Within the Business Plan for our Income Builder Portfolio, it says:

This project is about presenting interesting investment candidates for further research, about discussing concepts and principles, and about demonstrating the process of building a reliable, growing income stream through DGI. In other words, we are not suggesting that fellow investors replicate the Income Builder Portfolio.

Well, our latest buy is one such interesting candidate — VICI Properties (VICI), a real estate investment trust whose featured holdings include iconic Las Vegas casinos such as the MGM Grand, Caesars Palace and the Venetian Resort.

VICI Properties

VICI is not without risk, and it might not fit every Dividend Growth Investing practitioner’s portfolio. But I find it to be an intriguing opportunity, and I decided to make it this month’s primary IBP buy.

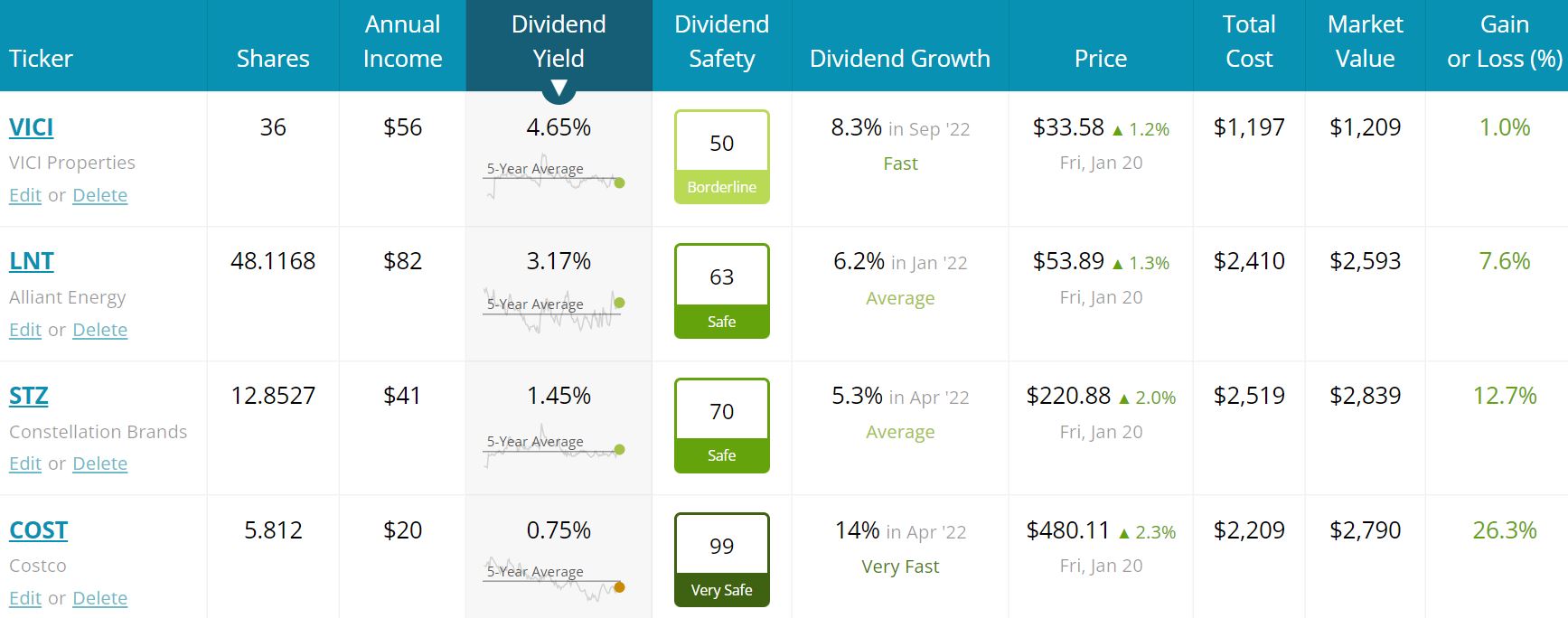

On Friday, Jan. 20, I executed a purchase order for 36 shares of VICI at $33.25 apiece on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

All buys were made using limit orders; the VICI purchase executed in two transactions a moment apart.

As you can see by the graphic above, I used the remainder of Greg’s $2,000 monthly allocation to add to the portfolio’s already existing positions in utility Alliant Energy (LNT), booze purveyor Constellation Brands (STZ) and warehouse retailer Costco (COST).

I’ll have a little more information about those three companies later, but this article is mostly about fast-growing VICI Properties, a self-professed “experiential REIT” with a 4.65% dividend yield.

What Is VICI?

Here is how the company describes itself:

VICI Properties Inc. is an S&P 500 experiential real estate investment trust that owns one of the largest portfolios of market-leading gaming, hospitality and entertainment destinations. … VICI Properties’ geographically diverse portfolio consists of 49 gaming facilities across the United States and Canada, comprising approximately 124 million square feet and featuring approximately 59,300 hotel rooms and more than 450 restaurants, bars, nightclubs and sportsbooks. … VICI Properties has a growing array of investing and financing partnerships with leading non-gaming experiential operators, including Great Wolf Resorts, Cabot, Canyon Ranch and Chelsea Piers. VICI Properties also owns four championship golf courses and 34 acres of undeveloped and underdeveloped land adjacent to the Las Vegas Strip. VICI Properties’ strategy is to create the highest quality and most productive experiential real estate portfolio.

Although the company’s jewels are its Las Vegas Strip properties, it also is well-represented in the Great Lakes region, the southern United States and the northeast.

VICI Properties

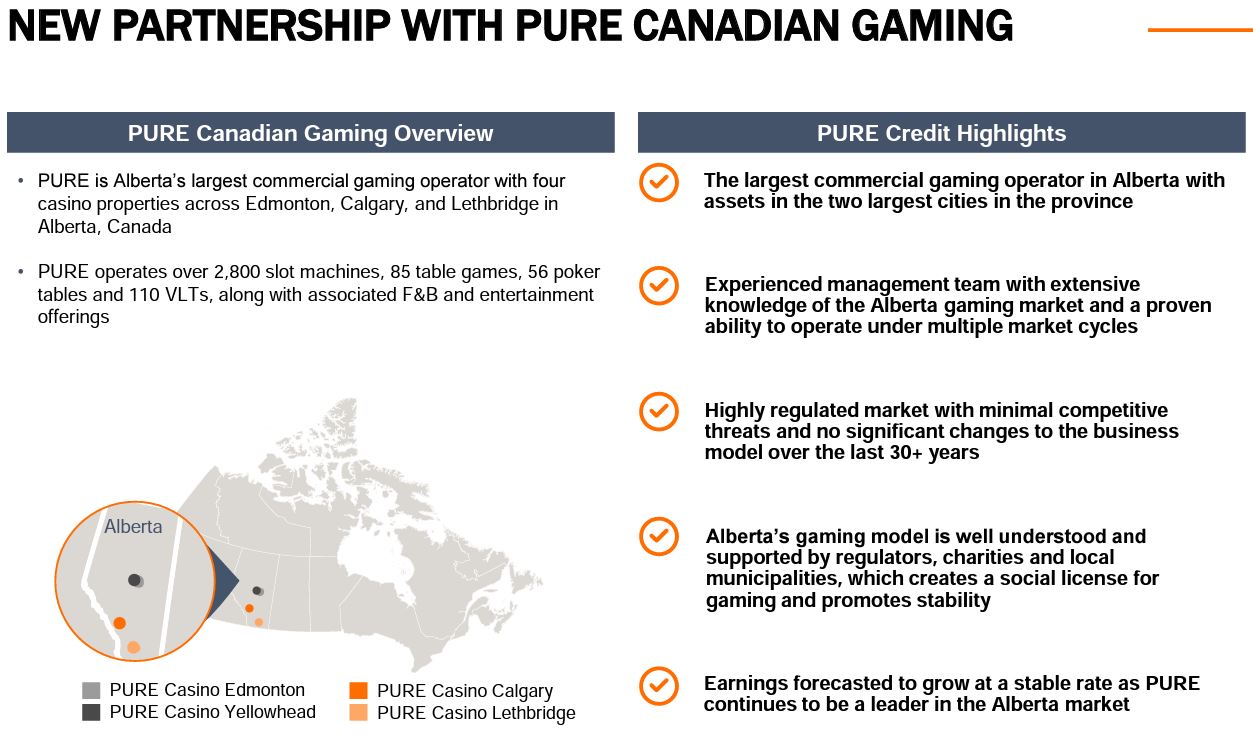

On Jan. 6, VICI made its first international move, acquiring four Canadian casinos for about $200 million USD. As part of the deal, it set up a triple-net lease with PURE Canadian Gaming that will bring back $16.1 million in the first year, a payment that will increase annually over the agreement’s 25-year term.

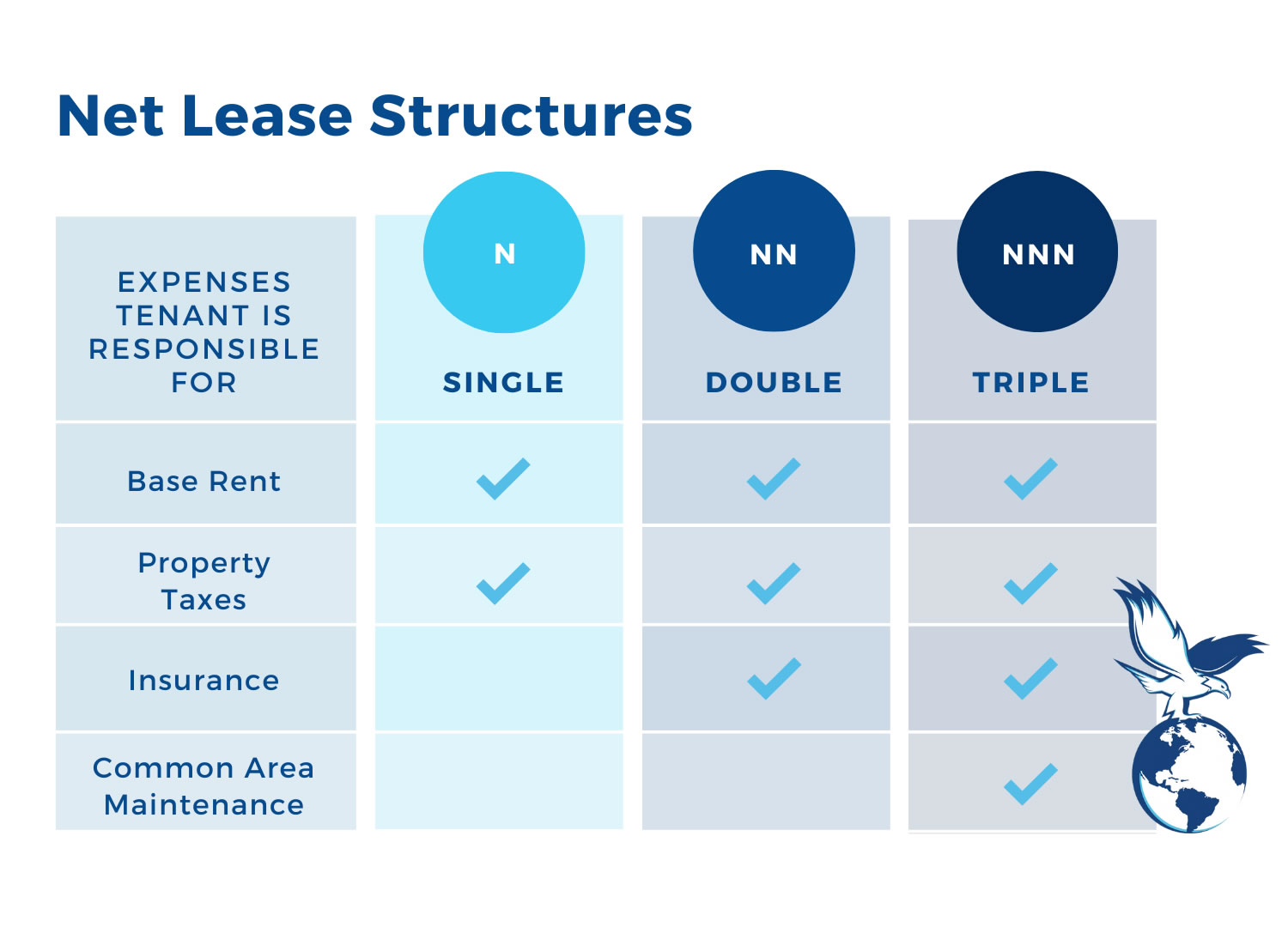

As seen in the right column of the graphic below, triple-net leases are highly beneficial to REITs because the tenants are responsible for property taxes, insurance and maintenance.

Excelsior Capital

So VICI gets to rake in rents from all of its properties without having to deal with day-to-day operations and costs.

The following two slides help explain the company’s reasoning behind the acquisition of the Canadian properties:

VICI Properties

VICI Properties

Viva Las Vegas (And Beyond)

I already mentioned three well-known casinos that VICI Properties operates in Las Vegas, but there are many more, most of which fall under the umbrella of the Caesars and MGM Grand brands.

These include familiar names like the Mirage, New York-New York, Mandalay Bay, Luxor, Harrah’s and Excalibur.

VICI Properties

Some analysts believe that one of the risks VICI faces is its outsized presence in one market. If Las Vegas suffers an economic downturn and/or if a prolonged global financial malaise curtails travel to Las Vegas, it could hurt VICI’s properties.

Two thoughts on that:

- Vegas is unique. Sure, bad economic times could adversely affect the casino industry there short-term, but it’s such a popular destination even for non-gamblers that I have trouble believing any downturn would be long-lived. Even now, after dozens of states have legalized gambling to end Las Vegas’ near-monopoly on the industry, visitors still flock to the Nevada desert. As Telly “Kojak” Savalas once said in a TV commercial: It’s Vegas, baby!

- Triple-net leases help protect VICI from all kinds of storm clouds. Yes, casinos have gone belly-up, but it’s very rare. And casinos have to pay their rent; I mean, it’s not as if Mandalay Bay can just decide to move elsewhere. During the early days of the COVID-19 pandemic, when theaters and other entertainment establishments stopped paying their bills, Vegas casinos continued to meet their obligations even though they were forced to close for months.

The last couple of years, VICI has been diversifying by location. In addition to Nevada, it now has casino resorts in New Jersey, Ohio, Indiana, Tennessee, Iowa, Mississippi, Louisiana, Missouri, Pennsylvania, Michigan, Maryland, Massachusetts, West Virginia and Illinois.

Additionally, the company has moved into family-friendly, non-gaming properties such as Great Wolf Resorts. It also now operates four golf courses — two in Nevada, and one each in Mississippi and Indiana.

Grand Bear Golf Club in Saucier, Miss.; photo from VICI Properties

While business diversification would seem to be a positive, there are observers who believe VICI should “stay in its lane” with casinos rather than branching out into golf and other industries. For what it’s worth, I don’t share that concern. VICI has experienced management and its people thoroughly research all expansion options.

VICI’s growth has been significant since it began operations only about 5 years ago. It already is among the leading publicly traded REITs in assets, revenue and market cap.

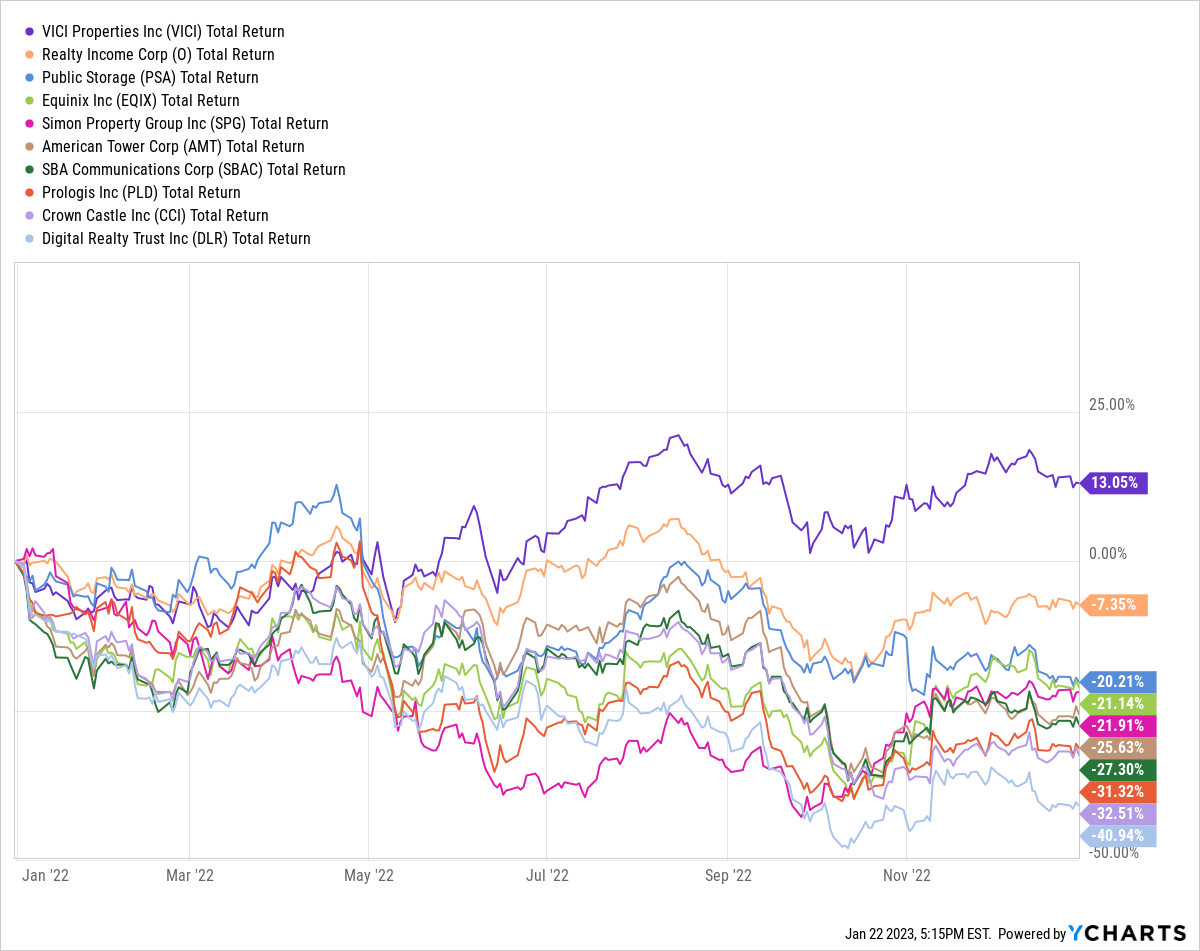

As an investment, it’s also been the best performer among large REITs over the last several years. Notably, while 2022 was brutal for the sector, VICI did very well for its shareholders.

VICI’s growth has been impressive, but it’s always more difficult for a larger company to continue to bulk up by double-digit percentages. That’s just common sense: When VICI only owned 10 properties and added 2 more of similar size, it instantly grew 20%. Now that it owns 49 properties, adding 2 more would be just a 4% increase.

VICI also has competition in its main realm, as other REITs are getting in on the gaming action. For example, Realty Income (O) — an established triple-net name that resides in many DGI portfolios (including the IBP) — recently made an auspicious entrance into the casino industry. Last month, it completed its $1.7 billion acquisition and lease-back of a Wynn Resorts property in Boston.

Still, there are so many untapped regions, especially outside North America. Casinos are popular in dozens and dozens of major international markets, and many will come available over the next several years.

Asked during the October earnings call about possibilities in foreign markets, John Payne, VICI’s chief operating officer, said:

We’ve grown, obviously, domestically in our first 5 years, but we always have positioned the company to grow internationally. And we’re spending time not only in the casino sector but also in the experiential sector outside the U.S. and studying markets where we think we would like to own real estate. And we’re in the middle of that process and understanding the underwriting and understanding the countries where we would own real estate and their laws and we’re right in the middle of it. Nothing to announce at this time, but it’s of interest for us to grow internationally.

Investors should like seeing VICI aspire to grow internationally, and they also should appreciate its measured approach.

Last year, VICI earned inclusion in the S&P 500 Index for the first time.

Also in 2022, Standard and Poor’s upgraded VICI’s credit rating to BBB- (low investment grade) after the company completed its deal for MGM Growth Properties, saying: “We believe the acquisition improves VICI’s scale and tenant diversity such that it can support a greater level of leverage at a higher rating. Additionally, VICI repaid the secured debt in its capital structure and unencumbered its asset base, which has led its capital structure to become more comparable with those of higher-rated REITs.”

Dividend Growth, Too

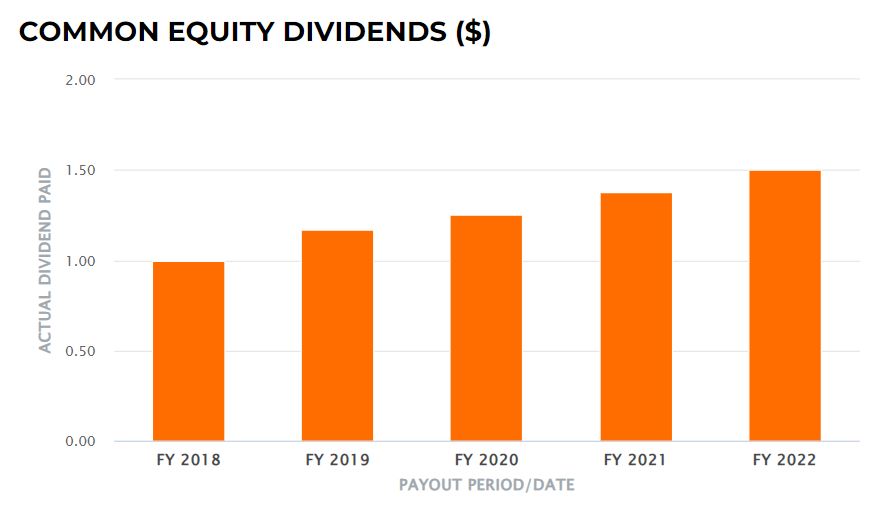

Since paying its first dividend in April 2018, VICI has increased the distribution substantially.

VICI Properties

Its most recent dividend hike was 8.3%, robust for a REIT. The company’s adjusted funds from operations (AFFO) payout ratio of 76% is not terribly high, suggesting plenty of room for more increases in future years.

Our 36-share purchase added $56 in projected annual income to the IBP. Throw in the Alliant, Constellation Brands and Costco buys, and the January stock acquisitions boosted our expected annual income by about $72.

Combined, the four companies are projected to pay about $200 in dividends into the Income Builder Portfolio in 2023 — though that figure is sure to grow as dividends are reinvested and as VICI, LNT, STZ and COST declare increases to their payouts.

Many observers believe that Costco, which has been executing at a high level and just announced a $4 billion buyback plan, will pay a large special dividend in 2023 (as it did in ’15, ’17 and ’20).

schwab.com

Meanwhile, Alliant could declare its next increase any time now; it traditionally does so in mid- to late-January.

As a relatively new company, VICI receives a “dividend safety” score of 50 — or borderline safe — from Simply Safe Dividends. I believe the folks there would like to see more of a dividend history and a little less debt for VICI before upping the grade.

The following graphic includes various income-related information about the IBP’s four January purchases, as well as their total-return histories since they’ve been part of the portfolio.

SimplySafeDividends.com

January’s buys pushed the IBP’s overall projected income stream past the $4,500 mark, meaning we are more than 90% of the way toward our $5,000 target.

Valuation Station

Analysts generally are bullish on VICI. Of the 20 monitored by Refinitiv, 18 call the stock either a Strong Buy or Buy.

Refinitiv, via fidelity.com

They have a mean 12-month price target of $37.90, representing a 14% gain from the price we paid for the IBP’s initial stake.

The analytical service Value Line sees 15% potential upside over the next 18 months (yellow highlight in following graphic) and a possible doubling of the stock price over the next 3-5 years (red circle).

valueline.com

Projected AFFO per share for 2023 is expected to rise from $1.85 to $2.06 … though macro issues such as interest rates, inflation and political brinksmanship could play a major role in what the actual performance will be.

Using that $2.06 figure, we just paid about 16x forward AFFO for the IBP’s new position, which is right around the norm for VICI.

As for the other January buys …

With its 32 forward P/E, Costco looks pricey (as always), but Morningstar says the stock is trading almost exactly at its fair valuation. Meanwhile, Morningstar says Constellation Brands and Alliant are somewhat undervalued.

Wrapping Things Up

Stocks have always been a bit of a gamble — so of course that’s true when investing in a company that deals with casinos.

phillymag.com

Seven years ago, VICI Properties didn’t even exist; it’s now one of the largest REITs out there. That kind of meteoric growth can make some investors a little nervous.

I’m intrigued enough about the company’s potential to have selected it for the Income Builder Portfolio and also to have bought a starter position for myself.

Nevertheless, I strongly urge investors to conduct their own thorough due diligence before buying VICI or any stock.

— Mike Nadel

This stock checks all the boxes. Pays a high dividend (8%), has a record of increasing that yield (an average of 37.5% throughout company history), and is set up perfectly to profit from continued Fed rate hikes. Click here for the name and ticker of the most perfect dividend stock on the market right now.

Source: Dividends & Income