I’m not going to lie to you: this market is headed for a fall. And if you’re caught holding the wrong dividend payers, you could be in for some serious losses indeed.

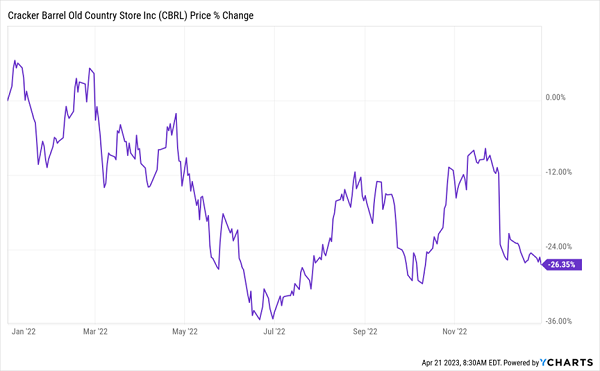

How serious? Well, the worst of the four stocks we’re going to delve into below—Cracker Barrel Old Country Store (CBRL)—plunged 26% last year, much further than the S&P 500. If you hold this one, or the other dangerous dividend we’ll discuss below, it’s time to cut your losses and get out now.

Cracker Barrel Plunged in ’22—a Sign of Things to Come?

But we’re not only going to sell today—we’re going on offense, too. Because despite this nosebleed market, there are still plenty of surging dividends out there tied straight into megatrends with decades left to run. I’ll name two particularly smart buys below, including one with a “shoe size” P/E and a boatload of cash heading out the door as dividends and buybacks.

But we’re not only going to sell today—we’re going on offense, too. Because despite this nosebleed market, there are still plenty of surging dividends out there tied straight into megatrends with decades left to run. I’ll name two particularly smart buys below, including one with a “shoe size” P/E and a boatload of cash heading out the door as dividends and buybacks.

Here, from worst to first, are four stocks to buy and sell as we pivot toward the choppy market headed our way soon.

Worst: Cracker Barrel’s Costs Are Soaring

If you’ve been to your local watering hole lately, you’ve no doubt noticed that it always seems to be packed.

It’s true—many folks are still catching up after years of lockdowns. But that’s cold comfort to restaurants, including Cracker Barrel Old Country Store. The chain is seeing higher sales, with revenue up 8% in the latest quarter. But soaring costs are still singeing its profits.

That was behind a 14% EPS slide, and the hits kept coming: wages jumped 6%; other store operating expenses soared 9%; general administrative expenses spiked 5%; and cost of goods sold was up 15%!

Where does that leave the dividend? In a dangerous spot.

CBRL yields 4.8% today, but that’s entirely the result of the stock’s plunge. Worse, CBRL is paying 109% of its last 12 months of earnings and 146% of free cash flow as dividends. That obviously can’t last.

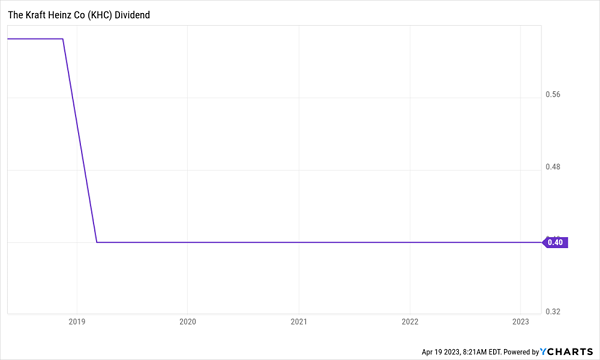

Second-Worst: Kraft Heinz Is Cheap for a Reason

Kraft Heinz Co. (KHC), with its raft of packaged-food brands (Oscar Meyer, Velveeta and Jell-O among them), may look like a bargain at 14.5-times forward earnings. And that is cheap compared to competitors like Mondelez International (MDLZ), at 22.4, and Coca-Cola Co. (KO) at 24.5.

But this one is cheap for a reason.

Think back to the lockdowns for a second. Back then, inflation was low, consumers favored foods that kept for a long time and no one was eating out. An ideal setup for KHC, in other words.

Today, all of those trends have flipped, and high inflation is weighing on KHC’s free cash flow, which fell 65% in the fourth quarter. That put the dividend (which was already cut by 36% in 2018 and has gone nowhere since) under pressure, as it now absorbs 126% of KHC’s last 12 months of free cash flow.

KHC’s Undercooked Payout

I’m not saying things can’t improve (a recession would bring KHC’s foods back into favor, for example). It’s just that waiting for KHC’s dividend to rise again isn’t worth the 4.1% yield—especially when there are better food stocks out there, like Pick No. 1 below.

I’m not saying things can’t improve (a recession would bring KHC’s foods back into favor, for example). It’s just that waiting for KHC’s dividend to rise again isn’t worth the 4.1% yield—especially when there are better food stocks out there, like Pick No. 1 below.

Second-Best: Johnson & Johnson Has Hidden Value

Johnson & Johnson (JNJ), with its 3% yield, doesn’t get many folks’ hearts racing—and that’s A-OK with us. Because while the first-level crowd rolls the dice on the likes of Tesla (TSLA), JNJ quietly does two things that come as close to guaranteeing upside as you can get:

- It’s a consistent dividend hiker: Its latest increase—to the tune of 5.3%—was its 61st straight yearly hike.

- It buys back shares: In the last decade, JNJ has taken 7.3% of its float off the market, boosting earnings per share—and putting upward pressure on the share price.

Then there’s the looming spinoff of its consumer-products division, which delivered 16% of JNJ’s revenue in fiscal 2022, into a new firm called Kenvue. Details aren’t yet final, but JNJ shareholders can expect to get their hands on Kenvue shares later this year.

That’s a plus for the “old” JNJ and Kenvue, as many studies have shown that parents and spinoffs outperform the market. Throw in a low valuation—JNJ’s forward P/E of 15.3 is below its five-year average of 16.7—and you have a nice buy window here.

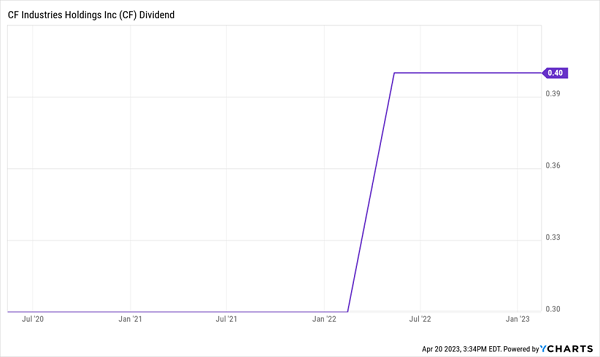

Winner: CF—a Food Stock in the Sweet Spot

Our No. 1 pick of this quartet, CF Industries (CF) is an American producer of agricultural fertilizers. Because CF has access to cheap (by global standards) natural gas, it dominates European and all international competitors.

Speaking of cheap, the stock has a price-to-earnings (P/E) ratio of seven. Seven! That’s just over half of the 12 P/E the great Ben Graham said was about right for a static, not even growing, company.

CF’s dividend is also on the move: after being parked at $0.30 per share since 2015, management popped it to $0.40—a 33% increase! And the payout still accounts for an ultra-safe 9% of the last 12 months of free cash flow.

CF’s Dividend Awakens—and Has Plenty of Room to Run

Over the past year, CF has taken advantage of its cheap valuation to repurchase nearly 10% of its stock. And it’s approved another $3-billion buyback program that would cut the outstanding share count by a further 17%.

Over the past year, CF has taken advantage of its cheap valuation to repurchase nearly 10% of its stock. And it’s approved another $3-billion buyback program that would cut the outstanding share count by a further 17%.

Fertilizer prices are down, which is why CF is so cheap. But in the big picture, the world needs more food and more fertilizer is a must-have. It’s a coiled spring.

— Brett Owens

8 More Dangerous Dividends You Must Sell Now [sponsor]

If you’re worried about this toppy market—and wondering why everyone else is still piling in—I’m with you!

Truth is, you haven’t missed anything: there is a storm coming. The Fed has broken the banks! And in hiking rates this far, this fast, Jay Powell has already set the stage for a recession and a pullback.

They’re baked in.

The time has come to batten down the hatches and dump dangerous dividends—including many stocks investors see as “sacred cows,” from our portfolios. It’s the only way to protect your nest egg and income stream!

To help you do just that, I’ve released an exclusive report called “Behind the 8-Ball: Eight Popular Dividends Set for a Cut.” Like Kraft Heinz and Cracker Barrel, the 8 popular dividend stocks in this report need to be dumped now, before their prices fall 25% (or worse!).

Click here and I’ll tell you all about the huge shift I see coming—and show you how to download this critical Special Report so you can protect yourself.

Source: Contrarian Outlook