Three years ago, I might have seen one Tesla on Charlotte-area roads every week or two. Now I see dozens pretty much every day — including the Model X that my daughter and son-in-law drive.

And Tesla (TSLA) doesn’t make the only electric vehicles out there, as manufacturers in the United States and around the world ramp up EV production.

According to a recent article put out by the International Energy Association:

Global sales of electric cars are set to surge to yet another record this year … leading a major transformation of the auto industry that has implications for the energy sector, especially oil.

The new edition of the IEA’s annual Global Electric Vehicle Outlook shows that more than 10 million electric cars were sold worldwide in 2022 and that sales are expected to grow by another 35% this year to reach 14 million. This explosive growth means electric cars’ share of the overall car market has risen from around 4% in 2020 to 14% in 2022 and is set to increase further to 18% this year, based on the latest IEA projections. …

“The trends we are witnessing have significant implications for global oil demand,” said IEA Executive Director Fatih Birol. “The internal combustion engine has gone unrivalled for over a century, but electric vehicles are changing the status quo. By 2030, they will avoid the need for at least 5 million barrels a day of oil.”

Which brings me to my June selection for our Income Builder Portfolio: Chevron (CVX).

chevron.com

What was I thinking? Well, simply stated, oil will remain vital to every nation on every continent for years to come.

If 18% of the vehicles on the road this year will be electric, as the IEA article stated, that means 4.5 times that many will still be sucking down gasoline. If 5 million barrels a day will be “avoided” in 2030, it still means 17 million barrels a day will be used in the United States alone.

And Chevron is no run-of-the-mill business. It’s the third-largest oil company in the world … it explores for, extracts and refines “black gold” … it’s a major supplier of natural gas … it’s making advancements in renewable energy sources … and it’s a free-cash-flow machine.

It remains one of the largest and most important companies in the world, and I believe that will be the case for a long time.

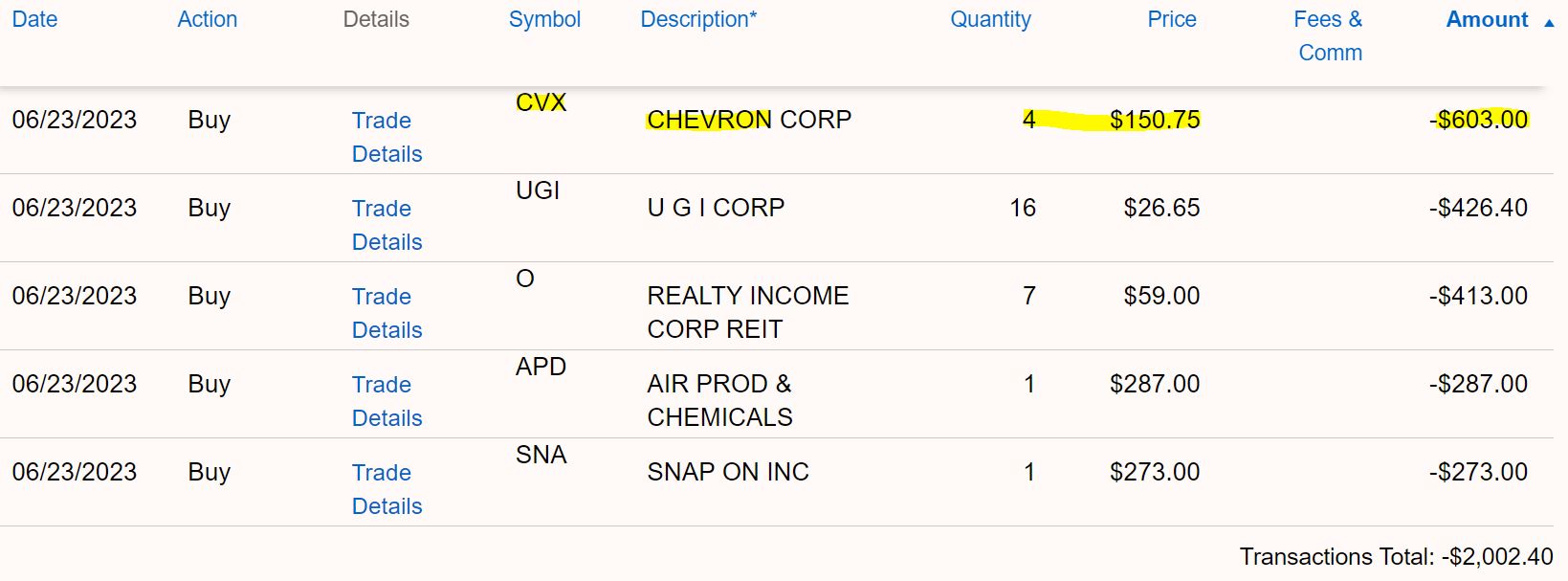

That’s why I selected Chevron for the IBP twice in 2019, and it’s why I just executed a purchase order for 4 more shares of CVX on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

schwab.com

As you can see, I used the rest of Greg’s $2,000 monthly allocation on UGI Corp. (UGI), a utility we added to the portfolio just last month; real estate investment trust Realty Income (O); industrial-gas company Air Products & Chemicals (APD); and commercial tool-maker Snap-on (SNA).

UGI, APD and SNA had been the portfolio’s smallest holdings. And I’m always looking for excuses to add to O, the wonderfully reliable REIT that has dubbed itself “The Monthly Dividend Company.”

I’ll have a little more on those four later. First, let’s do some digging into Chevron.

What’s Up With CVX?

Like all oil companies, Chevron was hurt by a worldwide glut from 2014-16. And then, just when CVX had recovered almost all the way, the pandemic had a chilling effect on commerce and oil prices — as well as the company’s profits and, ultimately, its stock.

As COVID-19 vaccines made it possible for some sense of normalcy to resume, consumers started spending again big-time. They took overseas flights, they made long car trips, they bought vehicles, they fixed up their houses, they did what consumers do: spend lots of money.

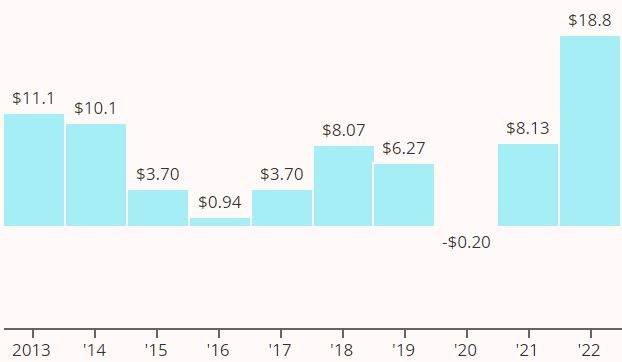

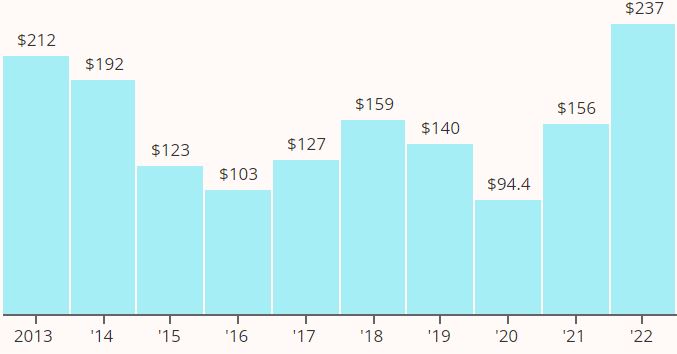

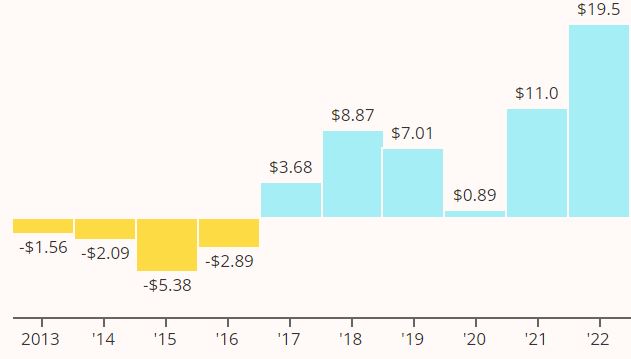

Chevron rode the wave, and 2022 was one of the company’s best years ever — as the following graphics from Simply Safe Dividends illustrate.

EARNINGS PER SHARE

SALES ($B)

FREE CASH FLOW PER SHARE

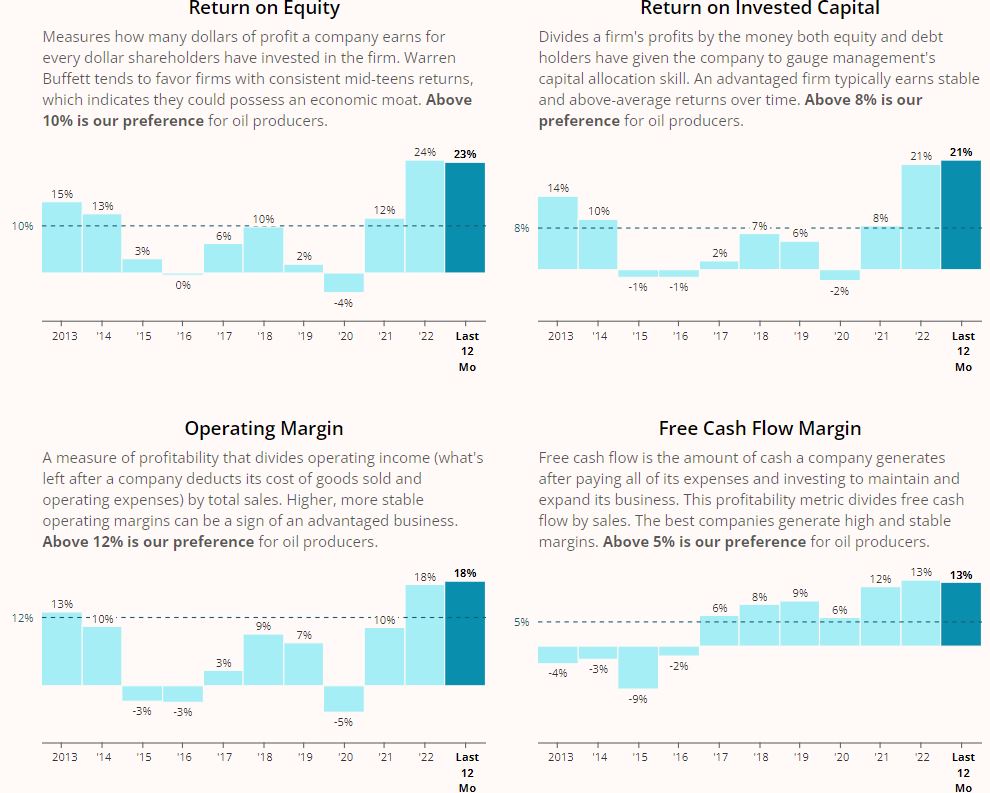

With all of that financial growth came vastly improved margins for Chevron.

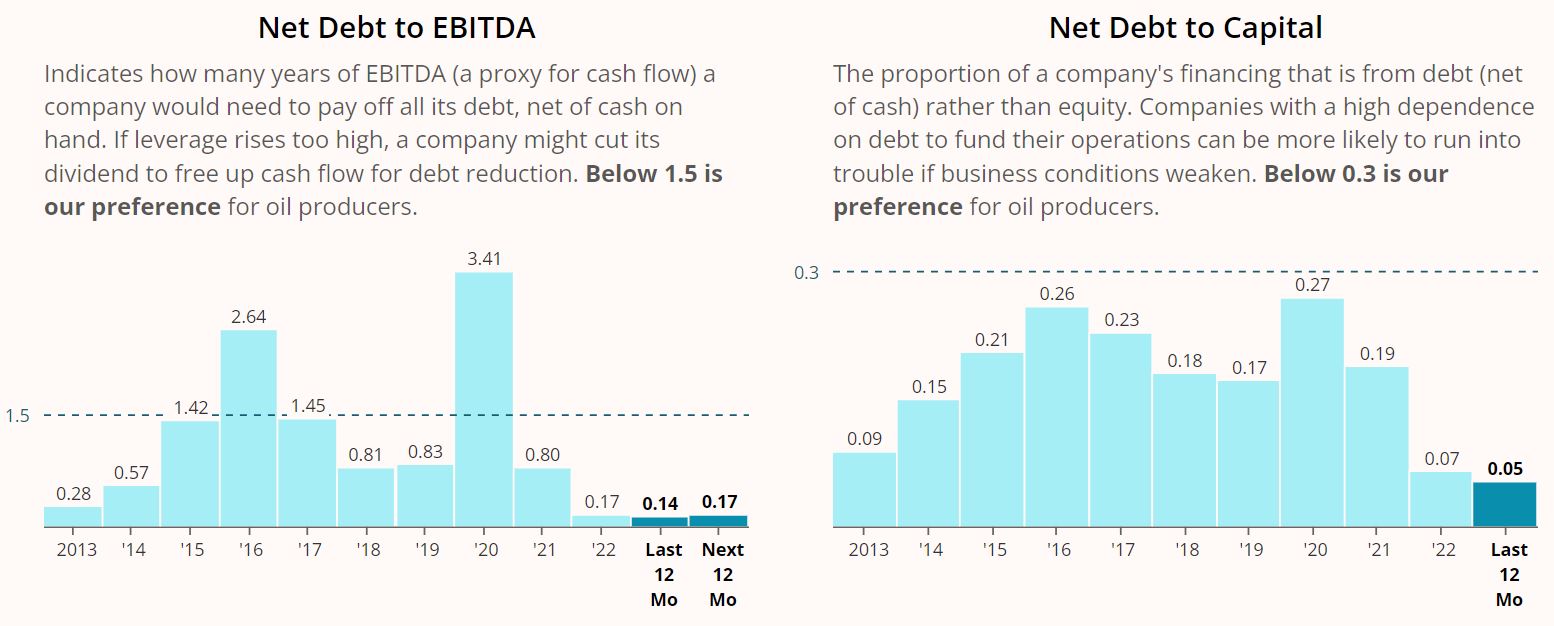

Meanwhile, Chevron management did a wonderful job of reducing the debt load it had built up during the struggles of previous years.

The debt reduction led Simply Safe Dividends to boost Chevron’s dividend safety score from 65 (near the bottom of the “safe” zone) to 90 (solidly in the “very safe” range). I’ll have a lot more on Chevron’s dividend later.

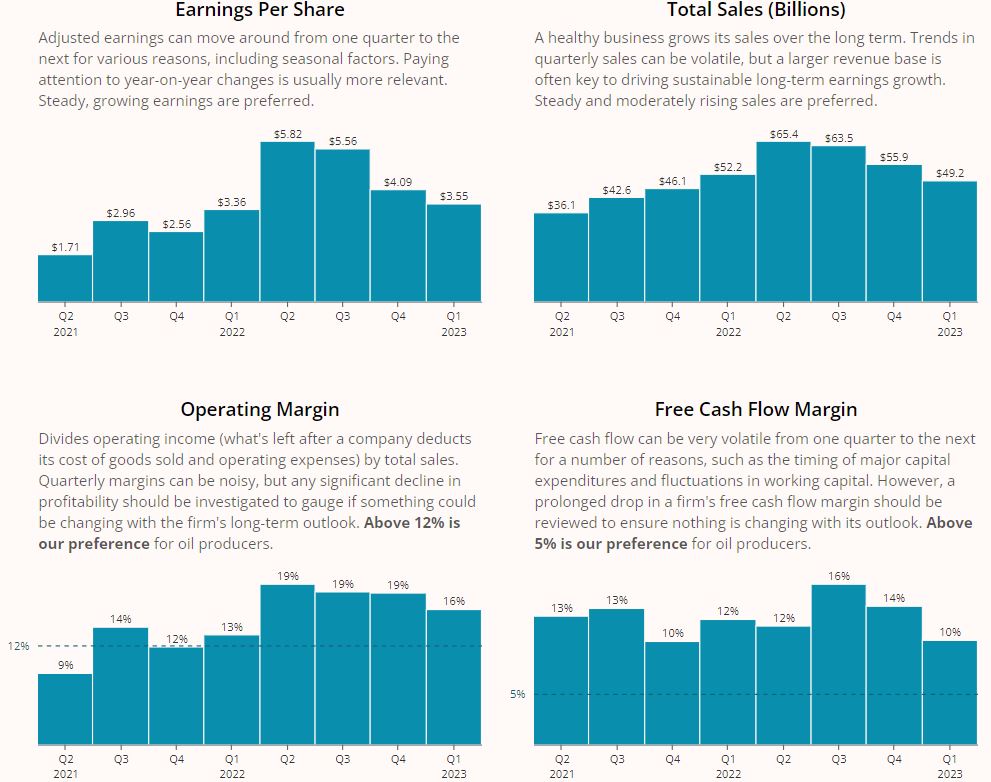

The most recent quarter’s financials weren’t awful, but they were nowhere near as impressive. Earnings grew only 6% year-over-year, and sales actually fell by 6%. Margins were adequate but hardly eye-popping.

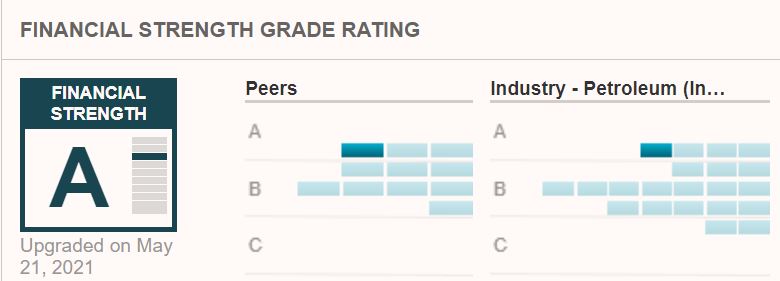

Still, we’re talking about a financially strong company. Value Line gives Chevron a solid A in that category, ranking it as the industry leader.

valueline.com

For that matter, Chevron gets numerous good “quality grades” from various analytical and ratings services. That’s also largely true of the other four companies whose IBP stakes we increased with our June buys.

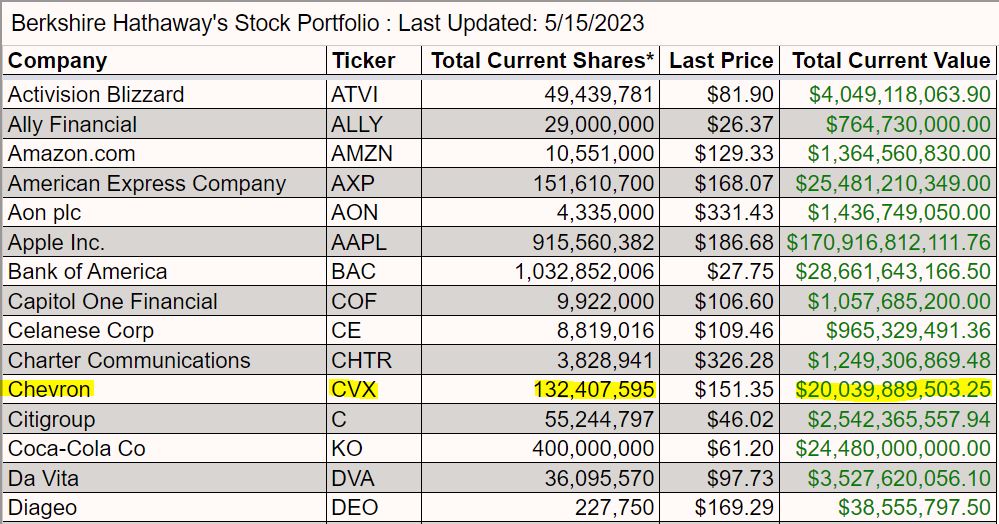

Warren Buffett sure thinks Chevron is a high-quality investment. His Berkshire Hathaway (BRK.B) holds about 132 million shares valued at roughly $20 billion, making it BRK’s fifth-largest position.

DailyTradeAlert.com

Buffett actually has reduced the CVX stake by some 33 million shares this year while building up Occidental Petroleum (OXY). Nevertheless, Berkshire still has almost twice as much CVX as OXY. And the combined $32 billion CVX/OXY investment shows that Buffett remains high on the industry.

In May, Chevron moved to increase its U.S. oil presence even more by acquiring shale producer PDC Energy.

CFRA’s Stewart Glickman likes the acquisition, and says CVX shareholders should like it, too:

We estimate the deal price at a remarkably attractive 2.8x multiple of enterprise value to projected 2024 EBITDA. Strategically, the deal adds acreage in both the Permian Basin and the DJ Basin, although we think the latter is the key to the deal, as the incremental acreage is largely adjacent to CVX’s own footprint, and should enable improvements in unit economics. If completed, we expect the deal to be accretive to earnings and cash flow.

Despite all of Chevron’s attributes, my friend and esteemed colleague Dave Van Knapp eliminated CVX from his Dividend Growth Portfolio last year, explaining:

I became less appreciative of its business model over the past few years because of how much – almost totally – the business model depends on the price of oil, over which Chevron has no control at all.

Each investor must establish his or her own portfolio guidelines, and I don’t blame Dave one iota for making that move. Those very concerned about that issue shouldn’t invest in Chevron or any company whose bottom line is affected by commodity prices.

I’m comfortable with Chevron in the IBP (and in my personal portfolio, where I have a rather large stake) because I consider it to be the best-managed company in an essential industry.

Valuation Station

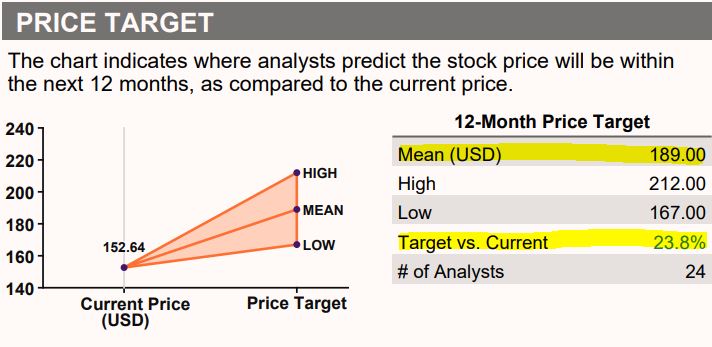

Many analysts believe Chevron is attractively valued, as a recent drop in the price of oil has created a buying opportunity for the stock.

For example, the 24 monitored by Refinitiv have established a mean 12-month target price of $189, suggesting a nearly 25% upside. Even the lowest price projection ($167) is about 11% higher than what we just paid for the stock.

Refinitiv, via fidelity.com

Value Line is especially bullish on Chevron’s mid- and long-term prospects, with a median 18-month target price ($210) that suggests 40% upside, and with an astounding forecast calling for the stock price to double or even triple over the next 3-5 years.

valueline.com

Here’s what Value Line analyst Michael Napoli said to justify those expectations:

This stock is ranked to track the broader market averages for the coming six to 12 months. Looking further out, we anticipate rising sales and considerable improvement in earnings per share for the company from 2024 until 2026-2028. As one of the largest oil companies in the world, Chevron remains well positioned in the energy sector. Investment in operations should allow the company to capitalize on increasing demand from global markets. From the recent quotation, this issue offers attractive long-term total-return potential. This is supported by a fairly competitive dividend yield. Leverage is quite low and the cash balance is ample. As a result, Chevron earns a good mark for Financial Strength.

Morningstar established a fair price of $161, making CVX slightly undervalued in its estimation. Said strategist Allen Good: “We continue to view Chevron favorably, as its oil leverage and capital discipline keep it a viable long-term holding to capitalize on higher commodity prices while collecting cash returns.”

CFRA has a 12-month target of $172 for Chevron, with analyst Stewart Glickman saying:

CVX notably has been cutting its development costs in the Permian Basin (down 25% since 2019), which we see as remarkable given rising oil services costs lately. Longer term, we think CVX will expand its offerings in low-carbon solutions, renewables, and hydrogen. … CVX took advantage of a clean balance sheet (pre-pandemic) to borrow to sustain the dividend when crude prices collapsed, and now that it has recovered, the deleveraging process is essentially complete. … We anticipate that 2023 cash from operations can fully fund CVX’s capex needs and the dividend, assuming crude oil prices (which have dissipated to the low-$70/barrel range) don’t drop below $45/barrel.

Here is a value-related look at all five companies we bought in June:

*As a REIT, Realty Income’s valuation is stated in forward price/adjusted funds from operations ratio (P/AFFO).

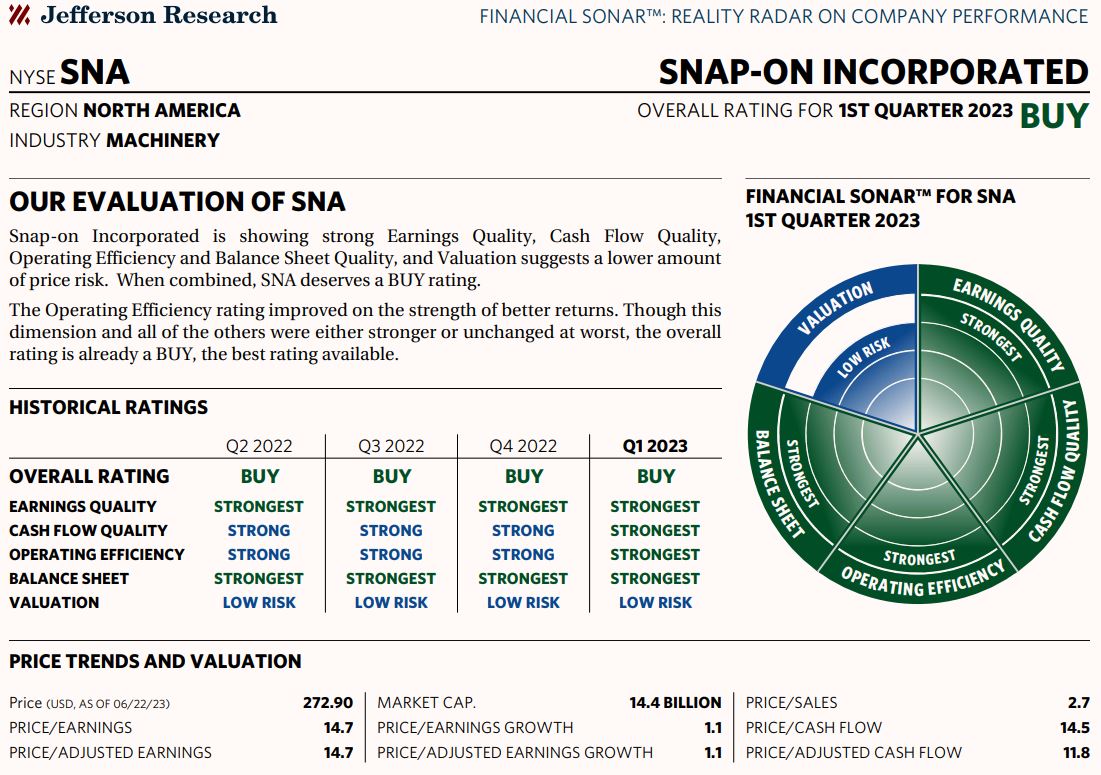

Snap-on appears to be the most overvalued of the group, with a forward P/E ratio at its highest point in several years. However, SNA has been such a high-quality operation, with such solid financial fundamentals, that I liked the idea of adding one more share to the IBP’s position.

I mean, you can’t find a better-looking “financial sonar” than this one, with Jefferson Research even calling the valuation “low risk” for investors:

Jefferson Research, via fidelity.com

Realty Income looks quite appealing here, with analysts calling it a buy thanks to its 5.2% yield and sub-15 forward price/adjusted funds from operations ratio.

Like CVX and APD, Morningstar gives O an “exemplary” rating for capital allocation, largely due to “the skill of its management team,” adding: “Management’s ability to generate additional cash flow while also reducing the risk contained in those cash flows shows a real skill for identifying how to build and shape a triple-net portfolio.”

UGI’s price has fallen significantly in recent months. But if I liked it enough to add it to the portfolio in May at $28.75/share (read why HERE), I certainly should be willing to buy more in June at $26.65.

Value Line’s Earl Humes believes UGI is a good investment:

Due to the recent market selloff, UGI stock is offering deep value for both medium- and long-term accounts. At the midpoint of our 18-month price projections, UGI stock is set to gain 55%. Further on, investors have the potential for above average long-term capital appreciation and an attractive dividend yield.

Income Report

Chevron is a Dividend Aristocrat that has been distributing income to its shareholders, without reduction or suspension, for well over a century.

SimplySafeDividends.com

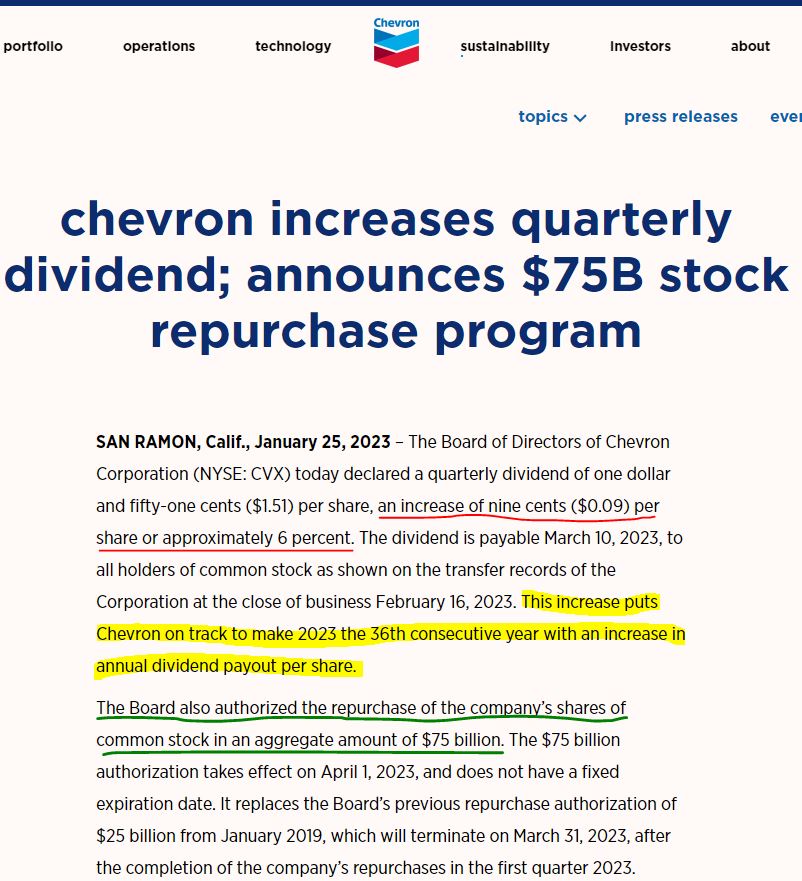

Early this year, the company announced its 36th straight annual increase, and paired that with a whopper of a share-buyback program.

chevron.com

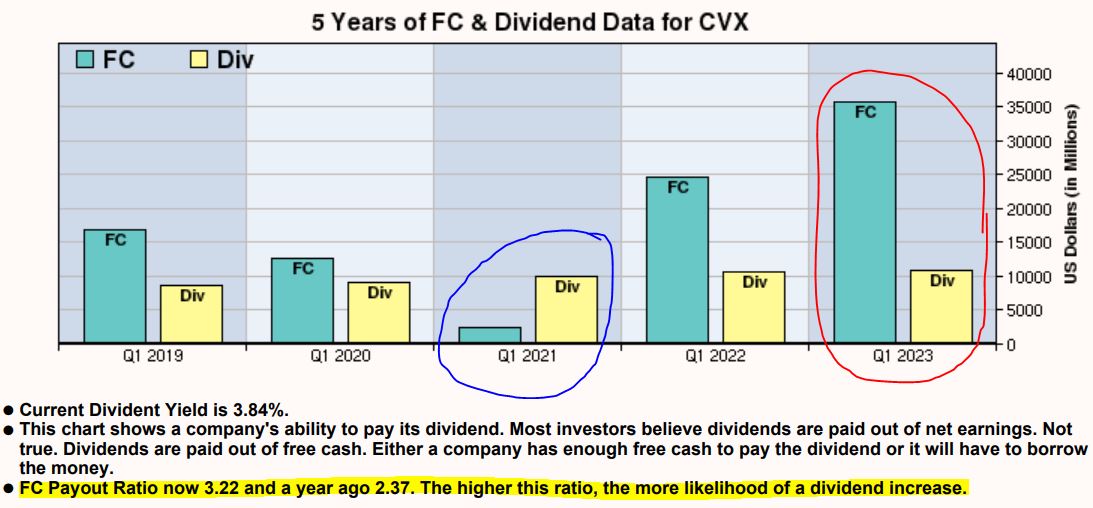

Like all oil corporations, Chevron is a cyclical company, with good and bad stretches due to oil prices and other macro conditions.

Only two years ago, CVX had to borrow just to pay its dividend (blue-circled area in the following graphic). Now, however, Chevron’s free cash flow easily covers the payout.

McLean Capital Research, via fidelity.com

Here is various income-related information for Chevron and the other four stocks we acquired in the June buy:

SimplySafeDividends.com

Notably, Simply Safe Dividends increased its safety scores for CVX and O. It also slightly reduced UGI’s rating from 99 to 90, which is still well within the “very safe” range.

Also, Realty Income recently raised its dividend, albeit by only a fraction of a percent — the 636th consecutive month the REIT has declared a payout since it was founded in 1994.

APD and O go ex-dividend this Friday, meaning those who want to receive the next payout for either stock must own it by market close of Thursday, June 29.

Wrapping Things Up

Chevron, Realty Income, Snap-on, Air Products and UGI will combine to contribute more than $500 in dividends to the Income Builder Portfolio over the next year … which leads to some BIG NEWS:

*** With this June spend, we have reached our target of $5,000 in projected annual income within 7 years of the IBP’s inception. ***

While I’m thrilled that we’ve accomplished what we set out to do — and that we’ve done so with a year and a half to spare, even while emphasizing quality along the way — this is also a little bittersweet for me because it means it’s time to wrap up a project I’ve enjoyed managing.

In a couple of weeks, I’ll be back to do a final review of everything that’s gone on with the Income Builder Portfolio since we launched it in January 2018.

In the meantime, please check out our HOME PAGE. There, you’ll find information about all 52 positions in the portfolio, as well as links to every IBP-related article I’ve written over these last 5 1/2 years.

As always, investors are strongly urged to conduct their own due diligence before buying any stocks.

— Mike Nadel

Buy this small group of unique stocks... never sell them... and make all the money you need... No matter what happens in the market. Revealed here: the name and ticker of the #1 stock.

Source: Dividends & Income