It’s an unsettling time for many investors, what with bank defaults, stubborn inflation, declining stock prices, and a possible recession looming.

Maybe you’re really thinking about preserving some capital, but you also still want to see your income stream grow. Or maybe you just want to stash some cash for a certain amount of time and not have to worry about it disappearing.

In either case, how does a safe 5%+ yield sound?

(And not the “kinda sorta safe” investment that financial pundits sometimes talk about. Sorry, but no matter how high quality a blue-chip stock might be, it really isn’t “safe.”)

I’m here today to talk about CDs — certificates of deposit, which are fully covered by the Federal Deposit Insurance Corporation.

In particular, I’ll be talking about a product available through major brokerages called brokered CDs.

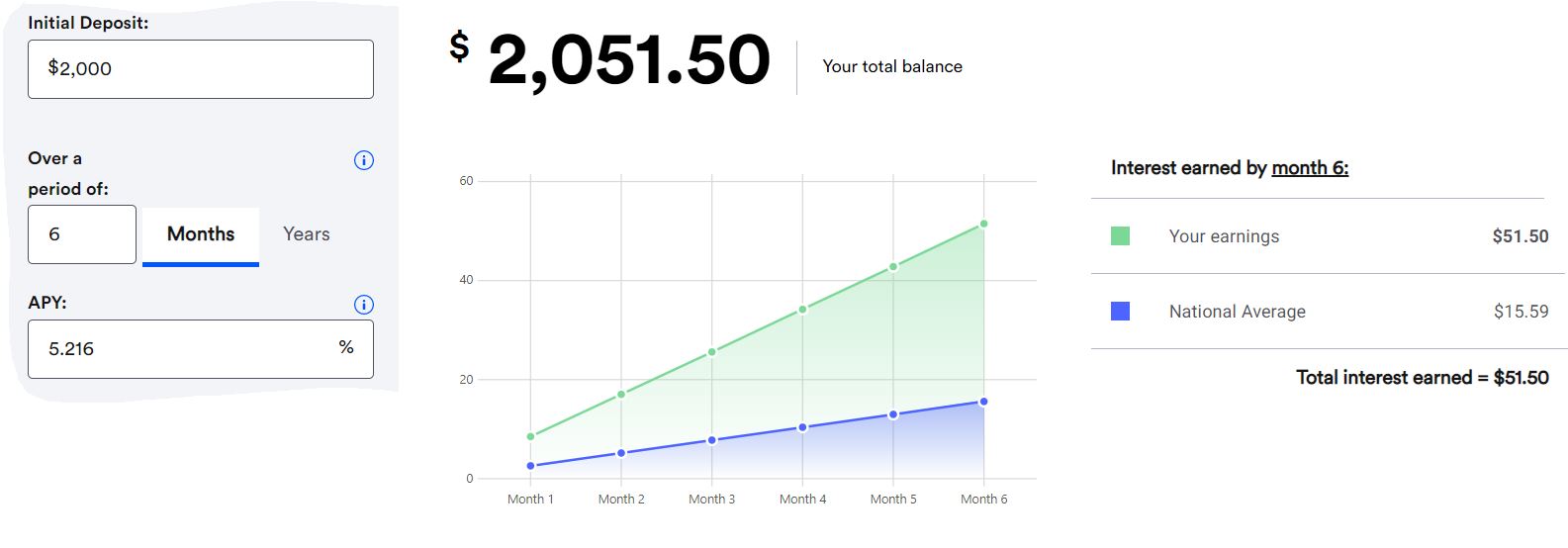

Actually, I’m not only talking about the product; I just executed the purchase of a 6-month brokered CD for our Income Builder Portfolio — using the entire $2,000 March allocation provided by this site’s co-founder (and IBP money man), Greg Patrick. (One doesn’t really “buy” a CD, one deposits money into it, but I’ll nonetheless use terms like “buy,” “purchase” and “invest” throughout this article.)

![]()

The IBP is in its sixth year (see the full 50-position portfolio HERE), and this is the first time I’ve selected anything other than a stock for it.

I asked Greg if he’d consider a brokered CD as a possible investment — not necessarily because he needed the little bit of income he’d receive, but as a way to present the product to readers who might be interested. His answer: “That would be awesome.”

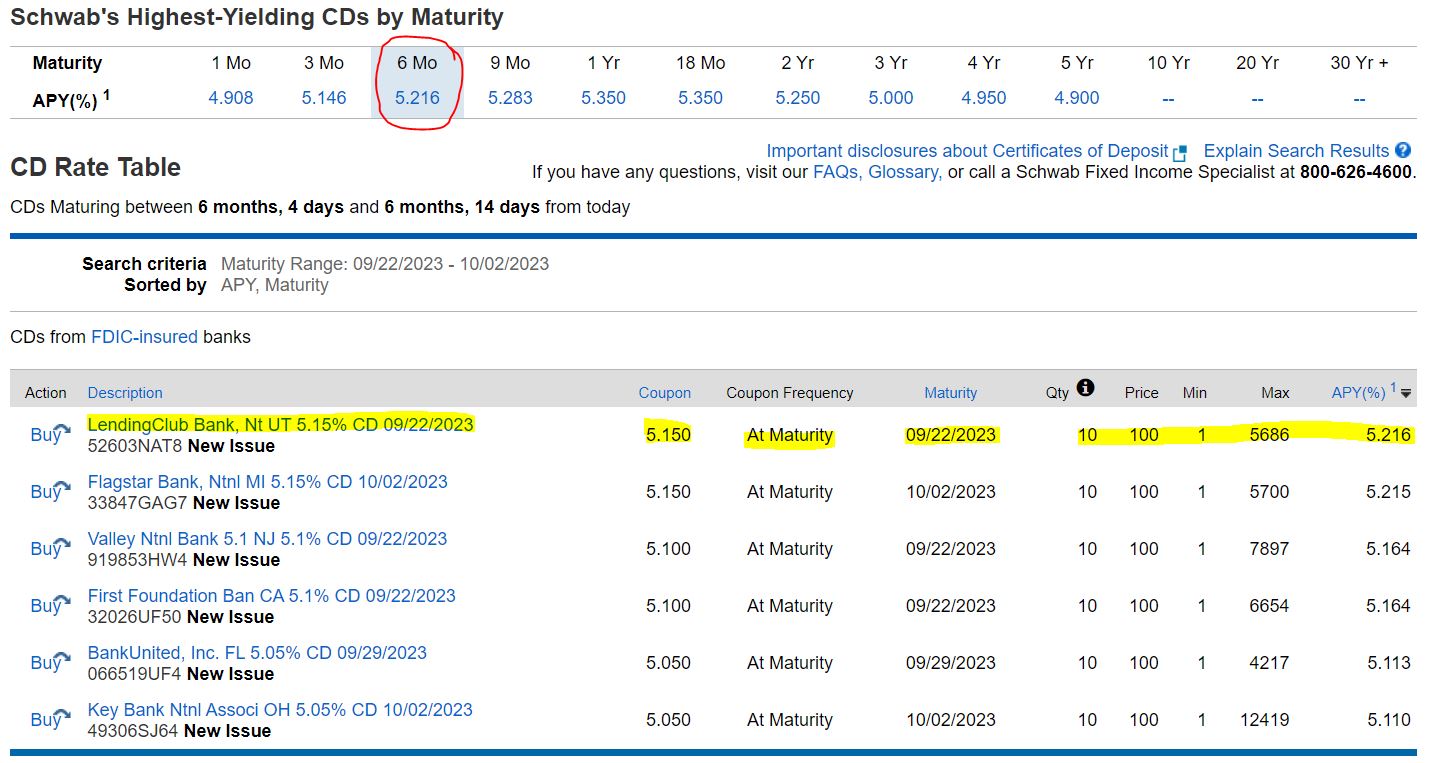

We use Schwab for the IBP, and the brokerage offers CDs of various lengths and interest rates.

The following image from Schwab’s online CD page indicates the products available and the top annual percentage yield (APY) in each time frame. It also shows the 6-month CD that I chose for the IBP from LendingClub Bank.

Vanguard, Fidelity and E-Trade (to name a few big brokerages) have fairly similar setups on their websites.

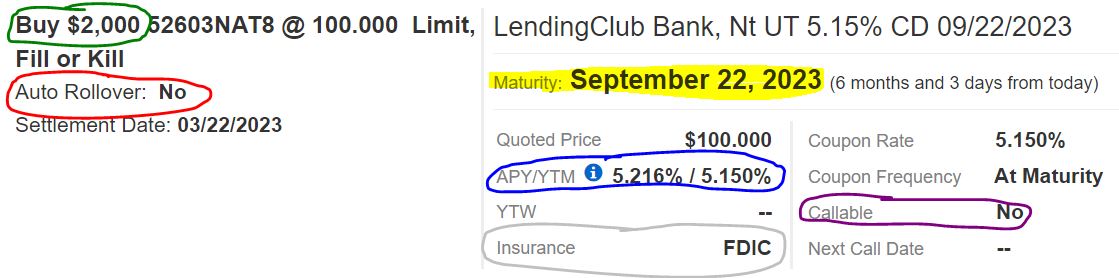

The following image of the IBP’s purchase is chock full of useful information:

schwab.com

The green-circled area shows the amount invested … the red-circled area shows that, after 6 months, the investment (principal and interest) will be returned to the investor, as opposed to being rolled into a new CD … the yellow highlight indicates the CD’s maturity date … the blue-circled area shows the APY and the yield to maturity … the purple-circled area shows that the issuing bank can’t “call” (or choose to cash in) the CD prior to maturity … and the silver-circled area indicates that the bank carries FDIC insurance for the CD.

CDs: ‘Old School’ Meets New Reality

In the United States, certificates of deposit have roots dating back to the Revolutionary War. My parents bought CDs at their bank, and their parents might have had some, too. During the Great Depression, the FDIC was created to insure bank deposits (including CDs).

If a bank cannot meet its obligations, the FDIC — an independent agency created by Congress to protect Americans from being victimized by bank defaults — will make depositors whole up to $250,000 per account ($500,000 for a joint account).

FDIC insurance became a major topic of conversation earlier this month, when Silicon Valley Bank and Signature Bank failed within a few days of each other.

Why Brokered CDs?

Brokered CDs are relatively new products. Here are some of the biggest differences between a bank CD and one opened through a brokerage:

- A brokered CD can be bought quickly and seamlessly with cash held in a brokerage account. My order for the IBP’s CD took about a minute to complete.

- It’s easy to buy a brokered CD within a traditional or Roth IRA. If you have cash in an IRA account at your brokerage, you can use it for a CD; most banks don’t offer such an option.

- Brokered CDs might offer higher interest rates than banks do.

- If you sell a bank CD before maturity, you will have to pay a penalty, usually 2-3 months interest. There is no penalty for cashing out a brokered CD before it matures. To redeem a brokered CD before maturity, however, you would have to sell it on the secondary market, and it could end up losing value if interest rates have climbed.

One of my general rules of thumb: If I think there’s any chance I’ll need the cash before the maturity date, I’ll usually opt for a bank CD and be willing to pay the penalty if necessary; but if I’m very sure I won’t need the cash until after the maturity date, and/or if I want to hold it in an IRA, I’ll go for a brokered CD.

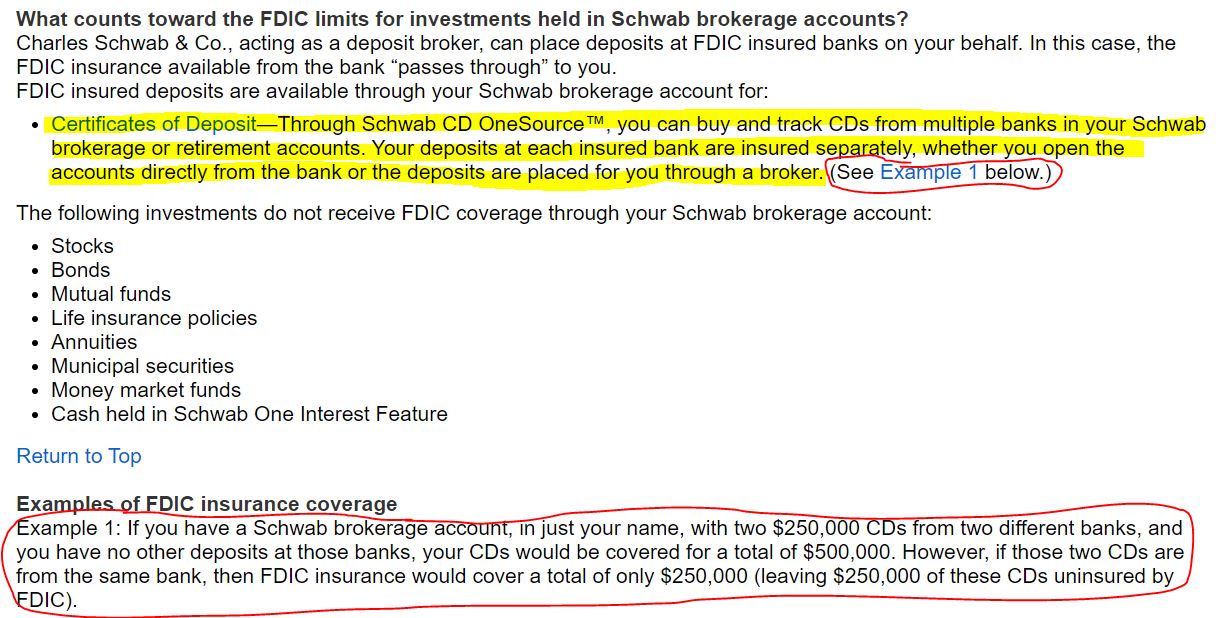

When it comes to FDIC insurance for brokered CDs, this snippet from Schwab’s website describes it well:

schwab.com

So I could buy $2 million in CDs using my brokerage … and as long as I divide the sum among 8 banks at $250K apiece, all $2 million would be FDIC insured.

The IBP’s Newest Investment

For some strange reason, Greg didn’t want to pony up $2M for brokered CDs, so the IBP will have to make do with the $2K he did allocate.

Six months from now, the CD will have generated $51.50 in income for the portfolio.

bankrate.com

Some might be saying: “Oh wow … a whole $51.50! Don’t spend it all in the same place!”

Well, although this is a real-money portfolio and Greg cares about making money, the IBP also has been a laboratory for investing ideas. And this was an idea we wanted to present as a safe alternative to volatile stocks.

We made this a short-term CD that matures in late September because Greg might want to use both the principal and the interest from the certificate differently once fall arrives. But some folks might prefer a 2-year or 3-year CD that locks in a 5% annual interest rate over a longer term.

And obviously, one can put a whole lot more than $2K into a CD. A $250,000 CD at the same exact terms as the one we just got for the IBP would generate more than $6,400 interest over 6 months — and the whole thing would be FDIC insured.

bankrate.com

That might sound better to some investors than buying $250K worth of Fifth Third Bank (FITB), Blackstone (BX), Advance Auto Parts (AAP) or other stocks with 5%-ish yields but considerably more volatility.

Indeed, now that safe 5% yields are available through CDs, and 4.5% yields can be found in money-market funds, it will be interesting to see if some income-oriented investors eschew stocks for these so-called “cash equivalents.”

So if certificates of deposit are “all that,” why not sell stocks and pile into CDs? A few reasons:

- Unlike qualified dividends and long-term capital gains, interest from CDs (unless held in IRAs) is taxed as regular income.

- High interest rates won’t be around forever. The Fed has been raising rates to combat inflation, but eventually it will start lowering them. When CDs mature and you’re ready to deploy the cash, stocks might be more expensive after the Fed cuts rates.

- And perhaps most importantly, CDs offer no growth. You get your interest, sure, but there is no potential for capital gains. Younger investors, especially, need growth.

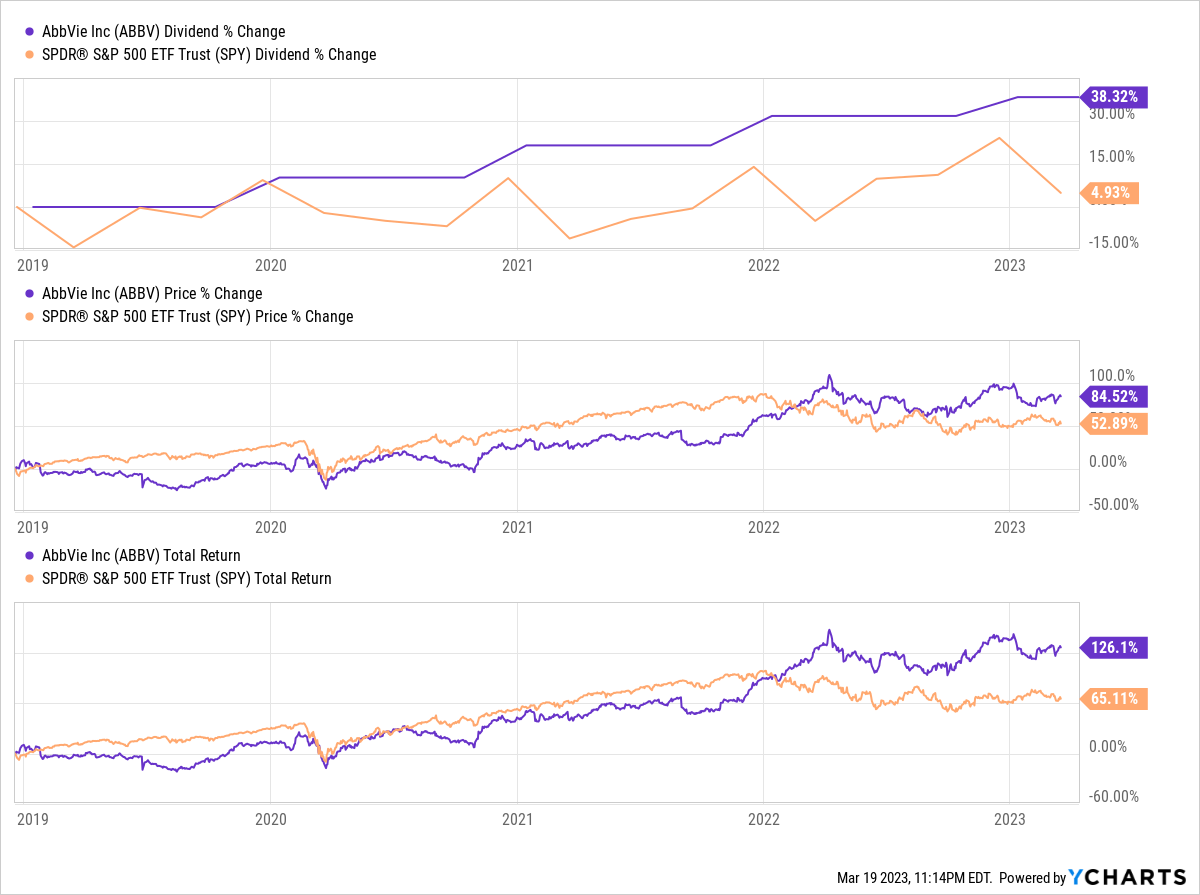

For example, when we first bought drugmaker AbbVie (ABBV) for the Income Builder Portfolio in December 2018, it had a 5% yield. Since then, its dividend has grown 38%, the price has appreciated 85% and the total return has been 126% — crushing the market in each metric.

The IBP would have missed out on some serious growth had we simply stuck the cash into a CD. Then again, we’d have been better off with CDs rather than a few stocks that have gone on to be losers.

Wrapping Things Up

Counting the $51.50 this brokered CD will generate over the next 6 months, the IBP’s projected annual income stream is now $4,722. That means we’re almost 95% of the way to the $5,000 target we established upon launching the portfolio.

Because the goal was to hit that mark within 7 years, we’re about 18 months ahead of schedule.

The purpose of this article isn’t to convince you to buy CDs instead of stocks (or vice versa). Only you know your own goals, risk-tolerance level and personal economic situation.

As always, readers are urged to conduct their own due diligence before making any investments.

— Mike Nadel

Silicon Valley venture capitalist Luke Lango says this little-known Apple project could be 10X bigger than the iPhone, MacBook, and iPad COMBINED! Investing in Apple today would be a smart move... but he’s discovered a bigger opportunity lying under Wall Street’s radar -one that could give early investors a shot at 40X gains! Click here for more details.

Source: Dividends & Income