In addition to the overall portfolio update, I have two activities to report in my public Dividend Growth Portfolio for this month.

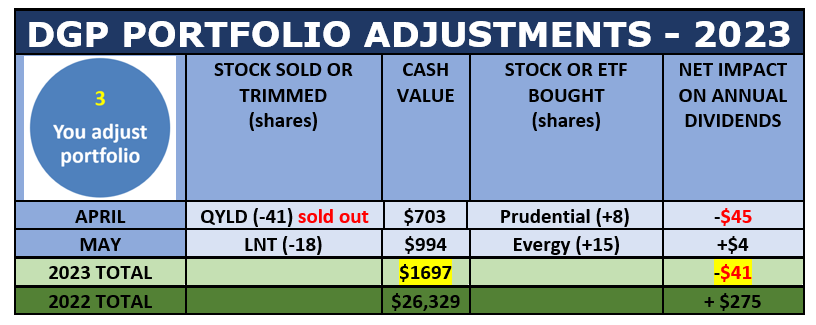

- I trimmed one stock whose size exceeds my maximum allowable size. I used the money to add shares to a utility position that I started last month.

- I executed my monthly dividend reinvestment by purchasing more shares of a technology-focused REIT.

Let’s start with those activities.

Trimming Oversized Position and Moving the Money

The portfolio’s updated Business Plan calls for limiting the maximum position size of any holding to 6% of the portfolio. Previously the maximum size was 8%. I have been slowly flattening position sizes for years now, and lowering the maximum size of the largest positions is another step in the evolution of the portfolio.

When I made the change, one position exceeded the new limit: Alliant Energy (LNT), which is a gas and electricity utility in the upper Midwest. I have owned Alliant since 2010, and it has been a rock-solid position ever since.

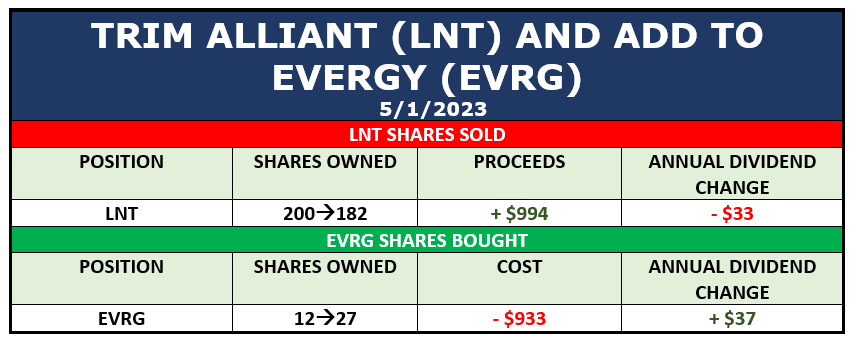

Alliant was only a fraction of a percent over the new size guideline, but I decided to trim it, not only to bring it under the new 6%-maximum line, but also to generate a little more dividend income with that money.

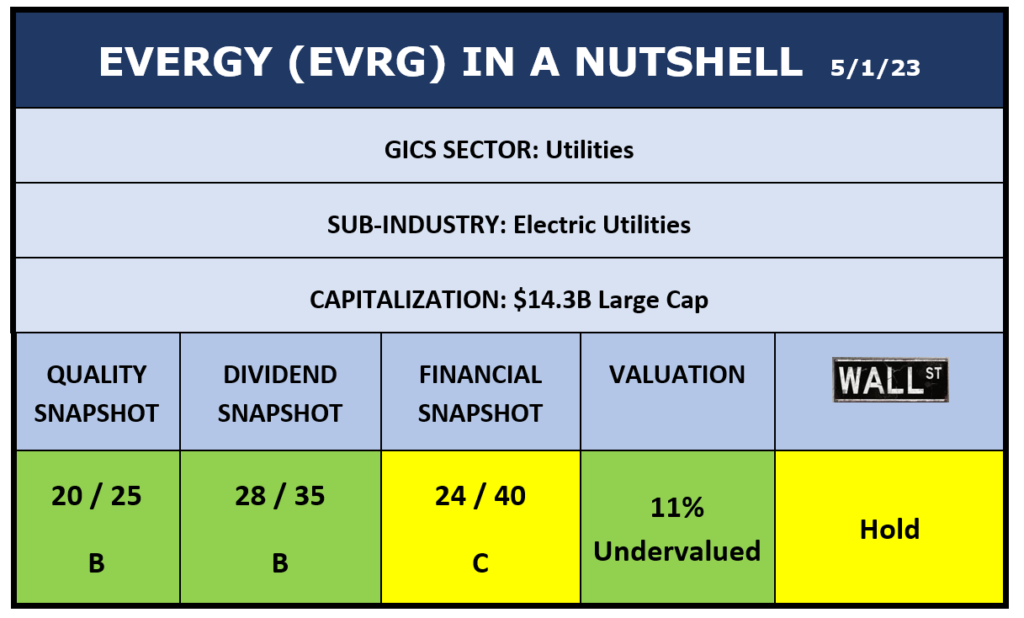

I decided to put the proceeds of the trim into a position started just last month, Evergy (EVRG), another Midwest utility. You can read more about Evergy in last month’s article. Evergy’s current yield is 3.9% compared to Alliant’s 3.2% – that is where the extra dividend income comes from.

Source: Author

Source: Author

Those metrics are virtually unchanged from last month, so I went ahead with the trim of Alliant and purchase of Evergy. Here is a summary of the transactions:

Source: Author

Source: Author

The net result of the trim-and-swap is that the portfolio:

- Picked up $61 for the reinvestment kitty

- Increased the annual dividend run-rate by $4 per year

- Took LNT down to 5.7% position size, beneath the 6% maximum size limit

- Grew EVRG from 0.4% to 1.0% of the account

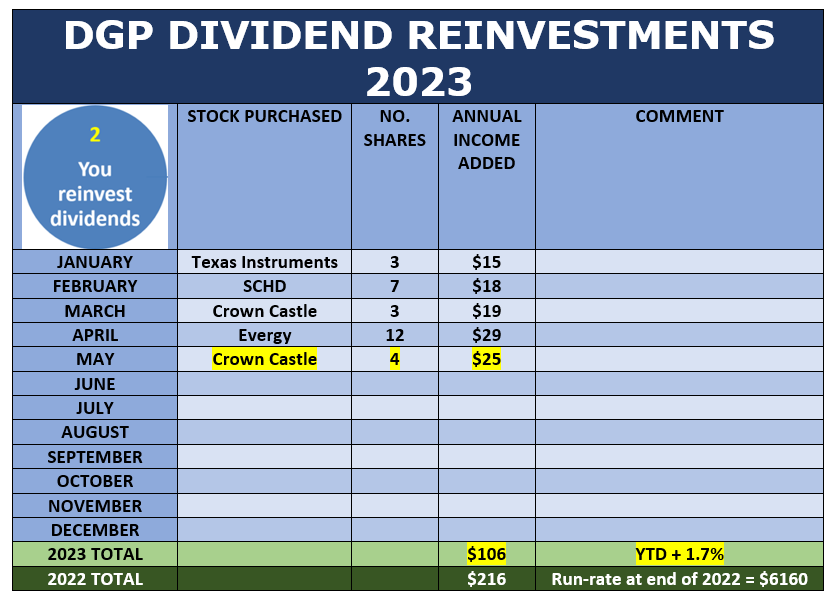

Dividend Reinvestment for May: Crown Castle (CCI)

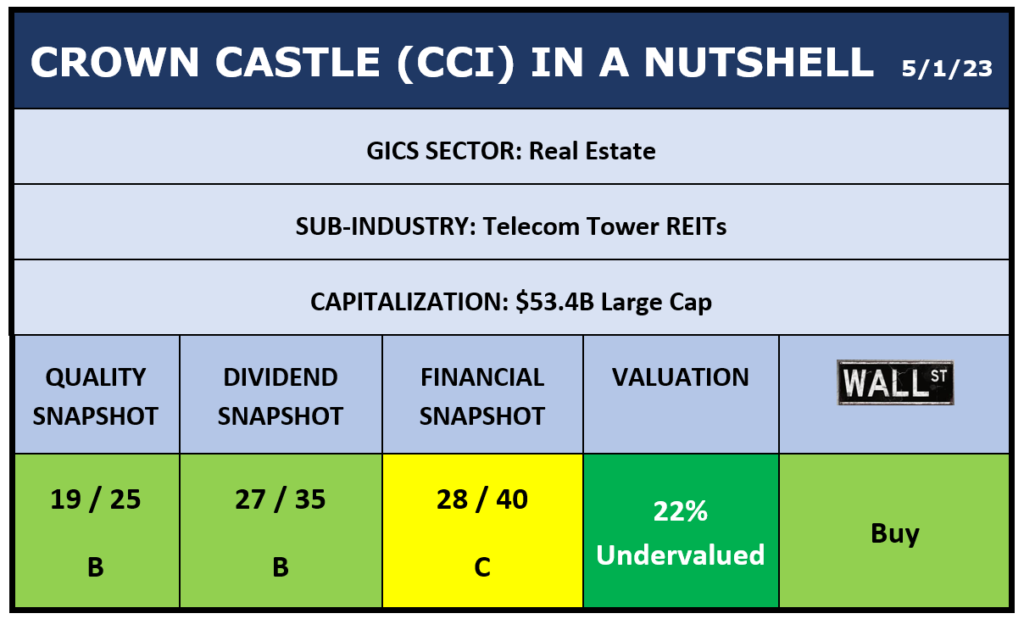

For this month’s reinvestment, I decided to add to my growing position in Crown Castle (CCI). This is a U.S.-centered REIT (real estate investment trust) whose business model involves infrastructure to handle electronic data via towers, small cells, and fiber. In previous articles, I have focused on the endless increase in data that we produce, which creates opportunities for data-infrastructure companies. My latest discussion of the promising business environment was in this article about my most recent purchase of CCI.

Here is a summary of the company:

Source: Author

Source: Author

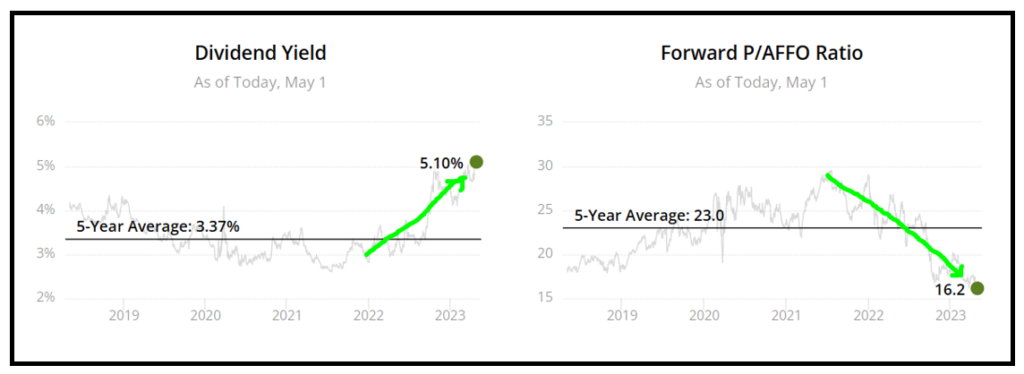

Due to a variety of circumstances, the market has hammered REITs over the past 12 months, as discussed in a recent Forbes article. That has not only driven their prices down but also pushed their yields up.

Source: Simply Safe Dividends

Source: Simply Safe Dividends

Crown Castle is now yielding over 5%, while its Price/AFFO (adjusted funds from operations) ratio is the lowest it has been in at least five years. And, by the way, CCI is on the list of best REITs to buy mentioned in the Forbes article.

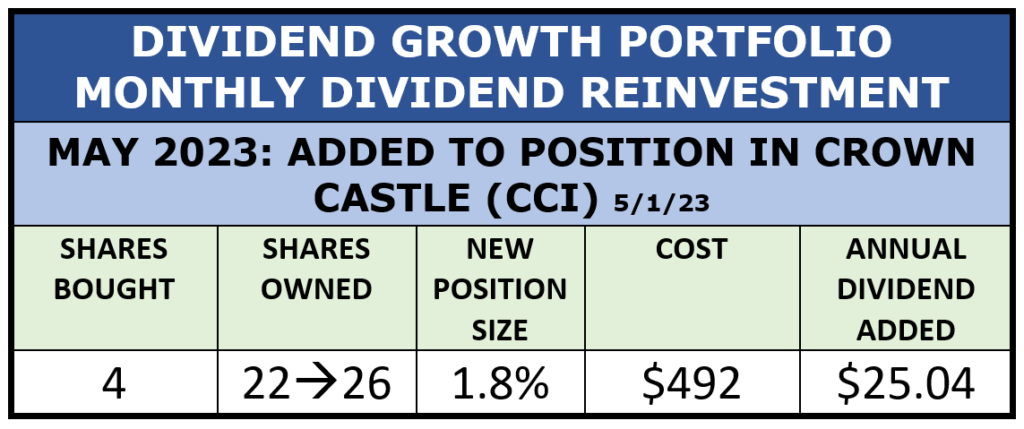

I opened my position in Crown Castle over a year ago, and this marks my fourth purchase as I build the position. Here’s what I did with the last month’s accumulated dividends:

Source: Author

Source: Author

The net effect of buying more CCI:

- Grew CCI to 1.8% of the portfolio. It is still a small position (under 3%) with a great yield, so I will continue to keep it on my shopping list for future purchases.

- Added $25 to the annual dividend run-rate.

- There is $23 left in cash to start the reinvestment kitty for next month.

Update of Full Portfolio

I started the Dividend Growth Portfolio in 2008 to demonstrate dividend-growth (DG) investing. The portfolio is real, the holdings are actual, and all decisions about managing the portfolio have been made in real time. This is not a back-test.

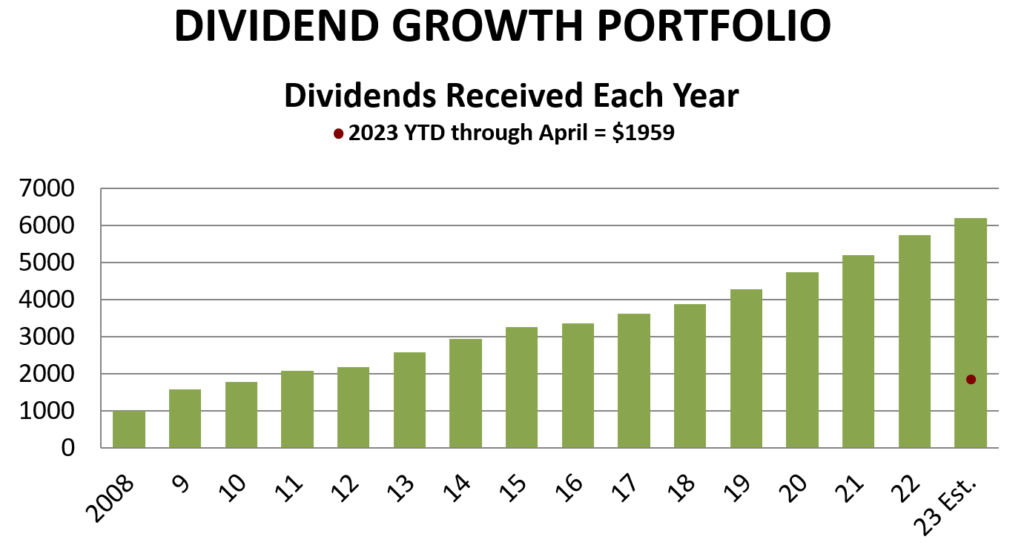

The main financial goal of the portfolio is to generate a reliable, ever-increasing stream of dividends in meaningful amounts, which it has done:

Source: Author

Source: Author

While the estimate for this year’s dividends changes a little each month as new information becomes available, the dividends collected so far in 2023 are about 13% more than the dividends collected last year through April. So annual growth seems assured again in 2023. As of now, I have 2023 projected to surpass $6000 in dividends collected for the first time in the portfolio’s history.

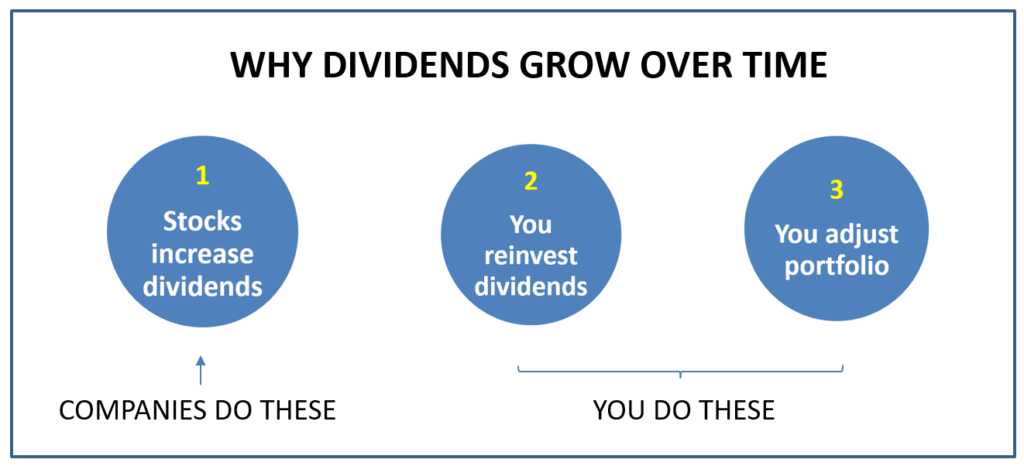

There are three reasons that dividends go up in a DG portfolio:

Source: Author

Source: Author

All three reasons were illustrated in April.

Reason #1. Stocks increase their dividends

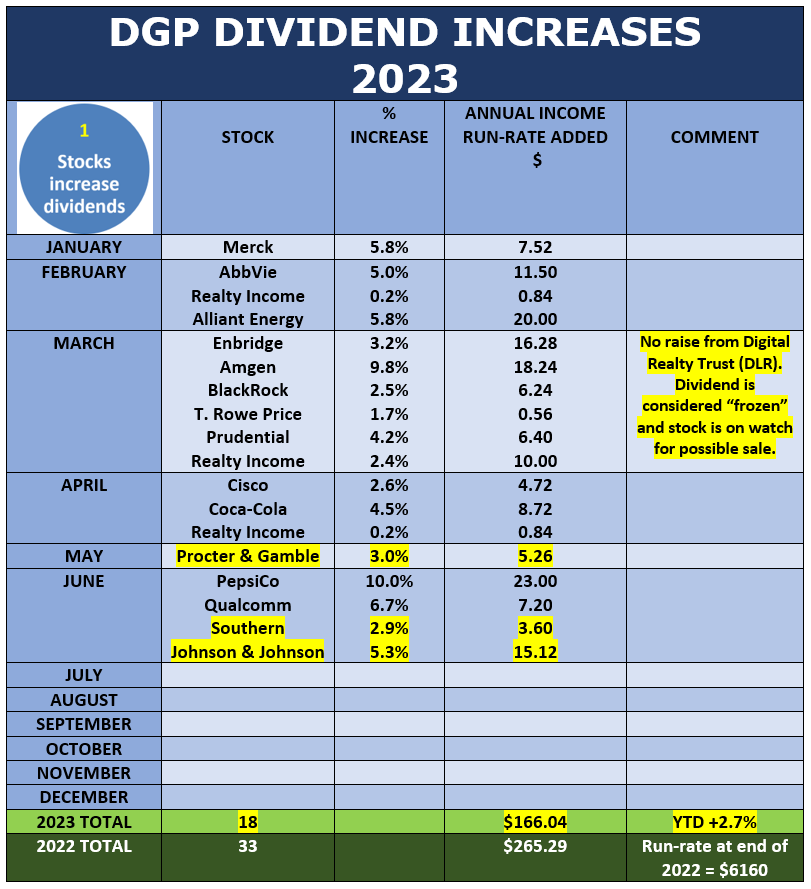

The following table shows the DGP’s dividend-increase record so far in 2023. New increases announced since last month are highlighted in yellow.

Also highlighted is the comment that Digital Realty Trust (DLR) skipped its expected dividend increase in March, and that was followed by a Dividend Safety downgrade from Simply Safe Dividends. While the dividend is still rated “Safe,” I have decided to put DLR “on watch” for possible sale. I want to see what management does to improve the company’s financial picture, and also to give management time to raise the dividend in 2023.

Overall, dividend increases are on pace to add about 5% to the portfolio’s annual dividend run-rate this year. They have already added 2.7%.

Source: Author, from company announcements

Source: Author, from company announcements

Reason #2. Reinvesting dividends

The second reason the portfolio’s dividends go up is that I reinvest them. Since dividends are paid per share, each additional share purchased causes the portfolio’s income to increase.

This reason was illustrated this month with my reinvestment in CCI. The table below shows how my dividend reinvestment program is going so far in 2023.

In contrast to dividend increases, which the companies do on their own, dividend reinvestment is something that I am responsible for as the owner of the portfolio.

Source: Author

Source: Author

At the YTD pace, it looks like the reinvestments will add around 3.5% to the portfolio’s dividend run-rate by the end of 2023.

Reason #3. Portfolio adjustments

This category refers to standard portfolio management activities, such as trimming or selling a stock, deciding how to replace it, and executing those decisions.

This reason is illustrated this month by the trimming of Alliant and moving the money over to Evergy.

Over the years, I haven’t churned the DGP very much. Every stock or fund I buy is one that I expect to hold “forever.” Not everything works out that way, but my portfolio turnover rate rarely exceeds 10% per year, and some years it is zero.

Source: Author

Source: Author

Overall, the three categories of dividend activities in May produced an increase in annual dividend income of $53.

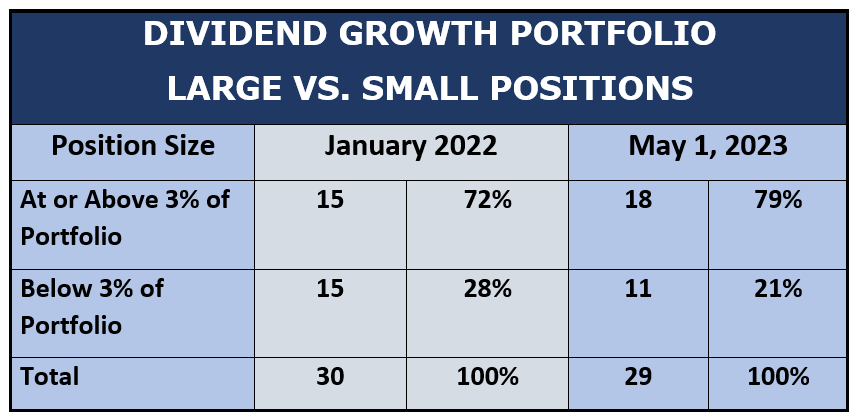

The last thing I want to show you this month is how my long-term program to reduce the number of small positions is working out.

Source: Author

Source: Author

I have increased the “full size” positions from 15 to 18, and reduced “small” positions from 15 to 11, since I began focusing on this at the beginning of 2022.

Of the 11 “small” positions, two are within a single purchase of crossing the 3% boundary. They are Texas Instruments (TXN) and Verizon (VZ). I expect both to reach the 3% mark, maybe by the end of this year.

There is nothing magic about the 3% position size, it is just where I drew the line to focus on either building positions into meaningful sizes or getting rid of them.

And that wraps up this month’s DGP review. If you want to see the positions in the portfolio at any time, its status as of the end of the previous month is always available here. That location also has an archive linking to all the articles and videos that I have published about the portfolio.

Thanks for reading!

-–Dave Van Knapp

After researching income stocks for over 30 years, I've come up with a one of a kind dividend portfolio. With the right 20-30 stocks, you can collect a dividend check every single day the market is open. That's over 260 dividend checks per year. Click here for the names of these 20+ stocks.

Source: Dividends & Income