As an investor, I obviously like it when one of the top companies in my stock portfolio presents an outstanding earnings report and offers encouraging guidance for the year to come.

And as an investor who wants most of his stocks to help his income stream grow, I absolutely love it when that same high-quality company announces a surprisingly robust dividend increase.

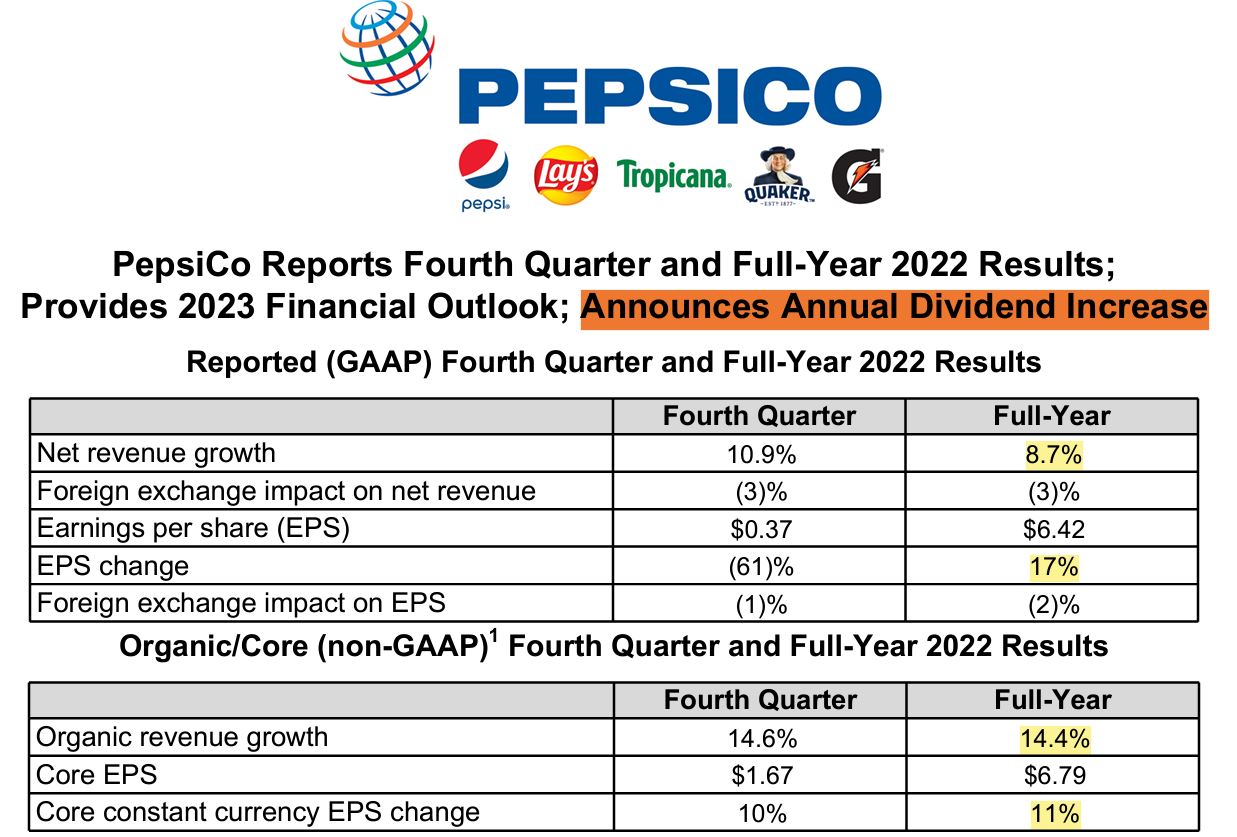

So I sure was digging it when PepsiCo (PEP) revealed last week that it had beaten expectations for earnings and revenue, forecast solid growth in both categories for 2023, and then topped it all off with a 10% hike to its dividend.

pepsico.com

Given that Pepsi is the third-largest holding in my personal portfolio, I celebrated the beverage and snack-maker’s report with an ice-cold Pepsi Zero Sugar and a bowl of Fritos.

And I followed that up by choosing PEP as the primary February buy for the Income Builder Portfolio, the real-money, public project I’ve been managing for 5+ years.

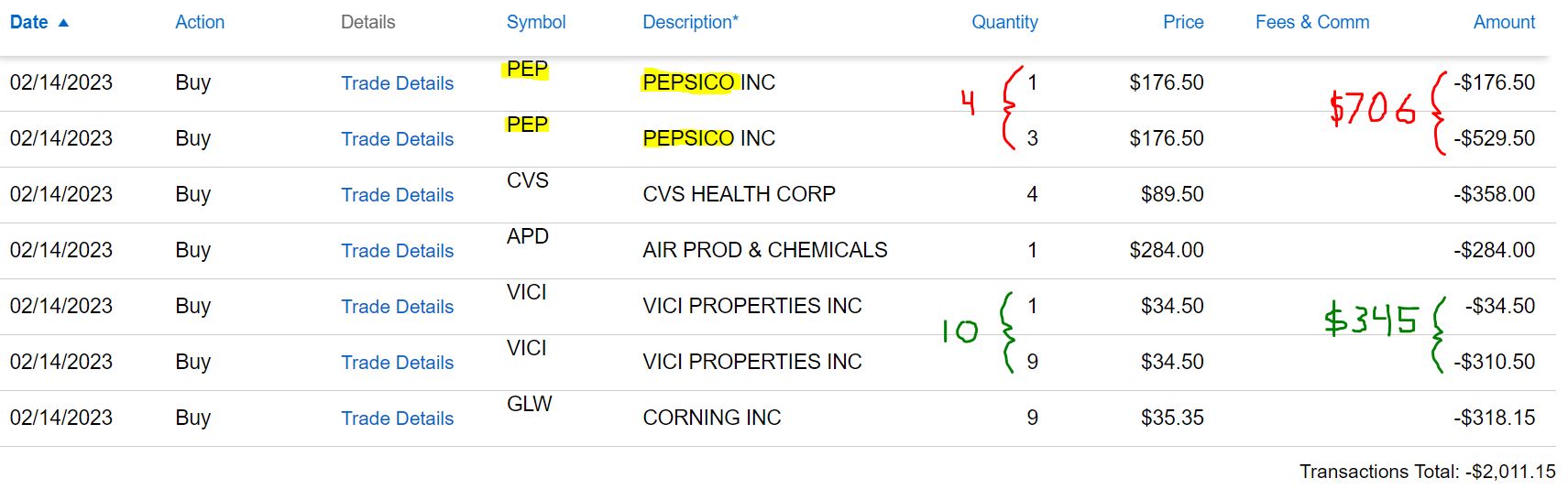

We added 4 shares to the portfolio’s existing PEP position on Tuesday, Feb. 14, when I executed a purchase order on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

As can happen with limit orders, the PEP and VICI buys each executed in 2 transactions a moment apart.

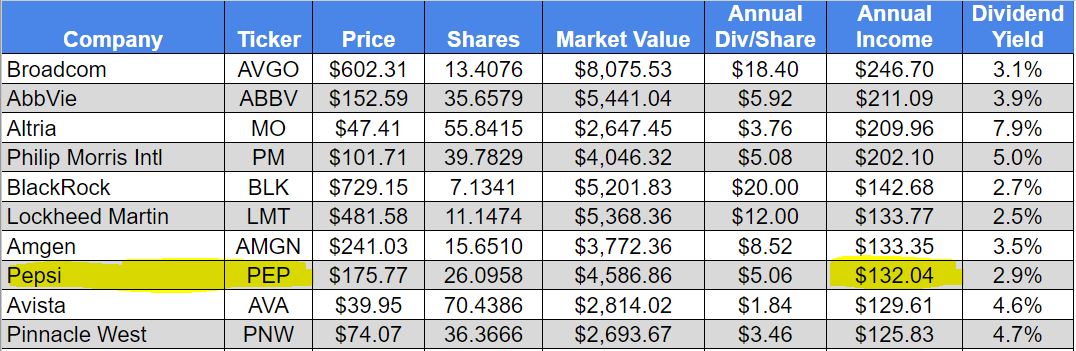

I used the rest of Greg’s $2,000 monthly allocation to beef up positions in four other dividend-growing stocks: CVS Health (CVS), Air Products & Chemicals (APD), VICI Properties (VICI) and Corning (GLW).

I’ll talk a little more about those companies later; the main focus of this article is Pepsi, a Dividend King (50+ consecutive years with dividend raises) that has been a market-crushing performer for the Income Builder Portfolio.

Market Masher

PEP was one of the first stocks we bought after launching the IBP in 2018, as we initiated our position with a $1,005 purchase on Feb. 27 of that year. Pepsi’s total return of 84% since then has easily bested the performance of the SPDR S&P 500 Trust ETF (SPY), a proxy for the overall market.

We bought $910 more worth of PEP on Oct. 30, 2018, and then spent another $333 on the stock on July 21, 2020. Including our February 2018 purchase, the cost of our Pepsi position was about $2,248.

At market close Feb. 10, 2023, the position was worth $3,893 — a total return of 73%.

Had we instead used the exact same amount of money on the exact same dates to buy SPY, the total return would have been a much lower 58%, as illustrated in the following table:

OK, that’s what Pepsi has done for the IBP (and investors like myself) throughout the years. Let’s talk a little about more recent times.

Growth, Growth & More Growth

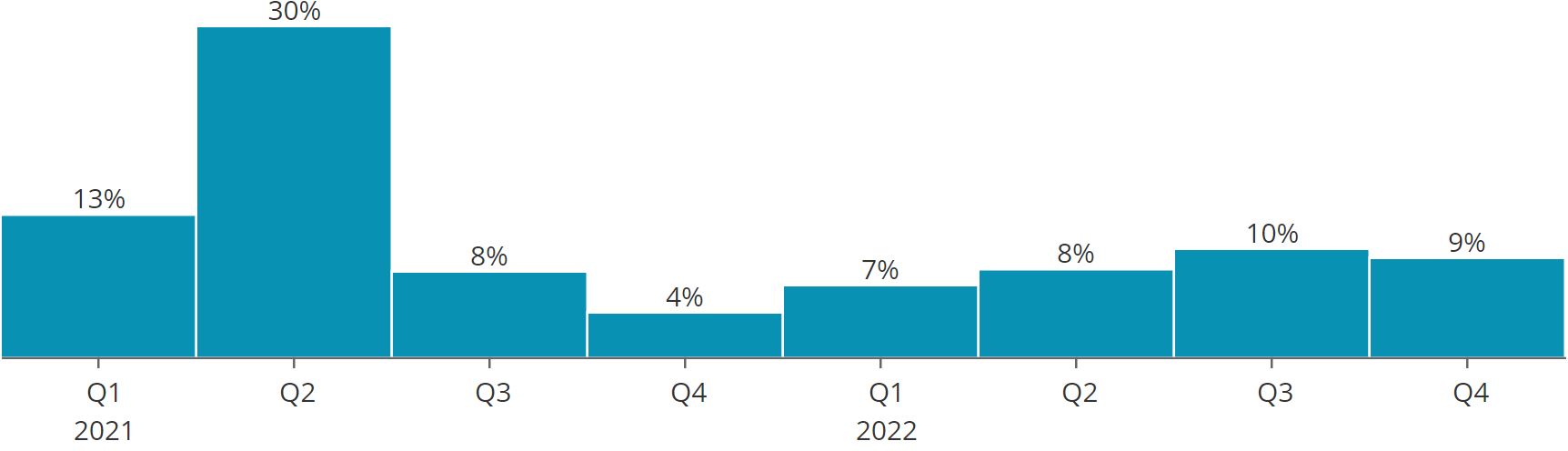

Emerging from the depths of the COVID-19 pandemic, the company has steadily grown earnings, quarter after successful quarter.

SimplySafeDividends.com

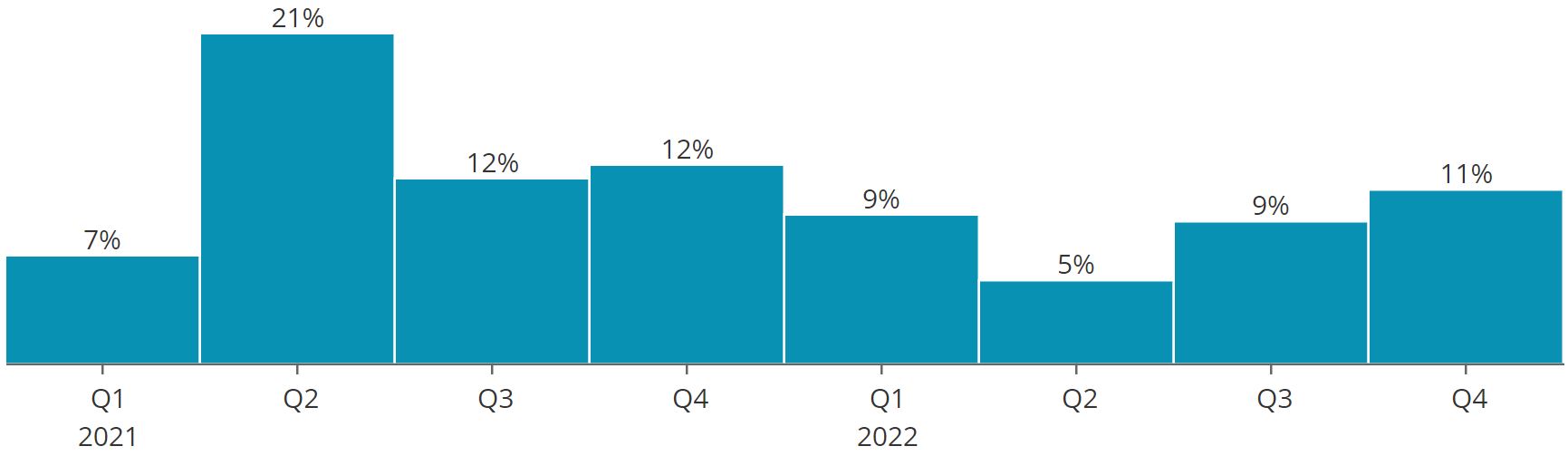

The same is true for revenue, with six quarters of at least 9% year-over-year sales growth.

SimplySafeDividends.com

Morningstar Investment Research Center was impressed with Q4 2022, and with Pepsi’s performance overall. Here’s what analyst Dan Su had to say:

The strong fourth-quarter results from wide-moat PepsiCo reinforced our confidence in the firm’s growth strategies around brand investment, product innovation, and channel expansion. The firm delivered a 15% increase in organic revenue (powered by an 18% snack sale expansion), and 10% growth in adjusted EPS, slightly ahead of our 9% and 5% respective estimates. After incorporating the better-than-expected results, we plan to raise our $170 fair value estimate by a low-single-digit percentage and view the shares as fairly valued.

We attributed the strong top line to a sharper focus on branding, research, and channel relations. We view creative marketing on localized content, coupled with innovation around new ingredients (for example, high-protein chickpeas) and package offerings (bite-size fare in easy-to-pour canisters), as crucial to driving double-digit volume growth in core brands Doritos, Cheetos, and Lay’s. We’d also point to Pepsi Zero Sugar volume growth (28%) and accelerating sales for energy drink brands Rockstar and Celsius as evidence that thoughtful marketing and consumer-centered innovations are a powerful combination to fuel sales expansion. …

On margins, we are impressed by PepsiCo’s ability to fully offset double-digit commodity cost inflation with pricing, point-of-sale execution and manufacturing efficiency gains, holding fourth-quarter gross margin (52%) flat year over year. Higher investments in advertising and channel partners hurt operating margins in the quarter (down 240 basis points, to 8.5%), though the full-year margin remained solid at 13.3%. We expect the firm to keep investing at these levels, which should bode well for its long-term competitive position.

I agree with that analysis, and I used red to highlight something that separates Pepsi from its beverage-producing peers: its strong and popular snack division, which offers the likes of Fritos, Doritos, Cheetos and Lays to the hungry masses.

Sales in that realm grew by 18%, enough to fuel all the growth for the company in the quarter.

Pepsi added PopCorners (kind of a chip/popcorn combo) to its product line in 2019, and the company’s Super Bowl ad — featuring characters from the iconic TV program Breaking Bad — was deemed a “winner” by most critics.

usatoday.com

The last year or so, inflation has been a drag on the bottom lines of most companies, and Pepsi has not been immune. But so far at least, the firm has been able to counteract the worst of it by raising prices — especially on its snacks.

I mean, what’s another buck or two when a person just has to have some Hint of Lime Tostitos?

And when it comes to quality, there aren’t many companies out there ranked higher than Pepsi.

Tasty Dividend

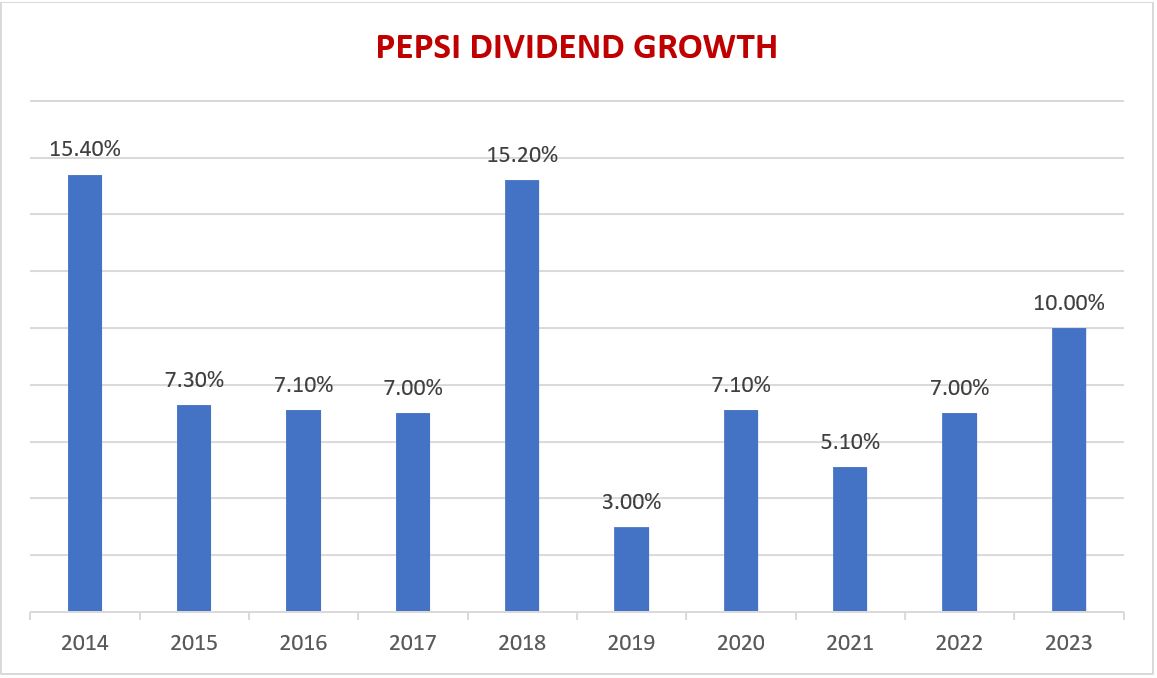

The last few years, Pepsi has “pre-announced” its dividend increase. Even though it still has one more divvy to distribute at the current rate on March 31, the company last week said it would lift the dividend by 10% year-over-year starting with its June 30 payment.

That PEP grew its dividend is nothing new — this will be its 51st consecutive year with an increase.

What was nice this time was the double-digit-percentage hike, one of its largest of the last decade.

Such a robust raise is a sign that management is committed to the dividend. The increase (along with a plan to buy back $1 billion in stock) also shows confidence in the company’s ability to keep growing earnings and free cash flow.

Here’s what CFO Hugh Johnston had to say during the earnings call with analysts:

The capital allocation principles we have are no different than what we’ve had in the past, the four basics of: make sure we invest in the business, pay the dividend, tuck-in acquisitions and share repurchase.

If I zero it in a little bit more for the environment that we’re in right now with some of the changes, I think our biggest priorities right now are going to be continuing to invest in the business and growing the dividend. And that’s not just a today statement — although obviously 10% dividend growth is a pretty healthy growth in our current environment. … The 10% dividend growth is bigger than what we’ve done in a number of years, and I think you’ll see us prioritize that a bit more over time.

That last sentence, highlighted in red, is as delicious as Nacho Cheese Doritos and as refreshing as a Gatorade Zero!

The combination of the dividend hike and the IBP’s latest 4-share buy vaulted Pepsi into the top 10 income-producers within the portfolio.

Of the five stocks we bought for the IBP in February, four have raised their dividends in the last couple of months — including CVS by 10% in December, Air Products by 8% in January and Corning by 4% last week. (VICI Properties announced an 8.3% increase last September.)

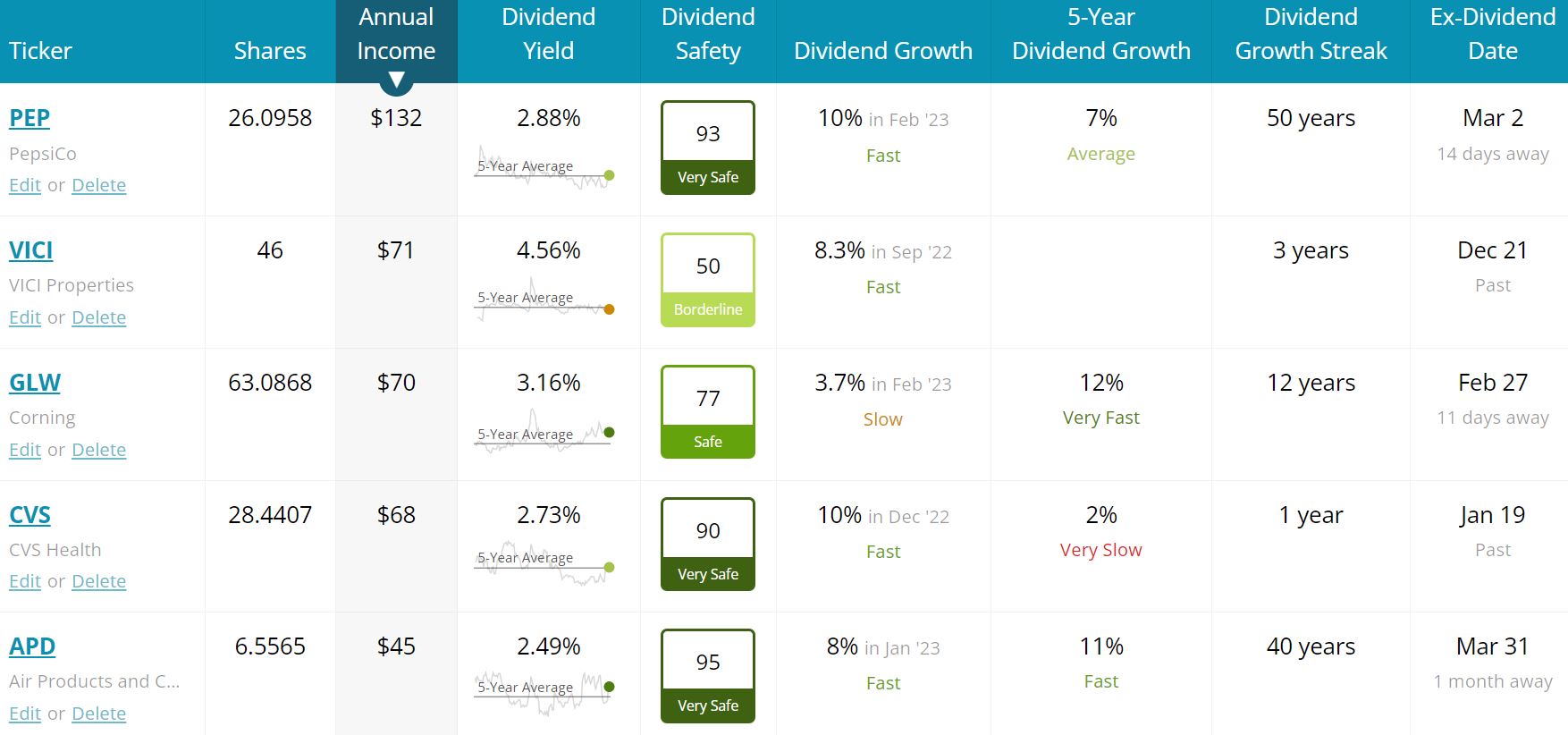

Here’s some income-related data on all of our February buys, courtesy of Simply Safe Dividends:

SimplySafeDividends.com

The five positions are expected to contribute about $400 to the IBP’s income stream over the next year. These buys pushed the portfolio’s projected annual dividend count past the $4,600 mark — meaning we are more than 92% of the way to our $5,000 target.

Pepsi’s ex-dividend date is March 2, so to receive the next quarterly payout of $1.15 (its last at the pre-raise rate) an investor must own shares by March 1. Others with upcoming ex-dividend dates are Corning (Feb. 27) and Air Products (March 31) — again, one must own each stock the previous day.

Valuation Station

Although analysts repeatedly call Pepsi a thriving, well-run company, most do not consider it a screaming buy here. Only half of the 24 tracked by Refinitiv put it in either the Strong Buy or Buy category, and two doubters even recommend selling PEP.

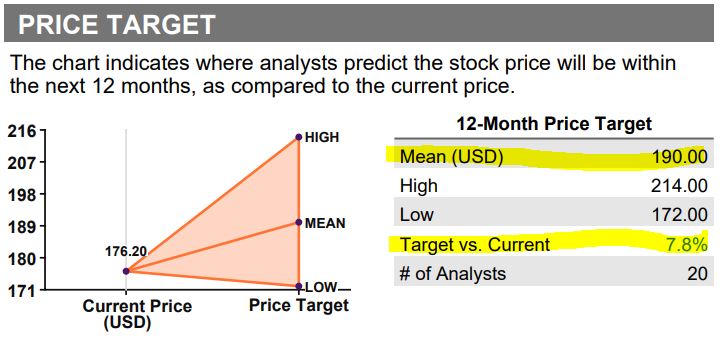

Refinitiv, via fidelity.com

The Refinitiv analysts’ average 12-month price target is $190, suggesting an upside of about 8% — not bad at all, but hardly a table-pounding number.

Refinitiv, via fidelity.com

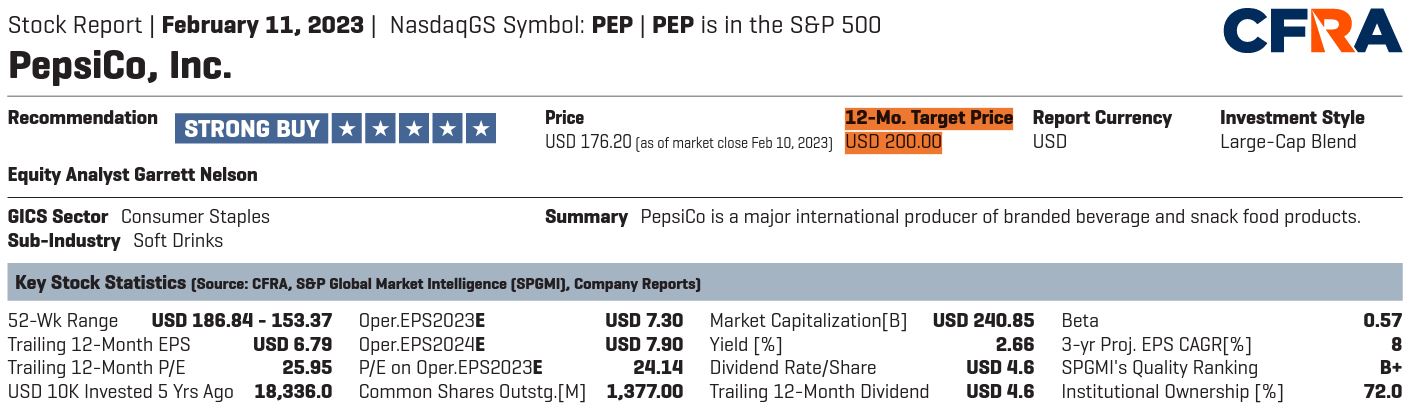

Still, there are plenty of analysts with a thirst for Pepsi now. CFRA’s Garrett Nelson, for example, calls it a Strong Buy with a price target of $200.

CFRA, via schwab.com

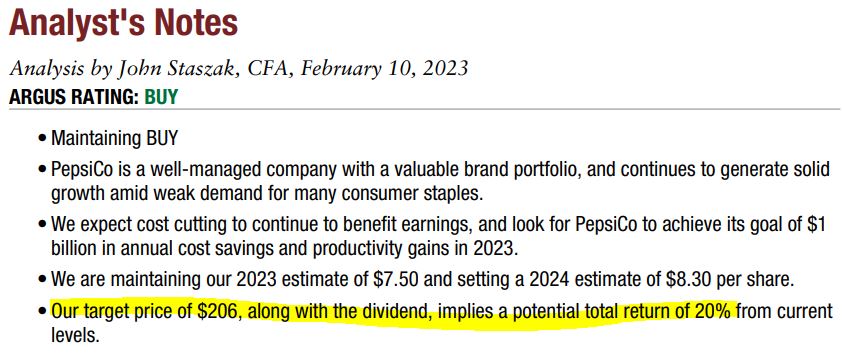

Argus analyst John Staszak, meanwhile, was impressed with the earnings report and has a $206 target on the stock.

Argus, via fidelity.com

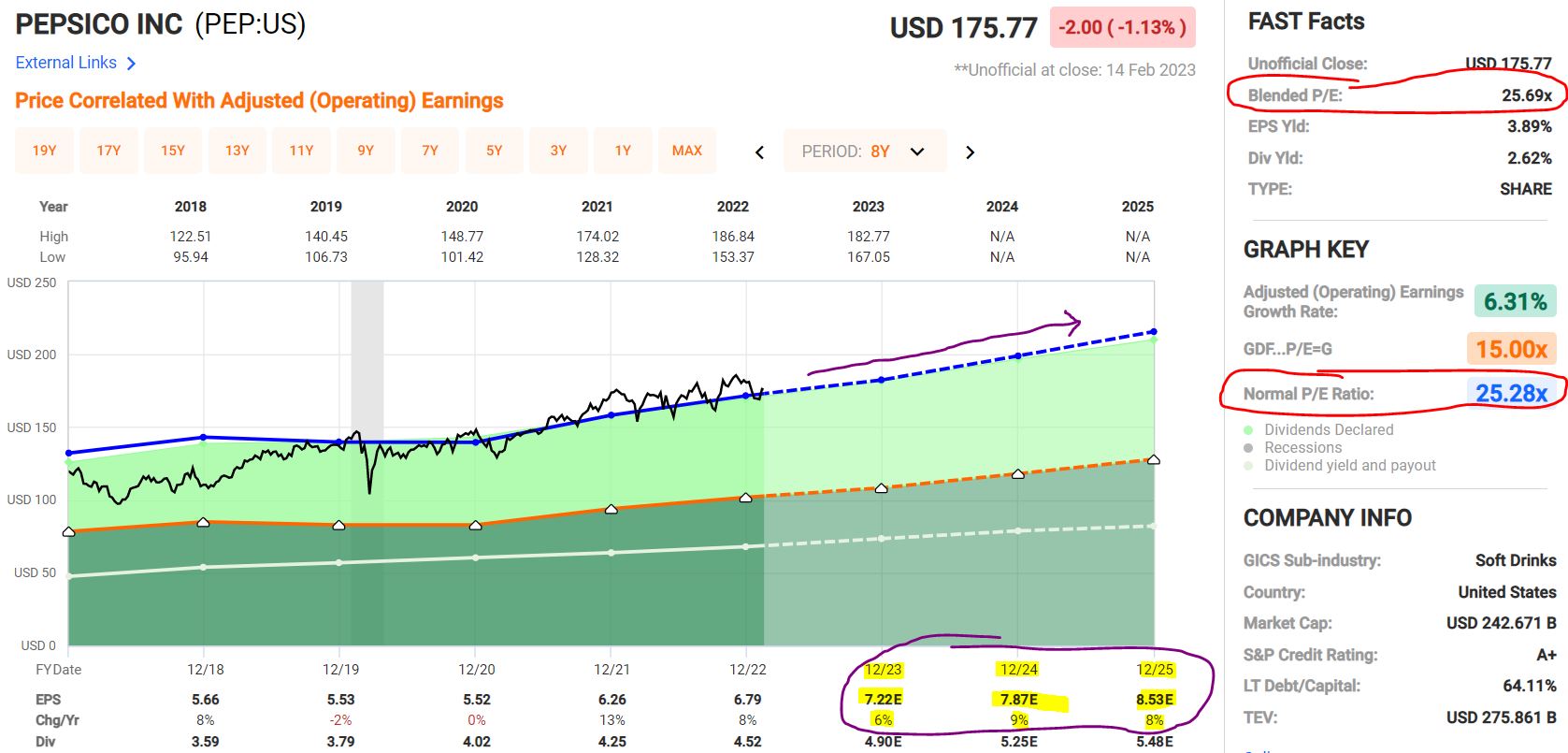

FAST Graphs shows a company that is fairly valued relative to its 5-year history.

fastgraphs.com

The purple and yellow markings in the above graphic illustrate the direction Pepsi earnings are expected to take in the coming years … and that direction is “up” at a steady pace. As an investor, that’s what I like to see.

Here’s a look at various valuation metrics and analyst opinions regarding all five February IBP buys:

+Morningstar said it will raise its fair value estimate by a “low single-digit percentage.” … *As a REIT, VICI is valued using price/adjusted funds from operations rather than price/earnings.

Wrapping Things Up

When selecting stocks for the Income Builder Portfolio, I’m always trying to balance quality and valuation.

With Pepsi coming off an outstanding earnings report, raising its dividend for a 51st straight year and yielding about 3%, I felt this was a decent time to bump up the position size of one of the best consumer staples names around.

But PEP certainly is not a bargain-hunter’s delight. Even though I agree with Morningstar that shares are fairly valued, I can see how some investors might opt to wait for better buying opportunities.

As for the four other stocks we bought in February: VICI was last month’s main selection for the IBP (read about it HERE); we initiated our GLW position in May (HERE); APD was first purchased in December 2021 (HERE); and CVS entered the portfolio in June 2021 (HERE).

As always, investors are urged to conduct their own thorough due diligence before buying any stocks.

— Mike Nadel

Buy this small group of unique stocks... never sell them... and make all the money you need... No matter what happens in the market. Revealed here: the name and ticker of the #1 stock.

Source: Dividends & Income