If you read only the CFRA analyst’s report, you wouldn’t buy shares of Honeywell (HON) … and if you already owned some, you’d probably unload them.

Then again …

If you read only the Morningstar analyst’s report, you very well might back up the truck and load up on Honeywell stock.

That contrast might tell us a bit about the value of stock analysts overall. (My takeaway: It’s OK to see what they have to say, but perhaps not wise to treat their word as it’s gospel.)

It also might tell us a little something about Honeywell, one of the world’s leading industrial conglomerates. Like many companies in the sector, its up cycles and down cycles can mean extreme differences in the price of its stock.

When I’m deciding whether or not to buy any stock, I first try to focus on the company’s business model and financial strength. I also pay attention to the reliability and growth of its dividends over time. Only then might I check out some analysts’ takes.

All in all, if I like what I see, I’ll do my best to buy shares at what I consider a reasonable price.

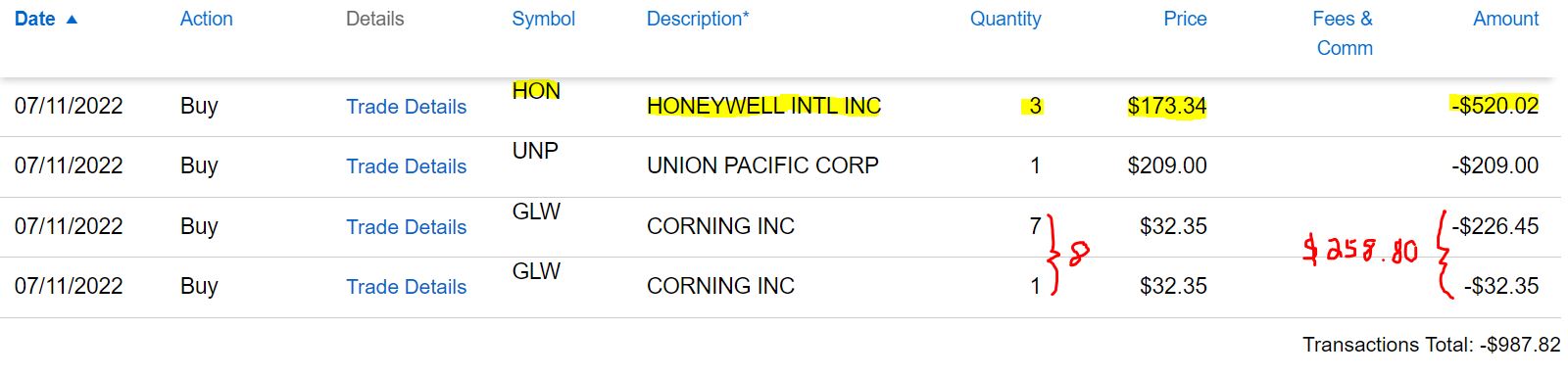

Honeywell fits the bill for me, so I decided we should add to our stake in the Income Builder Portfolio. On Monday, July 11, I executed a purchase order for 3 HON shares on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

As you can see, I used the rest of Greg’s semi-monthly allocation to keep building two of our newest, smallest positions: Union Pacific (UNP) and Corning (GLW).

They are high-quality operations — with Union Pacific Railroad being vital to American commerce, and Corning’s display and optical technology being instrumental to thousands of products. (My investment theses on UNP is HERE, and on GLW is HERE.)

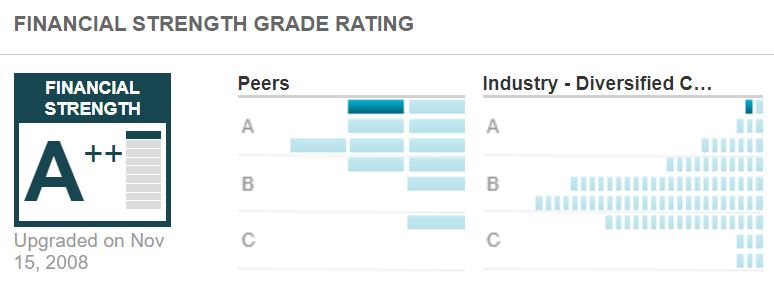

Honeywell, though, is the crème de la crème. Just look at these quality-related grades from various analytical services and ratings agencies:

I’ll talk a little more about Corning and Union Pacific later; the focus here, though, is on Monday’s main buy.

HONey Of A Business

Few observers — even those who aren’t bullish on the company at its current price — would question the strength of Honeywell’s business. As the following Value Line graphic shows, HON is at the top of the heap.

valueline.com

Over the decades, Honeywell has proven its ability to generate significant income, sales and free cash flow.

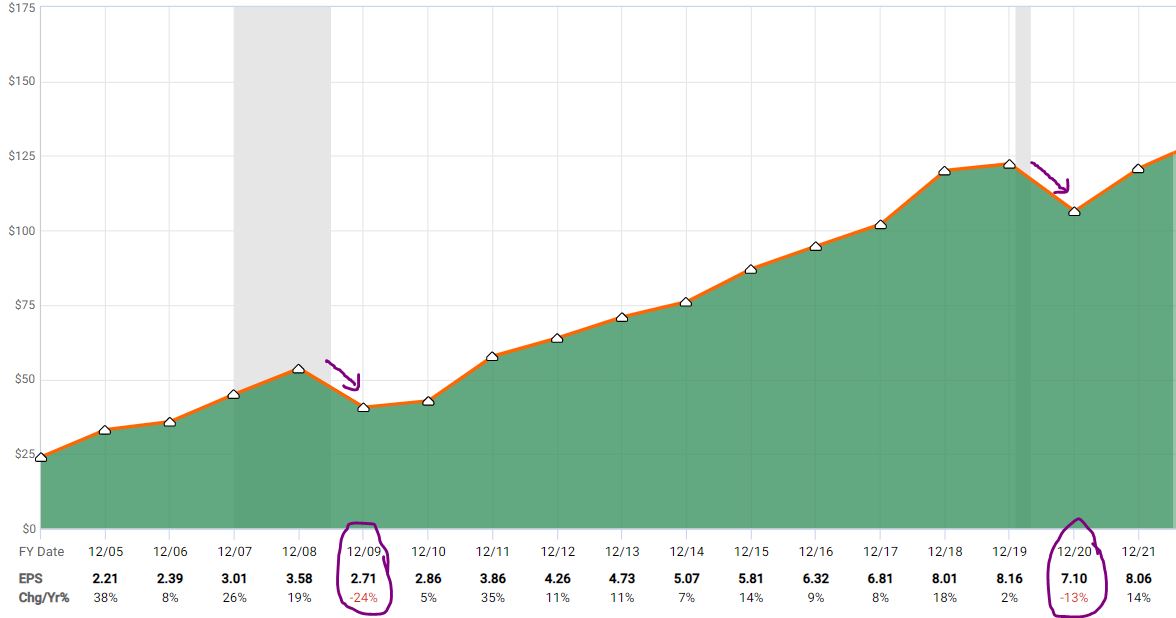

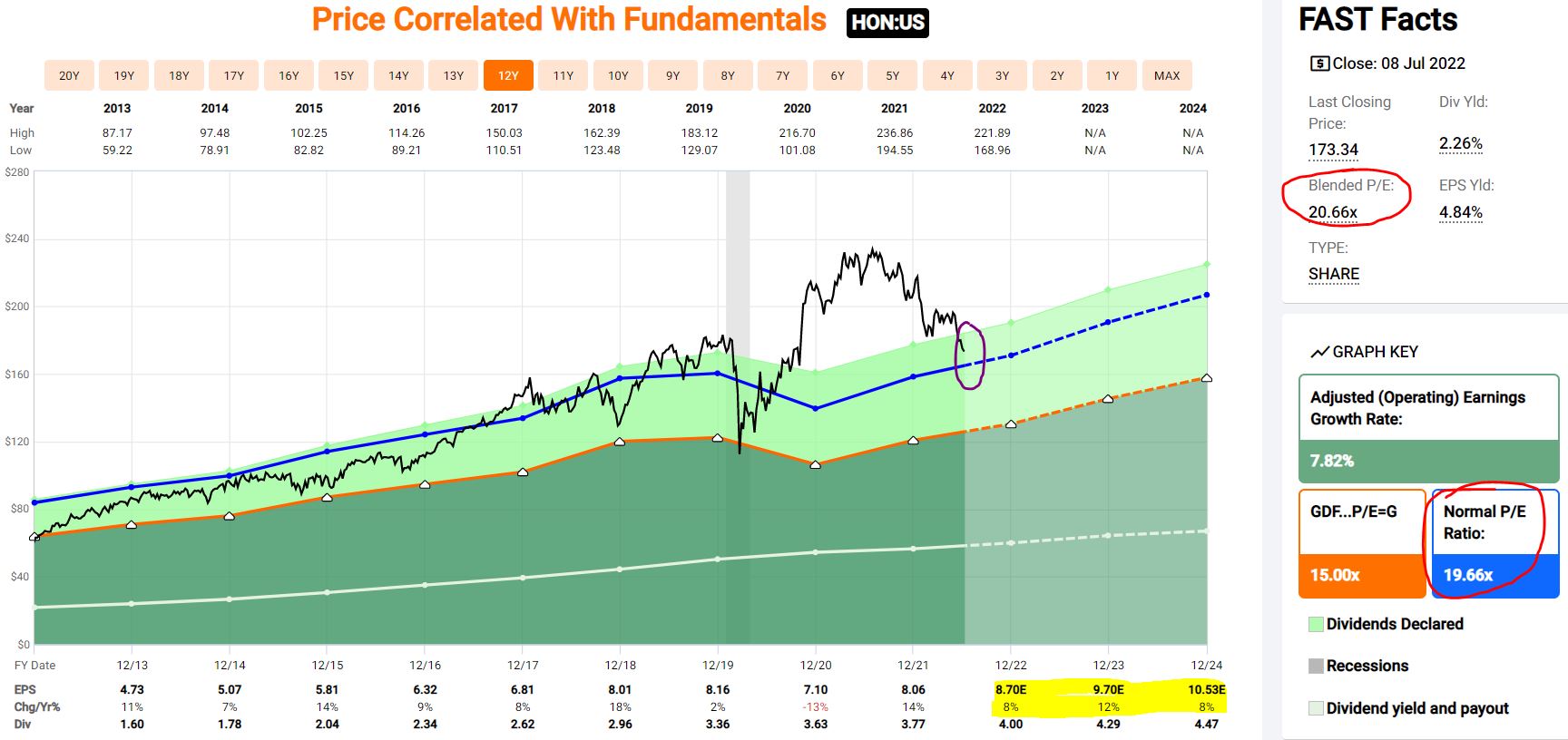

The following FAST Graphs image shows how consistently Honeywell has grown earnings per share over the past 15+ years. The only two years in which HON suffered EPS declines (as marked in purple) — during the depths of the Great Recession and the COVID-19 pandemic — were followed by strong ascents.

fastgraphs.com

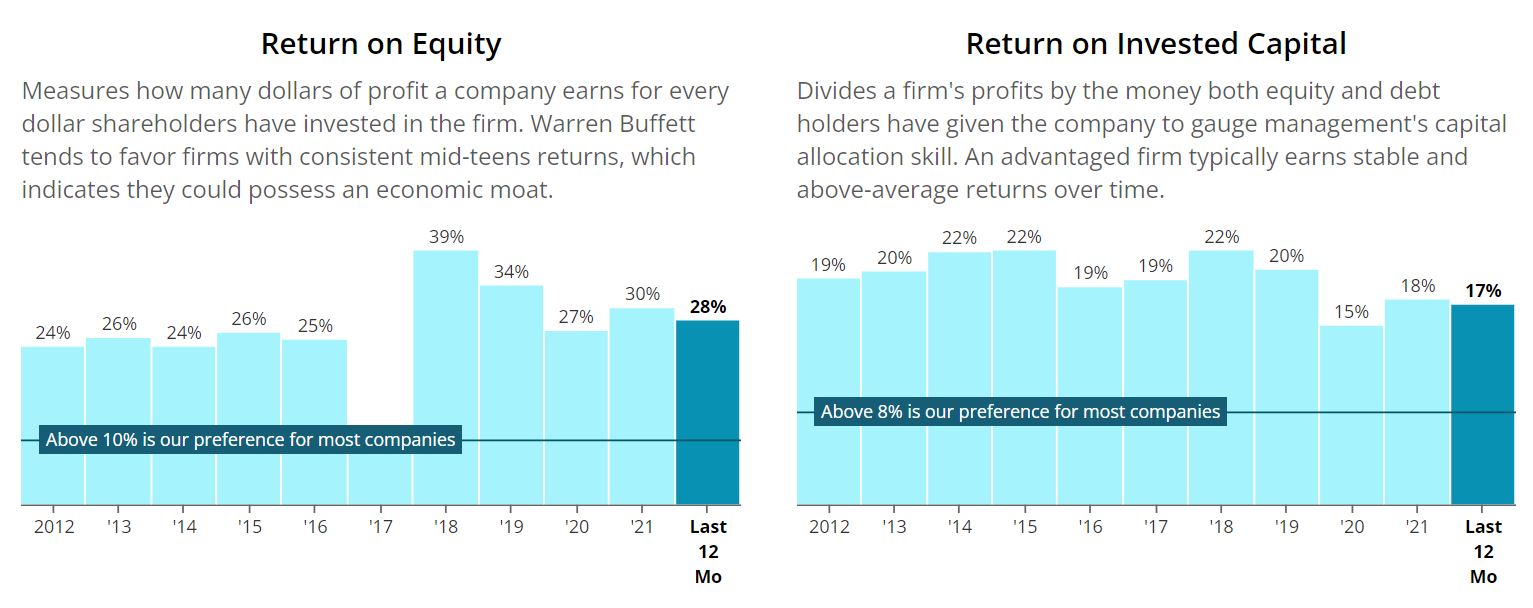

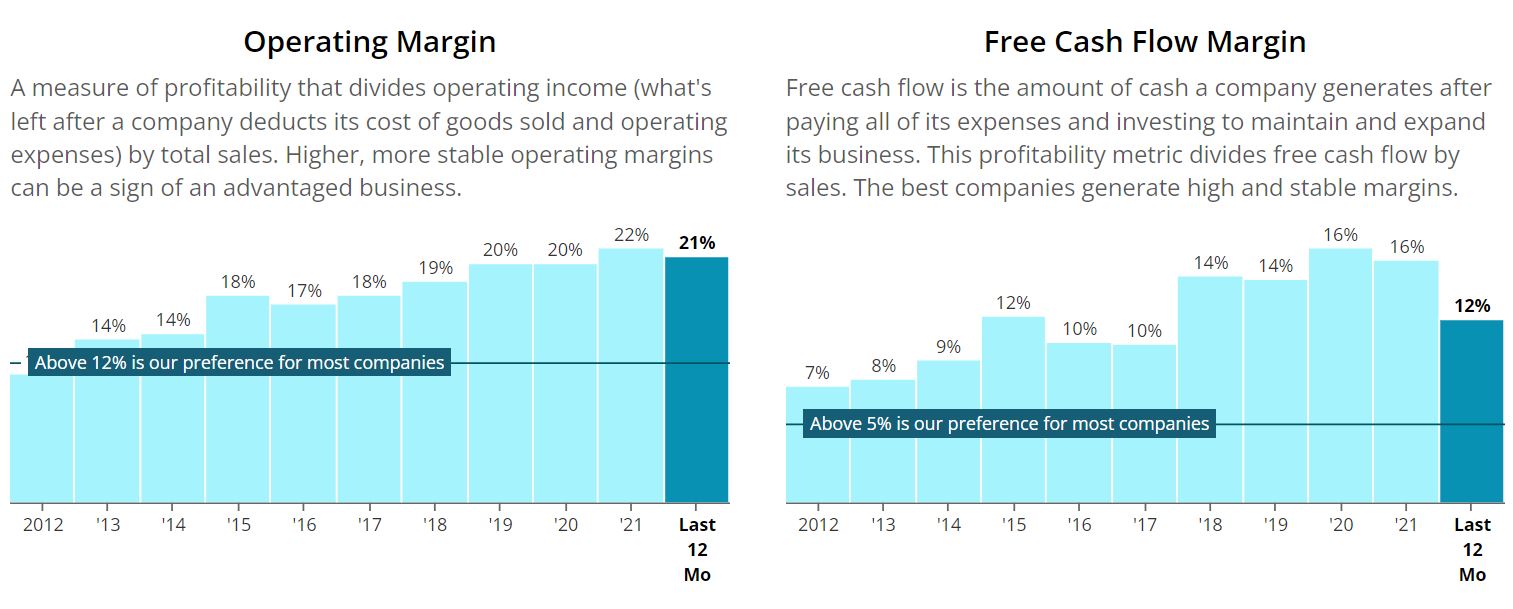

Across the board, Honeywell’s metrics are impressive, as indicated in the following decade-long look at return on equity, return on invested capital, operating margin and free cash flow margin.

SimplySafeDividends.com

SimplySafeDividends.com

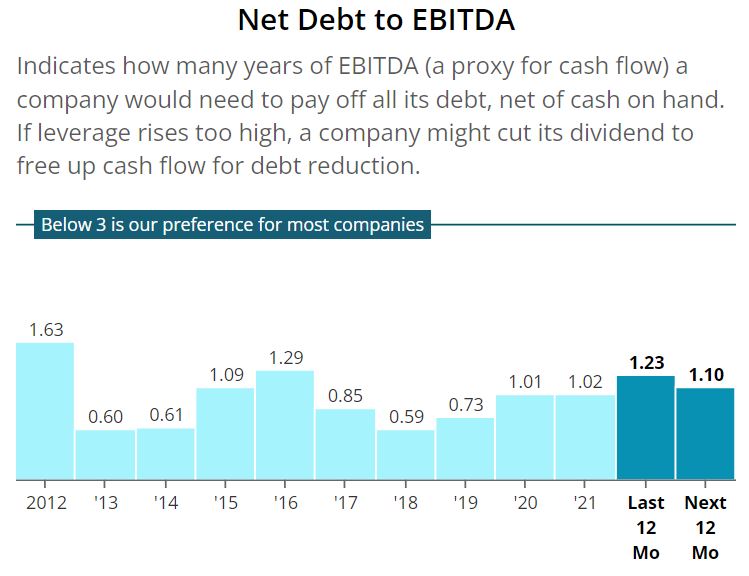

And Honeywell has done all this while maintaining a reasonable debt level. In these times of high inflation and rising interest rates, it’s crucial that companies have their balance sheets under control.

SimplySafeDividends.com

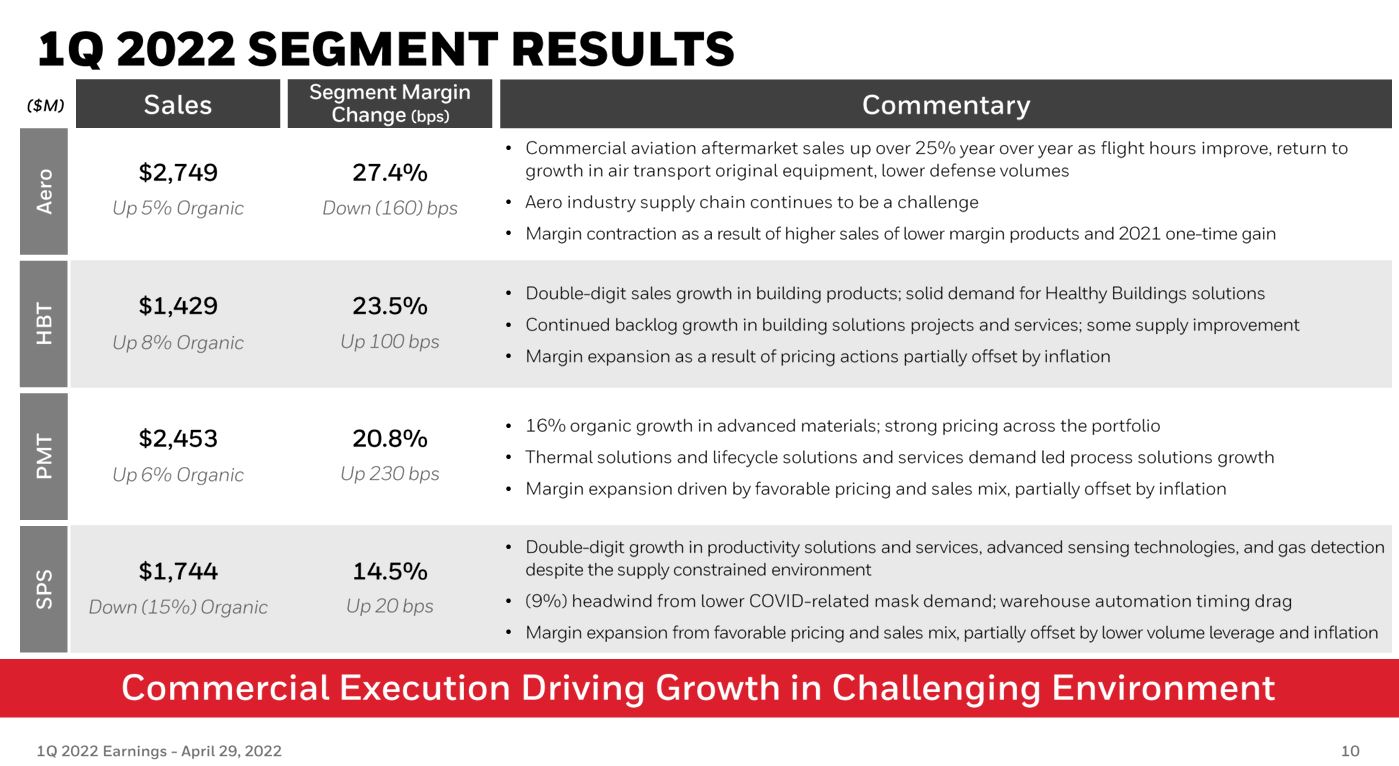

The company divides its operations into four segments: Aerospace; Honeywell Building Technologies; Performance Materials and Technologies; and Safety and Productivity Solutions.

Here is a slide from the first-quarter earnings report, summarizing how each segment performed during Q1:

Honeywell is scheduled to report Q2 results on July 28, and potential investors might decide it’s prudent to wait at least until then to make decisions regarding the stock.

Bank of America Securities opted not to wait, however, announcing Monday that it had upgraded HON stock from “neutral” to “buy.”

cnbc.com

Valuation Station

As long as I’ve shifted the subject back to analyst reports and valuations, let’s focus on that for a bit.

FAST Graphs uses a measurement it calls “blended P/E,” which combines the trailing price/earnings ratio with the forward P/E ratio. At 20.66, Honeywell is trading just about in line with its 10-year norm. The purple circle in the graph shows how the black price line sits only slightly above the blue normal P/E ratio line.

fastgraphs.com

I also like that Honeywell is expected to grow earnings at a healthy clip over the next few years (as shown in the yellow highlighted area) — for a total of about 30% projected EPS growth from 2021 through 2024.

Of course, guidance the company gives in future earnings calls could result in changes to those estimates.

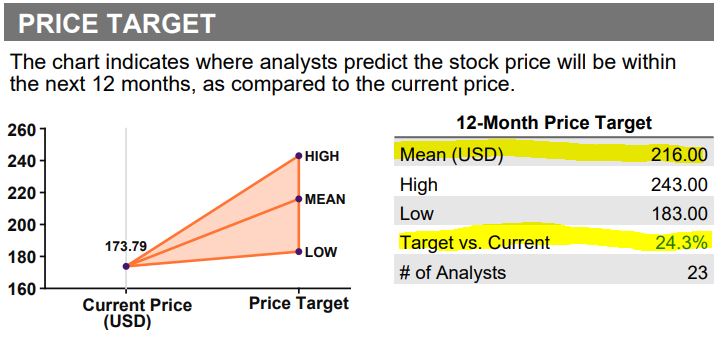

An aggregate of analysts monitored by Refinitiv results in a mean 12-month target price of $216 per share for HON stock — suggesting a 24% upside.

Refinitiv, via fidelity.com

Additionally, 16 of 29 analysts consider Honeywell to be either a “strong buy” or “buy.”

Refinitiv, via fidelity.com

One of those ratings does stand out in red — the “strong sell” from CFRA. Here’s what its analyst, Colin Scarola, said on May 11:

Our Strong Sell reflects our view that current valuation is too optimistic on HON’s long-term growth trajectory. Key end-markets for HON include commercial aviation, where soft demand is likely for at least two more years due to excess airline capacity amid the pandemic, which could also be a long-term issue if business travel never fully recovers; commercial buildings, which could see a long-term slump as interest rates rise and office tenants increasingly downsize leases to transition to work-from-home; and oil and gas, where risk stems from developed economies pushing anticarbon regulations and long-term decline in gasoline demand as electric vehicles and remote-work trends gain momentum.

Given recent sales decline amid a global economic recovery, and serious long-term risks to key end-markets, we don’t expect HON’s long-term EPS growth to beat the market. Yet shares currently trade at 20x consensus 2023 EPS, well above the S&P 500’s 16x, which we find difficult to justify. Key risks to our view are that the long-term stagnation we think might play out in commercial construction and oil and gas production turns out to be wrong.

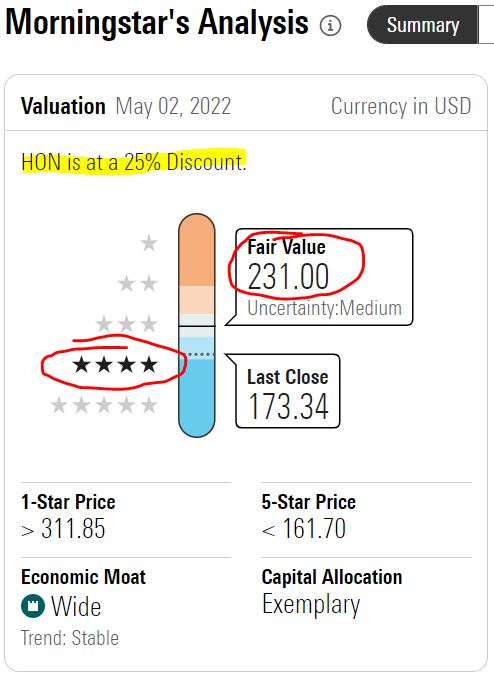

At the other end of the spectrum, Morningstar rates Honeywell a “4-star buy,” and says the stock is trading at a 25% discount to an estimated fair value of $231. Here’s analyst Joshua Aguilar’s take:

Honeywell is one of the strongest multi-industry firms in operation today. … Over the next five years, we think Honeywell is capable of mid-single-digit-plus top-line growth, incremental operating margins in the low-30s, low-double-digit adjusted earnings per share growth, and free cash flow margins in the mid-teens.

We believe Honeywell is capable of meeting our assumed targets through a combination of portfolio refreshes, powerful new product introductions, breakthrough initiatives, and strategic partnerships in areas where the firm has domain expertise, a focus on high-growth regions that’ll help the firm grow faster than its core markets, continuous improvement initiatives centered on fixed cost reduction, on-time delivery and simplified design, supply-chain automation, and an increasing shift toward software with a recurring revenue stream. In our view, Honeywell was wise to continue investing aggressively during the height of the pandemic, which we think will reward the firm with share gains. …

Honeywell’s early-stage investments like quantum computing represent a leapfrog in technology, and we think they have multiple use cases in fast-growing industries like cybersecurity. … We view Honeywell as one of the highest-quality companies in the diversified industrials space and assign the firm a wide economic moat.

It’s up to each investor to analyze the analysts to help decide if a company is worth buying and if the price is right. The following table includes more analyst calls on Honeywell, as well as information that could be helpful in evaluating Corning and Union Pacific.

Of the three, Corning looks like it’s the most attractively valued, but I believe Honeywell and Union Pacific are quite “buyable” here. (Disclosure: I also own HON and UNP in my personal portfolio but do not have a GLW position.)

Dividend Dandy

I’m into Dividend Growth Investing, and the Income Builder Portfolio is, at heart, a DGI-based project. So to me, Honeywell’s decades-long history of reliable and increasing dividends is a big part of its appeal as an investment.

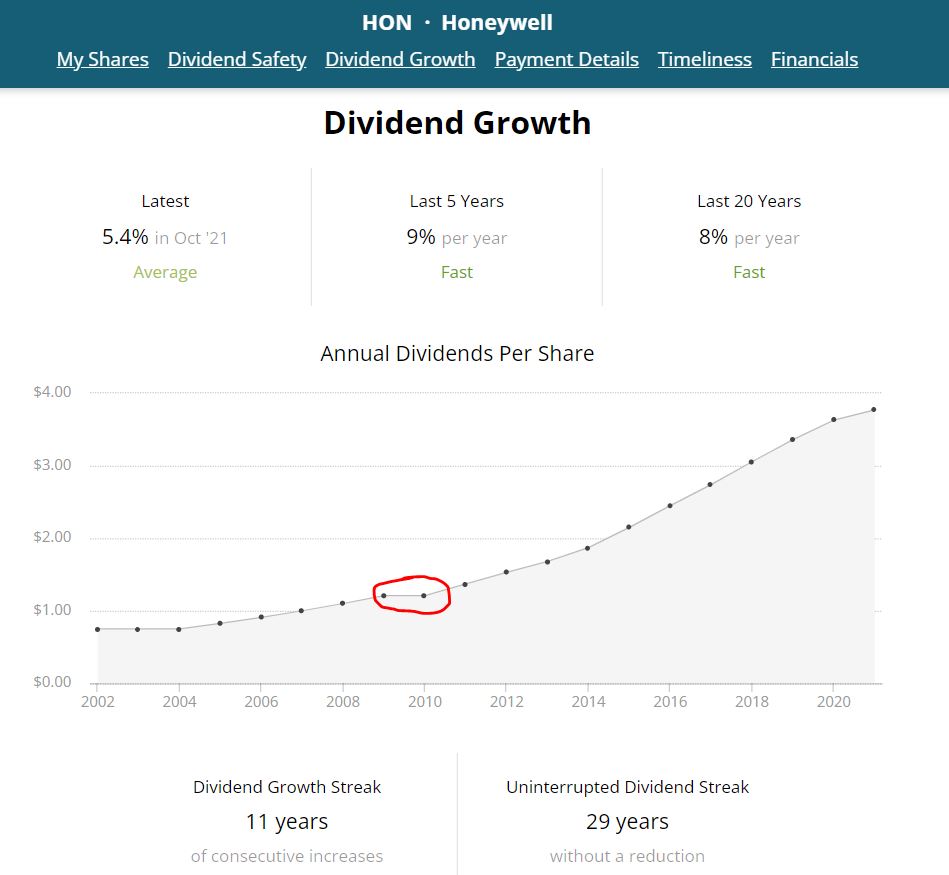

Its only dividend freeze, in the aftermath of the Great Recession, lasted just one year (red circle on image below).

SimplySafeDividends.com

After nine consecutive years of double-digit-percentage dividend growth, Honeywell had more modest increases in 2020 (3.3%) and 2021 (5.4%). HON will announce its next raise in the fall; given today’s challenges, I’m expecting another mid-single-digit hike.

With Monday’s buys, Honeywell, Union Pacific and Corning are projected to generate $167 in income over the next year — about 4.3% of the IBP’s $3,863 total. Here is some more income-related data on the portfolio’s three positions in the companies, as compiled by Simply Safe Dividends:

Wrapping Things Up

Honeywell’s dividend yield is only about 2.3%, which might be lower than some DGI practitioners like. That doesn’t especially bother me, as we own many lower-yielding stocks than that, and I love being able to count on HON paying (and raising) its dividend like clockwork — as indicated by the near-perfect 99 score the company receives from Simply Safe Dividends.

It’s all part of what makes Honeywell the kind of financially strong, wide-moat, well-managed business I want.

![]()

A table with information on all 48 Income Builder Portfolio holdings, along with links to every IBP-related article I’ve written, can be found HERE.

I also run another real-money project for this site, the Growth & Income Portfolio, featuring “growthier” names such as Alphabet (GOOGL), Costco (COST) and Zoetis (ZTS). See it HERE.

As always, investors are strongly encouraged to conduct their own thorough due diligence before buying any stocks.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com