Doing stock research sure can make me smile sometimes.

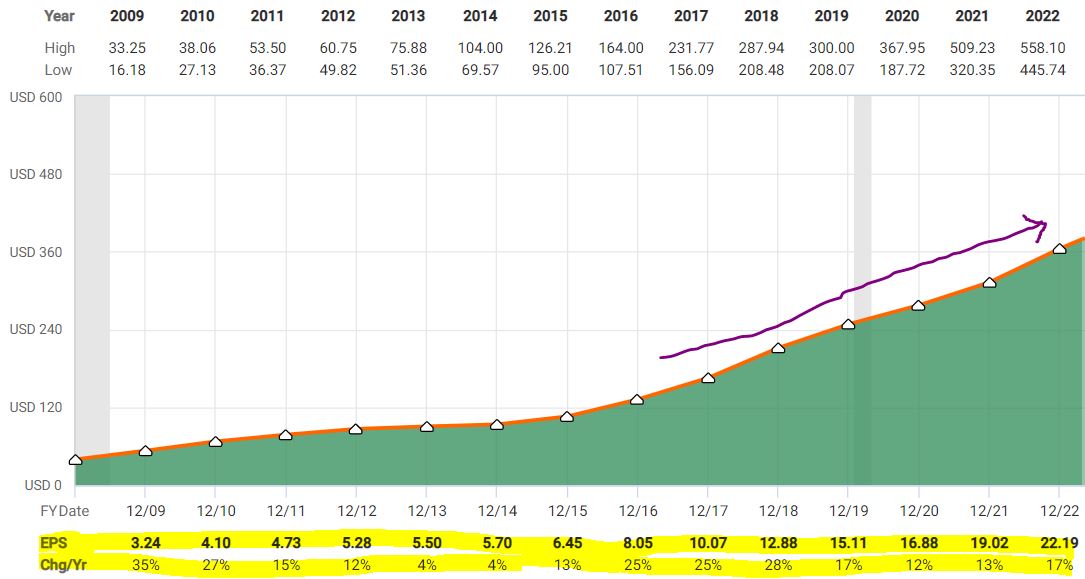

For example, I’ll see a graph like the one below and say, “Wow, look at those earnings! That’s been a heck of a company to own.”

fastgraphs.com

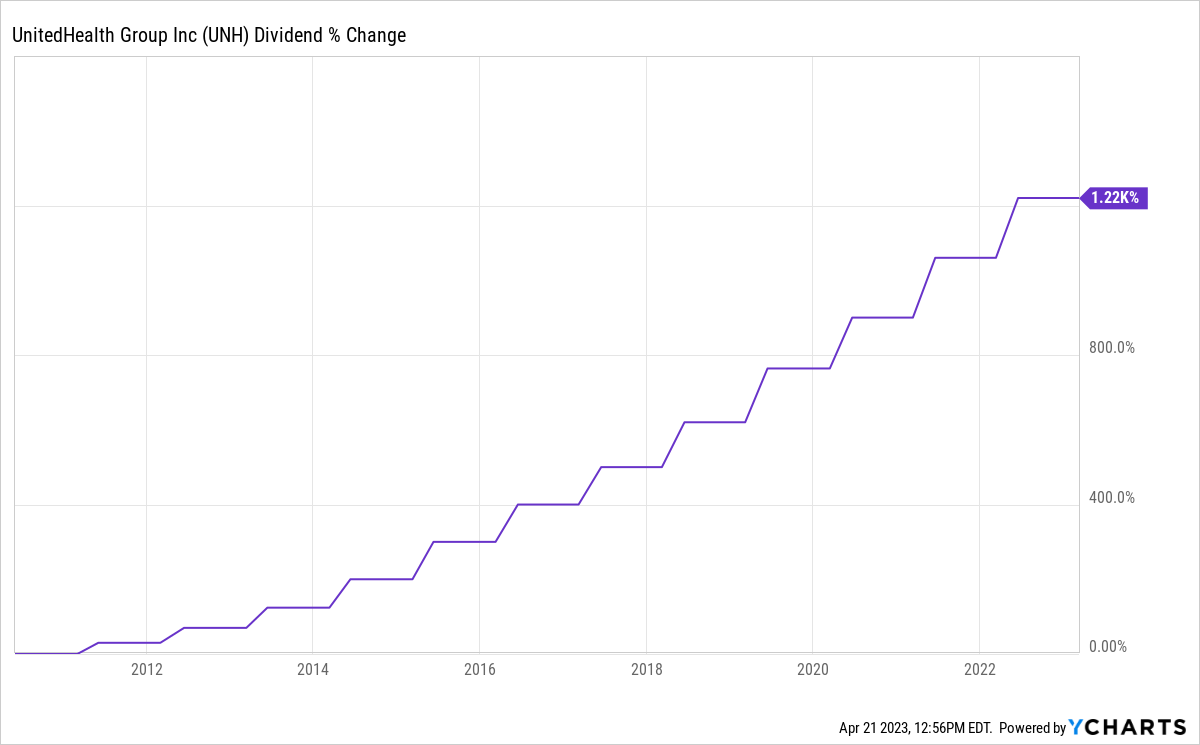

And as a guy who mostly uses the Dividend Growth Investing strategy, here’s another image that makes me happy:

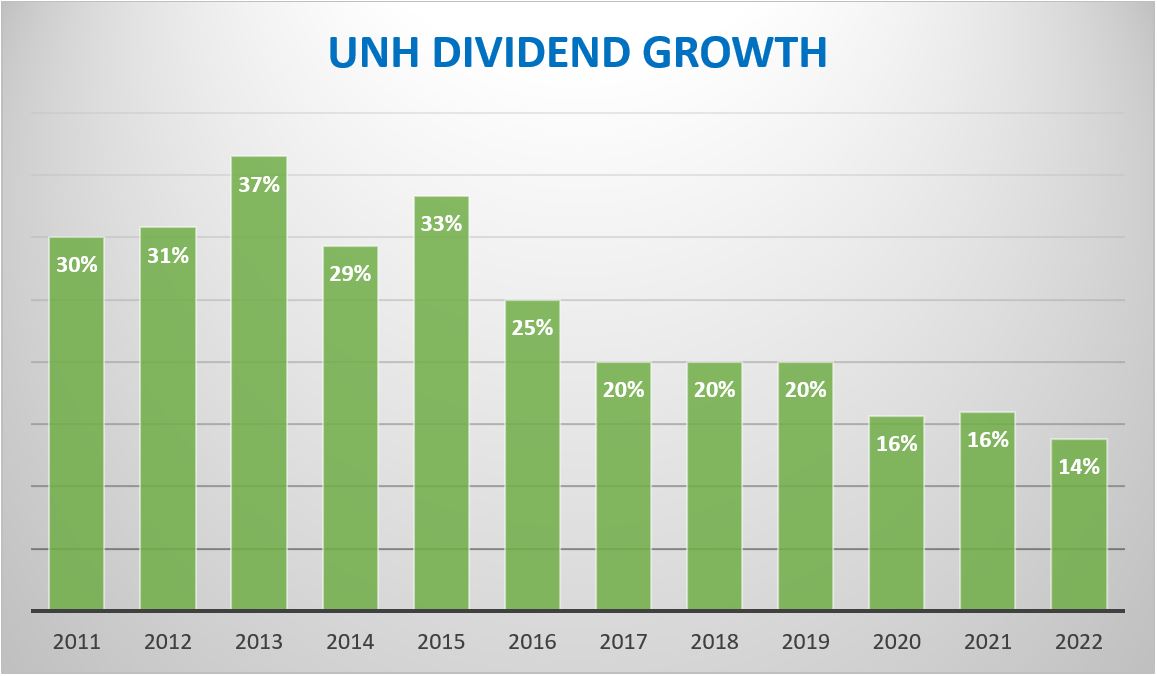

As you can see, the company I’m talking about is UnitedHealth Group (UNH) … and since initiating its quarterly dividend in 2010, UNH has increased its payout to shareholders by some 1,200%.

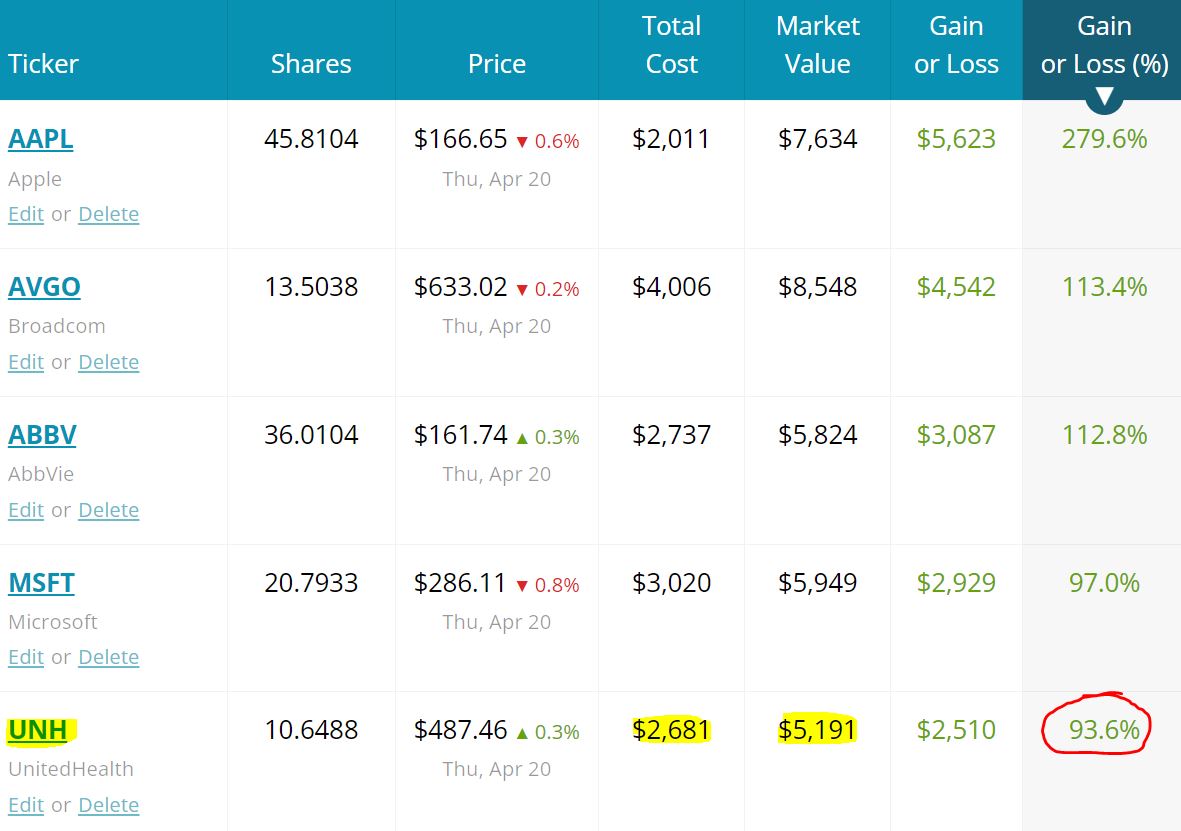

I first selected UnitedHealth for our real-money Income Builder Portfolio in June 2019, roughly doubled the position size just two months later, and added smaller amounts twice since (most recently in October 2021).

Each of those four UNH buys has absolutely crushed the gain that a similar S&P 500 Index purchase would have produced. Also, through market close of Thursday, April 20, the stock was the IBP’s 5th-best performer, with 93.6% total return.

SimplySafeDividends.com

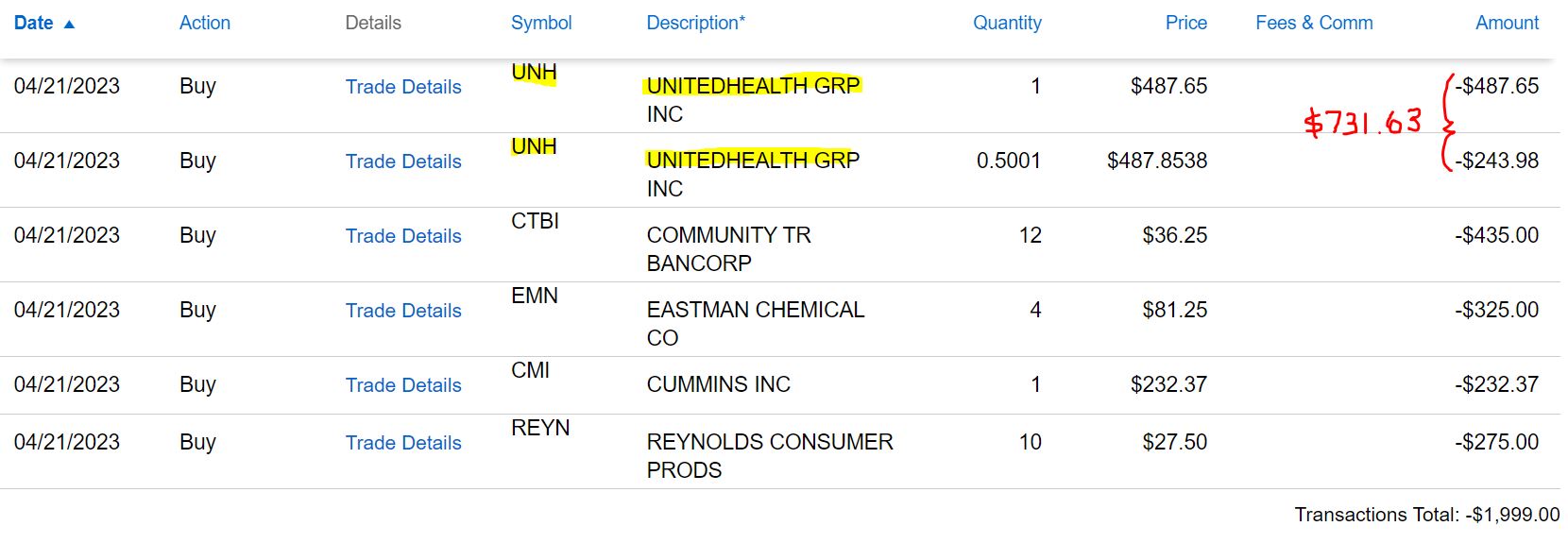

Given all of that, I felt good about adding another share and a half of UnitedHealth Group stock to our portfolio. On Friday, April 21, I executed a purchase order on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

I used the rest of Greg’s $2,000 monthly allocation to increase the size of what had been four of the IBP’s smaller positions — regional bank Community Trust Bancorp (CTBI), materials company Eastman Chemical (EMN), truck-engine maker Cummins (CMI) and consumer products company Reynolds (REYN).

I’ll talk a little more about those businesses later; the main focus on this article is UnitedHealth Group, which Morningstar calls a “health care colossus.”

Big-Time Industry Leader

For a detailed yet concise look UNH’s business strategy and outlook, here’s Morningstar analyst Julie Utterback:

Under one roof, UnitedHealth combines a top-tier health insurer (UnitedHealthcare), pharmacy benefit manager (Optum Rx), provider (Optum Health), and health analytics franchise (Optum Insight). The company’s integrated strategy has resulted in some of the best returns in the industry in recent years and has been copied at least in part by the late 2018 mergers at CVS Health (added Aetna’s medical insurance assets to its existing retail stores and market-leading PBM) and Cigna (added Express Scripts PBM assets to its existing medical insurance operations). Outside of substantial regulator-led reforms, we think these vertically integrated organizations could help bend the healthcare cost curve in the United States, and UnitedHealth should be one of the key leaders of that charge.

UnitedHealth has demonstrated an uncanny ability to remain at the leading edge of changes affecting the industry. For example, its 2015 acquisition of Catamaran greatly increased its PBM scale and helped create a more holistic view of a patient’s care. That combination of services has created attractive synergies for clients, such as employers or government programs, that are seeking to lower overall healthcare costs rather than just pharmacy or medical benefits. Adding service providers to the mix aligns incentives even further, especially since the firm’s outpatient care assets offer significantly lower costs than hospital-based services. The firm’s analytical tools help organizations pull various healthcare information related to its other operations together to provide an even fuller picture of a patient’s health and care options.

By providing those diverse yet connected services, UnitedHealth aims to grow in nearly any regulatory environment. It is shooting for 13%-16% earnings growth in the long run including strong operational growth and capital allocation activities, such as acquisitions and repurchases. While some regulatory scenarios could eventually cut into that mission, we suspect the value that UnitedHealth provides to the U.S. healthcare system will help it remain relevant in the long run.

For long-term investors, that’s sure a lot to like.

UNH released its first-quarter 2023 earnings report on April 14, and as usual the company delivered a lot of good news.

Revenue grew 15% year-over-year, and earnings from operations increased 16%. As has been the case in recent quarters, the Optum division led the way, with 25% growth in sales and 19% growth in earnings. Additionally, Optum Health revenue-per-consumer-served increased 34% year-over-year.

That all came after the company had, in Value Line’s words, “finished 2022 on a high note” to remain “the cream of the crop in the medical services industry.”

Yes … ho-hum … 2022 was yet another record year of earnings and sales for UnitedHealth.

SimplySafeDividends.com

Company officials also raised 2023 full-year guidance, and they’re now expecting adjusted earnings per share in the $24.50 to $25 range.

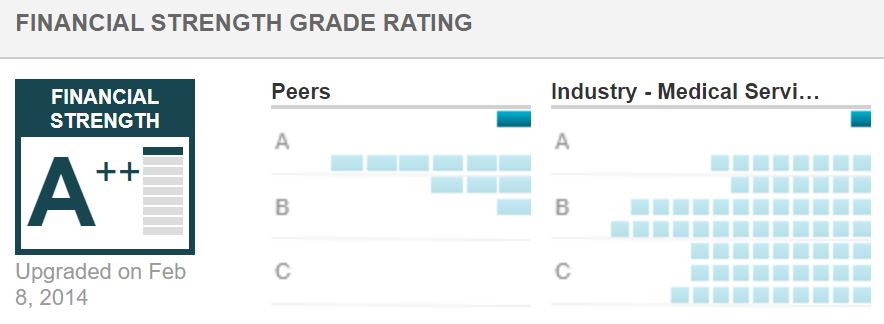

By any measure, UNH is a high-quality operation. Just look at the following graphic from Value Line, showing its take on the company’s financial strength. UNH towers over its peers.

valueline.com

Here are quality-related ratings of UnitedHealth Group from a variety of evaluators:

Dividend Elevator … Going Up!

The last column of the table above shows that Simply Safe Dividends gives UNH a high score for dividend safety, meaning a cut is extremely unlikely.

Indeed, if history is any guide at all — and I think it is — the company will announce another double-digit-percentage raise in June.

UnitedHealth’s dividend hikes were huge the first few years after it went to quarterly payments. As often happens over time, the raises have settled into a lower range on a percentage basis, but even recent increases have been healthy.

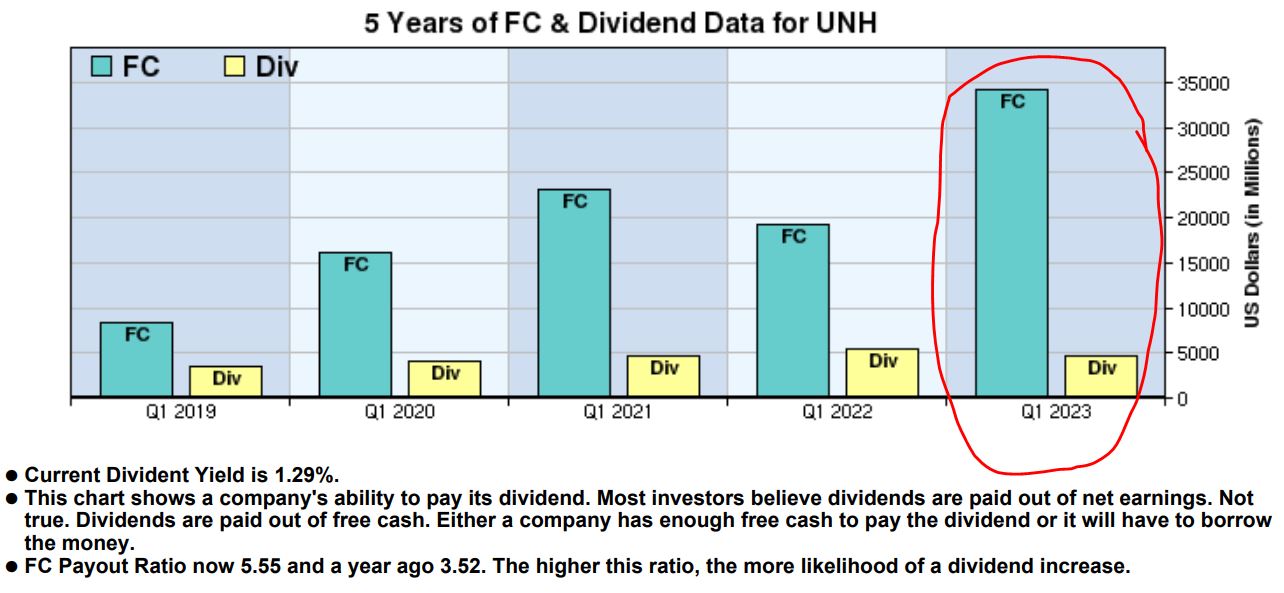

One thing for certain: UNH generates more than enough free cash flow to cover the dividend and give shareholders another great raise.

McLean Capital Research

The only complaint some DGI practitioners might have against UNH is that the share price has appreciated so significantly in recent years that the yield has fallen below 1.5%.

I consider that a nice “problem,” but yield-hungry investors might be interested in the other four companies that were part of the April IBP buy. Here’s some income-related information on the group:

SimplySafeDividends.com

With these latest purchases, the five positions are projected to generate about $393 in dividends over the next year, roughly 8.2% of the portfolio’s $4,811 total.

We’re now 98% of the way to our income target of $5,000 within 7 years of the IBP’s January 2018 inception. Given that the portfolio is only 5 1/2 years old, it is well ahead of pace. (See the Income Builder Portfolio’s home page HERE; it includes information on all holdings, as well as links to every IBP-related article.

A Note On CTBI

The highest-yielding stock we bought this month is Community Trust Bancorp. Its yield has risen significantly, to nearly 5%, because its price was whacked in the regional-bank drama that unfolded recently.

In an update after the company’s April 19 earnings call, Simply Safe Dividends said:

Through the years, CTBI has proven to be a conservatively managed community bank, resulting in 42 consecutive annual dividend increases. Recent stress in the banking system is unlikely to disrupt that impressive track record.

CTBI … reported earnings that showed the small-cap lender’s performance has remained resilient during this uncertain time.

Over the past month, many small banks had deposit outflows as clients shifted funds to larger institutions that they deemed to be safer places to park cash. However, CTBI’s deposits increased over 2% from the end of 2022. The bank does not face any pressure to increase its liquidity and reaffirmed its commitment to the dividend. …

Around two-thirds of CTBI’s loans carry variable rates, which provides some margin protection if interest rates and deposit costs keep rising. CTBI’s loan book has also continued growing, and credit performance remains solid with the bank noting a decrease in delinquencies last quarter despite the slowing economy.

Coupled with very healthy capital levels and a conservative investment portfolio that sits on smaller unrealized losses and has less duration risk than most of its peers, CTBI continues to look like a quality bank in these uncertain times.

I certainly can understand why investors might want to shy away from even well-run regional banks given all the industry turmoil. But it’s also true that one of the best times to find value and opportunity when buying stocks is when there is “blood in the water.”

Last July, I explained why I decided to include CTBI in the Income Builder Portfolio. It’s a Dividend Aristocrat whose most recent increase was 10%, and it’s one of the few banks that actually raised its payout during the Great Recession. So I’m not only comfortable adding a few shares to the IBP now, I also bought a little more on the dip for my personal portfolio.

Valuation Station

CTBI is a small-cap company that is not widely covered by analysts, so you can see in the following table that it has received no price targets. UnitedHealth and the other three recent IBP buys get much more coverage.

Of the five stocks, Eastman Chemical and Cummins were most likely to be considered undervalued, and Reynolds is arguably slightly overvalued (which is why we bought relatively little of it in April).

Concentrating again on UnitedHealth, analysts are generally bullish on the company’s stock. Thirteen of the 14 monitored by TipRanks call it a Buy, and their average 12-month target price suggests a 24% upside.

tipranks.com

Refinitiv tracks even more UNH analysts, with 23 of 26 giving the stock a Strong Buy or Buy rating.

Refinitiv, via fidelity.com

Value Line has established a medium-term (18 months) target price of $600, suggesting a 25% gain, as well as a longer-term target that projects a return of as much as 37%.

valueline.com

That explains why Value Line includes UNH in its model portfolio of “Stocks with Long-Term Price-Growth Potential.” VL analysts also have listed the company among 100 “Highest Growth Stocks.”

On the latter list, UnitedHealth is one of only 13 names to carry Value Line’s top rating for relative safety. The IBP owns a half dozen of those: Apple (AAPL), Mastercard (MA), Microsoft (MSFT), Starbucks (SBUX), Visa (V) and UNH.

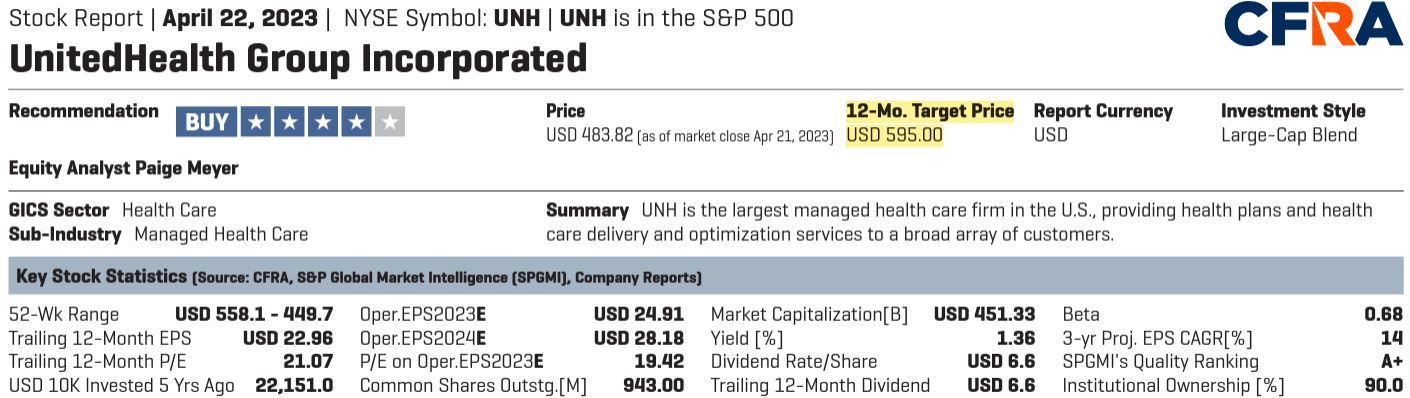

Another analytical firm that’s high on UnitedHealth Group is CFRA.

CFRA, via schwab.com

CFRA analyst Paige Meyer says: “Our Buy recommendation reflects our positive views towards UNH’s growth prospects. … With the Covid-19 pandemic over three years in, we anticipate more stability and predictability for the business. Our target of $595, based on a 23.9x forward P/E, is a premium to UNH’s historical average, justified by solid growth prospects.”

Wrapping Things Up

We created the IBP to demonstrate the process of building a long-term, income-focused portfolio that would appeal to dividend growth investors. And despite its relatively low yield, UnitedHealth fits the profile of what many DGI practitioners want.

The beauty of UNH is that it’s also attractive to those who prefer “growthier” portfolios that focus on total return. In addition to being in the IBP, the company is part of the real-money Growth & Income Portfolio that I manage. (See the GIP home page HERE.)

High-quality UnitedHealth Group is a reliable dividend grower that has consistently outperformed the overall market, and that’s good enough for me.

As always, investors are strongly urged to conduct their own thorough due diligence before buying any stock.

— Mike Nadel

The name of the ONE stock (ticker symbol and all) that has helped over 170,000 people discover how to gain their financial freedom... Learn More.

Source: Dividends & Income