What’s better than a safe 11% dividend? How about one with 11% upside or more, too!

Oil and gas stocks are in the midst of a multiyear bull market. China is about to reopen, which will reignite energy demand.

Which means the time to buy the dip in the black goo—especially dividend-paying energy stocks—is right now.

Let’s start with that 11% payer which also boasts a unique dividend distribution model.

A Twisted Path to Big Energy Dividends

Pioneer Natural Resources (PXD), a Texas-based oil exploration company that’s a pure player in the enormous Permian Basin, yields 11%.

Eleven percent!

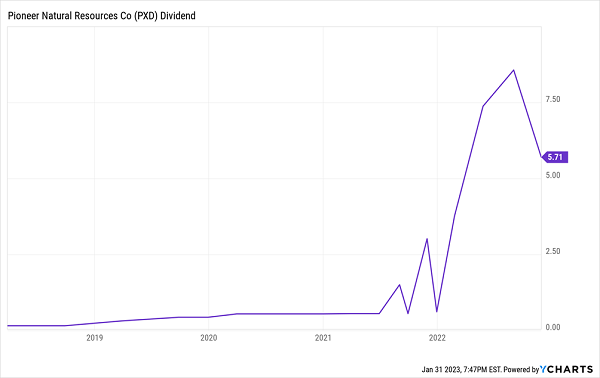

Risky? Well, we must take the time to properly understand its payment plan. PXD’s most recent dividend of $5.71 per share is more than 10 times the payout it delivered just two years ago—a wild dividend growth story, but one with a (misleading) hiccup—the surface worry that PXD’s dividend is now on the decline:

Did PXD’s Dividend Just Get Cut by 33%?

It’s not. (Be careful with internet charts!) This is simply a reflection of PXD’s “fixed-plus-variable” (FPV) dividend model.

It’s not. (Be careful with internet charts!) This is simply a reflection of PXD’s “fixed-plus-variable” (FPV) dividend model.

FPV Dividends: Answers to 2016 and 2020

We all know the usual dividend routine: A company pays a certain amount every so often this year, then next year, they keep it the same or make it bigger. That goes on and on until some bad thing happens, and suddenly, shareholders are hit with a sudden dividend cut—15%, 30%, 50%, you name it.

This played out during the 2014-15 energy crash, then again during 2020’s brief bout with negative oil prices, with these notable cuts:

- Kinder Morgan (KMI) slashed its payout 75% in 2015.

- ConocoPhillips (COP) hacked 65% off its dividend in 2016.

- Energy Transfer LP (ET) sawed its distribution in half in 2020.

Even the dividends of blue chips Chevron (CVX) and Exxon Mobil (XOM) were called into question!

The challenge in this business is that they are beholden to a single factor—oil prices—that is largely out of their control, and that can vary widely.

That’s why the fixed-and-variable model makes sense for energy firms. It’s almost identical to companies that distribute special dividends in addition to their regular dividends, but 1.) both the fixed and variable dividends are distributed in one payout, and 2.) the variable dividend is usually tied to some sort of preset ratio. For instance, Pioneer management has a target of distributing 75% of free cash flow (after payment of the base dividend).

Thus, shareholders in PXD (and a couple stocks like it—more on them in a moment) are uniquely situated to benefit twofold from higher oil prices: appreciating shares and plumper payouts.

So, why expect oil prices to rebound in 2023?

The Crash ‘n Rally Pattern: Still in the Rally Phase

The overarching reason I remain bullish on the energy sector is one of my favorite investing phenomena. It’s called the “crash ‘n rally” pattern—a pattern in oil prices that we saw play out between 2008 to 2012, and that has been unfolding yet again over the past couple of years.

You can check out this recent post to learn more about the subject, but in short, the crash ‘n rally tends to play out across five steps:

- First, demand for oil evaporates due to a recession. The price of oil crashes (2008 and 2020).

- Next, energy producers scramble to cut costs. They cut production aggressively (2008 and 2020).

- Then, the economy slowly recovers. Energy demand picks up (2009 to 2012, 2020 to today).

- But there’s not enough supply! So, the price of oil climbs and climbs and climbs (2009 to 2012, 2020 to today).

- Energy producers bring supply back online, but it takes time to explore and drill. Supply lags demand for years, and the price of oil climbs and climbs (2009 to 2012, 2020 to today).

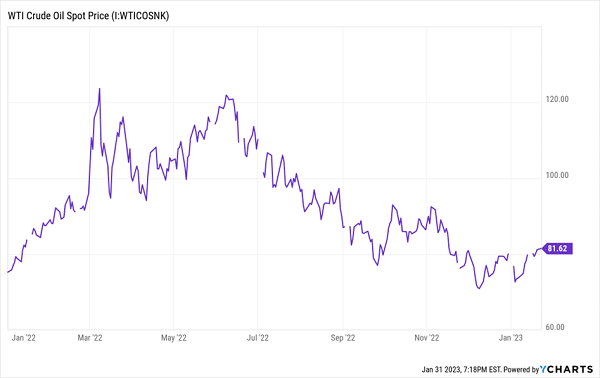

Disbelievers in this phenomenon typically latch onto short-term pauses or regressions in oil prices, like the current multi-month rut that has black gold priced around $80 per barrel—well off last year’s high of $130.

Is the Oil Rally Really Out of Fuel?

But I think energy bulls have a few reasons to get excited.

But I think energy bulls have a few reasons to get excited.

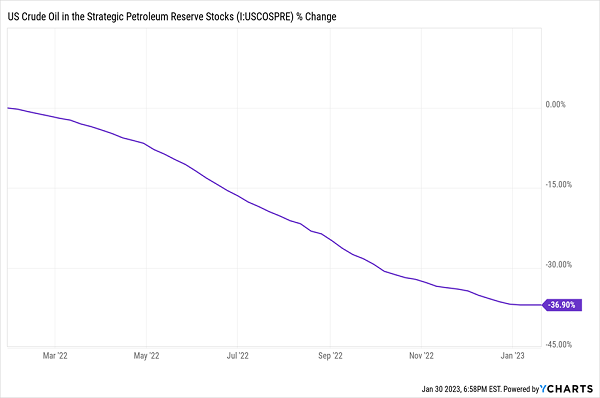

For one, the Biden Administration spent much of 2022 trying to tamp down oil prices by withdrawing from the Strategic Petroleum Reserve (SPR).

SPR: Off 37% in Just a Year!

That needle is about to start pointing in the other direction. In late December, the Department of Energy announced an oil repurchase to replenish the SPR—and the more the DoE buys back, the more that demand will nudge oil prices higher.

That needle is about to start pointing in the other direction. In late December, the Department of Energy announced an oil repurchase to replenish the SPR—and the more the DoE buys back, the more that demand will nudge oil prices higher.

Seasonality plays a part, too. Winter is historically the weakest period of the year for West Texas Intermediate (U.S. crude) oil prices. But oil tends to pick up steam during the spring and top out during the summer.

Other wild cards include an eventual emergence by China from its strict COVID-19 containment measures, which is expected to spur additional demand (and thus higher prices), as well as future policy decisions by both the Federal Reserve and OPEC+.

Again, I don’t expect a perfect line here—all these factors aren’t going to synchronize seamlessly and produce a clear “Eureka!” moment for oil investors. But one by one, I expect them to start pushing the rock back up the hill.

Back to Our Big Dividend Plays

Pioneer Natural Resources (PXD, 11.0% yield): Pioneer, which started this fixed-and-variable policy in August 2021, has a base dividend of $1.10 per share quarterly, which comes out to an admittedly paltry 1.9% yield—not much better than the market. But there’s ample potential for more. PXD forecast a roughly 10% yield for 2022 based on $80/barrel oil. It also boasts a sterling balance sheet and enjoys extremely low production costs, so as long as oil doesn’t crash, investors can expect at least some sweetening on a regular basis.

And hey, if oil spikes on China reopening, not only could PXD’s dividend jump to 11% or higher—but the stock may also rally by an easy 11% or more as income investors rush to chase this yield.

Diamondback Energy (FANG, 6.1% yield): Texas-based Diamondback is another Permian Basin explorer, this one seeking out oil and natural gas in the Wolfcamp, Spraberry and Bone Spring formations. FANG has similarly low production costs and excellent cash margins. Its base dividend of 75 cents per share comes out to a roughly 2.1% yield and is protected all the way down to $35/barrel. FANG previously committed 50% of FCF to its dividend and stock buybacks, but expanded that to 75% in Q3 2022 and expects that figure to be larger than 75% at least in the near future.

Devon Energy (DVN, 8.2% yield): Devon Energy is an exploration and production company with oil-and-gas operations across five states, tapping formations including the Delaware Basin and Eagle Ford. Its fixed-and-variable payout starts with an 18-cent quarterly dividend—that grew 45% in 2022—that comes out to a 1.1% yield. But it can be augmented with up to 50% of DVN’s excess free cash flow from the quarter. One noteworthy development worth eyeballing came in Devon’s Q3 report, which revealed encouraging results from drilling tests in the Niobrara shale formation.

— Brett Owens

Give Me 4 Minutes, I’ll 4X Your Retirement Income [sponsor]

The fixed-and-variable model is a huge improvement over energy’s old keep-paying-until-we-hit-a-brick-wall model. And it can still deliver some massive yields—sometimes.

But when oil and gas prices ultimately cycle back into the “crash” phase, you might be looking at a few quarters, or even years, of 1%-2% yields.

They’re a great swing-trading proposition with a big dividend kicker. But retirement investors can’t be lured in by their high-tide yields.

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we need to be able to plan around our income with laser precision. Which is why we only hold dependable payers in our “Perfect Income” portfolio.

What makes these dividend holdings “perfect”?

They pay you consistently, predictably and reliably.

They’re built to survive—even thrive—in market crashes.

They deliver double-digit returns, with safe, secure investments.

They take just a few minutes every month to “manage.”

They DON’T involve day trading, buying on margin or any other risky strategy.

They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for every position in my “Perfect Income” portfolio.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Source: Contrarian Outlook