Like many who are passionate about investing, I am a numbers guy. And like many people who are serious about facts and figures, it’s hard to bite my tongue when I run across egregious errors in financial media that might mislead the investing public.

Here are a few that have irked me lately that you should watch out for:

Stock splits: Arguing that Alphabet Inc. (GOOGL) is different after its July stock split is like arguing that cutting a pizza into more slices somehow changes the quality of the crust. The value of a company or its total profits doesn’t change just because there are more shares (or slices) to go around.

Percentage gains and losses: If you lost 20% of your $100,000 portfolio yesterday and then made back 20% today, you are not back to even. After your initial loss you’d be at $80,000 but a 20% gain from there only gets you back to $96,000. Don’t forget to recalculate based on the new base.

Inflated dividends: Many cookie-cutter dividend screening tools simply take the most recent quarterly dividend and multiply it by 4X to calculate the yield. That can be very dangerous, as it doesn’t reflect how unsustainable that figure is for some companies.

This last issue has caused a lot of pain for income-oriented investors salivating over yields in the oil patch lately. Yes, there are some generous yields there if you know where to look. But quality matters.

Let me give you a case study in how to separate the good from the bad in this challenging sector comparing the more stable and reliable Kinder Morgan, Inc. (KMI) with the very risky Pioneer Natural Resources (PXD).

The Tortoise vs. The Hare

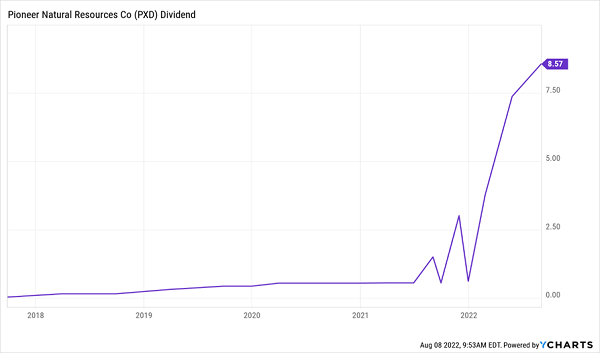

On the surface, there’s a lot to like about Pioneer. It went from paying dividends just twice a year as recently as 2018 to five total distributions in 2021 and an amazing upward climb in payouts.

Specifically, it paid just 32 cents in dividends for the full year 2018, but its latest dividend declaration is scheduled to pay a mammoth $8.57 in September alone – after a very generous $7.38 in May and $3.78 in February!

On the surface, that’s a tremendous track record. But dividend growth this dramatic should sound very suspicious to discerning investors – and after closer inspection, indeed seems too good to last.

On the surface, that’s a tremendous track record. But dividend growth this dramatic should sound very suspicious to discerning investors – and after closer inspection, indeed seems too good to last.

Yes, PXD has the cash to cover those payouts with projected earnings of more than $33 per share this fiscal year. But that’s in part because of a twin tailwind of rising oil prices and very shrewd hedging strategies to lock in attractive prices. The reality is that oil is now down more than 30% from its 2022 highs and Pioneer warned in late July that it is now on the wrong side of oil and gas hedging – and may actually record an $832 million loss thanks to futures trading, rather than windfall profits.

Those investors who piled into PXD a year ago certainly are more than pleased with their investment. But new money better tread lightly, or else they could find all the rosy predictions of double-digit dividends to fall well short.

Kinder Morgan, on the other hand, is a slow-and-steady stock that has learned from past energy volatility. For starters it is a “midstream” play focused on energy infrastructure, unlike an exploration and production stock like Pioneer. But most importantly, it has seen the negative consequences of dividend cuts before – and management will now move heaven and earth to avoid those kinds of headaches again.

Back in 2015, as oil began its slide to record lows that would eventually hit about $30 a barrel, KMI slashed its dividend from 51 cents quarterly to just 12.5 cents – and shares cratered as a result. In fact, they are still about half where they were prior to that dividend cut.

However, KMI has worked hard to restore investor confidence. The company has consistently raised its dividend each year since 2018, to 27.75 cents per quarter today — a 122% payout increase in less than five years.

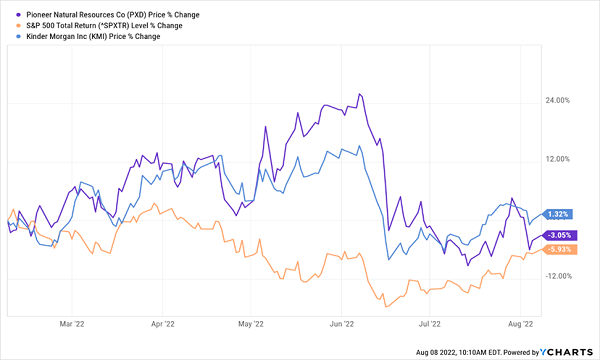

What’s more, KMI stock has actually outperformed both PXD as well as the broader S&P 500 index over the last six months of energy price volatility. Sure, Pioneer was looking better for a bit … but as soon as oil dropped, it fell fast and it fell hard.

What’s more, KMI stock has actually outperformed both PXD as well as the broader S&P 500 index over the last six months of energy price volatility. Sure, Pioneer was looking better for a bit … but as soon as oil dropped, it fell fast and it fell hard.

If this is the reaction even before the company goes ex-dividend, just imagine what will happen to shares once investors start to doubt future paydays.

How to Find Big, Reliable Dividend Payers

I’m not saying Kinder Morgan is perfect. It is still exposed in its own way to energy price volatility. But a stable and sustainable 6.2% yield and modest outperformance in a tough market seems like a much better idea than chasing the volatile and unreliable dividends in an oil explorer like Pioneer right now.

— Jeff Reeves

Sponsored Link: A deeper look into PXD vs. KMI also illustrates the danger of not doing your research. Many simple screening tools don’t account for long-term payout trends, or the outlook for a stock’s dividend payouts.

That’s where the research staff at Contrarian Outlook comes in. We look below the surface, identifying investments that have big yield but also investments that have staying power. And we refuse to chase fads that put risky short-term bets in front of long-term income and outperformance.

After all, dividend yield is normally calculated on an annual basis. Why would you bother investing in a stock if you can’t depend on it for more than a quarter or two?

In the wake of some big changes to the stock market in June and July, we’ve just updated our “7% Monthly Payer Portfolio” to reflect the realities on Wall Street. This diversified portfolio of dividend payers is built to provide a 7% payout on a monthly cycle – regardless of short-term volatility.

That means if you have a $500,000 portfolio, you’ll be raking in nearly $3,000 per month in dividends alone.

And best of all, you’ll never be required to withdraw a dime and put that initial nest egg at risk!

All of these monthly dividend stocks are running strong right now thanks to a combination of great performance, generous paydays and a bright long-term outlook. Click here to learn everything you need to know about these 7% dividend payers… and start cashing in those monthly checks ASAP!

Source: Contrarian Outlook