If you have up to $10,000 in cash that you don’t want to invest in the stock market, and if you know you won’t need it for about a year, here’s the no-brainer of all no-brainers:

Buy U.S. Series I Saving Bonds, and get the safest 7% yield in the world!

Yep, I said “7% yield” and “safest” in the same sentence. The U.S. Treasury Dept. might have its problems, but it will never default on these obligations. And the annual interest rate – actually 7.12% for an I Bond bought right now — is beyond delicious.

But wait … aren’t savings bonds, like, so 1940s-1980s?

Well, I did get a bunch of bonds as birthday, Bar Mitzvah and graduation gifts way back when. But today’s I Bonds are a different breed, and they are a great place to park cash or even a way to create a nest egg that you’re guaranteed will be there decades from now.

What Are I Bonds?

Let’s start with what the “I” stands for:

economyria.com

Yes, INFLATION … probably the most-used word in economic circles today.

I Bonds have variable rates that bob up and down with the Consumer Price Index for all Urban Consumers (CPI-U), so a bond-holder is essentially “protected” from inflation. As prices rise on food, clothing, cars, utilities and the like, so do I-Bond interest rates.

Introduced by the Treasury Dept. in 1998, I Bonds combine a guaranteed fixed interest rate that remains the same for the 30-year life of the bond, and the inflation-adjusted rate that I mentioned in the previous paragraph.

The variable rate is set every six months – on the first business day of May and the first business day of November each year.

Currently, the fixed rate is 0.00% and the semiannual variable rate is 3.56%; the latter is doubled to reach the 7.12% figure.

A bondholder gets that rate for a full six months, regardless of when he or she buys it.

treasurydirect.gov

As the above table illustrates, a bond you buy in March would have a 7.12% annual interest rate … and even if the rate is reduced to, say, 6.50% on May 1, you would continue to receive the 7.12% rate until Sept. 1 … at which time it would switch to 6.50% for the next six months.

By the way, I am NOT saying the rate will go down to 6.50%; that was just an example. I don’t know what the rate will be. It could be higher than that or lower than that. It will depend on what the CPI-U is at the time, and we’ll find out the rate for the May-to-October period in mid-April. But if it does fall, it probably won’t be by much because inflation isn’t going to disappear like magic.

Here’s something else that’s pretty cool: Even if you buy an I Bond on one of the last days of a given month, you’ll be credited with an entire month’s interest. So a purchase on March 29 earns all of March’s interest.

Other Good Stuff

- You’ll never lose money on an I Bond. Unlike some bonds that can actually show negative rates, the lowest rate an I Bond holder can receive is 0.00%, even if the U.S. economy is mired in a long deflationary period.

- I Bonds are tax-deferred. You do have to pay federal taxes on interest you earn, but you don’t have to do so until you cash them in. You have control over the timing; you can wait to redeem them when you are in a lower tax bracket (such as after a job loss or during retirement). And there are no state or local taxes on I Bonds.

- They can be part of a college savings plan. Depending on your income level, you might not have to pay federal taxes on an I Bond’s interest if it’s used to pay college tuition and fees for yourself or a dependent. For more on that, see HERE.

- It’s easy to set up an account, link a bank and start buying I Bonds online at treasurydirect.gov. The site also tracks each bond’s progress within each account over the months and years and decades.

Nothing’s Perfect

As great as all the “pros” of I Bonds are, there are “cons,” too.

- There is a limit of $10,000 per person per year. So if you’re sitting on $200K in cash and thinking you’re gonna get this great 7.12% rate on all of it, think again.

- There are no joint accounts, so if you and your partner want to max out your annual I Bond buys to a total of $20,000, each of you would need to open and fund an account with $10K. It’s an extra step, but it’s really not much of a hassle. (I wouldn’t buy an I Bond for a minor child for the reasons explained HERE, but it is possible.)

- You can’t hold I Bonds in an IRA or other tax-deferred account.

- You must hold an I Bond for at least a year. So while the bonds can be viewed as a place to park cash, they aren’t a super-short-term vehicle. If you’ll need the dough in a few months, sorry, but you’ll have to stick with low-rate bank accounts.

- You will be penalized the last 3 months of interest if you redeem an I Bond after one year but before you’ve held it for five years.

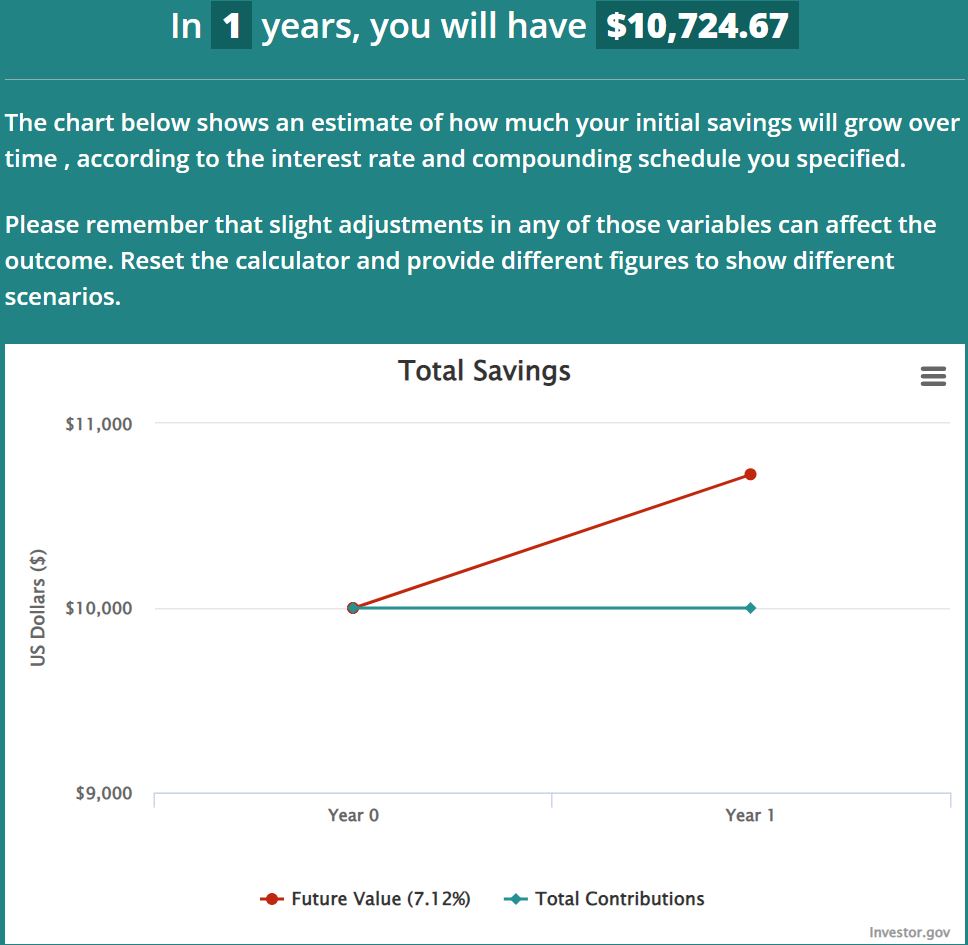

That penalty might sound severe, but it’s really not that bad. For example, I bought a $10K I Bond last week. For the sake of keeping it simple, let’s say the rate renews at 7.12% this spring, so I’ll earn that rate for 12 months. Because interest is added monthly and compounded semi-annually, the bond would be worth about $10,725 after one year.

investor.gov

If I redeemed it then, I’d be penalized the last three months of interest, about $183 … so my $10,000 investment will have turned into $10,542. That’s still an annual rate of 5.35% — far better than any savings account, certificate of deposit or other safe investment out there.

fdic.gov

How Inflated Will Inflation Be?

One more thing that some might view as a “con,” but I view simply as a fact: The current rate will not be around forever, and might not be around for very long at all.

The 7.12% I Bond inflation rate (as represented in the following chart by the 3.56% rate for six months) is at its highest since I Bonds debuted in 1998 — and it’s more than double the next highest rate over the last many years, when inflation has been tame.

treasurydirect.gov

With inflation now being seen as the biggest threat to the U.S. economy, the Federal Reserve is expected to raise its key interest rate at least three times in 2022 and to curtail other measures it had taken to boost the economy during the earlier waves of the COVID-19 pandemic. If the Fed succeeds, it will reduce inflation — and the inflation rate of I Bonds will follow.

As you can see in the last line of the above table, the inflation rate was only .08% for the six-month period beginning on May 1, 2016. I Bonds paid out only 0.18% interest over that stretch. It could happen again eventually.

Long-Term View

An I Bond will continue to accrue and compound interest for 30 years, so it’s a solid way to safely build inflation-protected, tax-deferred savings for the long term.

I’ll provide the best kind of example: my own real-world, real-money experience.

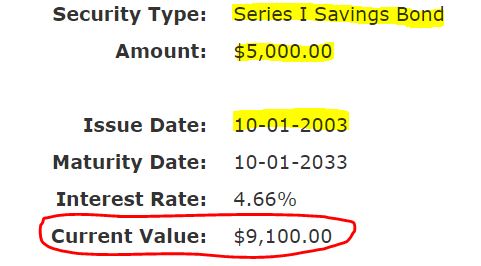

On Oct. 30, 2003, I bought a $5,000 I Bond. I had some money lying around and I had read that it would be a good way to make more than the prevailing bank interest rates.

At the time, the I Bond fixed rate was 1.1%. The combined annual rate, including the variable inflation rate, was 4.66%. Today, that bond is worth $9,100.

treasurydirect.gov

You can see that even though I bought the bond on Oct. 30, the “Issue Date” is listed as 10-01-2003. As I said earlier in this article, no matter when in a month an I Bond is purchased, you get the full month’s interest.

In growing from $5,000 to $9,100, my gain over these last 18-plus years has been 82%. Had I invested the money in an S&P 500 Index fund, its total return would have been more than 500%. But that’s comparing apples to orangutans. I wanted something completely safe to help balance out a stock-heavy portfolio.

I mean, we just as easily could compare how I Bonds have fared these last 18-plus years to stocks like PG&E (PCG), General Electric (GE) and American International Group (AIG).

So sure, this bond didn’t make me rich. But at least it isn’t worth significantly less now than what I paid for it — as an investment in GE would have been.

Gaining 82% with a completely safe investment is pretty darn good, especially considering how low inflation was during most of the time I’ve held my bond. It’s why I’m not overly concerned with how new Fed policy could affect future returns.

Unless I redeem it, my $5,000 I Bond will keep accruing and compounding interest until 2033. Its fixed rate hasn’t changed from the original 1.1% — and it never will. Its composite rate for the current 6-month period, meanwhile, is a lovely 8.26%.

treasurydirect.gov

And of course, if I do redeem that bond, there will be no penalty because I have held it for far longer than five years.

Other Things To Consider

There are numerous strategies about when to buy and redeem I Bonds to maximize their return.

- You could buy one next week and then cash it in on Jan. 2, 2023. Even though you technically would have owned it only 11 months and a handful of days, that would count as a full year for redemption purposes.

- If you’re using an I Bond as a short-term investment, getting in as early as you can makes sense because that means you’ll be able to cash out earlier. If you’re using it as a long-term investment, the start date isn’t as important.

- You could wait to hear what the rate for the next six months will be, and see whether the current or future rate is better. If the latter is higher than 7.12%, you could put off the purchase until May.

- It can take a day or three for an I Bond purchase to go through, especially if you’re just setting up an account for the first time. So if you want to own a bond by, say, April 30, I’d strongly recommend initiating the process by April 26 or 27.

- There is no need to make a $10,000 purchase all at once. You could buy half now and the other half later in 2022. For that matter, you could build your I Bond investment week by week, $25 or $50 at a time.

treasurydirect.gov

If you get a tax refund, it’s also possible to use it to buy up to $5,000 in paper I Bonds. You’d need to fill out IRS Form 8888 and include it when filing your federal return.

Wrapping Things Up

Since the 7.12% rate took effect last Nov. 1, my wife and I have bought three $10,000 I Bonds — one for each of us in December, and mine for 2022 last week. We might wait until we see what the May rate change will be before deciding when my wife should purchase her 2022 bond, but we could opt for earlier.

Regardless, we absolutely will buy $20K worth of I Bonds this year. There aren’t many no-brainers in the investing universe, so we’re not about to short-change a sure thing.

NOTE: I also manage two real-money portfolios for this site: The Income Builder Portfolio, which largely follows the Dividend Growth Investing strategy, can be seen HERE; and the Growth & Income Portfolio, filled with “growthier” stocks, is HERE. In addition, I make videos for our Dividends And Income Channel on YouTube; check out the most recent one HERE.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com