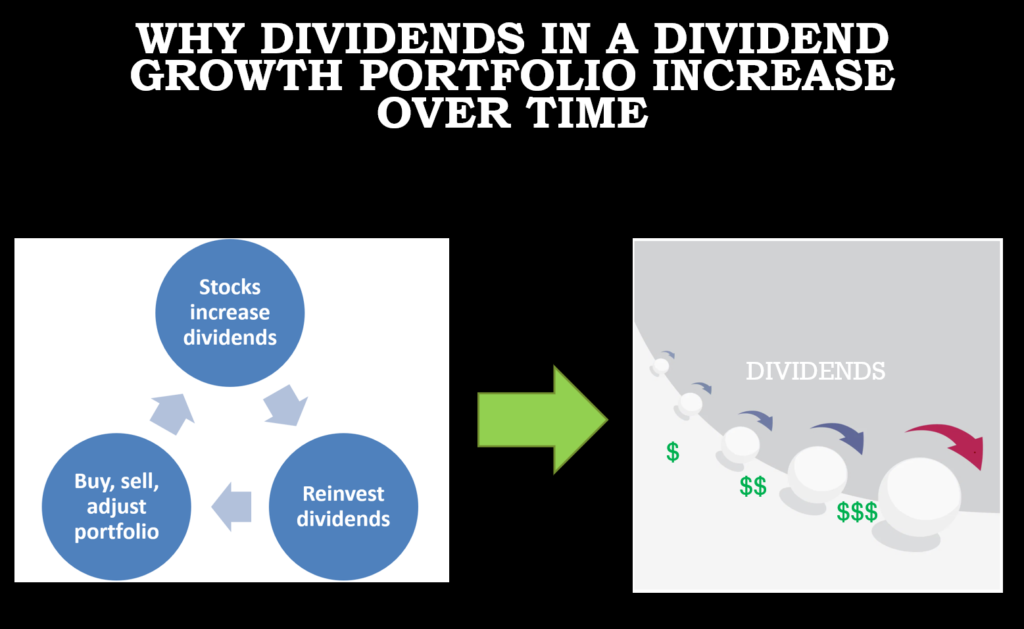

I hope that explanation was not confusing. The whole process of constant dividend growth in this kind of portfolio is actually quite simple.

There are three reasons that dividends go up in a DG portfolio, as shown by the three blue circles on this chart:

Source: Author

Source: Author

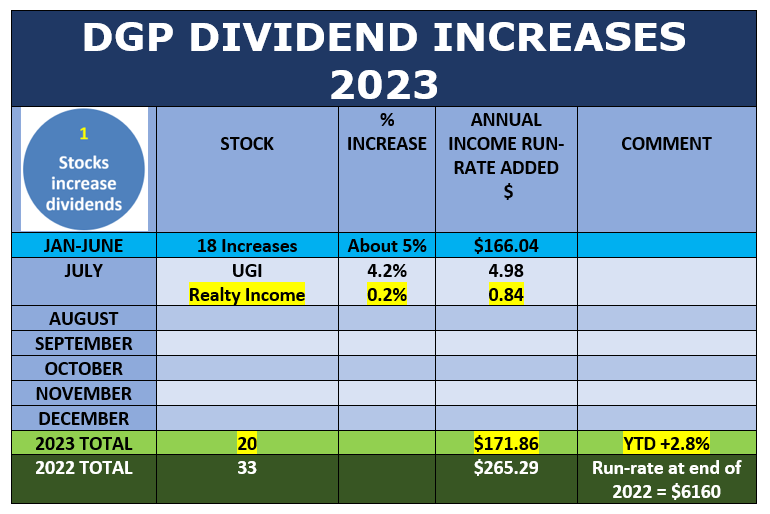

Reason #1. Stocks increase their dividends

The following table shows the DGP’s dividend-increase record so far in 2023. Note that I have scrunched the table down by combining January-June into a single line.

Source: Author, from company announcements

Source: Author, from company announcements

Just one company announced an increase since last time, and that is highlighted in yellow, along with the new totals at the bottom.

Overall, dividend increases are on pace to add about 5% to the portfolio’s annual dividend run-rate this year. They have already added 2.8%. I expect around 13 more increases to be announced by the end of the year.

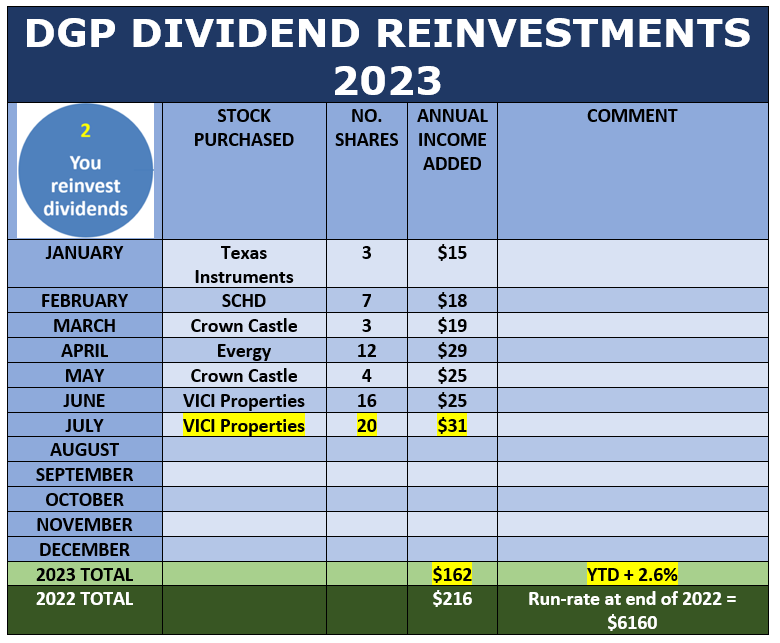

Reason #2. Dividend reinvestments

The second reason the portfolio’s overall dividends go up is that I reinvest them monthly. Since dividends are paid per share, each additional share that I buy causes the portfolio’s income to increase.

The table below shows how my dividend reinvestment program is going so far in 2023.

Source: Author

Source: Author

At the YTD pace, it looks like the reinvestments will add upwards of 3.5% to the portfolio’s annual dividend run-rate by the end of 2023.

And, in the good-news department, the extra $31 per year from the new VICI shares pushes the portfolio’s yield on cost to a new all-time high of 13.7%. Translation: The portfolio is now returning 13.7% of my of my original investment (with which I started the portfolio in 2008) per year in the form of cash dividends.

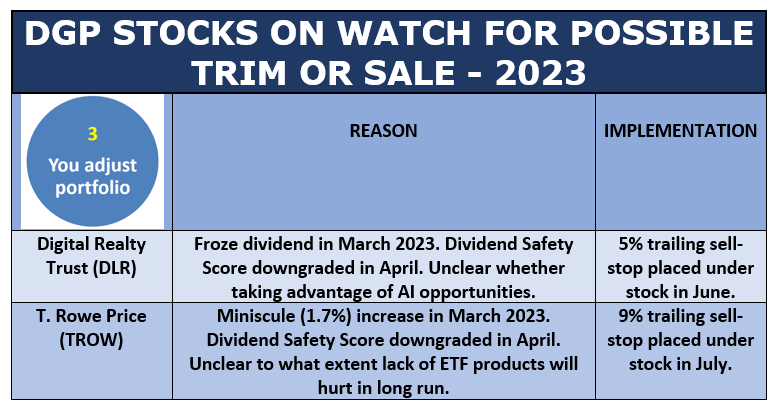

Reason #3. Portfolio adjustments

The third reason that dividends go up is via standard portfolio management activities, such as trimming or selling a stock, deciding how to replace it, and executing those decisions.

I did not make any such changes in June. But I have two stocks under the microscope for possible trimming or selling outright.

Both stocks – Digital Realty Trust (DLR) and T. Rowe Price (TROW) – disappointed with dividend increases in March, and both were downgraded by Simply Safe Dividends in April. I have put a trailing sell-stop under each stock.

Both stocks – Digital Realty Trust (DLR) and T. Rowe Price (TROW) – disappointed with dividend increases in March, and both were downgraded by Simply Safe Dividends in April. I have put a trailing sell-stop under each stock.

Interestingly, right after I put the trailing stop order under DLR a month ago, its price started going up. But the trailing stop follows the price up, lurking 5% behind. If the stock hits a wall and goes down more than 5% from whatever high it reaches, the trailing sell order will kick in, and the stock will be sold automatically. Of course, I can change these conditions any time that I want.

I just put a 9% trailing stop underneath TROW. I made this stop wider, because TROW makes its money from percentage fees based on assets under management (AUM). As the market goes up and down, TROW’s price tends to mirror those changes, over which TROW has no control.

My concern with TROW is not that cyclicality. Rather it is with TROW’s failure to enter the low-cost ETF business in an era when most investors are on the prowl for cheaper ways to invest. I would like to see TROW enter that business. They certainly have the investing acumen to do so. What I cannot determine is whether they wish to offer lower-cost funds to investors, or perhaps whether they know how to market such products.

Over the years, I haven’t churned the DGP very much. Every stock or fund I buy is one that I expect to hold “forever.” Not everything works out that way, but my portfolio turnover rate rarely exceeds 10% per year, and some years it is zero.

That brings us to the end of this month’s DGP review. If you want to see the positions in the portfolio at any time, its status as of the end of the previous month is always available here. That link also has an archive of all the articles and videos that I have published about the portfolio.

Thanks for reading!

-–Dave Van Knapp

The name of the ONE stock (ticker symbol and all) that has helped over 170,000 people discover how to gain their financial freedom... Learn More.

Source: Dividends & Income