Income investors can, in many ways, be even harsher critics than growth investors.

That’s because while some traders can delude themselves into believing the fancy growth stories of biotech or software startups … for “risk off” investors interested in dividends, the numbers matter.

And when a company isn’t measuring up, it shows.

There’s no greater proof of that than tools company Stanley Black & Decker (SWK). The stock has stumbled dramatically over the last year as supply chain pressures brought about the pandemic were compounded by rising raw material costs.

Thanks to weak margins and flat revenue, the stock is down a gut-wrenching 56% or so year-to-date.

But SWK may also soon illustrate the flip side of the numbers-based scrutiny that income investors are known for.

Because while growth investors often overlook deep flaws in sexy but financially unsound stocks, they also tend to overlook long-term dividend potential in boring and beaten-down names that aren’t in fashion.

In truth, a close look at SWK shows this may be a Dividend King about to turn things around.

Let me show you what I mean.

A Closer Look at SWK

The current troubles of Stanley Black & Decker are pretty simple. Bloated operations, overstocked inventories and a projection of a small revenue decline next year to boot. In any market those are bad things… but in 2022, when even decent stocks have struggled, it’s been very bad news for SWK.

That’s the bad news. But let’s get to the good stuff.

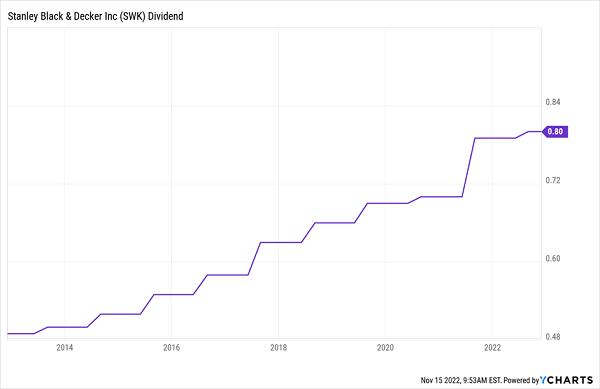

First, the payouts: the forecast for fiscal 2023 profits is $4.64 a share, which more than covers its expected $3.20 in dividends. That dividend is up slightly, too, with a one-cent bump in quarterly distributions as of September.

In short, the math shows the 3.8% dividend yield isn’t just sustainable but likely to edge higher – particularly as it is in the rarified group of “dividend kings” with more than 50 years of consecutive dividend increases.

In short, the math shows the 3.8% dividend yield isn’t just sustainable but likely to edge higher – particularly as it is in the rarified group of “dividend kings” with more than 50 years of consecutive dividend increases.

Secondly, the outlook. SWK’s management knows what’s going on and has taken steps to trim the fat from the business to the tune of $2 billion. For instance, earlier this year the company sold off its Commercial Electronics and Healthcare Security business lines for $3.2 billion to pay down debt and streamline operations. Unfortunately, the bulk of this long-term efficiency plan won’t be realized until 2025.

What’s more, the company is intentionally dragging out production because of its inventory backlog that needs to be bled down. That means even if it right-sizes the operation for efficiency, it has no intention of putting the pedal down anytime soon.

This adds up to a company that has stumbled, but certainly isn’t down for the count.

There’s a risk here, to be sure. If you’re interested in riding a recovering dividend stock, SWK has something to offer.

— Jeff Reeves

Think Like a Contrarian [sponsor]

As I write, the S&P 500 is up almost 12% since October 1, hinting that 2022 may close out on a positive note after what was otherwise a year most investors want to forget.

But is the bull market back? Or is this just another head fake, a bull market trap?

If you’re a long-term dividend investor like me, the answer to that question may not matter much. Because your portfolio should be built with years of income in mind, and uncorrelated returns that don’t march in lockstep with the major indexes.

Who cares if the S&P 500 is up or down over the last few days? What’s more important is total return, with the target date of retirement instead of the next weekend.

If you think like a contrarian, you can find durable returns that outperform the market. That involves thinking differently about stocks like Stanley Black & Decker, as well as a host of others.

To illustrate the opportunities out there, we’ve just updated our latest report on 7 top dividend growers to buy and hold forever.

These stocks have strong cash flows, a history of generous and reliable dividends and bargain valuations to ensure you’re getting a great stock at a great price.

Click here for risk-free access to these 7 “Bull or Bear” dividend payers, as well as tickers, current yields and much more!

Source: Contrarian Outlook