I don’t know if you’ve noticed, but there’s been a flurry of doom-and-gloom articles making the rounds that all preach the same thing: anyone looking to retire now faces a bleak time of it indeed.

To that I say: nonsense! Below I’ll show you three closed-end funds (CEFs) whose yields are so high right now (up to 11.2%) that buying them and living off their rich payouts has rarely been this attractive.

We’ll talk more about these three funds, and the many benefits CEFs offer retirees, shortly. First, let’s talk about the “retirement alarmism” we’re seeing in the media today. Because these articles (all driven by the fact that fearsome headlines get clicks) suggest that a mix of high inflation and still-high stock valuations will result in retirees facing much lower “safe withdrawal rates,” or SWRs.

The “SWR” term comes from retired financial advisor William Bengen, who first wrote the popular rule that you can withdraw 4% of your investments yearly and have enough money to keep going through retirement.

Bengen came up with the 4% figure in the mid-1990s. At the time, he simply looked at past stock and bond returns and figured how much one could withdraw to cover inflation and living costs. A retiree who took out 4% wound up with a portfolio that lasted decades; one who took out 5% yearly ran out of money.

Sure, that may have made sense back then. But let’s fast-forward to today and look at the returns on a portfolio of 55% stocks and 45% bonds, which was the weighting Bengen used when developing his rule.

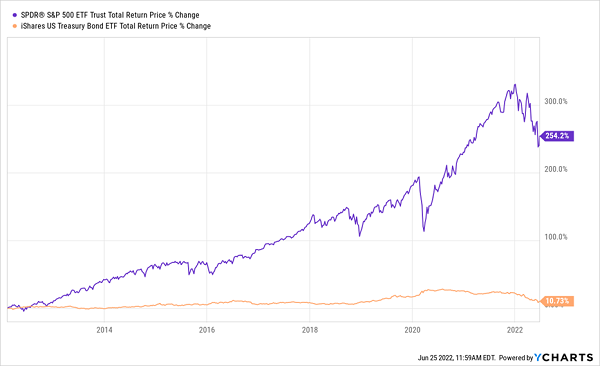

1990s Retirement Rule Crumbles Today

A quick look at the historical returns of both asset groups shows the first problem when applying the 4% rule in the last decade: government bonds delivered terrible returns.

In fact, switching to all stocks would have allowed for an SWR of 11.5%! This was not only because stocks on their own delivered a 13.5% average annualized return over this period, while bonds returned about 1%, but also because inflation was low, averaging around 2%.

Bengen, to his credit, realized this and swiftly changed his 4% rule to 4.5% and again to 4.7%, although his model still assumes an extremely high allocation to government bonds for a long period, which puts a strict limit on returns.

Things are different now, of course. Inflation is high, and stock returns this year have been, well, let’s just say not great. So is it time to give up on the 4.7% SWR rule?

Forget the 4% Rule. Try the 8% Rule Instead

One of the reasons why Bengen’s rule is so popular is that it’s simple: you have a strict rule that encourages over-saving so, in the end, you won’t face the unhappy prospect of running out of money in retirement.

Thing is, there’s an even easier way to retire than the 4% rule. It doesn’t rely on lowly returns from government bonds or big-name ETFs that dribble out measly sub-2% returns.

The best part? You won’t have to sell a single share in retirement! So when a crash like the one we’ve been enduring this year hits, you can keep your portfolio intact without having to unload shares at depressed prices to generate extra cash. This is also a great way to leave a legacy to your loved ones.

3 CEFs That Send the 4% Rule to the Dustbin

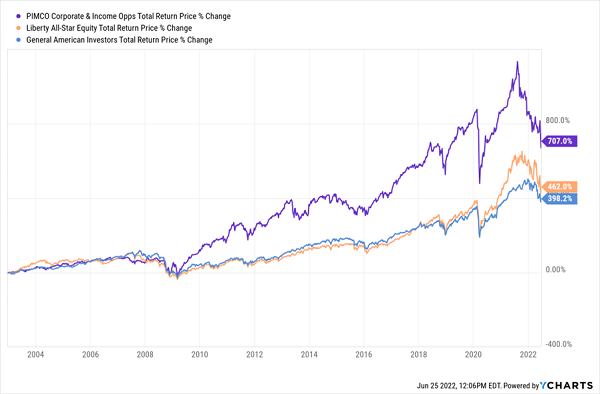

I’m talking, of course, about CEFs. The three we’re going to focus on are the PIMCO Corporate & Income Opportunities Fund (PTY), Liberty All-Star Equity Fund (USA) and General American Investors Fund (GAM).

These three funds get you corporate bonds (through PTY), a basket of blue chip stocks (with USA) and value stocks (through GAM).

Soaring Returns From Professionally Run Funds

Put these three together and you have a portfolio that has provided strong returns over two decades, coming close to the full length of the average American retirement. Investors who ignored Bengen’s advice when it first came out and put their money here instead would have received an annualized 8.7% return overall, including high, reliable dividends.

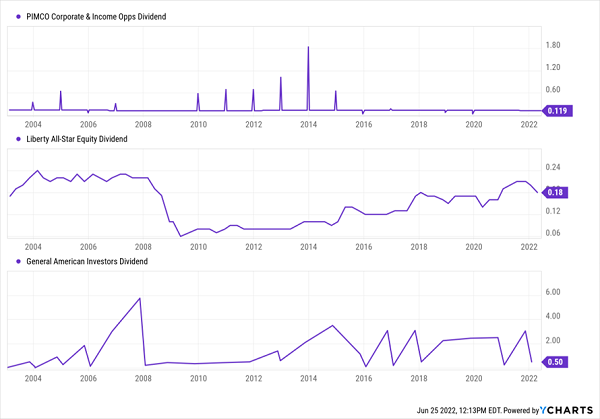

Sustainable Payouts and High Yields

Because of these funds’ managed-distribution policies, which allow management to control payouts relative to market conditions, they could, on average, sustain reliable payouts over the long term. That’s why GAM and PTY could continue the level of payouts investors expected. USA’s dividends did dip during the Great Recession, but the fund returned a hefty 670% from the low of that disaster until now, so we’ll happily give it a bit of a break here.

Now let’s talk payouts, because as I mentioned, the recent selloff has made these funds’ dividends very attractive indeed.

9.5% Is the New 4.7%

Since yields rise as prices fall, the selloff means that, as of this writing, PTY’s yield has soared to 10.8%; USA’s has climbed to 11.2%; and GAM’s has hit 6.5% (which, incidentally, is a little low for a CEF, but we’ll take it for GAM’s more conservative approach).

Put them all together and you’ve got an average dividend payout of 9.5% that means you don’t have to sell a single stock. This is the real Achilles’ heel of Bengen’s approach because it means you have to sell stocks and bonds continuously, regardless of market conditions, which today could mean being forced to sell at a loss.

But CEFs, thanks to their high dividends and professional managers, who can steer them through turbulent times, work more actively to protect portfolios during downturns like those of 2008, 2020 and 2022. Funds like the three above can keep paying out high yields that double your SWR from Bengen’s level all the way up to 9.5%.

— Michael Foster

These 5 “Retirement-Ready” CEFs Have an Incredible Safety Record (and Yield 7.9%) [sponsor]

When I talk to investors about CEFs, many don’t realize how well-established many of these funds are: there are plenty of CEFs that have been paying dividends for decades. In my CEF Insider service, we even recommend one fund that was founded back in 1929!

And here’s something else to consider: of the CEFs that have been around for a decade or more, 96% have made money. Of the 14 that did lose money, almost all were in the energy sector. Dump those and you’re looking at a near-100% success rate for the most well-established CEFs.

The three CEFs I’ve just showed you are good examples of the reliable, well-run funds that are out there. And I’ve zeroed in on five more CEFs that are even better deals today, with wide discounts I see propelling them 20%+ above today’s levels when the market finally settles. Meantime, we’ll collect some very tidy dividend payouts, thanks to their 7.9% average yield.

Go right here and I’ll give you a full breakdown of this terrific asset class and show you how to get an exclusive Special Report detailing the names and tickers of these 5 reliable 7.9%-yielding CEFs. I’ll also give you an opportunity to road test CEF Insider on a risk-free basis.

Source: Contrarian Outlook