Back in August 2020, we paid $217.50 per share to buy a stock for our Income Builder Portfolio. Some 27 months later, it was trading at $214.75 … and we just bought it again.

Why would we invest more money in a company whose stock price has essentially gone nowhere for more than 2 years? Well, there are several reasons:

- It’s still a fine company with a good business model and a solid balance sheet.

- Interest rates eventually will head lower, as will inflation, and those favorable conditions will bode well for the firm’s future.

- The stock is attractively valued.

- The combination of its flat performance and 28 consecutive years of dividend raises has resulted in one of the highest yields the company has had in more than a decade.

The company I’m talking about is Essex Property Trust (ESS), a real estate investment trust that specializes in high-end apartments in top West Coast markets.

investors.essexapartmenthomes.com

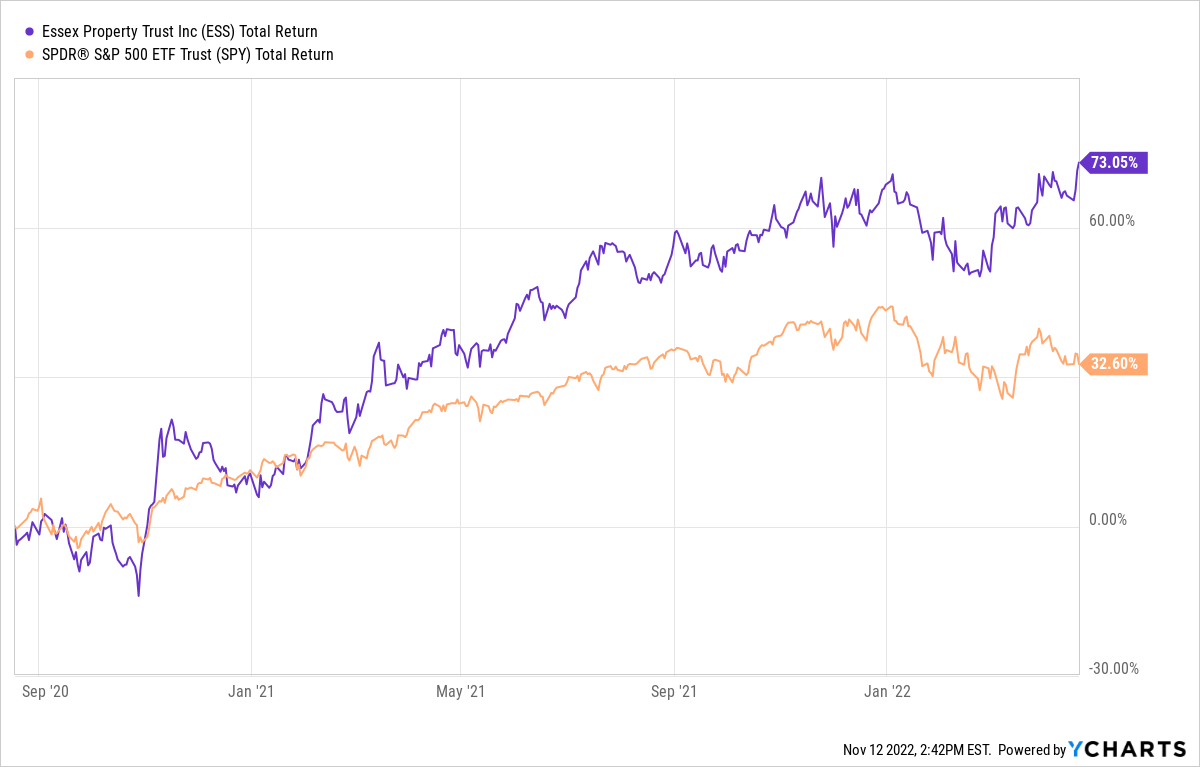

Despite the challenges presented by the COVID-19 pandemic, Essex more than doubled the total return of the S&P 500 Index from the time we first bought ESS through mid-April of this year.

Since April 22, however, ESS has fallen 39%. The chief culprit has been the Federal Reserve’s aggressive interest-rate increases in an attempt to battle surging inflation — which has had an adverse affect on most REITs, as well as plenty of other stocks in a variety of industries.

A little relief might be in sight, though. Last week, the October inflation numbers came in better than expected, and the market surged 5.5%. ESS surged right along with it.

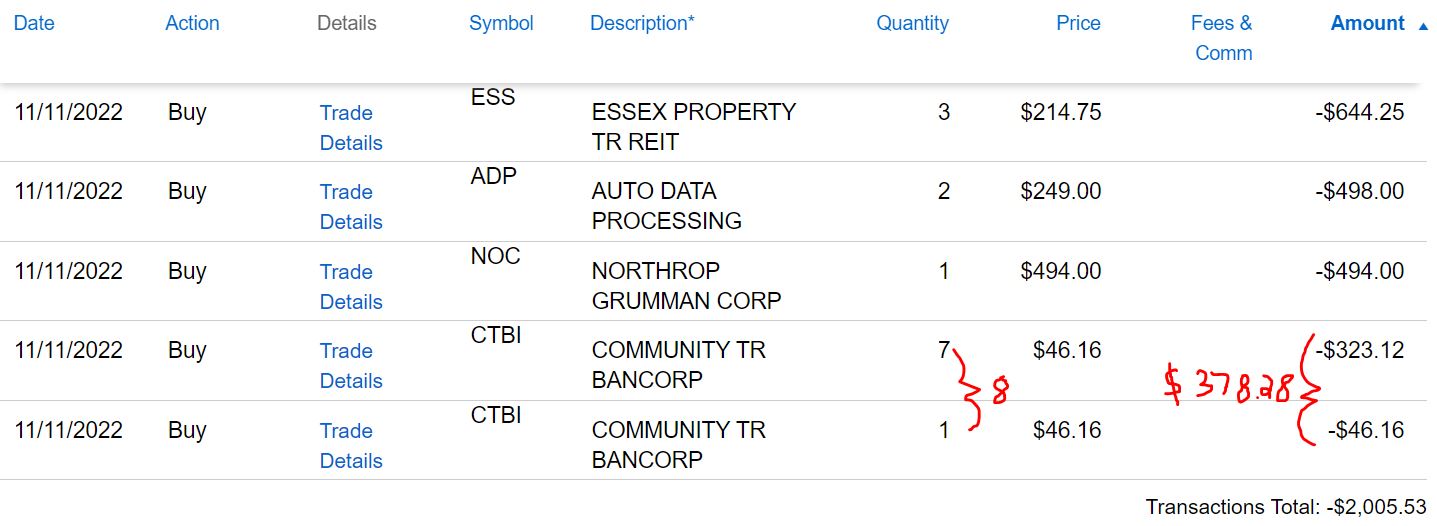

Even after that rally, ESS is priced 40% below its all-time high, and I thought it was a pretty good time to add to the Income Builder Portfolio’s position. So on Friday, Nov. 11, I executed an order to buy 3 additional shares on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

Limit orders were used for all buys. As can happen, the CTBI order executed in two transactions a moment apart.

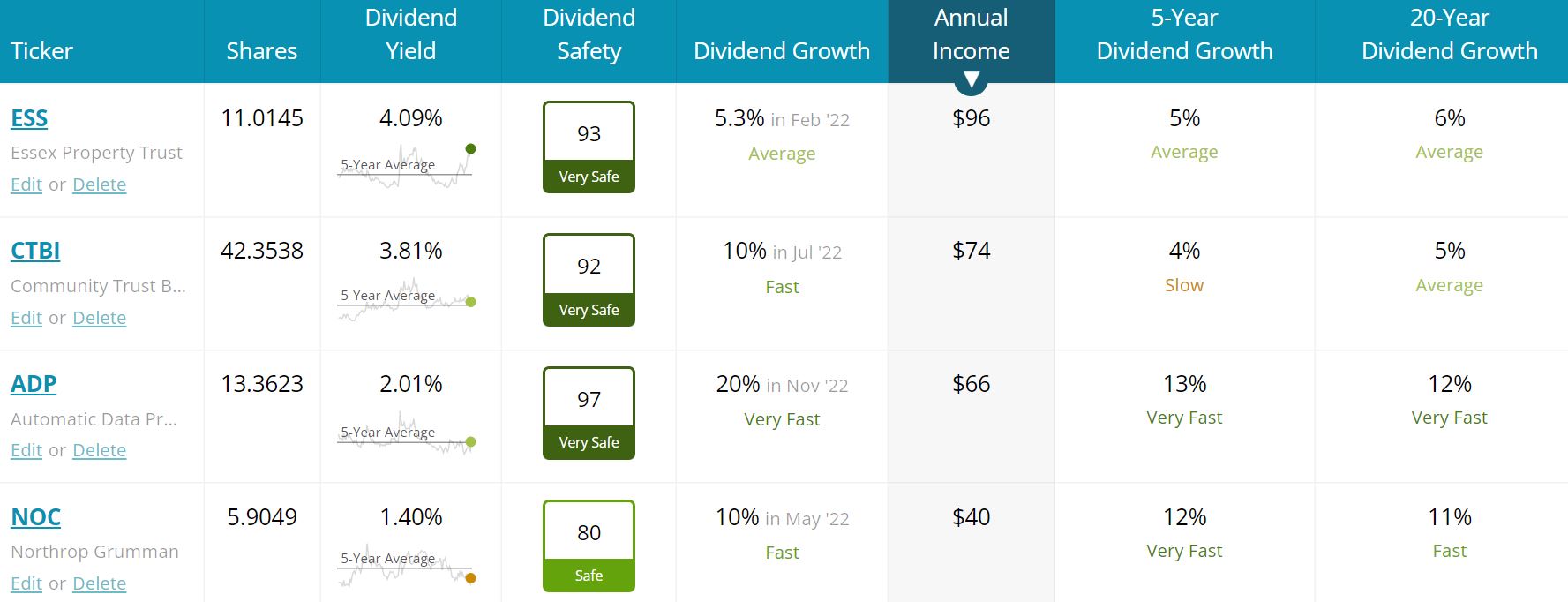

As you can see, I used the rest of Greg’s $2,000 monthly allocation to build on existing positions of cloud-based human capital management solutions company Automatic Data Processing (ADP), weapons maker Northrop Grumman (NOC) and small-cap Kentucky bank Community Trust Bancorp (CTBI).

ESS, ADP, NOC and CTBI were four of the IBP’s smaller positions, so I had been looking to increase their presence in the portfolio. I’ll have more on the latter three in a bit, but the focus of this article is on Essex Property.

Growth Returns

I explained why I wanted ESS for the Income Builder Portfolio on Aug. 18, 2020 (HERE), and the investment thesis remains the same today.

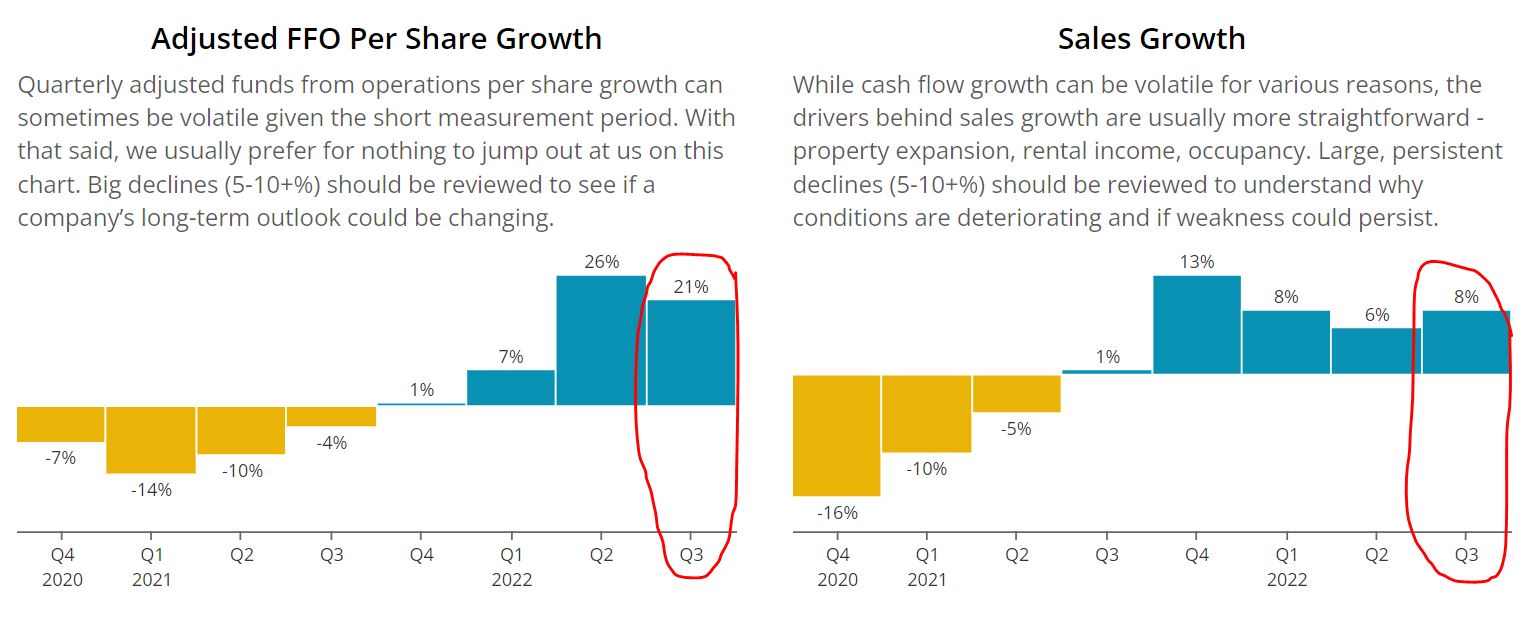

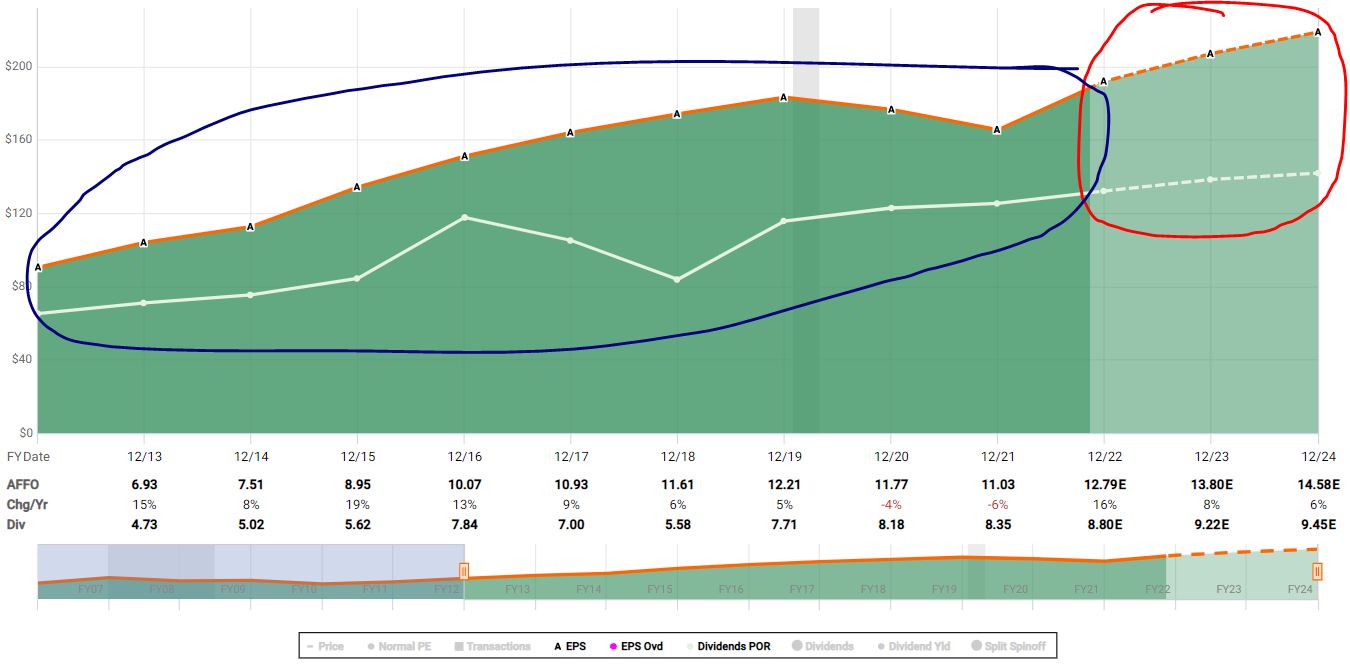

Essex endured difficulties in fiscal year 2021 due to the pandemic. But both adjusted funds from operations — AFFO is used instead of earnings to evaluate and compare REITs — and sales have resumed nice growth this year. (The following graphs are from Simply Safe Dividends.)

The company’s chief financial officer, Barb Pak, discussed the balance sheet during the Oct. 27 earnings call:

Our net debt-to-EBITDA ratio remains healthy at 5.8 times, and we expect this to further improve as EBITDA continues to grow. It should be noted that we operated around these same leverage levels before the pandemic, and our balance sheet metrics are strong. In addition, we are well-positioned from a capital-needs perspective. …

The company has no significant unfunded development needs and can fund the dividend, operations and capital expenditure needs from free cash flow. … With over $1.1 billion in liquidity, no funding needs for the next 18 months, and access to a variety of capital sources, the balance sheet remains well positioned.

Thanks to its solid financial standing, Essex has received an investment-grade BBB+ credit rating from Standard & Poor’s.

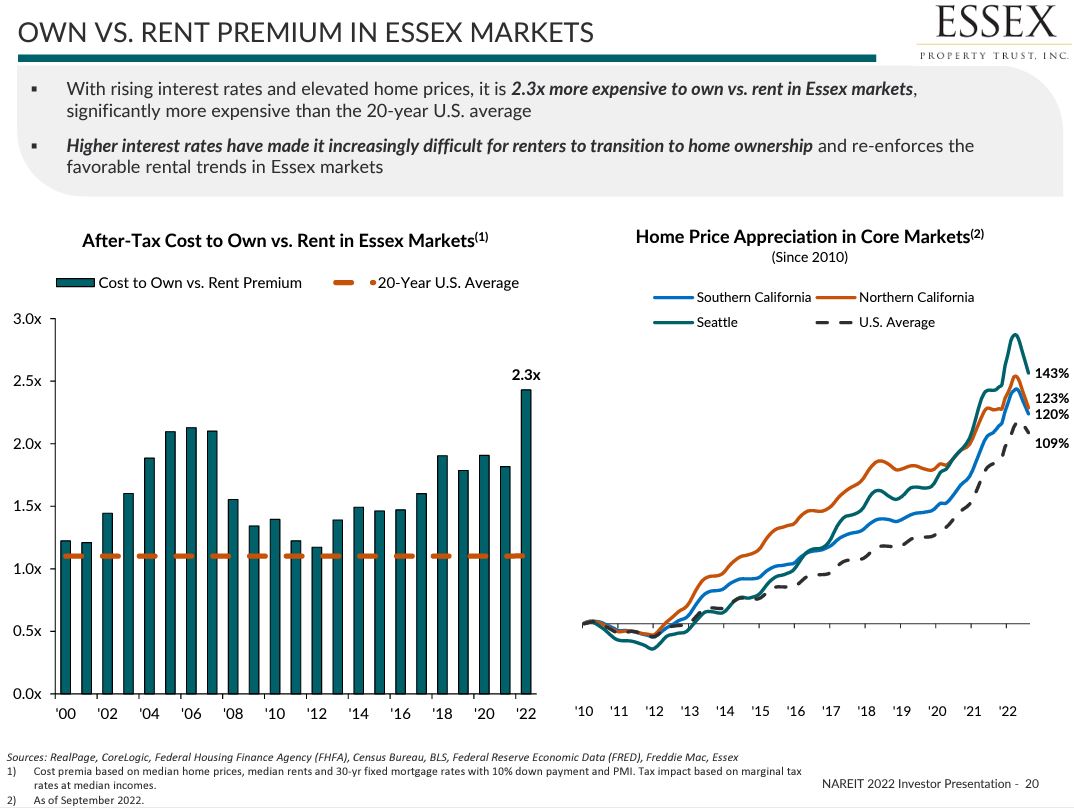

Essex benefits from operating in expensive communities where homeownership is out of reach for many residents. And the rising-rate environment has made it decidedly tougher for prospective homebuyers to qualify for mortgages.

investors.essexapartmenthomes.com

Princely Dividend

As a Dividend Growth Investing proponent, one thing the CFO mentioned especially made me smile: “The company has no significant unfunded development needs and can fund the dividend, operations and capital expenditure needs from free cash flow.”

As the following FAST Graphs image shows, Essex’s funds from operations have easily covered the dividends over the past decade (blue circled area) and are expected to continue doing so for years to come (red circle).

fastgraphs.com

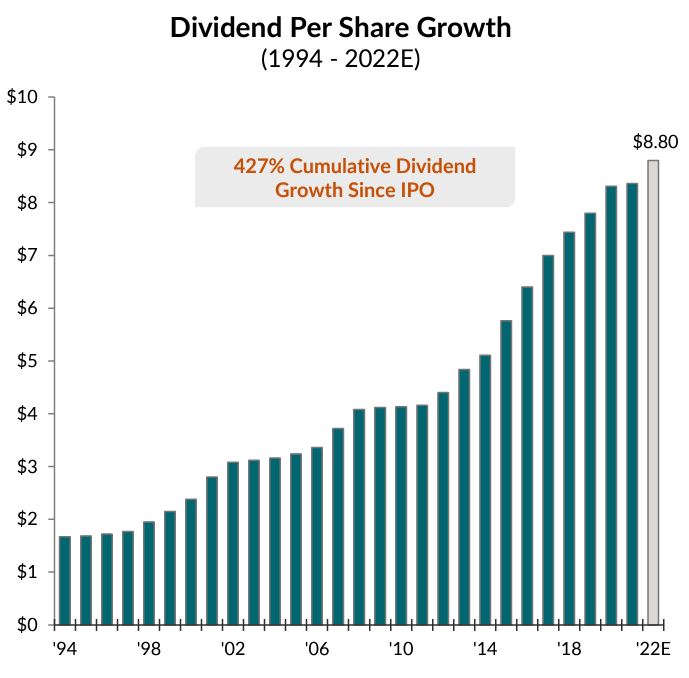

With 28 consecutive years of increases to its shareholder payout, ESS one of the few Dividend Aristocrats in the REIT sector.

investors.essexapartmenthomes.com

Emerging from the deepest depths of the pandemic in 2021, Essex raised its dividend by less than 1%. But ESS came back with a 5.3% hike for 2022, and I wouldn’t be surprised to see similar or higher next year.

Simply Safe Dividends also says shareholders can depend on the distribution being paid quarter after quarter; it gives Essex a “Very Safe” score of 93 on its 1-to-100 scale.

For that matter, three of the four companies we bought for the IBP in November have received “Very Safe” scores in the 90s. And the fourth (Northrop) gets an 80, putting its dividend at the very top of the “Safe” range.

The following graphic presents various dividend-related information about ESS, CTBI, ADP and NOC.

SimplySafeDividends.com

Friday’s buys added about $57 to the IBP’s projected annual income stream.

The full ESS, CTBI, ADP and NOC positions are expected to generate approximately $276 in dividends over the next year — about 6.5% of the portfolio’s almost $4,300 projected income stream.

Last week, Automatic Data announced a spectacular 20.2% dividend increase, its 48th consecutive annual raise. CTBI, which lifted its payout by 10% in July, also has a 40+ year streak going. And even though Northrop isn’t quite an Aristocrat yet, its 10.2% hike last spring marked its 19th straight increase.

Valuation Station

Of the four stocks we just bought, Essex is easily the most attractively valued — as indicated by all the green in the following table of fair values and analysts’ target prices.

*ESS is measured by Forward P/AFFO Ratio

There haven’t been many opportunities the last several years to buy ADP at a great price, and I’d understand if some investors consider it to be simply too expensive. The 20% dividend hike helped talk me into adding a little now to the IBP.

Northrop also looks frothy, as its recent slight pullback hasn’t sliced much off of the all-time high it set just a couple of weeks ago. But we hadn’t bought any NOC in a year, and our position was up big, so I thought we could add a share.

CTBI seems fairly appealing, with a forward P/E ratio of 10, but it is such a small bank that it’s not covered by most analytical firms. It’s the IBP’s newest position; my article about the selection is HERE.

That brings us back to Essex Property Trust’s valuation, which looks pretty darn appealing. For instance, 16 analysts tracked by Tip Ranks had an average $273.67 target price — suggesting a 27% upside over the next year.

tipranks.com

Similarly, the 22 analysts monitored by Refinitiv have a $270 mean target price.

Refinitiv, via fidelity.com

Perhaps you noticed in both the Refinitiv and Tip Ranks graphics that even the low target ($219) is higher than the stock’s current price.

Morningstar says ESS is trading at a huge discount to its $322 fair value.

morningstar.com

Value Line’s analysts believe the price for ESS could appreciate 35% over the next 18 months and could double over the next 3-5 years.

valueline.com

Simply Safe Dividends says that all the dividend-related information — especially the relatively high yield and the relatively low forward P/AFFO ratio — suggests undervaluation.

SimplySafeDividends.com

FAST Graphs also shows the stock trading at a historically low valuation. That’s indicated by the green-circled figures to the right of the image, as well as by how far the end of the black price line is sitting below the blue normal P/AFFO line.

fastgraphs.com

Furthermore, using analysts’ forward estimates and the company’s typical 5-year P/AFFO ratio, FAST Graphs shows that if ESS grows at what has been its normal pace, it would produce a nearly 26% annual rate of return through fiscal year 2024.

fastgraphs.com

Wrapping Things Up

In Essex, ADP and Northrop, we have three industry leaders, and CTBI has been a nice success story as The Little Bank That Could. All four are well-run companies and reliable dividend growers, and I’m comfortable having them as part of our Income Builder Portfolio.

To see data on all 49 positions, as well as links to every IBP-related article I’ve written, check out our home page HERE.

I also manage another real-money project for this site, the Growth & Income Portfolio. See the GIP home page HERE.

As always, investors are strongly encouraged to conduct their own due diligence before buying any stocks.

— Mike Nadel

Yes, right here and right now... in this brutal market. Where even the greatest financial minds of our time are having a hard time making a profit... It's a way you could amplify profits on stocks by as much as 7X - without using options, shorting, or any other gimmicks. I can show you the signal that is A mathematical antidote to fear - even when the market feels like its spinning out of control. Get Access to the #1 Tool that Pinpoints When to Buy a Stock, How Many Shares to Buy, and When to Sell It.

Source: Dividends & Income