As difficult as this selloff has been for all of us, it has left some attractive (and discounted) dividends on the board, especially in high-yield closed-end funds (CEFs).

I know it’s tough to buy in a market like this, but the dividends we’re going to talk about today actually benefit from rising inflation, posting higher and higher cash flows as the CPI shoots higher and higher, too.

These are the companies we want to be in now, both to collect their high dividends through today’s tire fire and to profit when the market waters (inevitably) calm and investors finally take notice of these stocks’ sturdy cash flows.

REITs Are Underappreciated All the Time—Especially Now

I’m referring to real estate investment trusts (REITs). These “landlords” are by far my preferred way to invest in real estate—much better than buying a home yourself and renting it out (unless you enjoy replacing broken appliances and unclogging toilets, that is).

Let’s start with the rent checks all landlords (REITs included) are collecting today, because they’re on the rise, due to many trends that don’t look like they’ll subside soon. The first is rising interest rates, which, when mixed with still-high home prices, are pushing many Americans into the rental market. That, in turn, is causing rents to skyrocket.

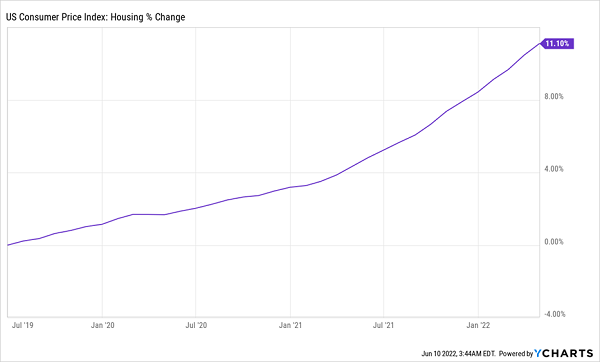

Housing Cost Inflation Accelerating

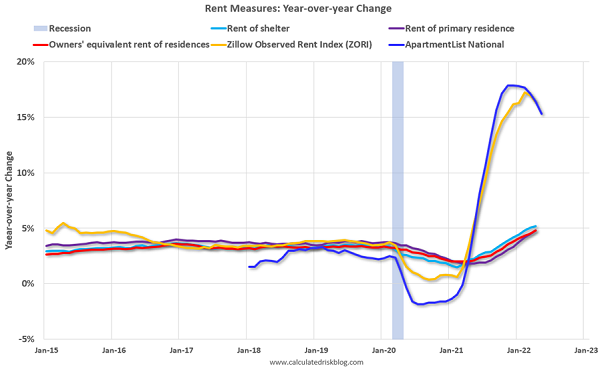

Data from a variety of sources points to the same fact: while government data (through the overall cost of housing—see the chart above) indicates that rent is going up faster than in the past, private companies are showing a more dramatic turn of events, with Zillow and Apartment List (the yellow and dark blue lines below) showing double-digit increases from a year ago.

No matter how you slice it, rent is soaring, and the Federal Reserve is doing what it can to stem the trend—although some would say that by raising borrowing costs for everyone, it’s just making matters worse. But either way, this amounts to sharply rising profits for landlords.

REITs Let You Sidestep the Pricey Housing Market

There’s just one problem for would-be landlords: if they don’t own rental property now, they’ll have to pay elevated prices to buy a home to rent out. So the better move is to buy into a REIT that already rents housing to others. And instead of buying at an elevated price, thanks to the market selloff, we can buy into these firms at a discounted price instead.

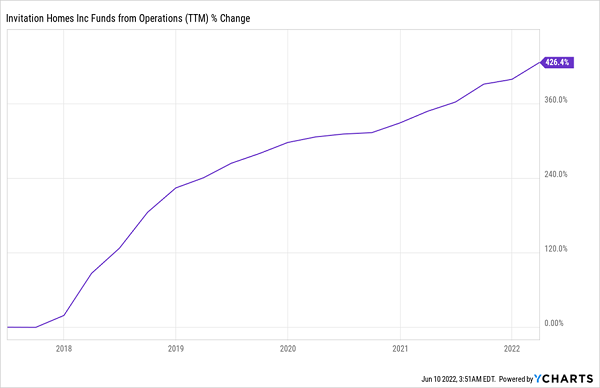

For example, Invitation Homes (INVH) owns thousands of single-family homes across the country, with a portfolio worth over $20 billion. That gives it a lot of diversification, which individual landlords, typically limited to one or a handful of properties in one, or at most two, markets, don’t have. Invitation also has the advantage of having its portfolio professionally managed by a team of real estate pros.

That diversification and management acumen have sharply increased the REIT’s funds from operations (FFO, which is a better measure of REIT performance than earnings per share).

Invitation Homes’ Cash Flow Soars

However, the company’s high, and rising, cash flow is being punished by a market fueled by fear, causing the REIT’s share price to tumble nearly 25% this year.

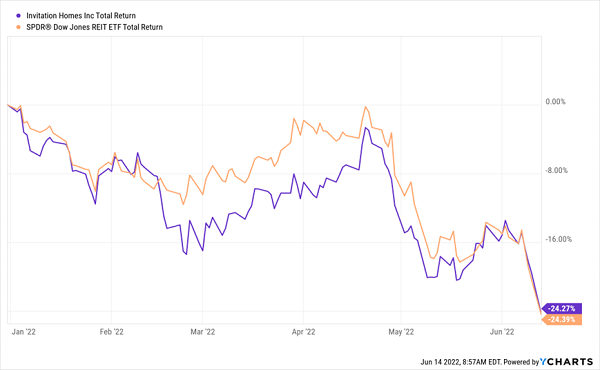

An Irrational Selloff

See how Invitation’s share price has fallen almost exactly as much as that of the benchmark REIT ETF, the SPDR Dow Jones Real Estate ETF (RWR)? That’s no coincidence: Invitation’s selloff has been the result of indiscriminate selling of REITs everywhere, meaning it isn’t the only bargain to be had these days.

For diversification’s sake, buying a fund of REITs over Invitation makes sense, because you’re getting exposure to REITs across various industries, as well as the different management teams taking care of those properties.

RWR is an option, but it’s not one we CEF investors would ever consider, mainly because its 3.4% yield is pretty low by our standards.

A Savvy CEF Play on Rising Rents (That Yields 7.4% Today)

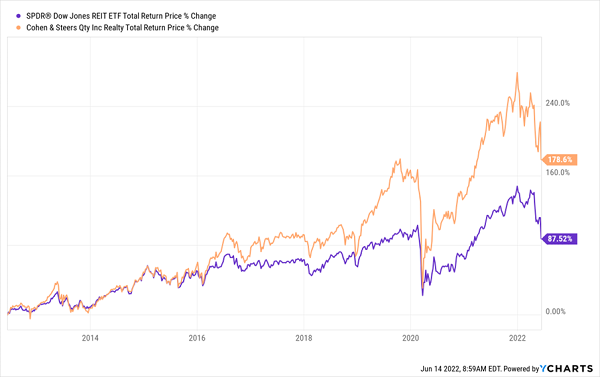

Instead of an ETF, we much prefer CEFs like the Cohen & Steers Quality Income Realty Fund (RQI), which yields a rich 7.4% as I write this. RQI is a major holder of Invitation Homes (it’s one of the fund’s top-10 holdings), plus it holds a range of other types of REITs, like data-center operators and self-storage owners, which are also producing rising FFO. That diversification, plus the REIT’s sharp human managers (Cohen & Steers is a leading name in the CEF space, which helps it attract top talent) has helped it beat RWR over the last decade.

RQI Trounces Its Benchmark

Bear in mind, too, that because of RQI’s high yield, the bulk of the return you see above has been in dividends.

RQI’s outperformance has been rewarded with a big premium to net asset value (NAV, or the value of the REITs in its portfolio) in the past (at one point, its premium was more than 15%). But it currently trades at a 4% discount, although it traded at a premium just a few years ago.

That means we can buy RQI at a discount today, wait for it to go back to the premium it normally has when the market stops panicking, and then sell at a potential profit. In the meantime you can pocket its dividend, which boasts a 7.4% annualized yield and is paid monthly.

— Michael Foster

My 4 Top CEFs Are Built for Volatile Markets (and Pay Monthly Dividends Yielding 8.5%) [sponsor]

Right now, I’m recommending 4 CEFs trading at such big discounts that I fully expect them to do the following:

- Rise 20% in one year if the market bounces from here, as their ridiculous discounts vanish, or

- Hold their own in a flat or falling market, again, thanks to those wide discounts.

Either way, we’ll collect their 8.5% dividends while we wait—and all four of these unsung income funds pay dividends monthly!

I’m ready to share my research on these funds with you now, as well as my full CEF-trading strategy, which I’ve custom-built for panicky markets like today’s. Click here to learn more, and get instant access to the names, tickers and my research on these 4 high-yielding—and monthly paying—CEFs.

Source: Contrarian Outlook