Shall we turn 2023 into a bounce back year for our retirement portfolios?

How about we shoot for, say, 23% total returns?

The surest way to do it is by employing a technique I call the dividend magnet. It’s safe. Reliable. And works beautifully on the back side of a bear market.

A few weeks back I gave a guest lecture for a finance class at California State University, Sacramento. One of the students, to put it lightly, was excited to make money in stocks.

His hand went up from the back of the classroom. (Nobody sits in the front rows. Some things never change!)

I pointed, he responded: “So I read that stocks with big dividends aren’t necessarily the best to buy. And that we should focus on, well, the medium yields.”

“Yes!” I yelled. Nearly pumping my fist. “Jon, flip the deck forward,” I instructed my friend, the actual professor of the class, to flip my slides.

“Look, big dividends are great if you are retired. Or close to being retired. Because you can live off of the income and not have to sell any stock.

“But you all are far from retirement. I mean, you haven’t even started working yet. You have enough time to make a lot of money. So that you can retire early—and then collect dividend income on your giant cash pile.

“Seriously, how much longer are you all going to be here?” I waved my arms maniacally at the surrounding campus. “A couple more years? More? Maybe you can make enough money using this strategy that you never have to work.”

Blank stares from the class. Even from my new pal in the audience. (As usual, I got carried away and “completely overdid it” as my wife likes to say.) But I was just getting started. Heck, I had 90 slides to share!

A flurry of them showed the dividend magnet at work—my safe “get rich quick” strategy. Here’s one:

Valero’s Dividend Magnet

This is blue-chip oil refiner Valero (VLO). Its share price, the purple line above, is volatile because it moves with energy prices.

This is blue-chip oil refiner Valero (VLO). Its share price, the purple line above, is volatile because it moves with energy prices.

Valero’s dividend, the orange line above, is much steadier. The company is a cash cow and most years, it raises its dividend.

You can see that its payout (orange) acts as a “magnet” for its price (purple). The stock price can wander for months—sometimes many months—at a time. But eventually, the magnet “pulls” it higher.

It’s no coincidence that over this decade, VLO’s price appreciated 504% while its dividend climbed 460%. The magnet pulled the stock price higher.

Now VLO yields 3.4%—a “medium” dividend in wise student terms. It rarely pays much more because its stock price is always climbing to “catch up” with its payout raises. Dividend investors see when Valero’s yield is higher than its average and they buy. The buying boosts the price, to the tune of 504% in 10 years!

Here’s another one we all know—soft drink and salty snack peddler PepsiCo (PEP). It’s the type of recession-resistant stock we’ll hear more about in 2023 as the economy slows.

PEP raises its payout every year, though not as quickly as VLO. As a result, its price doesn’t climb as fast. PEP’s magnet is slower.

Here’s a 5-year look at the sugar beverage maker. Its payout grew 43%—not bad, but hardly a breakneck speed. PEP’s price increased at a similar pace, by 49%. That’s a respectable 8% annualized, but not going to make us rich over time.

PEP’s Dividend Magnet: Slower Than VLO

PEP yields 2.5% as I write. Also not bad, but not enough for us to retire on its dividend. We would only buy PEP if we thought its price was going to pop, but today? Its dividend is just growing too slowly for that to happen.

PEP yields 2.5% as I write. Also not bad, but not enough for us to retire on its dividend. We would only buy PEP if we thought its price was going to pop, but today? Its dividend is just growing too slowly for that to happen.

To make real money—and live up to my “get rich soonish” insight—we want a dividend magnet that is moving fast. That means the likes of VLO, which leaves PEP in the dust. We want triple-digit returns, not double digit.

So, let’s turn to locksmith Allegion PLC (ALLE), a manufacturer likely to have a field day with a weaker dollar in 2023. (The greenback was incredibly strong for most of this year, with the Federal Reserve hiking rates faster than the rest of the developed world. When the Fed pauses next year, the buck will take a break. The dollar’s recent downward trend is a “sneak preview.”)

I wouldn’t have to lecture Allegion CEO John Stone about this, of course. John sees it—which is why he just bought 12,500 more shares (for cash, these aren’t options exercises) for his personal account!

John could have spent or invested his $1,305,625 differently. Why did he pick ALLE?

Insiders may sell for a variety of reasons but they buy for only one. The big boss is bullish on ALLE.

Last quarter, the company’s revenue dropped an ever-so-slight 0.8%. But currency headwinds totaled 12.8%. Which means ALLE’s sales would have risen 12% if the dollar had simply held steady.

This is why with the buck’s bull market finally bending, ALLE is setup for some currency tailwinds. Which is what John is probably betting $1.3 million on.

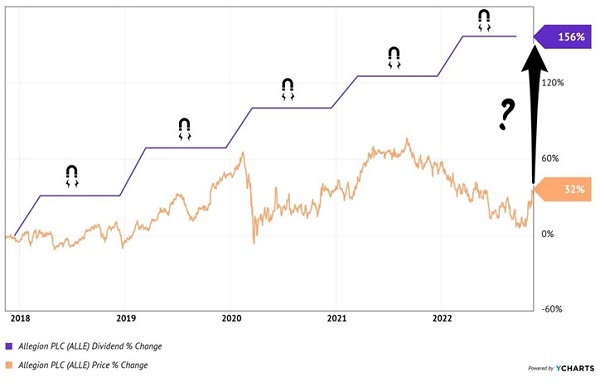

His stock sure is due. Allegion’s dividend has risen a fantastic 156% over the past five years, but its price is up only 32%. A weak dollar could very well trigger the dividend magnet and send ALLE higher:

ALLE’s Dividend Magnet is Due

Could ALLE return 23% in 2023? I’d bet on it, and certainly over PEP.

Could ALLE return 23% in 2023? I’d bet on it, and certainly over PEP.

— Brett Owens

Sponsored Link: Heck, it’s possible in 2023 that we’ll see returns of 61%, 112%, even 148% from my favorite dividend magnet candidates. It wouldn’t be the last time—these are actual numbers from recent winners in my Hidden Yields research service!

If total returns up to 148% are not a problem for your portfolio, then why not check out my current hot list of dividend magnet plays?

Source: Contrarian Outlook