Hundreds of “experts” — from government officials, to CEOs, to those who analyze the economy for a living — say a recession in the next 6-12 months is imminent.

I had that in mind when considering the Income Builder Portfolio’s purchase prospects for May.

I wanted our primary buy to be a company with a dividend that was highly unlikely to get cut even in a painful economic scenario, a stock that was less volatile than the overall market, and a business whose share price could hang in there during a recession. I also wanted some dividend growth and a decent yield.

So, using the Simply Safe Dividends website, I set up the following screen:

SimplySafeDividends.com

The screen revealed 14 companies, including four that are already in the IBP: Johnson & Johnson (JNJ), Pepsi (PEP), Chevron (CVX) and Community Trust Bancorp (CTBI).

It also produced a lesser-known name that I wanted to dig into a little more: UGI Corp. (UGI), a natural gas utility and propane provider.

After doing some research, I decided to initiate a position in the company. And on Friday, May 12, I executed a purchase order for 51 shares of UGI on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

As you can see, I used most of the rest of Greg’s $2,000 monthly allocation on VICI Properties (VICI), a casino-centric real estate investment trust that became part of the portfolio back in January. And because there was still a little money left over, I also added a single additional share to the IBP’s stake in AT&T (T).

UGI’s Recession History

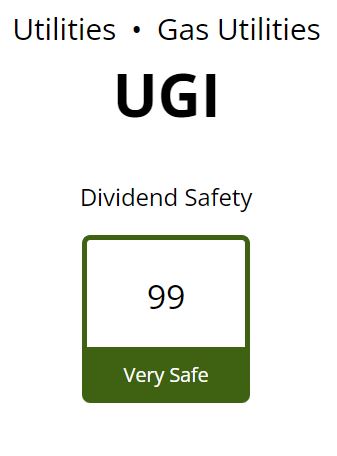

The following graphic that I plucked from Simply Safe Dividends’ section on UGI’s dividend safety really caught my eye:

SimplySafeDividends.com

The company has been paying dividends without a reduction since the late 1800s. In other words, UGI’s dividend has survived two World Wars, several other major military operations, the Great Depression, the Great Recession, the dot-com collapse, and, yes, at least a dozen too many seasons of Grey’s Anatomy.

During the Great Recession — the second-worst financial crisis in modern history — UGI increased its dividend, suffered a less-than-disastrous revenue decline, and saw its stock price fall only a fraction as much as that of the overall market.

Now, there is absolutely no guarantee that UGI’s history will repeat itself if and when another recession hits, but it’s hard not to be impressed with that track record.

What Is UGI?

If you own or rent a house, I wouldn’t be surprised if you had one of UGI’s leading products right now.

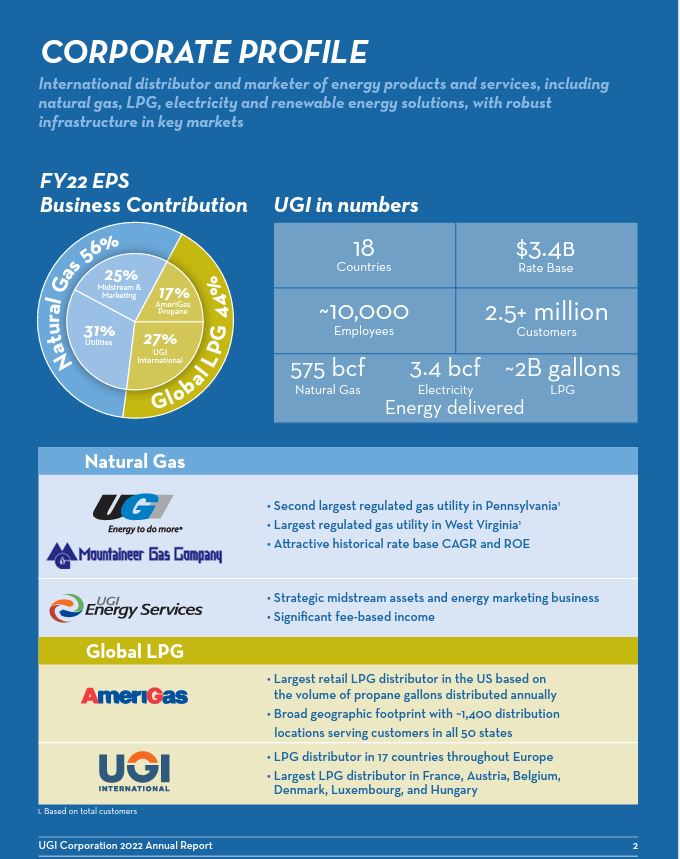

AmeriGas, the largest retail liquid propane gas distributor in America, is one of UGI’s four divisions. It has 1,400 distribution locations, serving customers in all 50 states. Not surprisingly, an AmeriGas tank is hooked up to the grill in my backyard.

This profile, from UGI’s 2022 annual report, gives a quick outline of all four divisions and the company’s overall operations:

UGI becomes the Income Builder Portfolio’s sixth utility holding — joining (in order of position size): NextEra Energy (NEE), American Electric Power (AEP), Avista (AVA), Pinnacle West (PNW) and Alliant (LNT). But it’s the first that focuses on natural gas distribution.

It has the largest international component of the group, and also has a midstream business that functions less as a utility and more as an energy operation.

So there’s a lot going on with UGI, and that adds to the diversification of the IBP’s utility profile. It also adds some risk, because most of UGI’s business doesn’t ensure incoming revenue the way regulated utilities often do.

Last year, UGI did receive approval of a two-phase rate increase for its Pennsylvania natural gas operations — including a weather-normalization adjustment rider that makes it more likely for UGI to generate predictable earnings.

Moody’s gives UGI an investment-grade A3 credit rating.

More Dividend Discussion

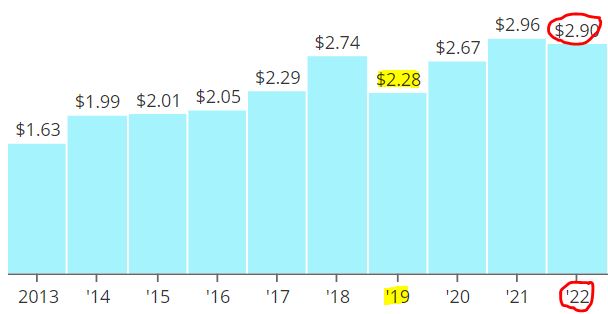

In addition to the incredibly long streak of dividends paid, the company has raised its payout for decades. Over the last 20 years, the compound annual growth rate of the dividend has been 7%, very nice for a utility.

ugicorp.com

Actually, the above graphic from UGI’s website is a little dated. On May 3, the company announced a 4.2% dividend raise, meaning its streaks have gotten even longer. Said CEO Roger Perreault:

We are pleased to mark the 36th consecutive year of increasing dividends, building on our long history of delivering returns to shareholders while investing for continued growth. This consistency demonstrates the strength and resilience of UGI and its capital allocation strategy as we seek to create shareholder value as both a growth and income investment.

Such commitment and consistency is heavenly to any investor interested in reliable, growing income.

With the increase, the stock now has a 5.2% yield — its highest since 2002.

Simply Safe Dividends gives UGI its best “safety” score, meaning its analysts believe the dividend is very unlikely to get cut.

SimplySafeDividends.com

Our May buys of UGI, VICI and T added about $103 to the IBP’s expected annual income stream.

That pushes the portfolio’s projected total past the $4,900 mark — meaning we’re more than 98% of the way to the $5K income target we established at the project’s outset back in January 2018. Yes, it’s just about time to celebrate reaching that major milestone!

UGI’s ex-dividend date is June 14, so those who want to receive the next payout must own shares by market close June 13.

The IBP’s new 51-share stake in the company will generate a $19.13 dividend to be paid July 1. As per portfolio rules, that will be automatically reinvested in more UGI.

OK, So What’s The Bad News?

UGI Corp. has underperformed for quite some time. After years of steadily increasing earnings, EPS fell big in 2019 and then, after regaining some ground, pulled back again a bit last year.

SimplySafeDividends.com

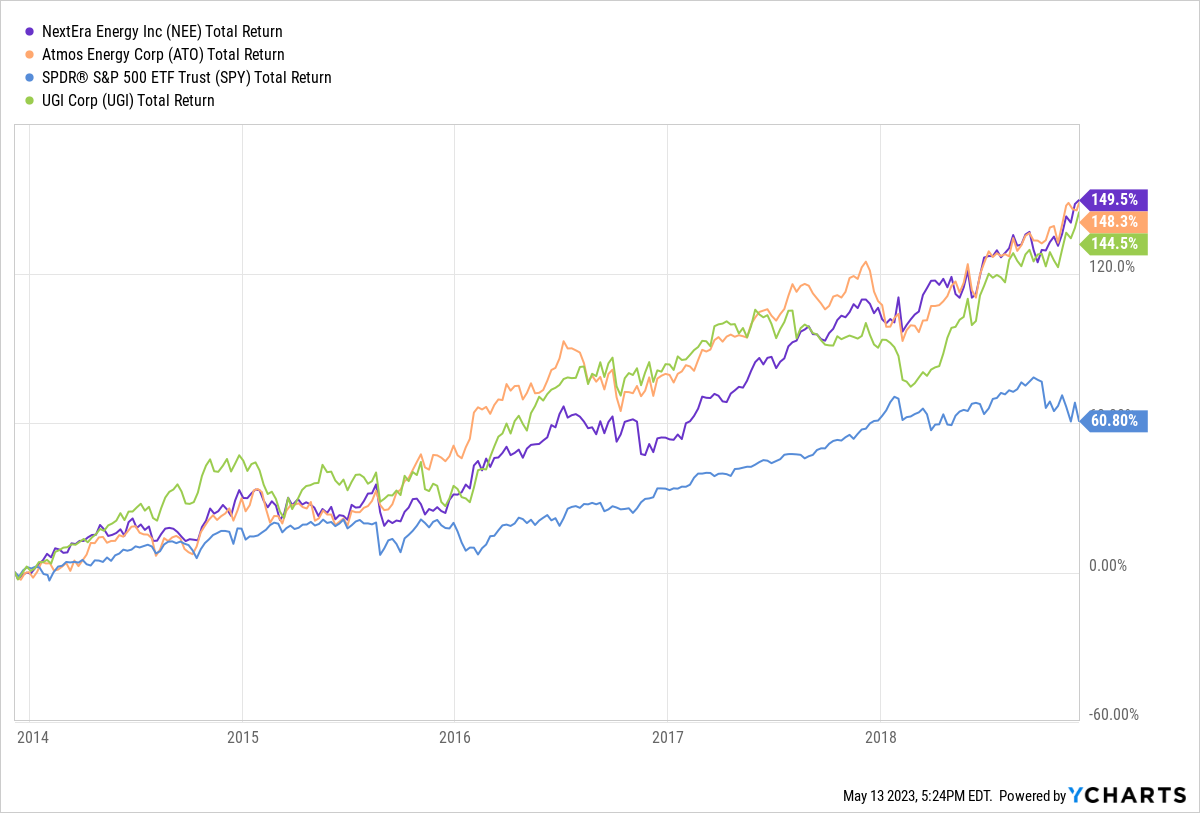

As a result of that, and some macro issues such as the falling price of natural gas, the stock has been hit hard since late 2018.

UGI has a total return of -44% over that stretch, a stark contrast to top IBP utility holding NextEra, natural-gas peer Atmos Energy (ATO), and the S&P 500 Index.

Indeed, the main reason that UGI’s yield is over 5% is because the stock price has fallen below $29 for the first time since the brief pandemic recession of 2020; take away that one-off scenario, and you have to go back to 2014 to see a price so low.

Compare the recent stretch to the previous five years, when UGI roughly matched NEE and ATO in total return while more than doubling the index’s gain.

I could offer numerous quotes from the company’s leaders as to why they think UGI will regain its mojo going forward. But they’re paid handsomely to build investor confidence, so I’ll instead look at what some analysts are saying.

Valuation Station

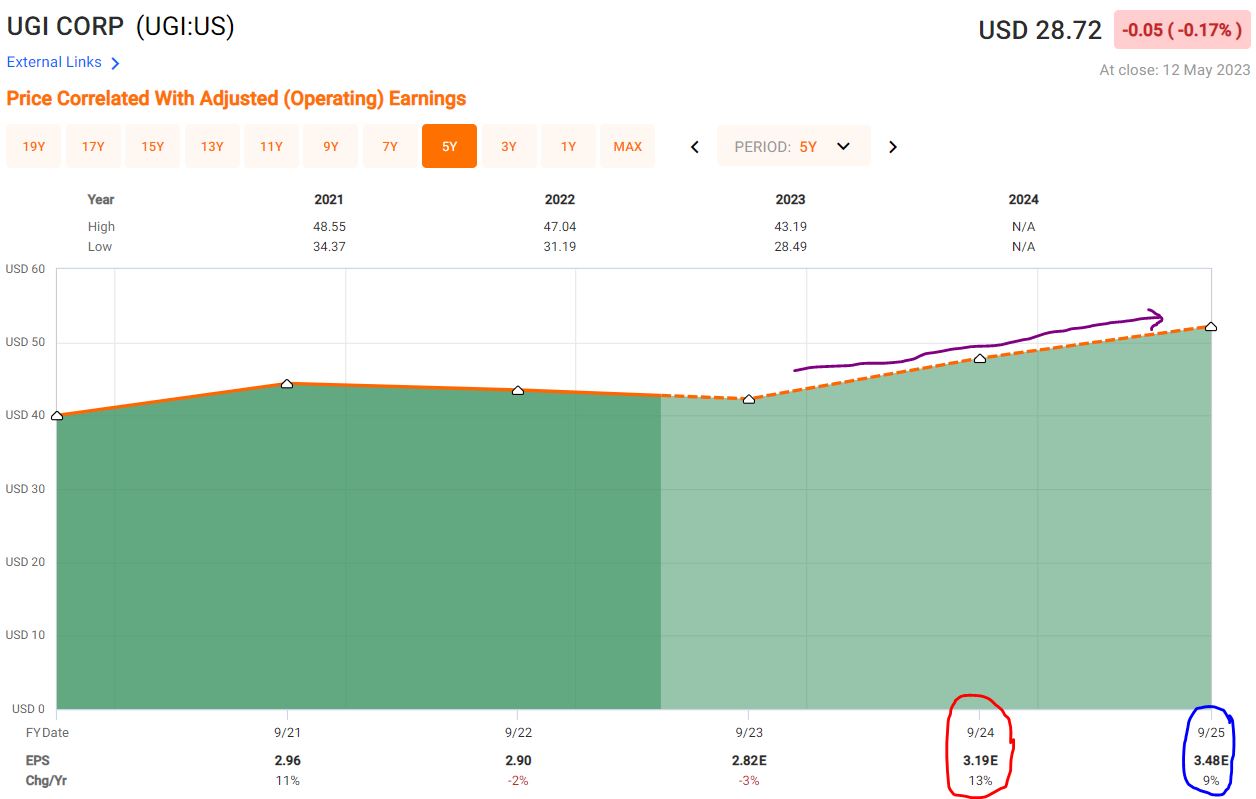

The following FAST Graphs image shows that after an expected 3% EPS drop in 2023, analysts are forecasting earnings to rise by 13% in 2024 and 9% more in 2025.

fastgraphs.com

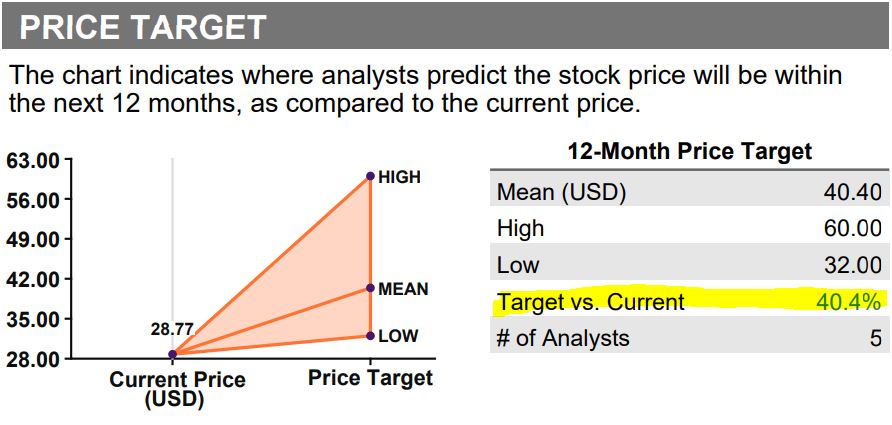

Five analysts monitored by Refinitiv think that fairly soon, improved earnings will act as a tailwind for UGI’s stock price. They have an average 12-month target price of $40.40, suggesting a 40% gain.

Refinitiv, via fidelity.com

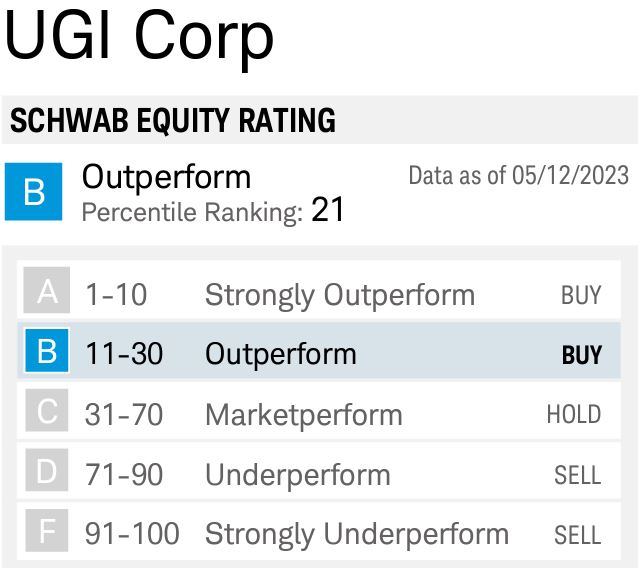

With a market cap of about $6 billion, UGI is not as widely covered by analysts as many other utilities are. One fairly bullish on the company is Schwab, which gives the stock an Outperform rating.

schwab.com

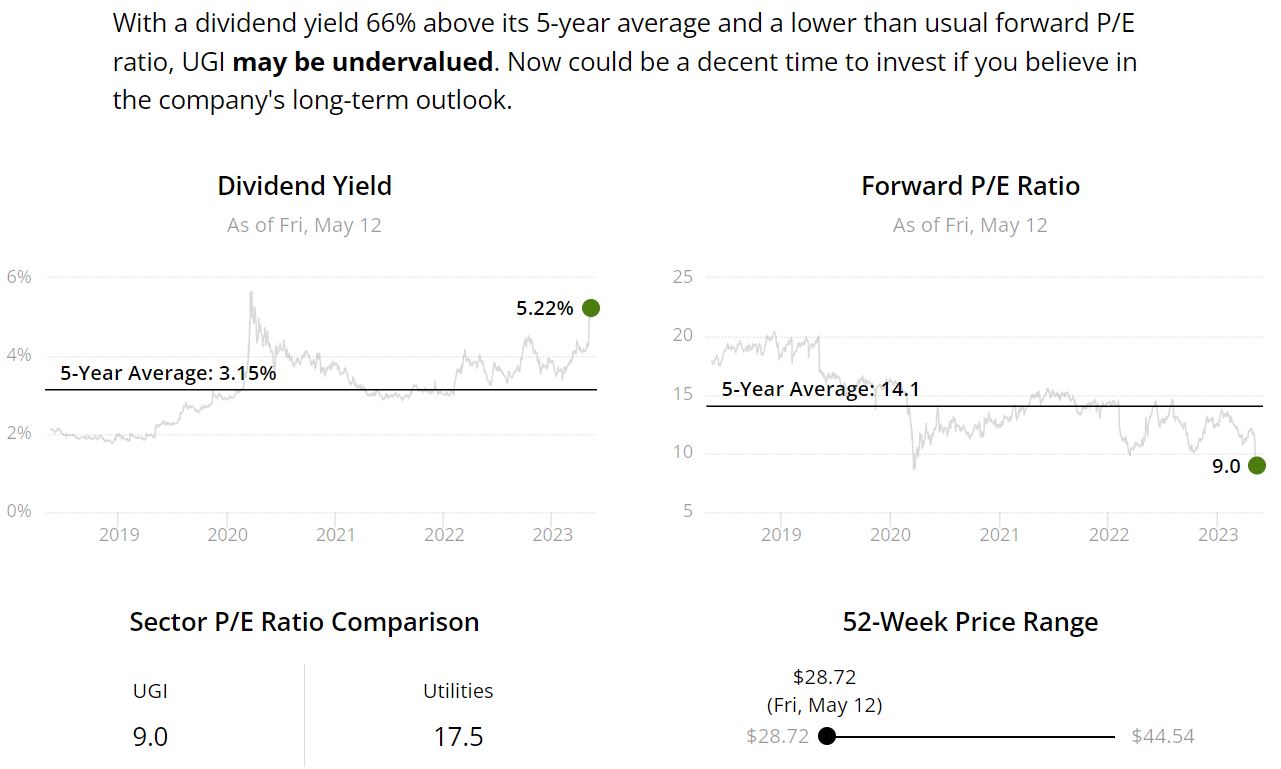

By every metric it uses, Simply Safe Dividends shows UGI to be quite undervalued.

SimplySafeDividends.com

Value Line says UGI isn’t necessarily for those with a short-term horizon: “The shares offer worthwhile risk-adjusted total return potential out to 2026-2028. All told, this high-quality large cap diversified energy stock is suitable for conservative-minded, long-term investors seeking an attractive dividend yield.”

I agree with that assessment. I’m a long-term investor who values growing dividends. So in addition to picking UGI for the Income Builder Portfolio, I bought a small position for my own personal account.

In early 2021, my colleague Dave Van Knapp added UGI to his Dividend Growth Portfolio, and he used some of the income the DGP produced to buy a little more of the stock in May 2022. It hasn’t performed well for Dave on a total-return basis, but he told me recently he was planning to keep the small position because “the 5%+ yield, combined with the maximum safety score, make it attractive at this time.”

Wrapping Things Up

![]()

Remember, the IBP isn’t about convincing our readers to replicate the portfolio. It’s about presenting interesting candidates for further research, and it’s about discussing the concepts and principles of Dividend Growth Investing. (See all 52 positions, as well as links to every IBP-related article, HERE.)

Like any stock, UGI might not appeal to everybody. To feel good about buying it, one has to believe it’s a solid value play and a fundamentally sound business ready to move forward again.

Whether or not a recession is likely, we always urge investors to conduct thorough due diligence before buying any stock — and that’s certainly the case with UGI.

— Mike Nadel

This stock checks all the boxes. Pays a high dividend (8%), has a record of increasing that yield (an average of 37.5% throughout company history), and is set up perfectly to profit from continued Fed rate hikes. Click here for the name and ticker of the most perfect dividend stock on the market right now.

Source: Dividends & Income