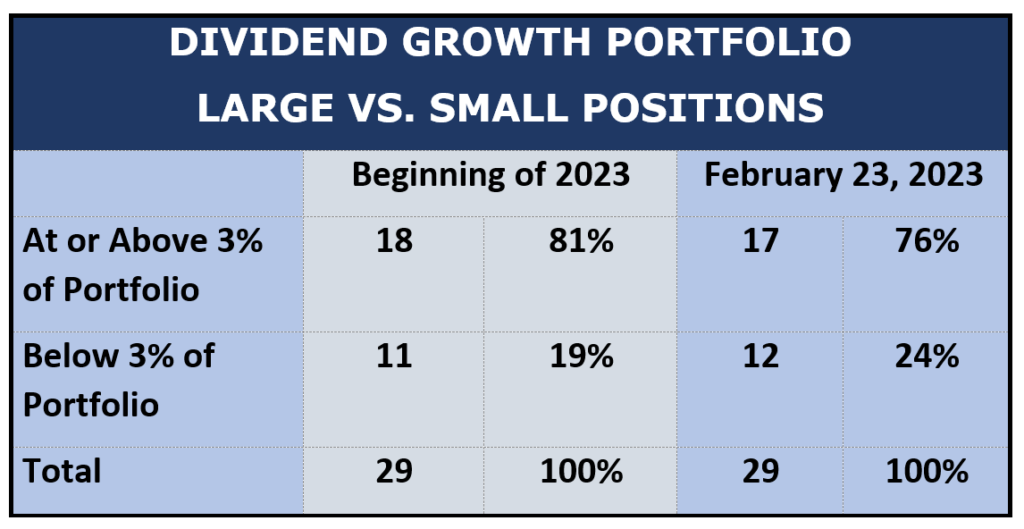

I am continuing this year to focus on the smallest positions in my public Dividend Growth Portfolio. I have been deciding which ones to keep and build up. Along the way, I have discarded a couple.

As of the end of February, this was my breakdown of positions by size compared to the beginning of the year:

Source: Author

Source: Author

The table makes it look like I have gone backward a little in shrinking the number of small positions, but in fact that is only because one stock – Texas Instruments (TXN) – went backwards in price, taking it just under the 3% cutoff size. In the long run, I am not worried at all about TXN.

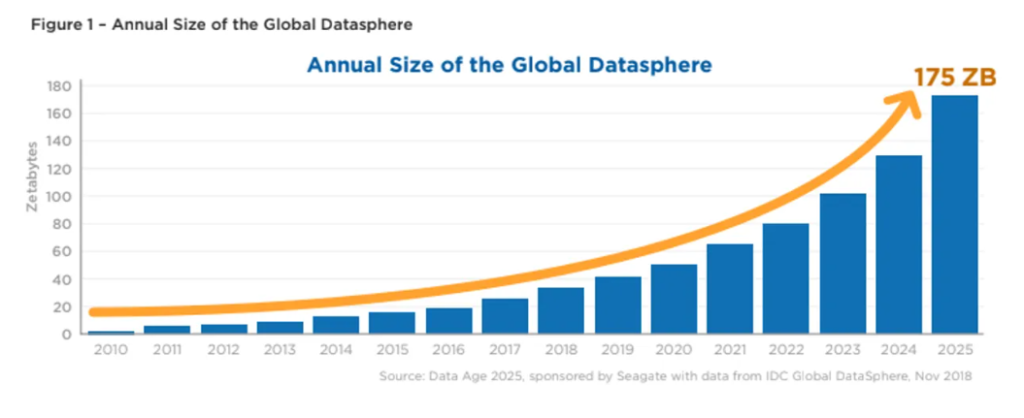

After looking over my other small positions, one jumped out at me as a high-quality stock that also feeds into a theme I have been emphasizing: The explosion of online data and the build-out of the infrastructure needed to create, store, and move it.

The rise in data creation is simply breathtaking. It is a result of the proliferation of smartphones, internet-connected devices, social media, and cloud computing.

The total data in existence is called the “datasphere.” The datasphere is growing exponentially:

Source

SourceIn the chart, ZB stands for zettabytes, which is a unit that denotes the sheer amount of electronic data. It is equivalent to 1,024 exabytes or 1,000,000,000,000,000,000,000 bytes.

The shape of the curve shows the opportunities for companies involved in filling data infrastructure needs. That leads to my stock selection this month.

Dividend Reinvestment for March, 2023: Crown Castle (CCI)

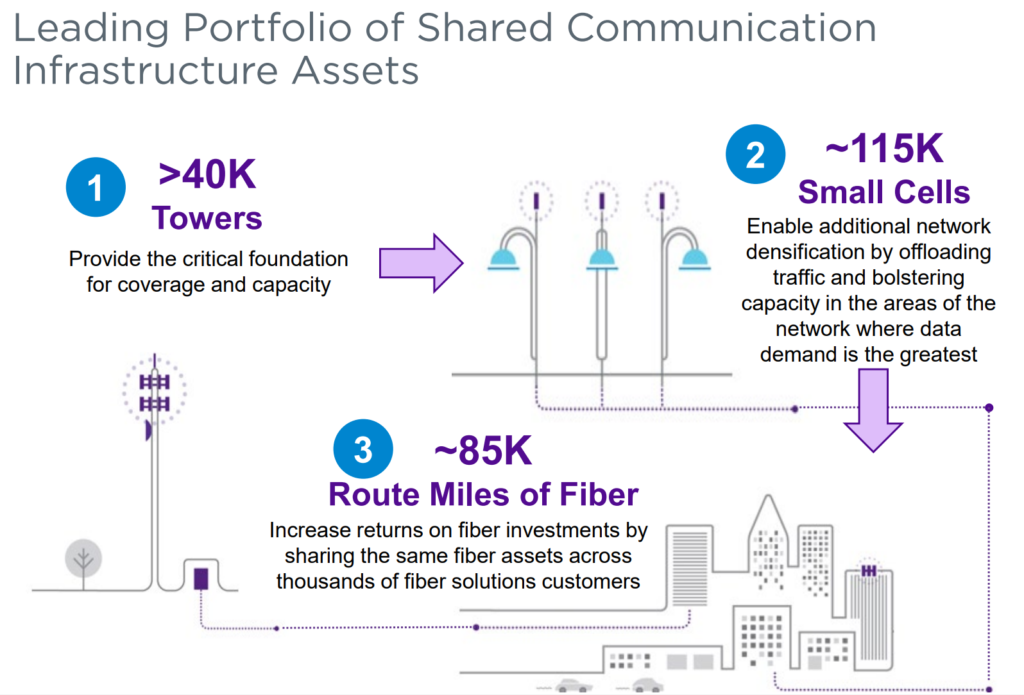

Crown Castle (CCI) is a REIT (real estate investment trust) that bills itself as the nation’s largest provider of shared communications infrastructure. It owns cell towers, short-range small cell nodes, and tens of thousands of miles of fiber. Its portfolio is entirely in the United States, and it has a presence in every major domestic market.

Source: Investor Presentation

Source: Investor PresentationCCI says that the existence of high-quality wireless networking in the U.S. has led to unprecedented growth in wireless data demand over the last decade, and that demand is projected to continue to grow at 25% per year through 2027.

As stated by CEO Jay Brown on their earnings call in January, CCI looks forward to about 5% organic growth in towers this year. “The established national wireless operators are deploying mid-band spectrum in earnest as a part of the initial phase of their 5G build-out.”

CCI also expects a doubling in the pace of deployments of small cells to 10,000 nodes in 2023, as customers will require small cells “at scale” as they build out their 5G networks. Brown stated that CCI has 60,000 nodes already on air and another 60,000 contracted. He believes that CCI is in the early innings of a decade-long growth opportunity in 5G.

Brown also said that CCI continues to support DISH with its nationwide build-out of a new wireless network, and he believes that CCI is “in a great position to continue to capture an outsized share of that opportunity.”

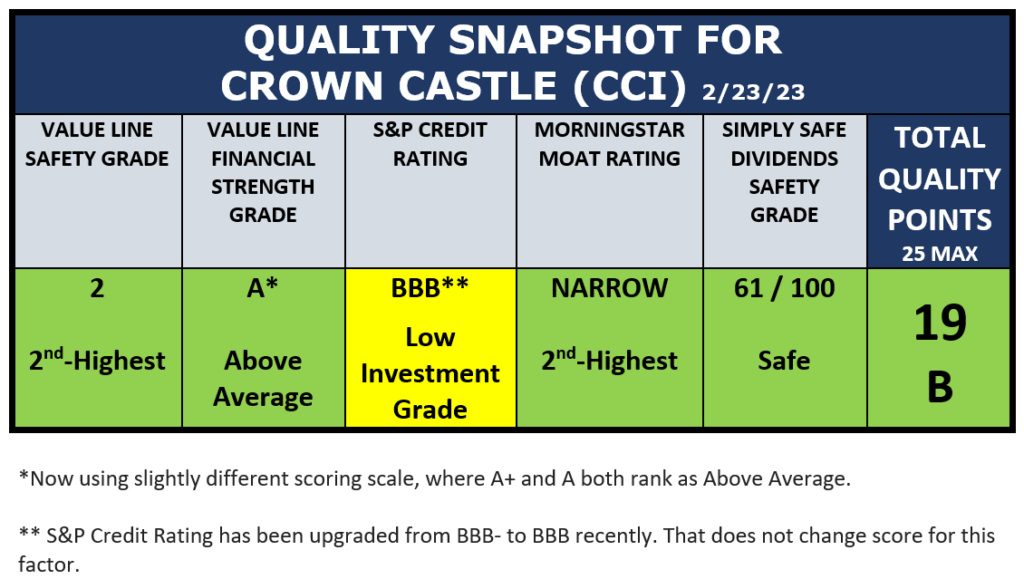

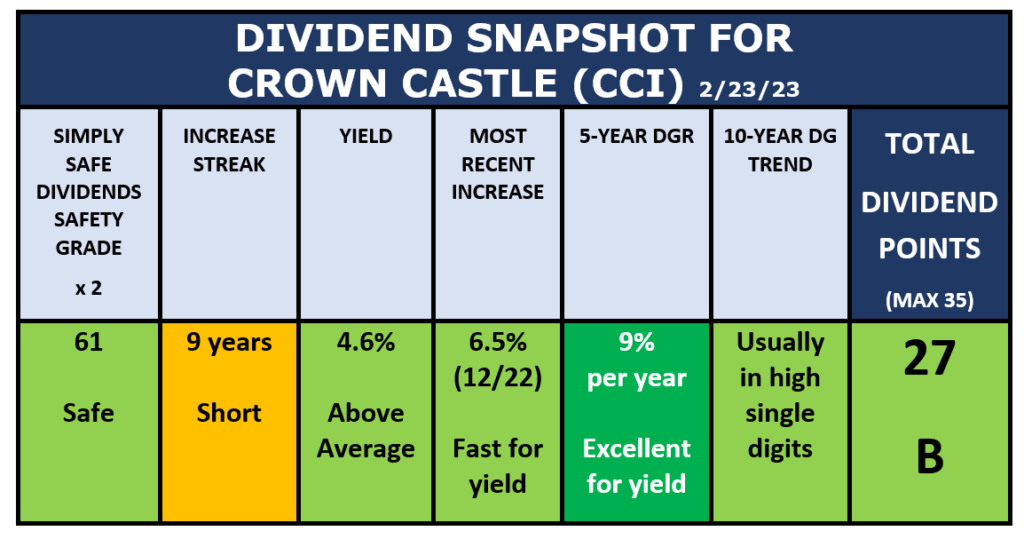

Here is Crown Castle’s Quality Snapshot. The company merits an Above-Average rating in overall quality.

Source: Author, from sources noted in table

Source: Author, from sources noted in table

Notice that since I purchased Crown Castle last year, its S&P Credit Rating has been raised a notch. That is a good sign, although it does not change the grade that I give it on that factor.

CCI’s dividend record is also Above Average.

Source: Author, using data from Simply Safe Dividends

Source: Author, using data from Simply Safe Dividends

This is an attractive dividend record. The only non-green category is CCI’s increase streak, which at 9 years is just one year short of the next step up, which will raise its grade by a point from “Short” to “OK.” CCI has been paying and raising its dividend since it officially became a REIT in 2014, so its growth streak is as long as it could be.

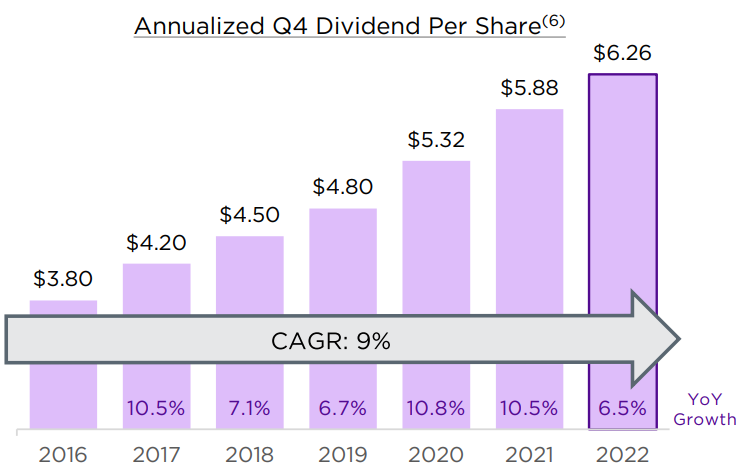

CCI has expressed its commitment to dividend growth, as shown in this graphic from its most recent investor presentation.

Source: Investor Presentation

Source: Investor PresentationIn the conference call accompanying that presentation, CEO Jay Brown added that CCI looks to establish a long-term annual dividend per share growth target of 7% to 8% per year.

If CCI follows its established schedule, its next dividend increase will be announced later in the year and will be payable in December.

CCI’s upcoming March dividend has already been declared, and because its ex-dividend date is March 14, the shares I am buying now will qualify for the March payout.

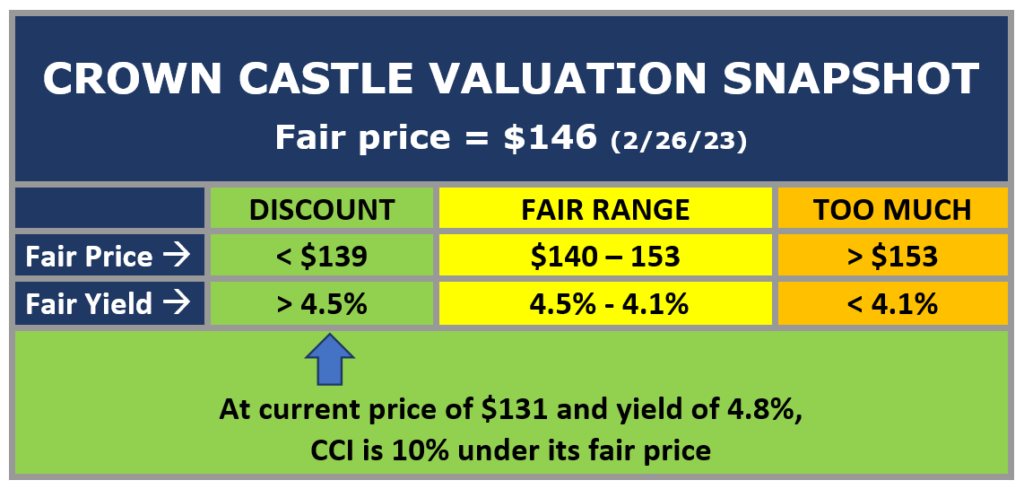

The final step in deciding on Crown Castle is its valuation. I only buy stocks when they are fairly valued or on sale. When valuing a stock, I use several valuation models and then average them out.

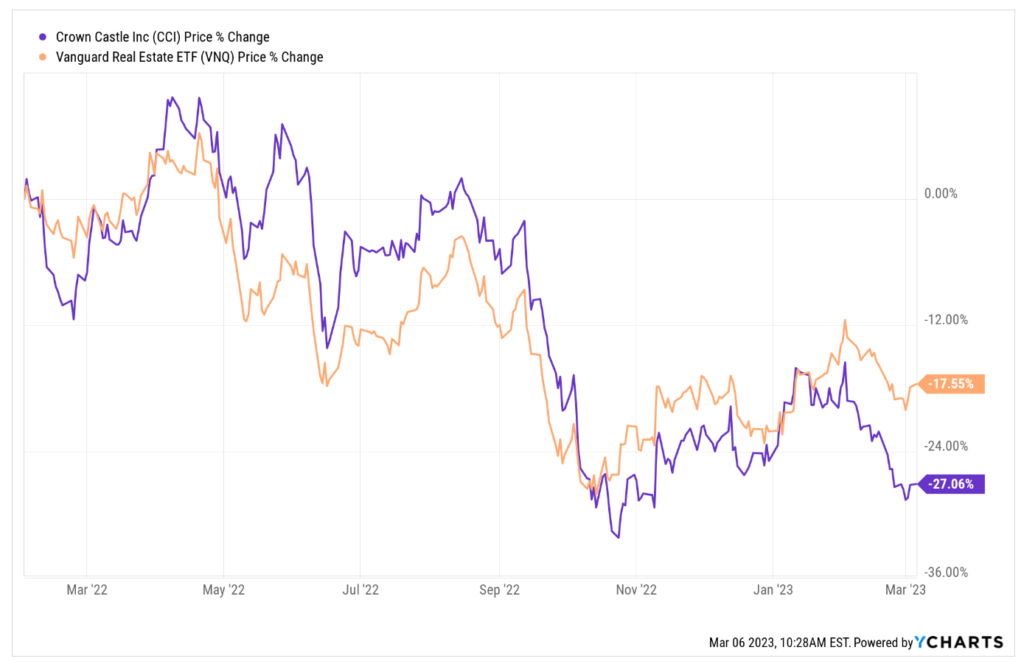

Valuation is a function of price compared to a stock’s fair (intrinsic) value, and since I first bought CCI in February 2022, its price has gone down, including a sharp recent drop that has been steeper than the REIT sector’s performance.

Since CCI is a high-quality stock with good growth prospects, that price drop would appear to create a nice buying opportunity. To verify that, I use a multi-step process for valuing stocks. If you want to see how I figure valuations, click on this video:

Since CCI is a high-quality stock with good growth prospects, that price drop would appear to create a nice buying opportunity. To verify that, I use a multi-step process for valuing stocks. If you want to see how I figure valuations, click on this video:

Here is my valuation summary for Crown Castle:

Here is my valuation summary for Crown Castle:

Source: Author

Source: Author

By my reckoning, CCI is selling for about 10% less than it is fairly worth.

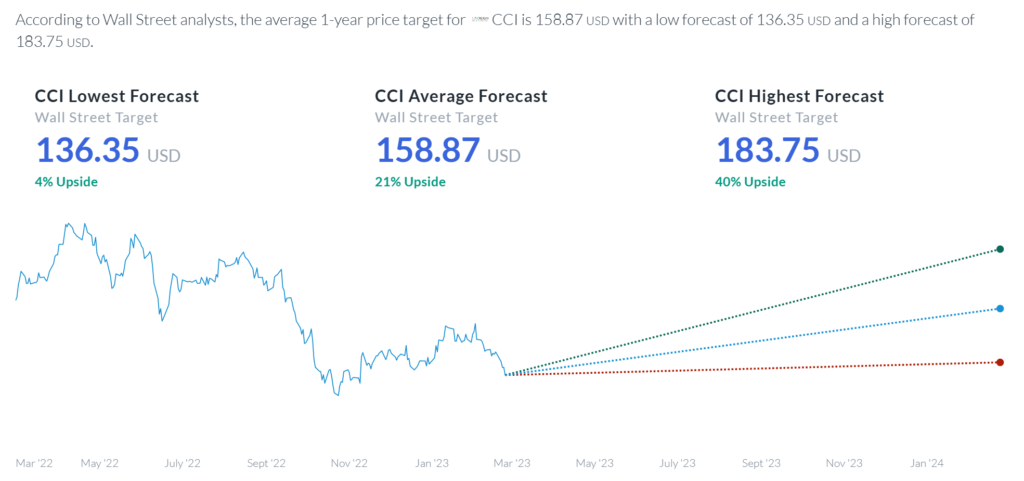

This is in the same range as Wall St. analysts. The following chart shows analysts’ average one-year price targets for CCI.

Source: AlphaSpread

Source: AlphaSpread

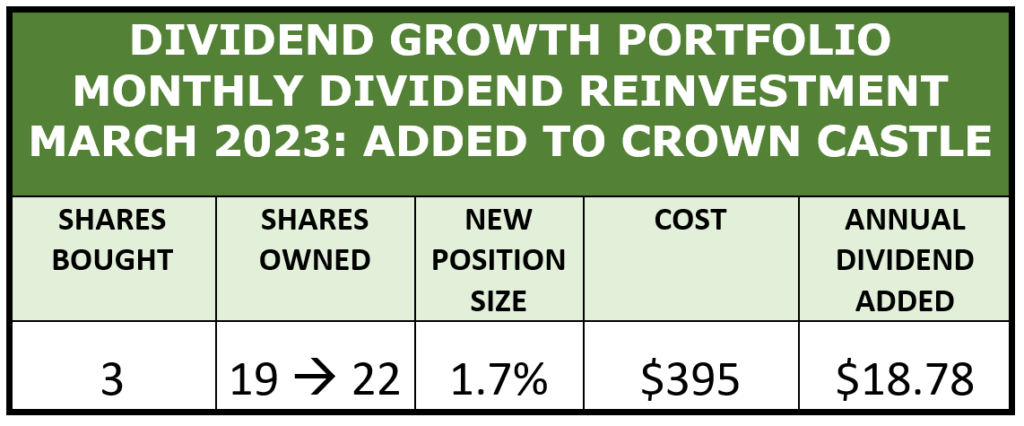

Therefore, I went ahead on March 6 and made this month’s regular dividend reinvestment by purchasing 3 shares of Crown Castle (CCI).

Source: Author

Source: Author

Here is my updated position in CCI. I highlighted the new total of CCI shares that I own and the percentage of the account that CCI now occupies.

Source: Simply Safe Dividends

Source: Simply Safe Dividends

Because CCI is still under 3% of my portfolio, it remains a candidate for further expansion provided its quality, fundamentals, and valuation remain favorable.

Dividend Growth Portfolio Update

Let’s move on from CCI to consider my Dividend Growth Portfolio more broadly. The DGP is a public, real-money, real-time portfolio that I started in 2008 to illustrate (and profit from!) dividend-growth investing.

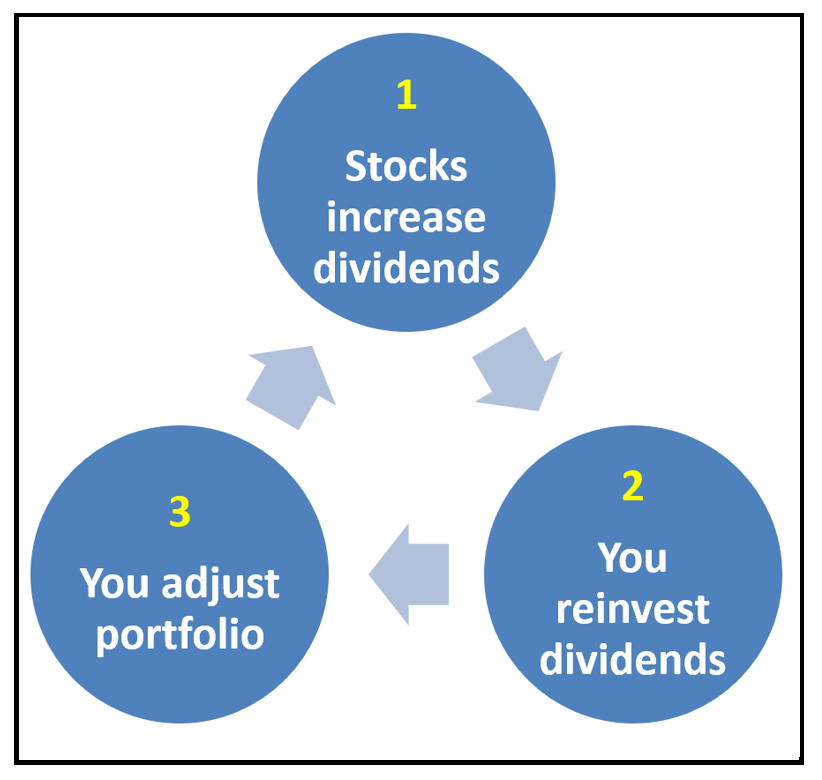

There are three reasons that dividends go up relentlessly in a DG portfolio.

Source: Author

Source: Author

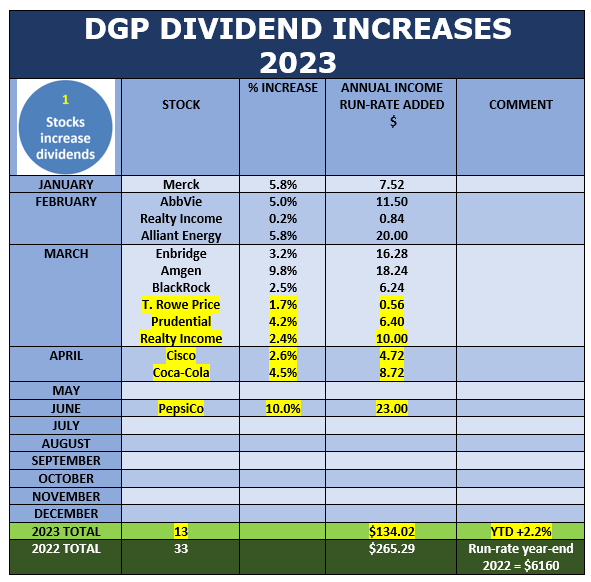

The first reason that the dividend stream grows is that I own stocks that usually raise their dividends one or more times each year. The following table shows the DGP’s dividend-increase record so far in 2023. New increases announced since last month are highlighted in yellow.

Source: Author, from company announcements

Source: Author, from company announcements

By the end of the year, I expect that the portfolio’s annual dividend run-rate will go up around 5% from dividend increases alone.

As the investor, I am not required to do anything to make this happen. The companies do it themselves. My only involvement is to have picked companies that will probably keep raising their dividends, and to continue to add to them by reinvesting accumulated dividends each month.

That’s what I just did by adding shares of Crown Castle. By reinvesting dividends, I added more shares. Since dividends are paid per share, that causes the portfolio’s income to go up.

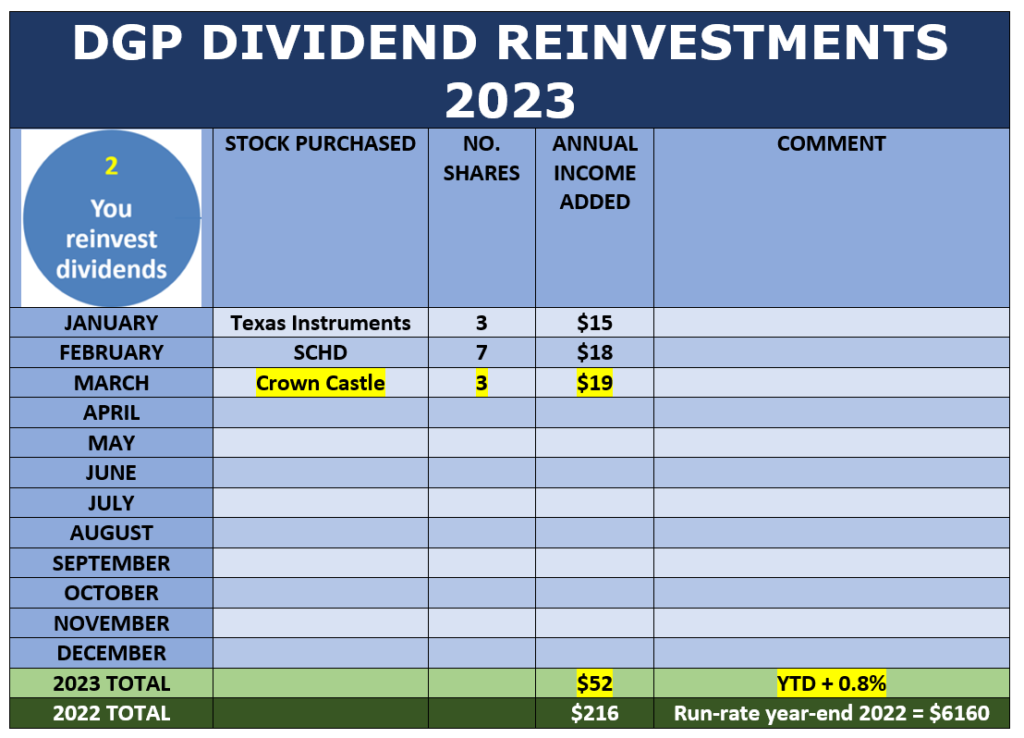

This table shows how my monthly dividend reinvestment program is going so far in 2023.

Source: Author

Source: Author

The reinvestment program is running smoothly. By the end of the year, I expect that the reinvestments, by themselves, will add about 3.3% to the portfolio’s dividend run-rate.

So the first two reasons – dividend increases and dividend reinvestments – will probably combine to add more than 8% to the portfolio’s annual rate of paying dividends.

So far this year, I have not employed Reason #3. I have not sold or trimmed any holding nor redeployed the money elsewhere in the portfolio. That said, I think that before the year is over I will probably end my experiment with QYLD (an ETF based on generating income by selling covered calls), and I may pull the plug on another holding or two, depending on how circumstances develop.

Overall, however, right now I am pretty satisfied with the DGP. Its performance over its lifetime has met or exceeded the hopes I had when I started it. If you want to see the positions in the portfolio at any time, its status as of the end of the previous month is always available here. That location also has an archive listing with links to all the articles and videos that I have published about the portfolio.

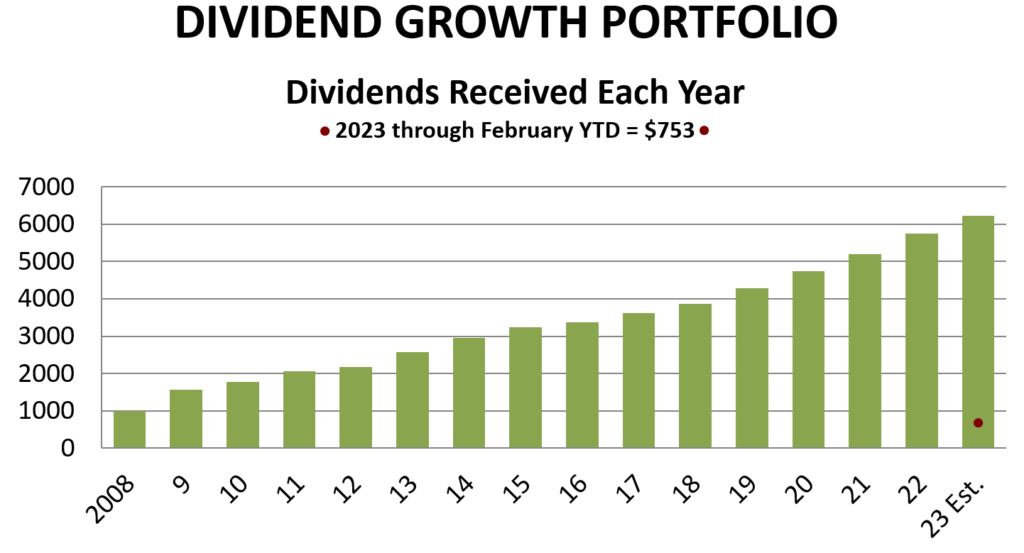

The following is my favorite chart for the portfolio. It sums up why I invest using the precepts of dividend-growth investing.

Source: Author

Source: Author

Next is a new analysis that I created showing the portfolio’s holdings arranged by yield (low to high) and 5-year dividend growth rate (slow to fast). As a general principle, I want holdings that generate higher dividend income and grow it quickly. As you can see, the vast majority of the DGP’s holdings meet those criteria. And of course, this is done in consonance with holding stocks whose dividend safety is reliable.

Source: Author

Source: Author

Remember, I do not present this portfolio as best or a model for what anyone else should do. I show what I do and why I do it, in the hopes that other investors will find it inspirational and educational for their own purposes.

Thanks for reading!

-–Dave Van Knapp

Marc Lichtenfeld - Author of the best-selling book Get Rich With Dividends – is giving away his Ultimate Dividend Package... Free of charge! Click Here to Get His #1 Dividend Stock... The Safest 8% Dividend in the World... Top Three "Extreme Dividend" Stocks, And Much, Much More.

Source: Dividends & Income