Toll Brothers, Inc. (TOL) is still seeing strong demand for new homes in 2023 despite higher mortgage rates. This Zacks Rank #1 (Strong Buy) is now expected to actually grow earnings in 2023 over 2022’s strong year.

Toll Brothers builds luxury homes in the United States for first-time, move-up, empty-nester, active-adult, and second-home buyers. It also serves urban and suburban renters.

It builds in 24 states, in over 60 markets.

Another Beat in the Fiscal Second Quarter

On May 23, Toll reported its fiscal second quarter 2023 results and blew by the Zacks Consensus Estimate by 50.8%. Earnings were $2.85 versus the consensus of just $1.89. That’s a $0.96 beat.

It has an amazing earnings surprise track record, especially when accounting for a pandemic which put the freeze on housing, at least initially. It has beat 13 quarters in a row and has only missed once in the last 5 years, and that was in early 2020.

Home sale revenue was up 14% compared to the prior year, to $2.5 billion. Delivered homes were also up 4% to 2,492.

Signed contract value declined 26% in the fiscal second quarter, however, to $2.3 billion from last year. Contracted homes also fell 19% to 2,333 as higher mortgage rates made buyers more cautious.

However, the adjusted home sales gross margin, which excludes interest and inventory write-downs, was 28.3%, up from last year’s adjusted home sales gross margin of 26.1%.

As mortgage rates stabilized this year, the buyers finally returned. Starting in Jan 2023, buyer demand returned and Toll Brothers said it has continued through the fiscal second quarter, and into the third quarter.

Toll Brothers also had a strategy to increase its spec homes in the spring to meet rising demand, especially as existing home inventory, it’s normal competitor, remained low. If you want to buy a home, new homes may be your only choice. Buyers can close on spec homes quickly.

“Importantly, with 71,300 lots owned or controlled, we continue to have sufficient land under control to increase community count in FY 2023 and beyond. Our financial position and liquidity remain very strong, and we expect to generate significant cash flow from operations in FY 2023,” said Douglas C. Yearley, Jr., CEO.

“In the second quarter, we retired $400 million of senior notes, extended our term loan and revolving bank credit facilities out five years, repurchased $84 million of common stock and paid $23 million in dividends.”

“At quarter end, our net debt to capital ratio was 23.5%. We expect to continue to invest in the growth of our business while reducing debt and returning cash to stockholders for years to come,” he added.

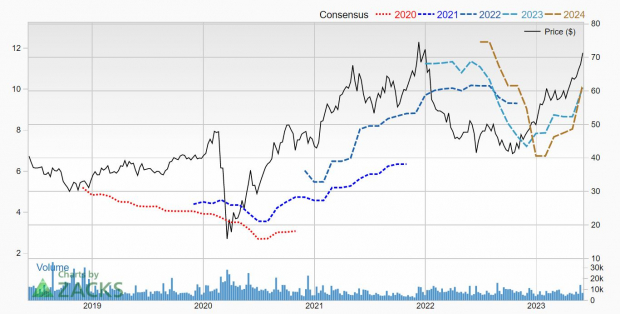

Earnings Estimates for Fiscal 2023 Jump Higher

Toll Brothers was bullish and so were the analysts.

5 estimates were revised higher for fiscal 2023 over the last 30 days pushing the Zacks Consensus up to $10.08 from $8.66. That’s earnings growth of 1.4% as the company made $9.94 last year.

While that may seem like small growth, just a few months ago, analysts were expecting a double digit earnings decline.

Shares Hitting New 52-Week Highs

Toll Brothers shares have been red-hot even before the recent earnings report. Shares have gained 42% year-to-date and are at new 52-week highs.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

But it’s still dirt cheap. Toll trades with a forward P/E of just 7.1 and a PEG ratio of 0.6. A PEG under 1.0 indicates a company has both value and growth.

It also is shareholder friendly and pays a dividend, currently yielding 1.2%.

If you are looking for a way to play the return of demand to the new home market, Toll Brothers is one that should be on your short list.

— Tracey Ryniec

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks