Sometimes a stock that has been sitting on my watch list for a long time becomes such a compelling value that I finally have to buy it.

That was the case with Eastman Chemical (EMN).

I hadn’t invested much in the Materials sector, but I had kept an eye on Eastman, which manufactures fibers and plastics that are used in industrial and consumer products.

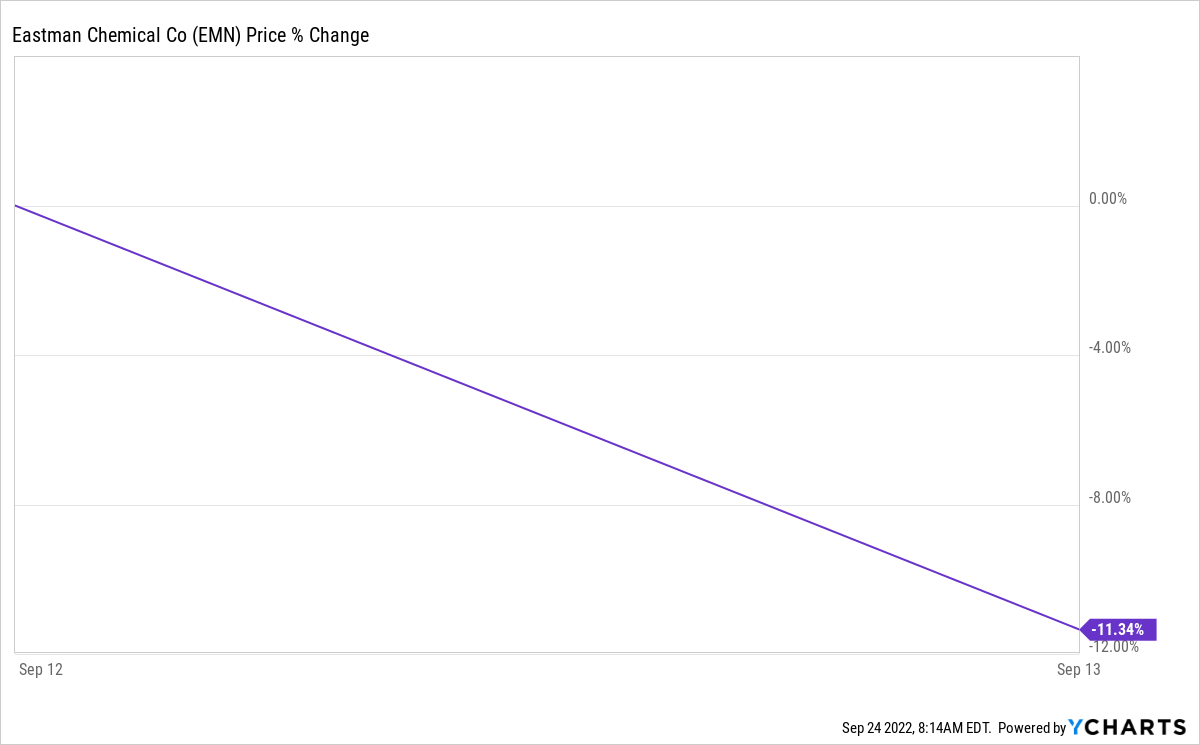

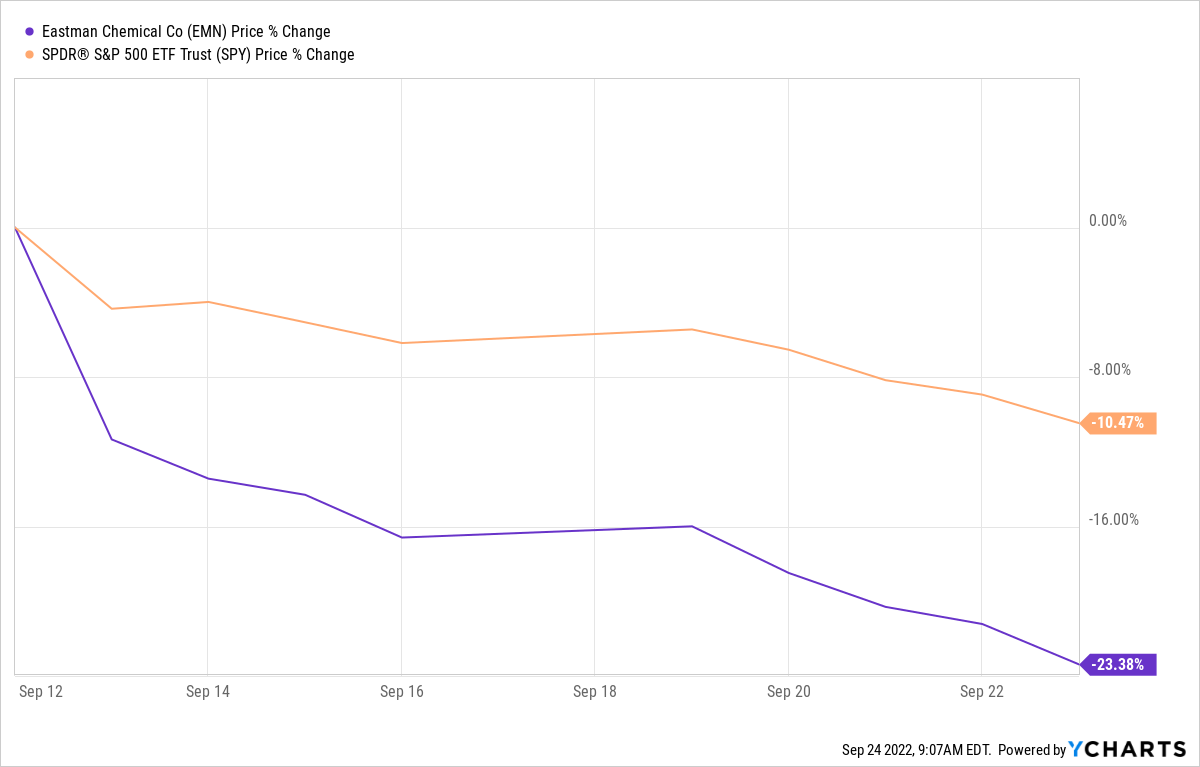

Whenever I checked, its stock price had always seemed a little on the pricey side … and then came Sept. 13.

Eastman management revealed that the company had adjusted its third-quarter outlook sharply downward — reducing expected earnings per share from $2.46 to $2.

As CFRA analyst David Holt said:

The company cited three drivers impacting volume and mix, including a slowdown in consumer durables and construction end markets. Concurrently, logistical constraints, especially on the U.S. East Coast, are resulting in higher costs. Lastly, an electricity outage in July took longer than expected to bring back online, resulting in lower polymer-related product sales.

That got my attention, as did this from Holt:

EMN plans to adjust pricing to help partly offset the unexpected costs – at this juncture, many setbacks seem isolated in nature, and priced into shares after today’s drop, especially with durable demand trends still intact across agriculture and personal care end markets. We trim our 12-month target to $110 (from 125), applying an EV multiple of 8.8x to our 2023 EBITDA estimate, a discount to peers.

In other words, Eastman’s longer-range outlook was still good — and, even after CFRA trimmed its target price, EMN was looking well undervalued.

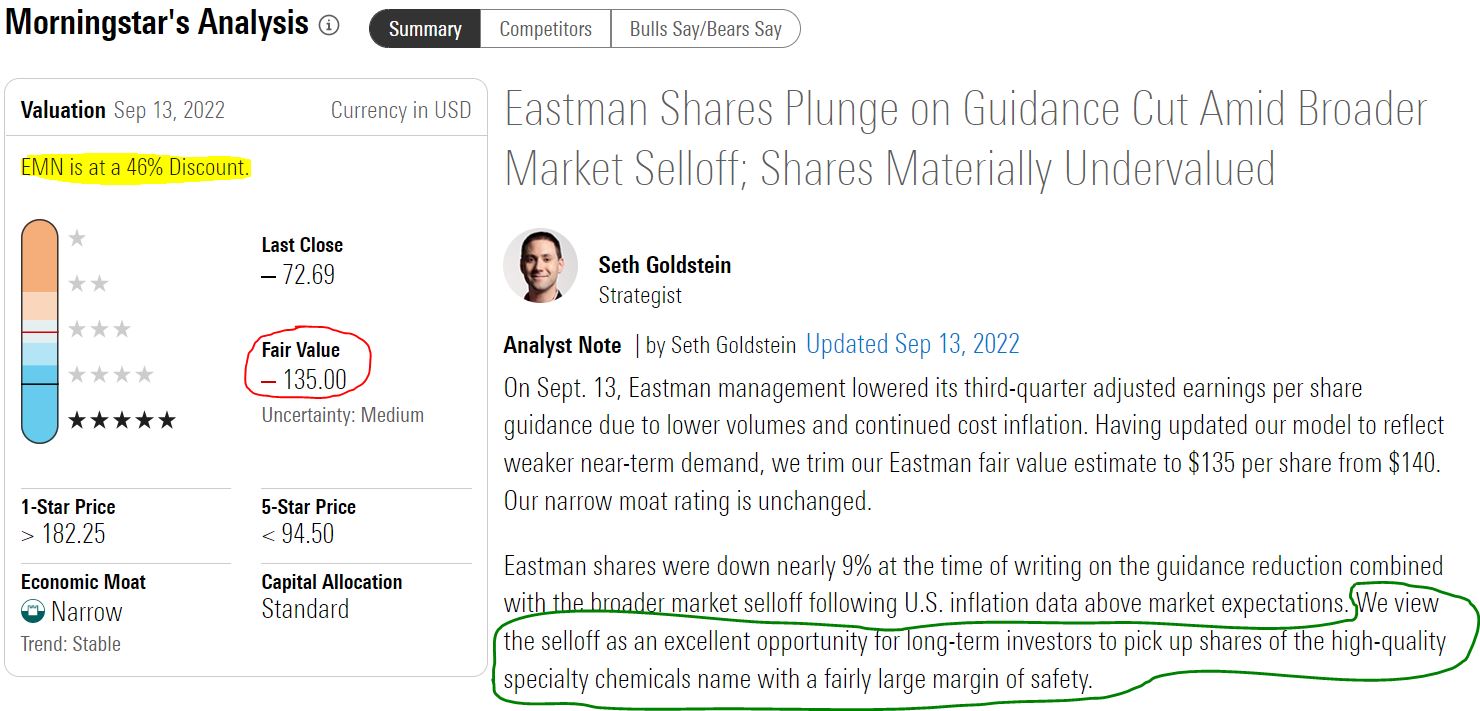

Morningstar analyst Seth Goldstein offered a similar assessment:

morningstar.com

Eastman’s price has continued to move down along with the overall stock market, and Morningstar now considers it a 5-star strong buy trading at a 46% discount to fair value.

Ultimately, I agreed with the sentence that I circled in green: “We view the selloff as an excellent opportunity for long-term investors to pick up shares of the high-quality specialty chemicals name with a fairly large margin of safety.”

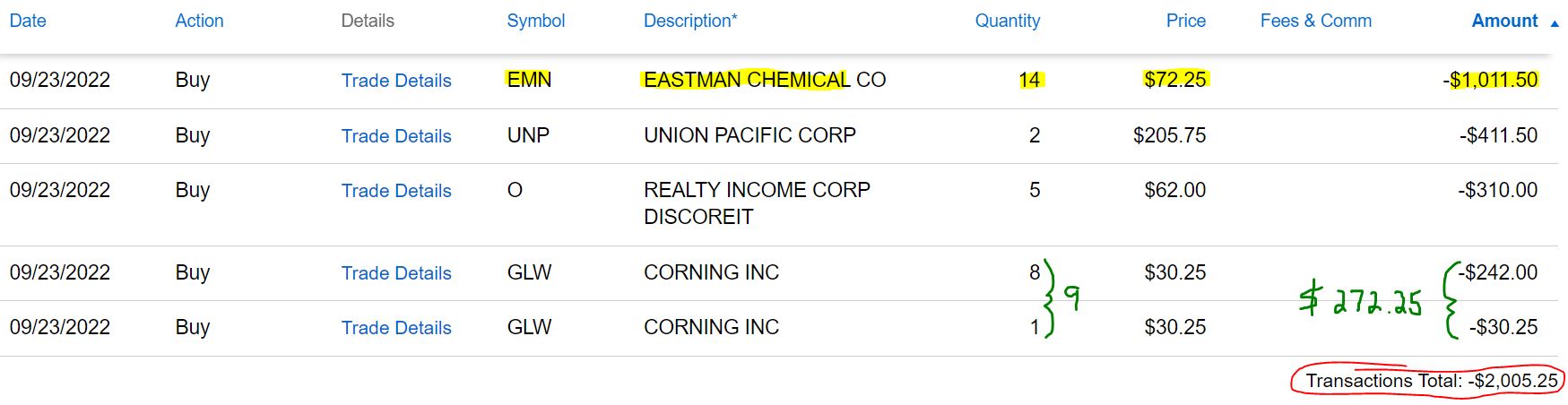

So on Friday, Sept. 23, I initiated a position in Eastman Chemical within my personal portfolio. I also decided to add it to our public, real-money Income Builder Portfolio, and I executed a purchase order for about $1,000 worth of EMN on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

Limit orders were used for all buys. As can happen, the GLW order executed in two transactions a moment apart.

As you can see, I used the remainder of Greg’s $2,000 monthly allocation to add to the IBP’s existing positions in three strong companies: railroad Union Pacific (UNP), real estate investment trust Realty Income (O), and display and optical technology firm Corning (GLW).

We initiated the Corning position just a few months ago; see my investing thesis HERE. Union Pacific was first added about a year ago; read about it HERE. Realty Income has been part of the portfolio since 2020, and I last wrote an in-depth article about it in November 2021 — HERE.

I’ll have some updated data on those three stocks in a bit, but most of this article will be focusing on our newcomer.

![]()

Here is how CFRA describes the Tennessee-based company’s business:

Eastman Chemical Company (EMN) is a global advanced materials and specialty additives company that produces a broad range of products found in various everyday items. EMN has 41 manufacturing facilities and equity interests in three manufacturing joint ventures in 12 countries that supply products to customers worldwide. In 2021, sales outside of the U.S. and Canada accounted for 56% of the company’s sales.

EMN operates in four segments: Additives & Functional Products, Advanced Materials, Chemical Intermediates, and Fibers.

The Additives and Functional Products segment (35% of 2021 sales) manufactures chemicals for products in various markets, including transportation, consumables, building and construction, animal nutrition, crop protection, energy, and personal and home care. Its products include solvents, hydrocarbon resins, cellulosics, and specialty polymers.

The Advanced Materials segment (29%) produces and markets its polymers, films, and plastics with differentiated performance properties for value-added end uses in transportation, consumables, building and construction, durable goods, and health and wellness markets.

Chemical Intermediates (27%) manufactures … products used in markets such as industrial chemicals and processing, building and construction, health and wellness, and agrochemicals. Technology platforms include acetyls, oxo, benzene and derivatives, polyester, and alkylamines.

In the Fibers segment (9%), EMN is one of the world’s two largest suppliers of acetate cigarette filter tow and the leader in acetate yarn for use in apparel, home furnishings, and industrial fabrics.

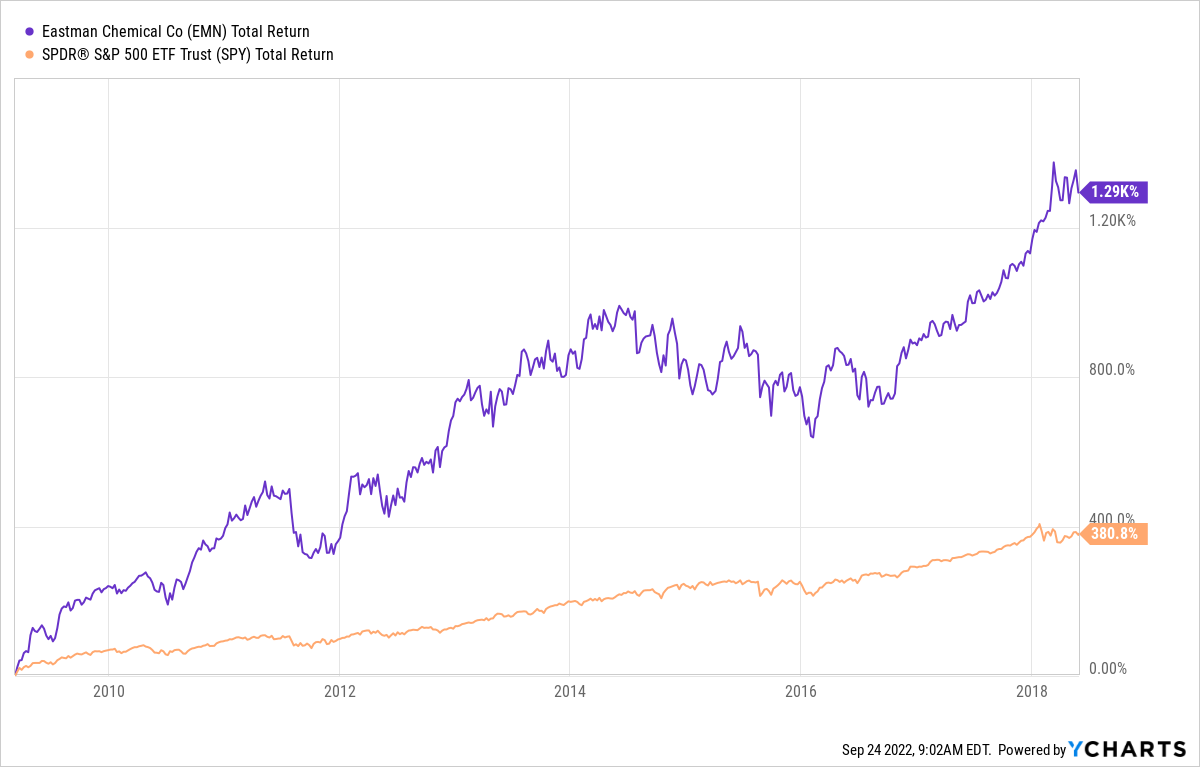

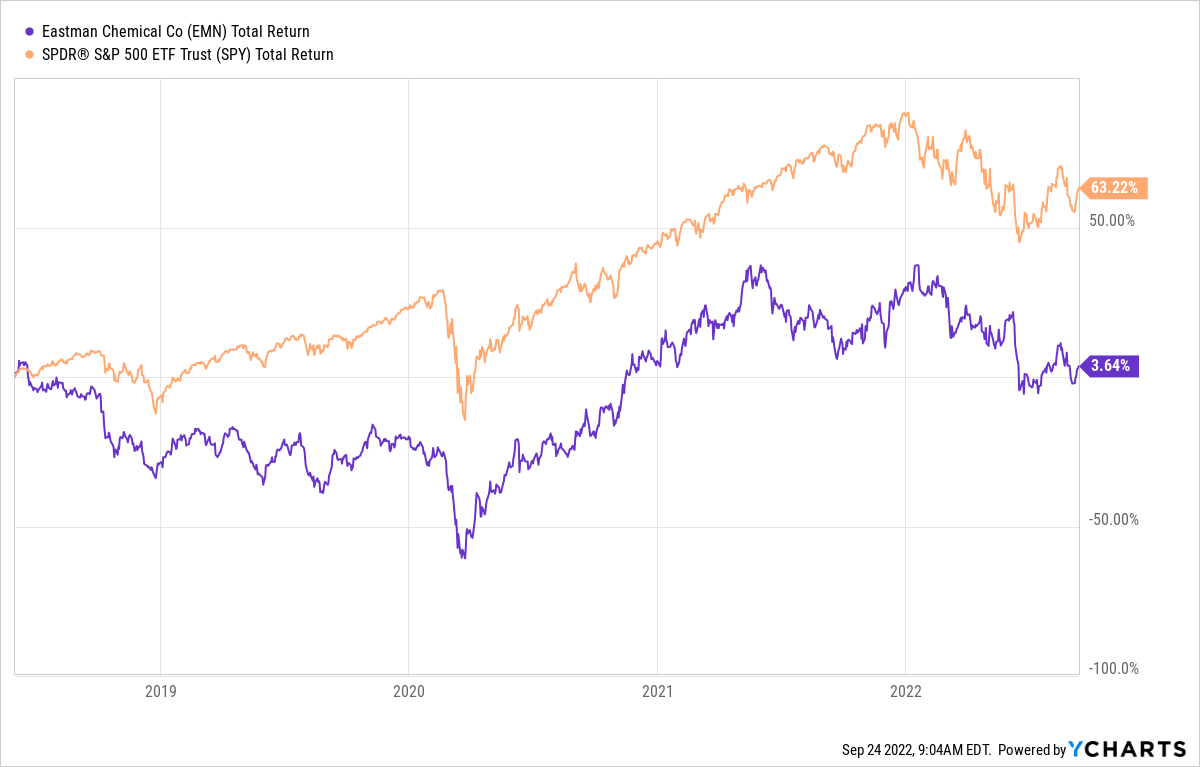

Eastman Chemical emerged strongly from the Great Recession, and its stock outperformed the S&P 500 Index by more than a 3-to-1 margin through May 2018.

The company’s cyclical business ebbed and flowed over the next several years, producing a flat-ish total return from June 2018 through Sept. 12 of this year.

And we’ve already talked about what happened since Sept. 13. As poorly as the market has performed, Eastman’s stock price has fallen even more.

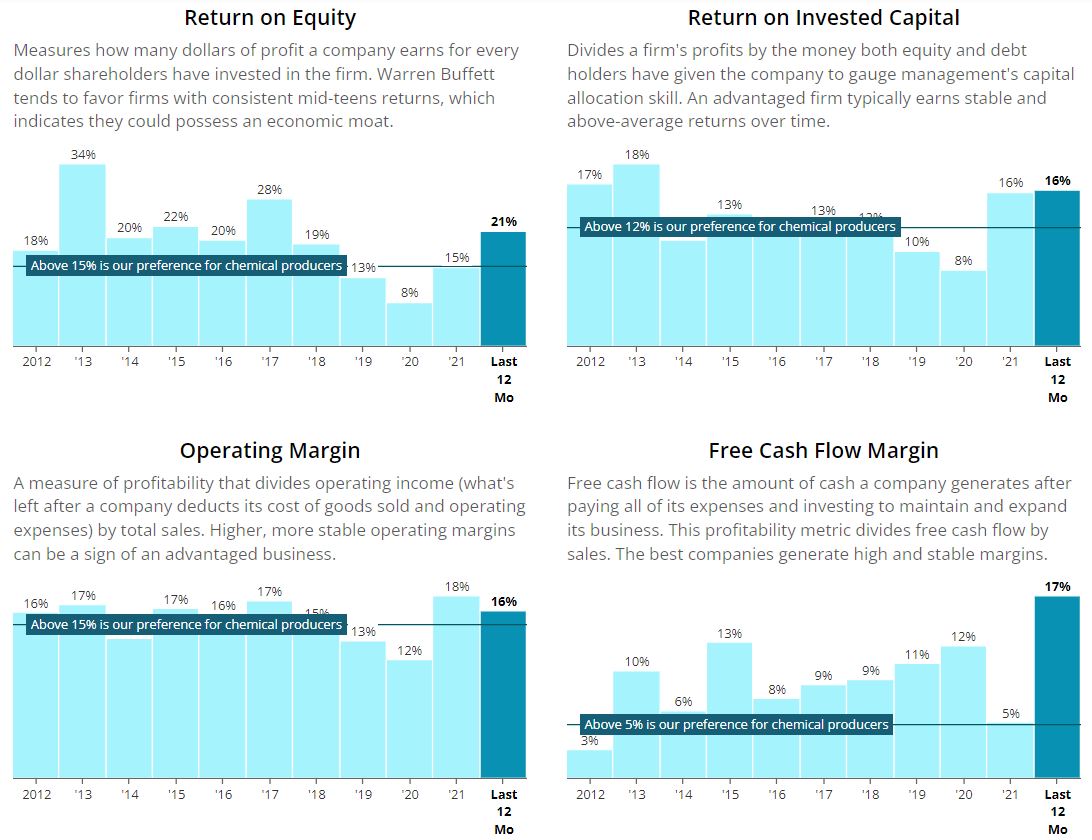

Despite the recent downdraft, though, we’re talking about a fine operation.

For most of the last decade, Eastman has had outstanding margins and return on equity.

SimplySafeDividends.com

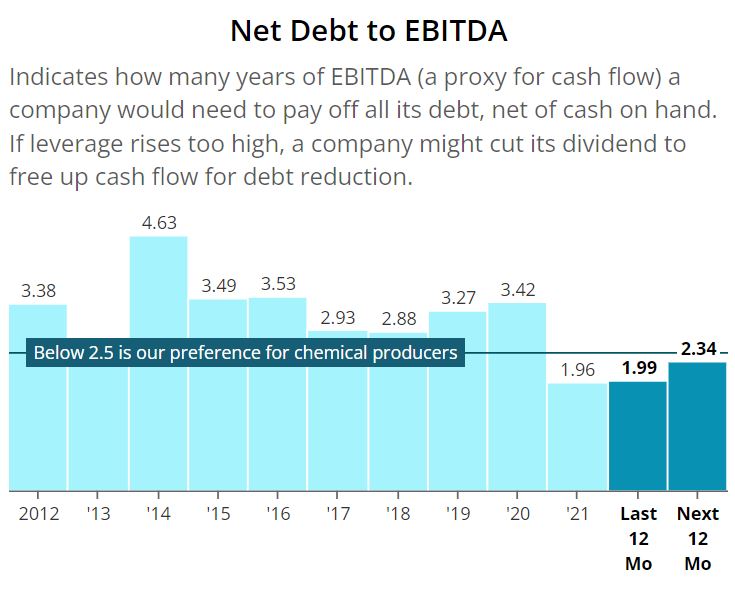

Eastman’s balance sheet is in good shape, as the company has reduced its debt significantly the last few years.

SimplySafeDividends.com

A look at the last decade of EPS shows how cyclical earnings can be in the sector, but also demonstrates the general upward movement for the company.

SimplySafeDividends.com

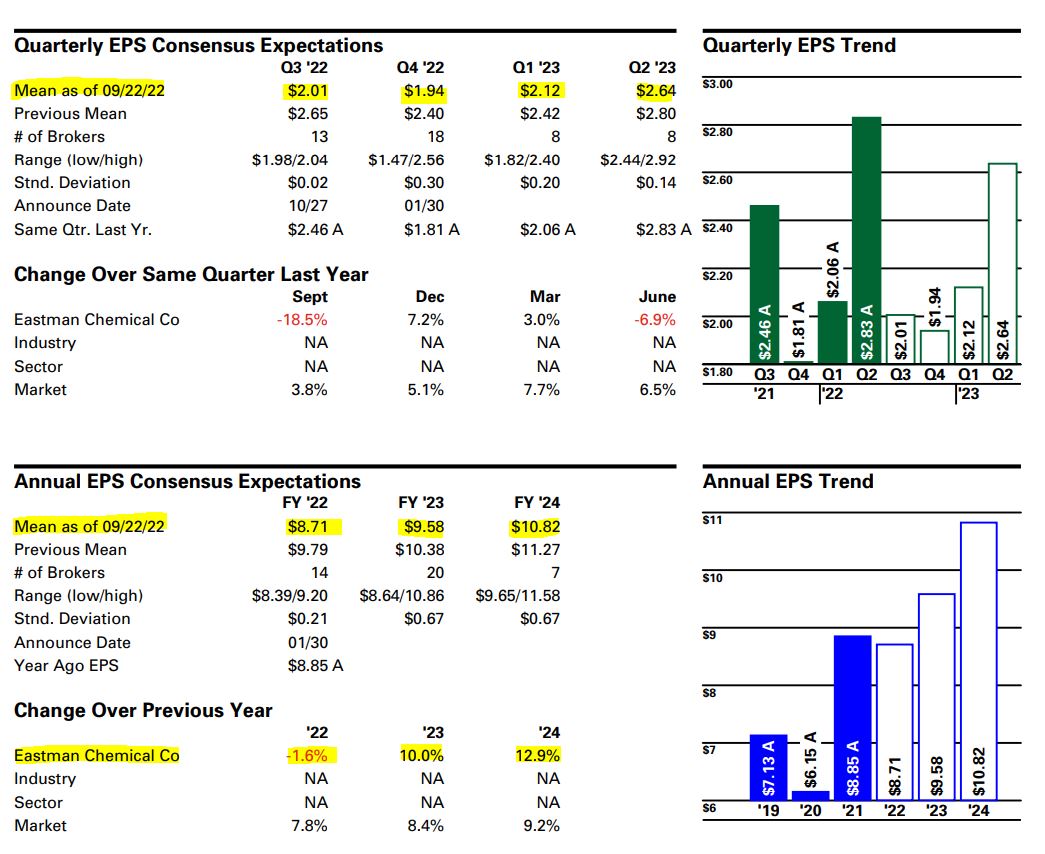

Following management’s lead, analysts have lowered their expectations for the rest of this year, as well as for 2023 and 2024.

The following graphic from Refinitiv reflects those revisions, but it also indicates pretty nice projected growth, with EPS expected to rise about 10% in 2023 and another 13% in 2024.

Refinitiv, via fidelity.com

And because investing is always about trying to look into the future, we’re buying Eastman’s expectations of growth in earnings, sales and free cash flow. As Morningstar’s Goldstein said:

We think the market may be overly weighing the company’s near-term results. We forecast declining revenue and contracting margins in 2023. However, we expect the decline will be short-lived. We estimate around half of the company’s end-market exposure is less cyclical as the company sells into the agriculture and healthcare end markets, while the other half has more cyclical exposure.

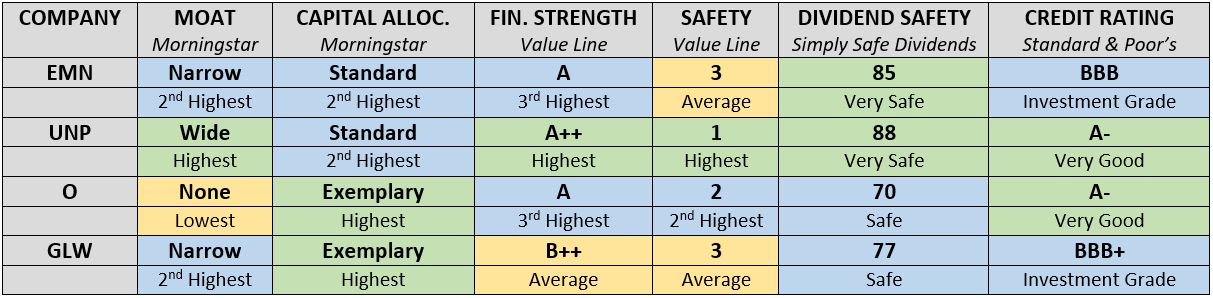

Eastman receives solid quality grades from Morningstar, Value Line, Simply Safe Dividends and Standard & Poor’s — as do all of the companies we bought for the IBP in this latest round of purchases.

Dividend Doings

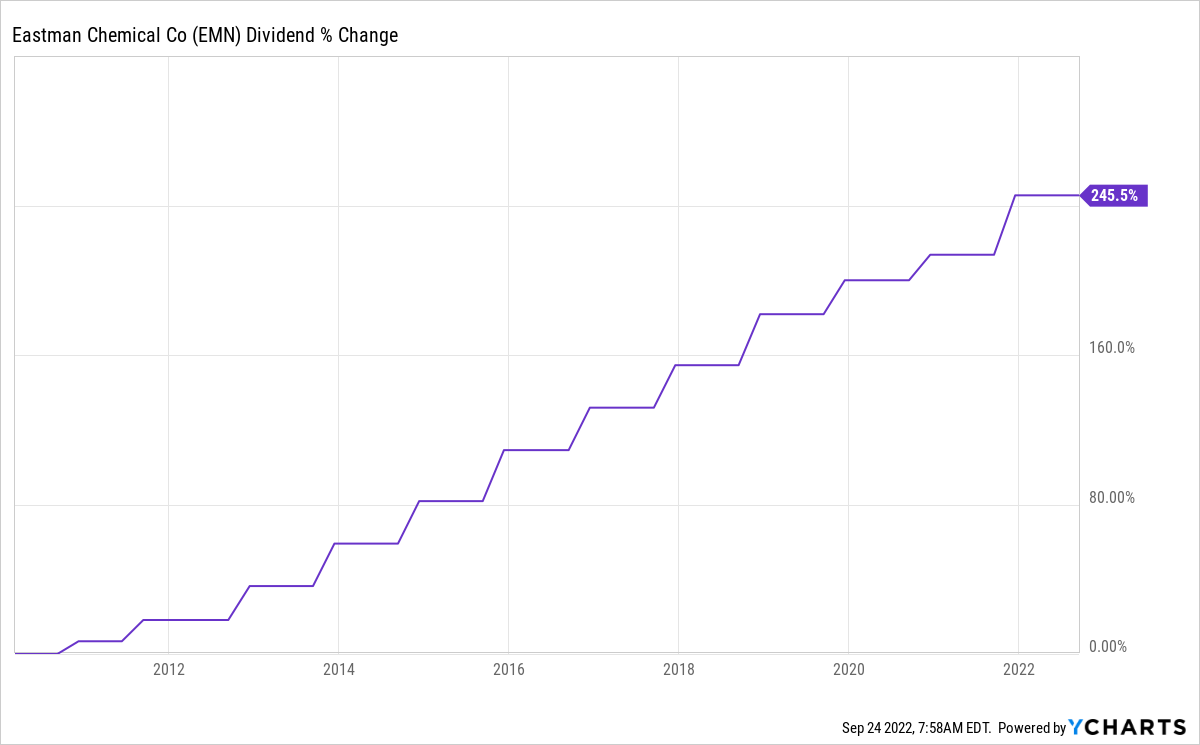

Eastman Chemical has been paying dividends without interruption for 27 years, but only relatively recently did it became the kind of company that Dividend Growth Investing proponents could embrace. The payout has increased by an average of 11% over the last decade.

The combination of the increased dividend and the falling stock price has pushed Eastman’s yield to 4.2% — aside from a brief spike during the market’s 2020 pandemic plunge, that’s the highest yield for EMN since the Great Recession.

Its most recent raise was 10.1% last December, and it’s due for another hike in a few months.

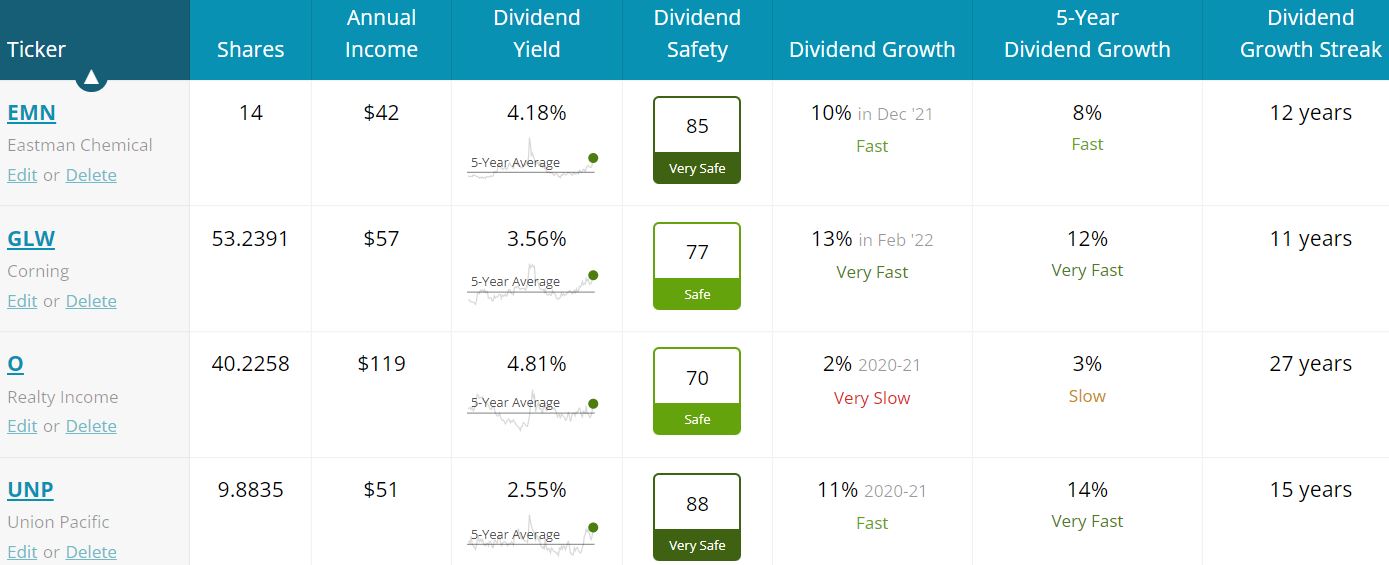

From Simply Safe Dividends, here is a look at various dividend-related information of the four stocks we bought for the Income Builder Portfolio in September:

SimplySafeDividends.com

The buys are expected to bring $77 in additional annual income to portfolio, with the four positions now projected to contribute about $271 to the IBP total.

Valuation Station

Given what’s gone on in the market this year, and especially the last month or so, there seemingly are a lot of “bargains” out there. With the Fed vowing to keep fighting inflation by raising interest rates, prices can (and probably will) fall from here.

Then again, Mr. Market doesn’t sound a horn at the bottom. So in times like these I try to identify high-quality dividend-growing stocks at what I feel are compelling values, and then I make relatively small buys.

Still, I understand why some investors would say, “I’m not buying anything until I see signs of a turnaround.” I just hope all those sages will let us know when it’s “safe” again!

Not surprisingly, analysts say all four of the stocks we bought in September look undervalued. Here are some of the fair values and target prices:

*As a REIT, Realty Income’s valuation is stated in price/adjusted funds from operations ratio (P/AFFO).

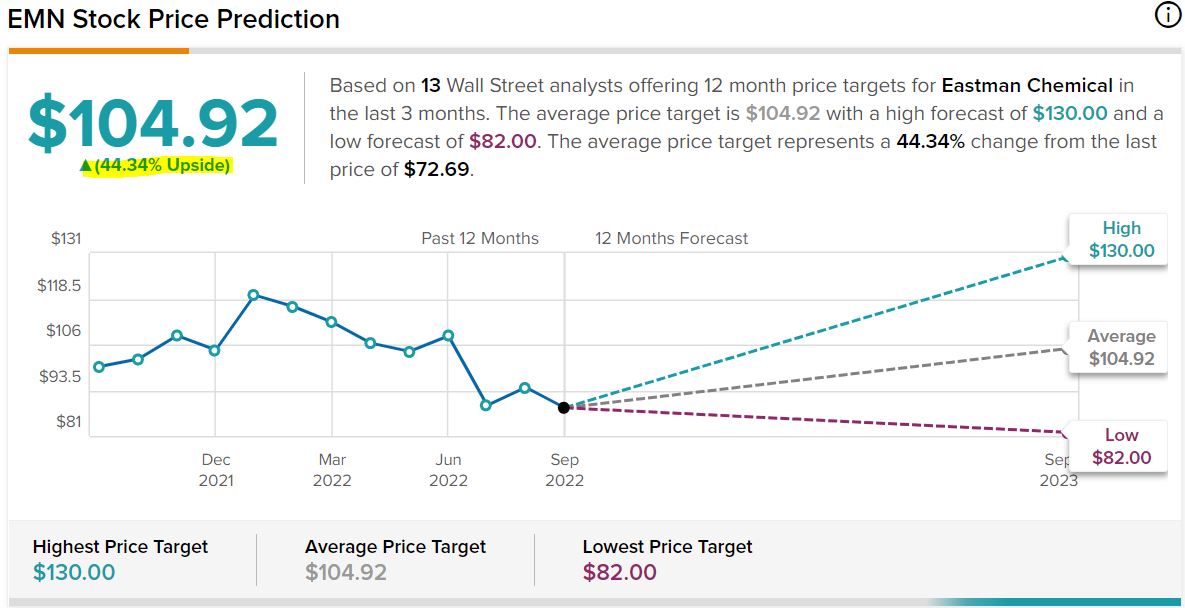

Getting back to Eastman Chemical specifically, pretty much every analyst out there thinks EMN’s price will move considerably higher over the next year.

The average 12-month target price of the 13 analysts monitored by TipRanks is $104.92 — suggesting a 44% upside.

TipRanks.com

Analysts at Morgan Stanley recently ran a quantitative screen to determine the top stocks to own (and also those to avoid) over the next year. No. 1 on the “stocks to own” list was Eastman Chemical, with a 77% upside.

Value Line says EMN could see 65% price appreciation over the next 18 months; its analysts also project as much as a 113% price gain over the next 3 to 5 years.

valueline.com

Wrapping Things Up

I’m a big fan of celebrating investing milestones, and we just achieved a pretty big one:

The Income Builder Portfolio’s projected annual income stream has raced past the $4,000 mark. Woo-hoo!

The stream actually has hit $4,075 (and counting), which means we’re more than 80% of the way to the goal we established when we launched the IBP back in January 2018 — $5,000 in projected annual income within 7 years. Considering that we still have three months to go in Year 5, we’re well ahead of schedule.

Eastman is the portfolio’s 49th position. To see them all, as well as links to every IBP-related article I’ve written, check out the home page HERE.

As always, investors are strongly urged to conduct their own thorough due diligence before buying any stocks.

— Mike Nadel

I have been working very hard to introduce you to the greatest trading book ever written. At my trading firm, the very first thing that any new trader had to do was read this book. They wouldn't be allowed in my office if this book was not read. Now, I've taken this book and built an entire trading system around it. For anyone that has any interest in trading, this is a must read. It's about success, failure and then success again. This book is being offered today, Get Your Copy Now.

Source: Dividends & Income