When economic conditions are challenging — such as when inflation is high, interest rates are rising, and recession is a real possibility — I like to invest in companies with proven business models, rock-solid balance sheets, and plenty of cash on hand.

Oh, and if those companies grow their dividends year after year, I like ’em even more!

So today, I’m talking about Cisco Systems (CSCO) — the “old tech” networking giant, and one of the world’s great generators of free cash flow.

SimplySafeDividends.com

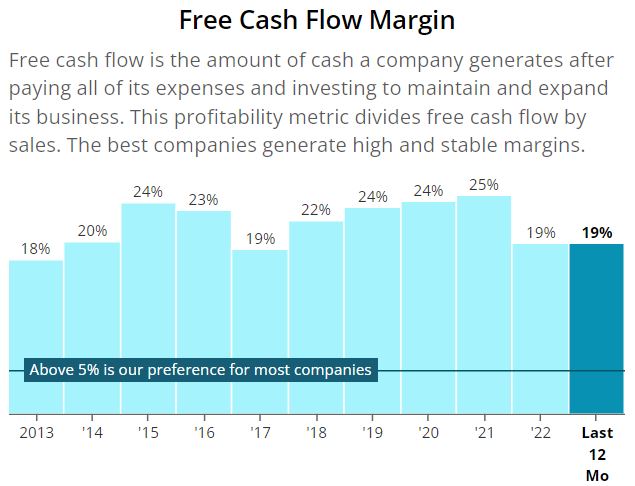

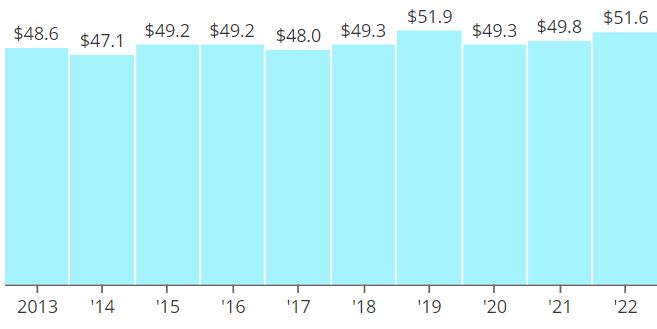

You can see by the above graphic that Simply Safe Dividends prefers companies with free cash flow margins of 5% or more (as do I). Businesses with margins of at least 10% are considered cash flow beasts.

Well, Cisco’s FCF margin for fiscal year 2022 (which wrapped up at the end of July) was 19% — and, relatively speaking, that was a “down” year for the company.

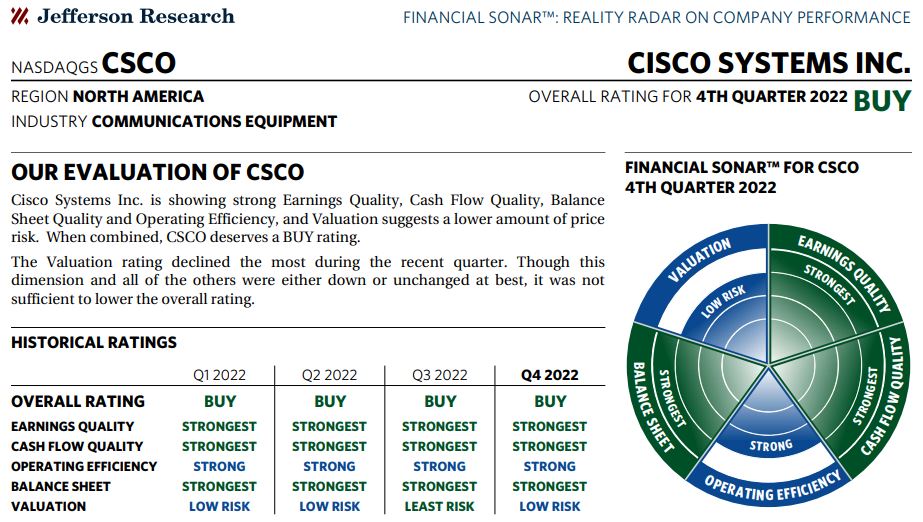

How strong financially is Cisco? The following graphic from Jefferson Research offers a reassuring illustration.

Jefferson Research, via fidelity.com

Given all of that information and considering what’s going on in the economy, I decided to add to the Income Builder Portfolio’s stake in Cisco Systems.

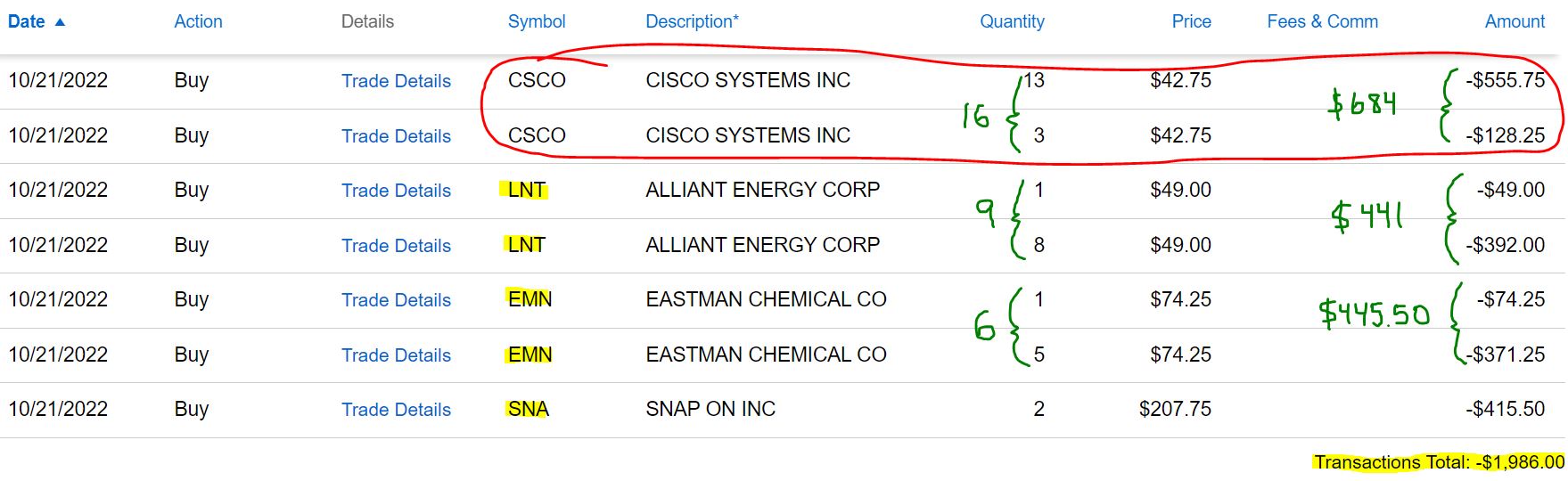

On Friday, Oct. 22, I executed an order to buy 16 shares of CSCO on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

As can happen with limit orders, those for CSCO, LNT and EMN filled in two separate transactions a moment apart.

I used the rest of Greg’s $2,000 monthly allocation to build on existing positions of utility Alliant Energy (LNT), materials company Eastman Chemical (EMN), and commercial tool-maker Snap-on (SNA).

We just initiated our Eastman position in September — read my investment thesis HERE. Alliant and Snap-on were 2021 additions to the portfolio; my write-ups on those companies are HERE and HERE.

I’ll discuss some dividend and valuation information regarding EMN, LNT and SNA in a little bit. But now let’s revisit Cisco Systems, which we first bought for the portfolio in 2019.

The analytical firm Argus offers a good, concise business summary for the company:

Cisco is a worldwide leader in communications equipment. Originally created to provide routers and switches for Ethernet-based networks within enterprises, the company has expanded into collaboration, data center, service provider video, security, wireless, analytics and other hardware and software niches.

Once one of the biggest innovators in Silicon Valley, Cisco does a lot of its growing now by being a serial acquirer — it keeps buying much smaller businesses.

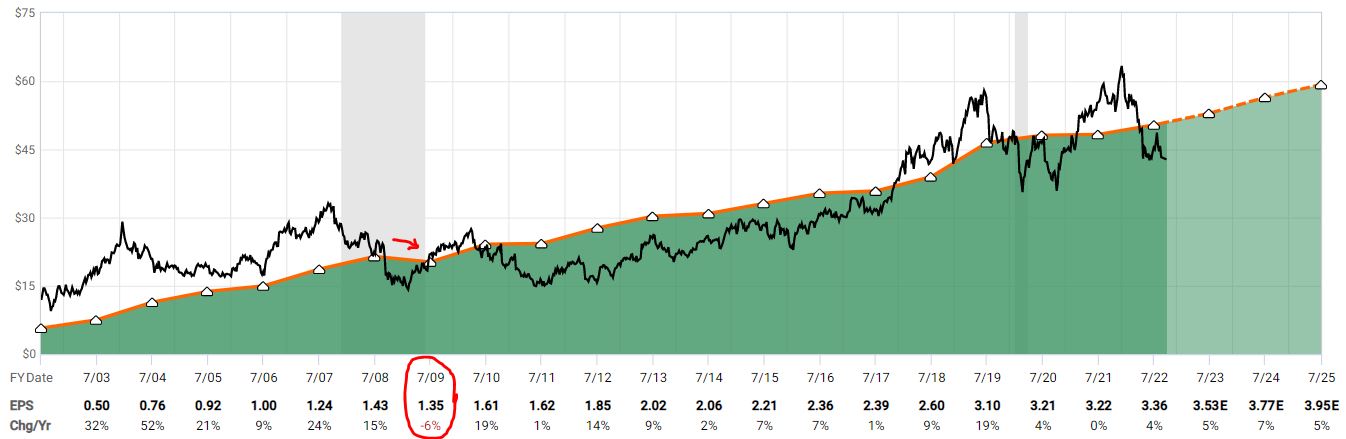

In addition to having incredible FCF, as I mentioned early in this article, Cisco has an impressive stretch of year-over-year earnings growth. Only once in the last 20 years, during the depths of the Great Recession, did the company experience a small decline in earnings per share.

fastgraphs.com

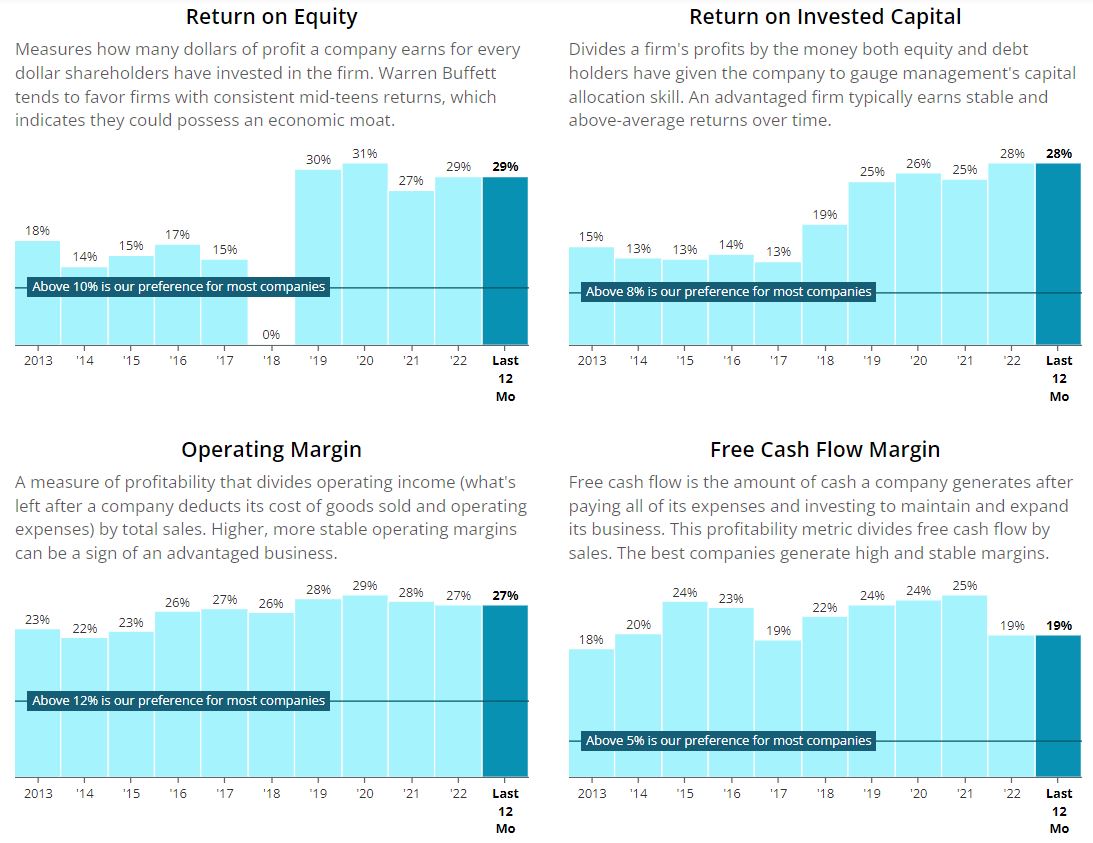

Cisco’s return on equity, return on invested capital and operating margin numbers also are outstanding.

SimplySafeDividends.com

One area of relative weakness for Cisco is that it no longer grows revenue as rapidly as it once did.

Still, 2022 produced the second-highest annual sales total in company history, just a shade below where they were in the last pre-pandemic year (2019).

SimplySafeDividends.com

As part of Cisco’s fourth-quarter earnings announcement in August, CFO Scott Herren said:

Total revenue exceeded our expectations in Q4, as a result of our strong execution and the numerous initiatives we have taken to reduce the impact of the global supply situation. Our operational discipline is reflected in our healthy operating margin and strong cash flow generation, enabling us to return nearly $4 billion to our shareholders in Q4. And we continue to make good progress in our business model transformation with (contractual obligations) of over $31 billion, which, coupled with our record backlog, provide us with substantial visibility and confidence in our future revenue.

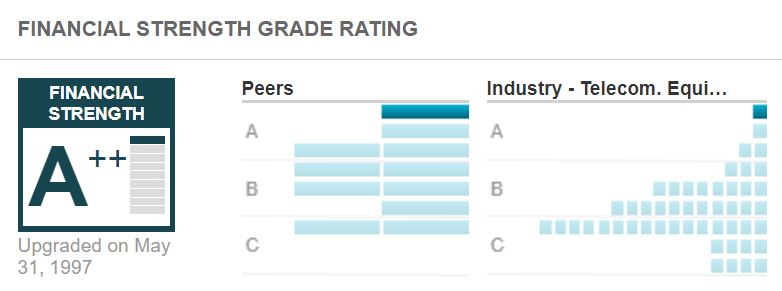

The analysts at Value Line certainly agree, giving the company its highest score for Financial Strength.

valueline.com

That’s just one of many quality-related metrics that sticks out for Cisco Systems. All four of the companies that we bought more of for the IBP in October are well-regarded, but CSCO is the standout across the board.

Dividend Doings

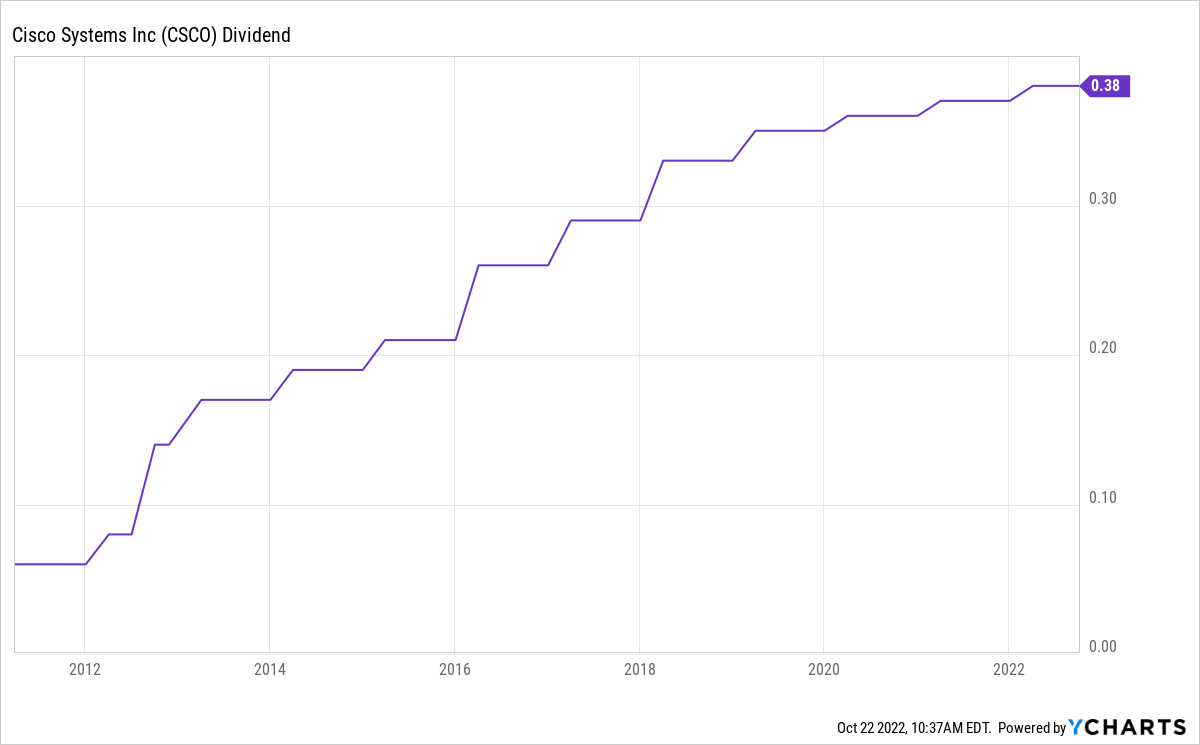

Cisco made its first dividend payment in 2011, and it aggressively grew the payout to shareholders for the next several years.

Dividend growth has slowed more recently, with each of Cisco’s last three annual raises being less than 3%.

The company instead has focused on buybacks, repurchasing $7.7 billion worth of shares during its 2022 fiscal year — part of an $18 billion buyback program authorized by Cisco’s board of directors in February.

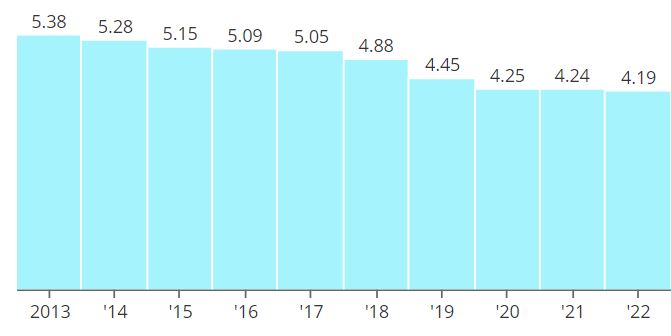

Stock buybacks are nothing new for Cisco. Over the last decade, the company has reduced shares outstanding from 5.38 billion in 2013 to 4.19 billion now — a 22% decrease.

SimplySafeDividends.com

Although I’m a Dividend Growth Investing proponent who generally prefers large dividend raises to buybacks, reducing share count is one way Cisco adds value for shareholders by giving them a higher percentage of ownership in the company.

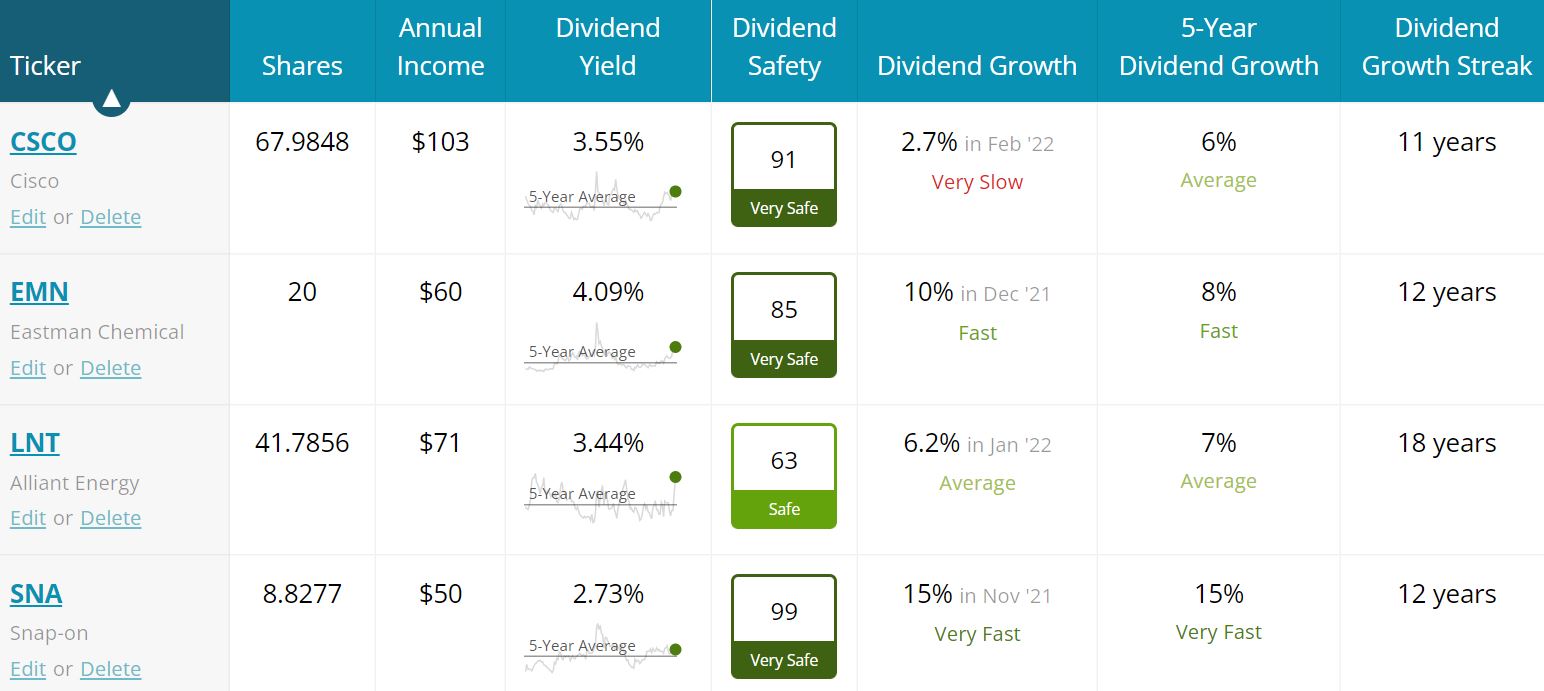

Here is some income-related information on all four of the companies we bought for the IBP in October:

SimplySafeDividends.com

Together, the four positions are projected to produce about $285 in income over the next year, 6.8% of the IBP’s approximately $4,200 total.

Valuation Station

The stock market is coming off one of its best weeks of the year, up about 5%, but the S&P 500 Index is still down 21% in 2022.

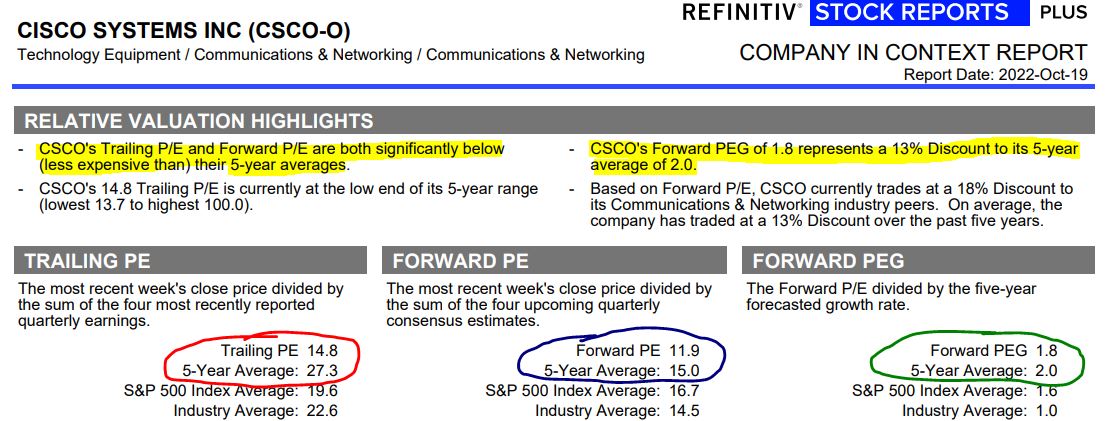

CSCO’s share price is down even more (32%). Given Cisco’s strength and potential, most analysts consider it to be attractively valued now — with a forward P/E ratio of around 12 and a sub-2 PEG ratio.

Refinitiv, via fidelity.com

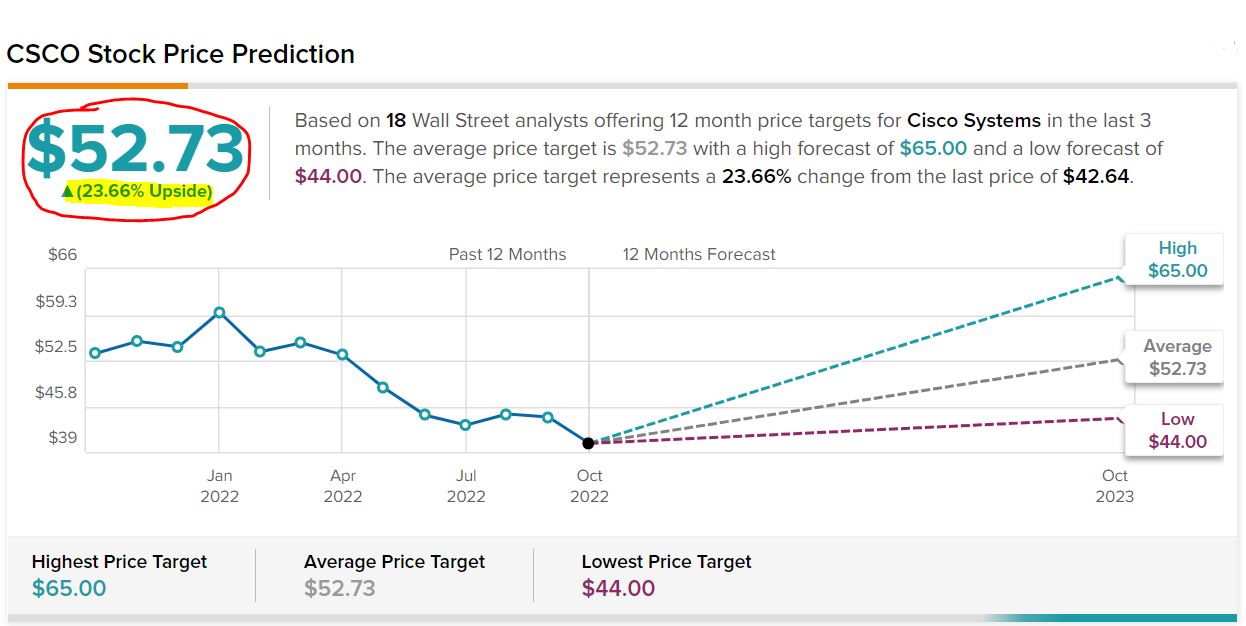

The 18 CSCO analysts monitored by TipRanks have an average 12-month price target of about $53, suggesting a 24% upside.

tipranks.com

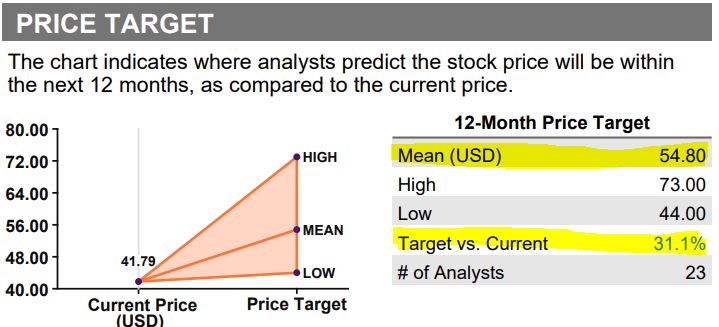

The 23 analysts monitored by Refinitiv combine to have an even higher target price — $55 — for a 31% upside.

Refinitiv, via fidelity.com

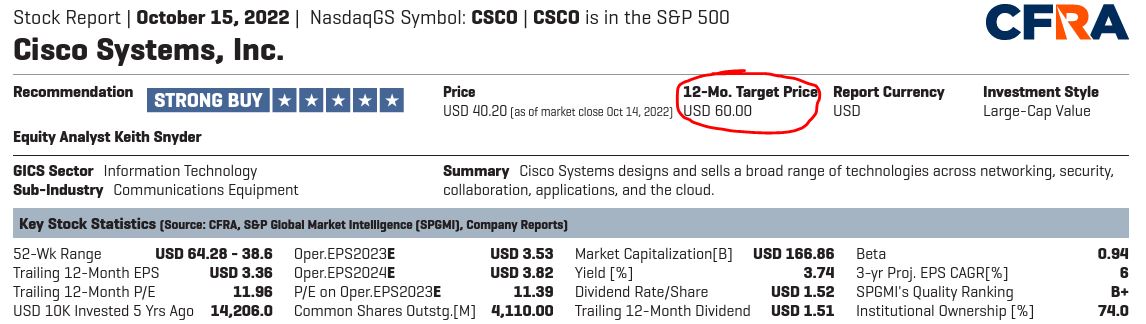

CFRA calls Cisco a “strong buy,” with a $60 target price.

CFRA, via schwab.com

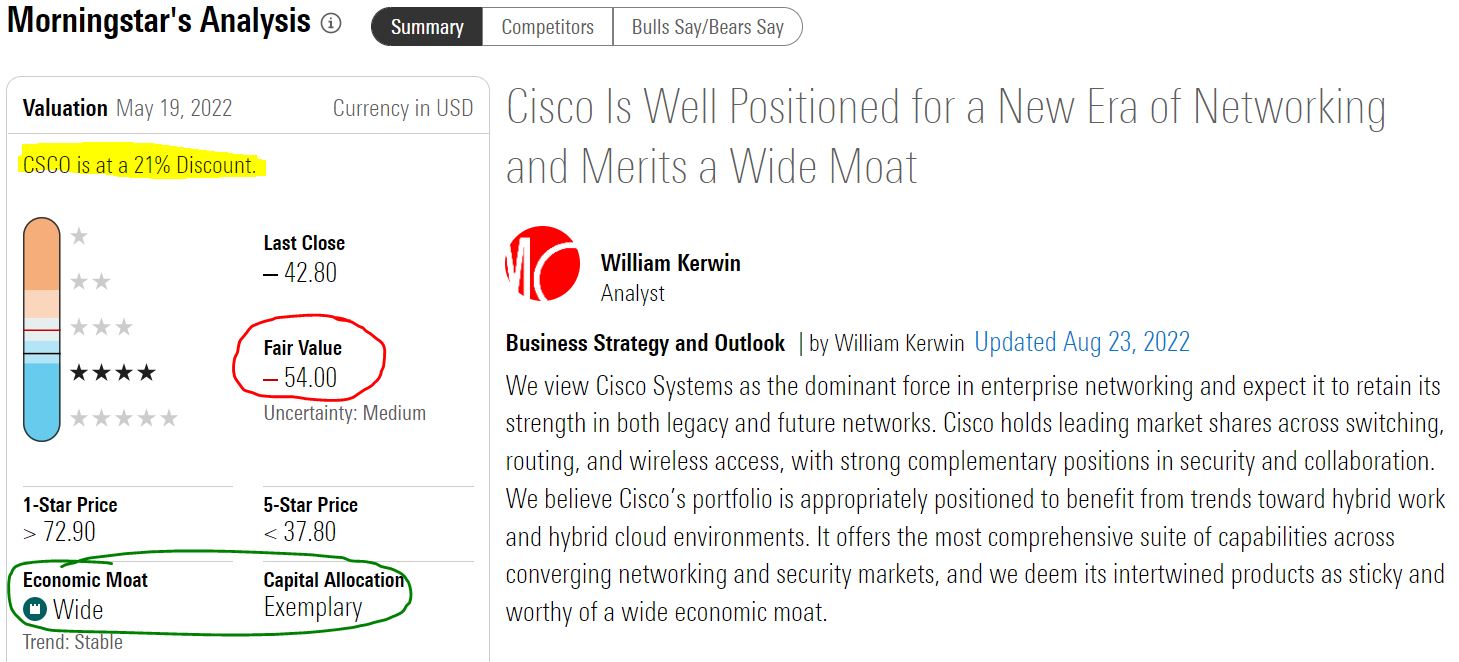

Morningstar appreciates Cisco’s wide moat, business model, financial strength and management — and its analysts believe the stock is quite undervalued.

morningstar.com

Value Line’s 18-month target price suggests 25% upside, and its longer-term outlook indicates possible price appreciation of more than 100%.

valueline.com

Value Line includes Cisco in its model portfolio of “Stocks with Above-Average Dividend Yields,” and also has the company on its list of “Low-Risk Stocks for Worthwhile Total Return.” Said Value Line analyst Kevin Downing:

Management has pointed out that there are now more technology transitions occurring concurrently than there have been in the past 20 years. These include hybrid cloud, hybrid work, security, IoT, 400-gig, 5G, and Wi-Fi 6. Costs ought to stay elevated near-term, but margin pressure should ease as the year progresses, and Cisco has proven its ability to adjust to difficult environments. … We think these shares offer compelling risk-adjusted, long-term, total-return potential at recent price levels.

Indeed, all four of the companies we bought for the Income Builder Portfolio in October look compelling at their current prices.

Here are various analytical firms’ fair values and target prices for Cisco, Eastman Chemical, Alliant and Snap-on:

Wrapping Things Up

During his company’s earnings call, Scott Perren, the Cisco CFO, had this to say:

Our strong balance sheet and overall financial position is clearly a competitive advantage in tough environments.

I totally concur, which helps explain why I thought it was time to add some more CSCO to the Income Builder Portfolio.

To see data on all 49 positions, as well as links to every IBP-related article I’ve written, check out our home page HERE.

I also manage another real-money project for this site, the Growth & Income Portfolio. See the GIP home page HERE.

As always, investors are urged to conduct their own due diligence before buying any stocks.

— Mike Nadel

This stock checks all the boxes. Pays a high dividend (8%), has a record of increasing that yield (an average of 37.5% throughout company history), and is set up perfectly to profit from continued Fed rate hikes. Click here for the name and ticker of the most perfect dividend stock on the market right now.

Source: Dividends & Income