There are few givens in life, but here’s one: Realty Income (O) markets itself as The Monthly Dividend Company, so the folks there will do everything in their power to pay the dividend every month and grow it every year.

Still, even though it wasn’t a huge surprise, it sure was nice to see this press release last week:

realtyincome.com

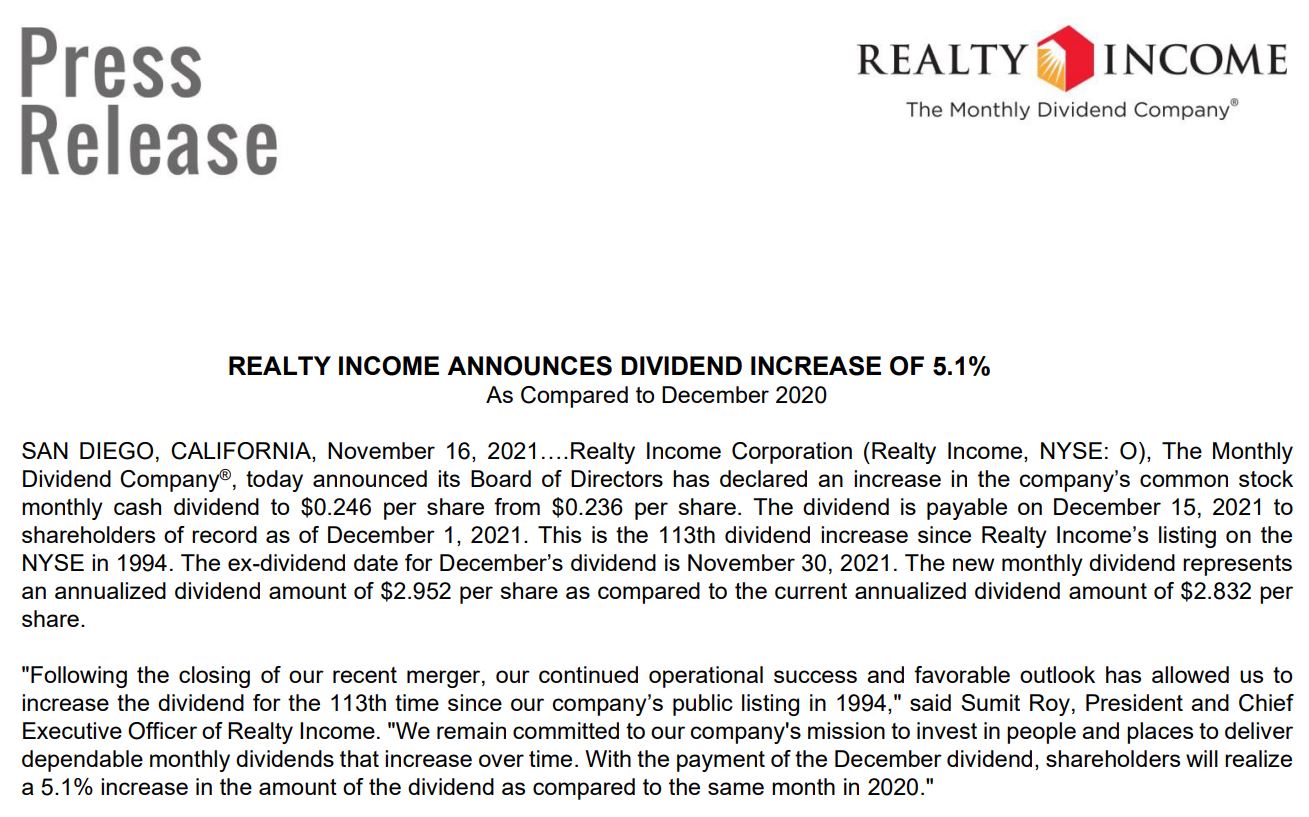

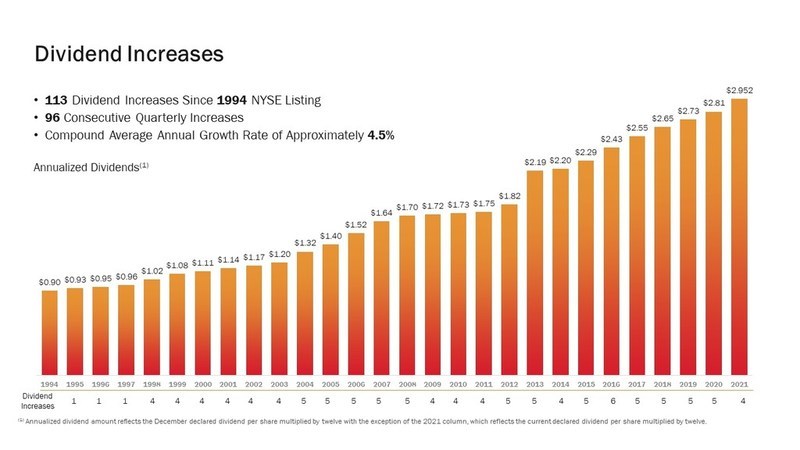

That’s right: Since it went public 27 years ago, Realty Income has increased its dividend 113 times. This latest raise — 4.2% quarter-over-quarter, and 5.1% year-over-year — marks the 96th consecutive quarter in which the company has lifted its payout to shareholders.

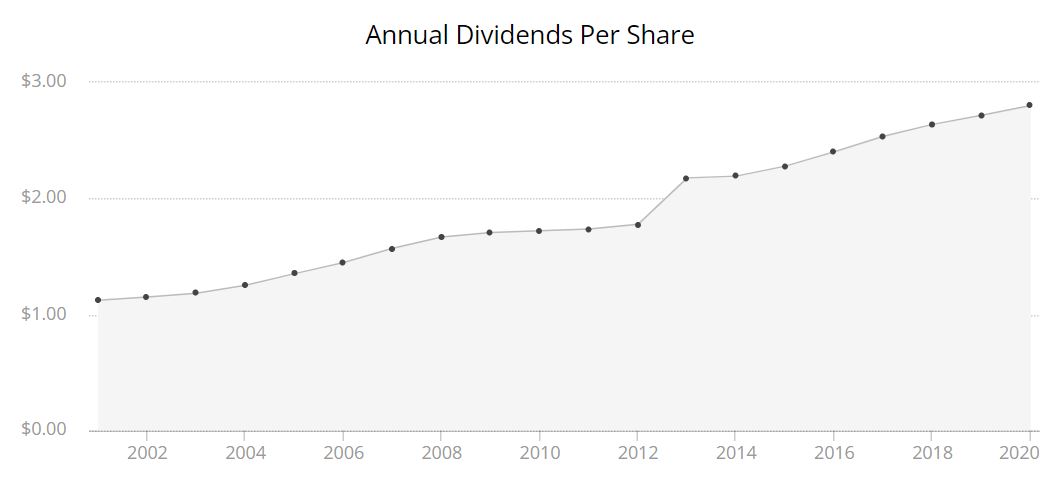

As a guy who’s into Dividend Growth Investing and as the caretaker of the Income Builder Portfolio, I always like seeing this kind of stairway to income heaven:

realtyincome.com

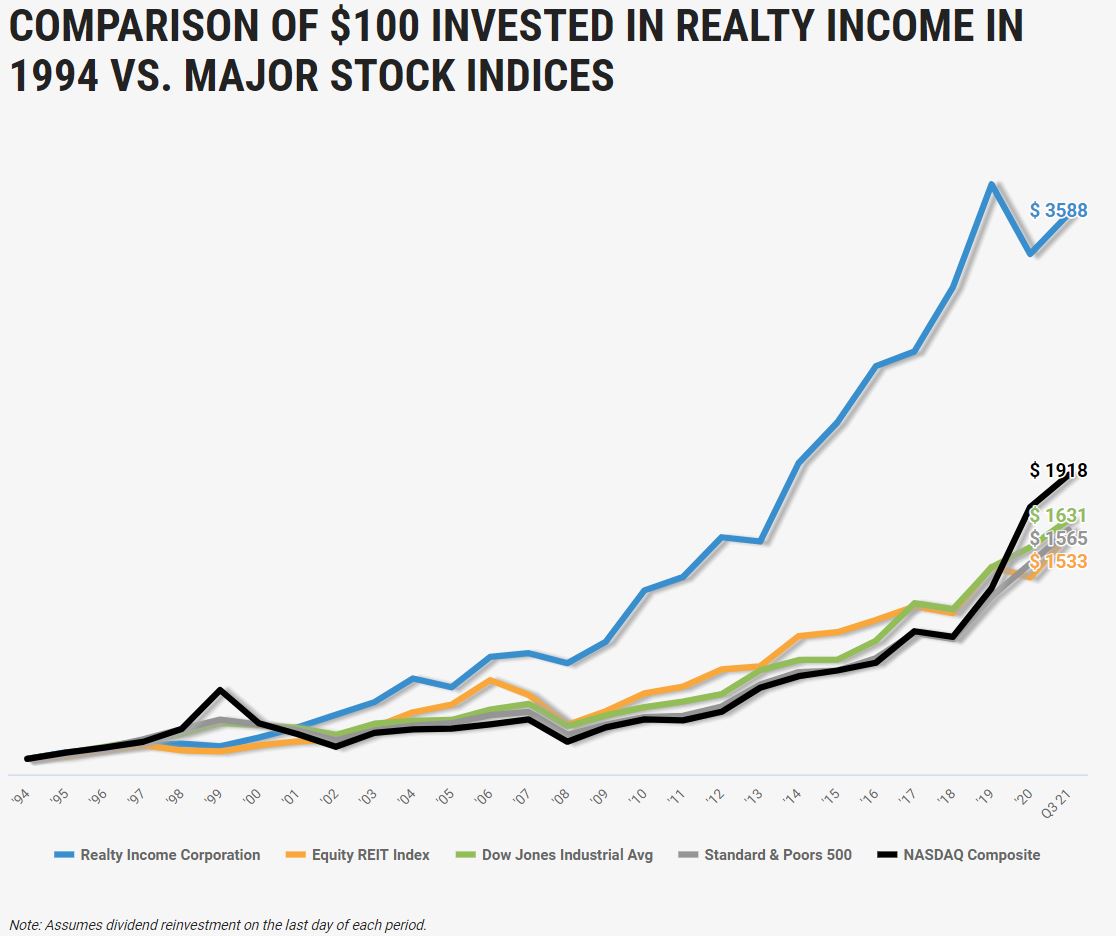

And yet, Realty Income is about so much more than the income it produces. It is a high-quality real-estate company that is one of the leaders in its industry, and it is a stock with an enviable long-term history of outperformance.

realtyincome.com

In this article, I’ll talk about Realty Income’s business, why I’ve selected it several times for the IBP, and how it might interest those who use DGI as an investing strategy.

A History of Growth

Realty Income is a real estate investment trust (aka, REIT) that was founded in 1969, with its first property being a single Taco Bell restaurant.

The company began trading on the New York Stock Exchange in 1994. Within two years, Realty Income received investment-grade ratings from the leading credit services.

The business continued to grow, and by 2011, O was acquiring $1 billion of new property annually.

realtyincome.com

It paid $3.2 billion to acquire REIT rival American Realty Capital Trust in 2013. Two years later, Realty Income was added to the S&P 500 Index.

In 2016, O surpassed $1 billion in annual rental revenue for the first time.

realtyincome.com

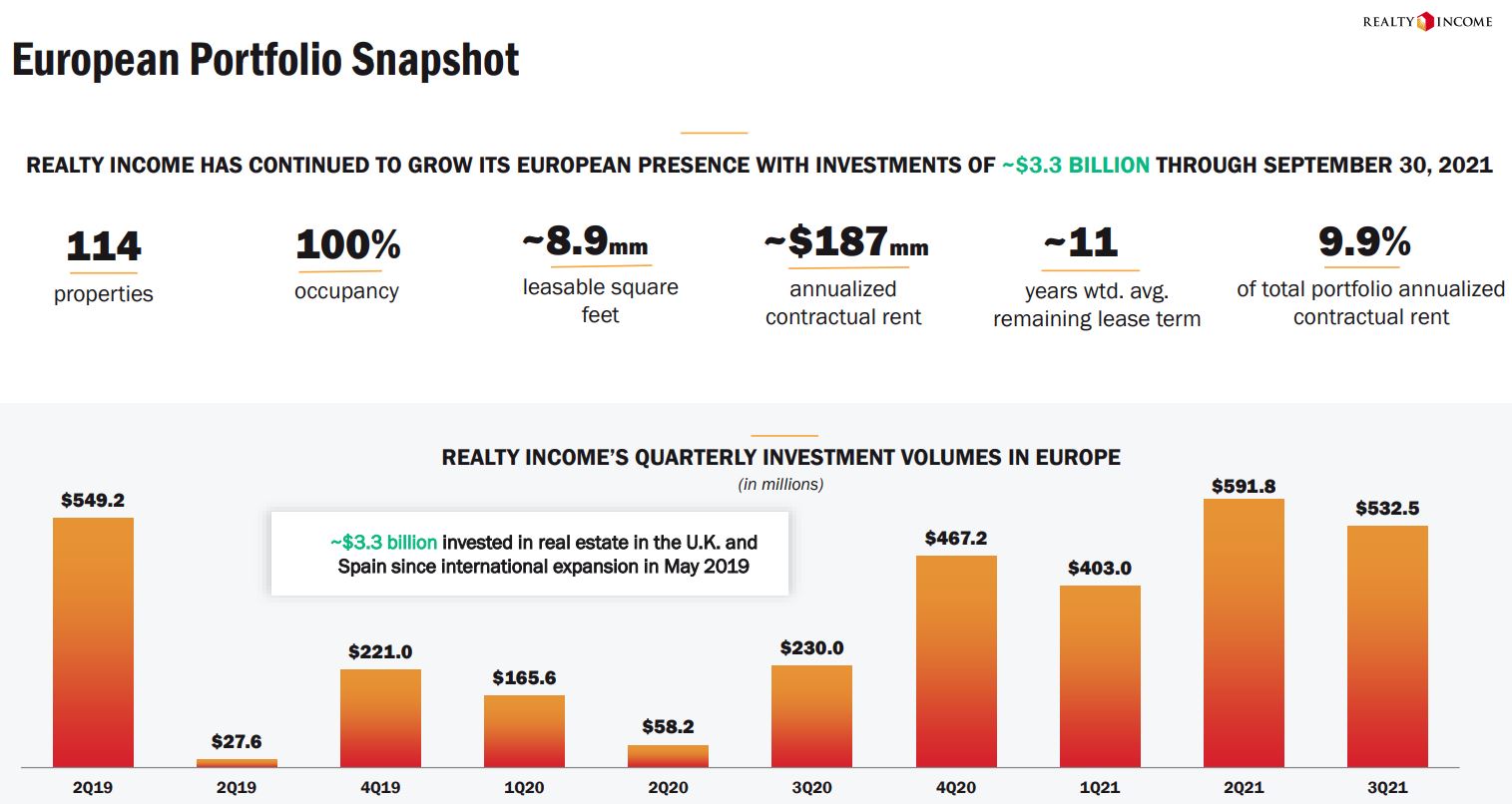

The company expanded its operations into the United Kingdom in 2019, when it acquired a dozen properties that were entered into long-term, net-lease agreements with the Sainsbury’s grocery chain.

That was the start of a $3 billion-plus investment in Europe, covering 114 properties.

realtyincome.com

In 2020, after raising its dividend for the 25th consecutive year, Realty Income became a Dividend Aristocrat — making it one of only three REITs to have achieved that lofty status.

On Nov. 1 of this year, the company completed an $11 billion acquisition of competitor VEREIT. Realty Income then spun off many of its office assets into a new company, Orion Office REIT (ONL).

The Income Builder Portfolio received shares of the new company and we promptly sold them. More on that later.

Realty Income’s Business

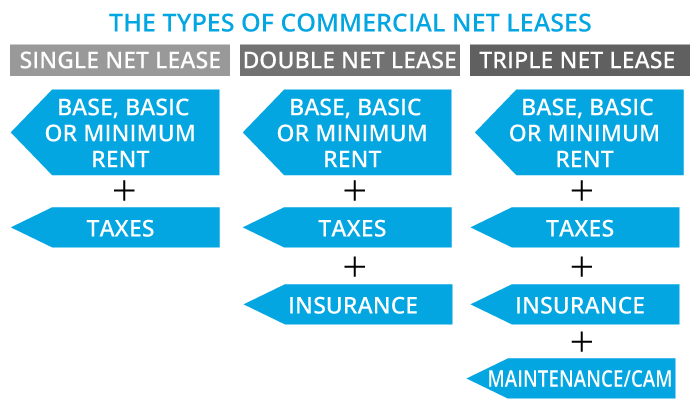

The company buys commercial real estate leased to clients under long-term agreements.

Most of its contracts are structured as triple-net leases. This is a great business model for Realty Income — and for shareholders — because it makes the client responsible for each property’s operating expenses, such as maintenance, insurance and taxes.

cressblue.com

That structure reduces a REIT’s exposure to rising expenses and preserves a predictable cash-flow stream — a stream that Realty Income uses to pay its monthly dividend.

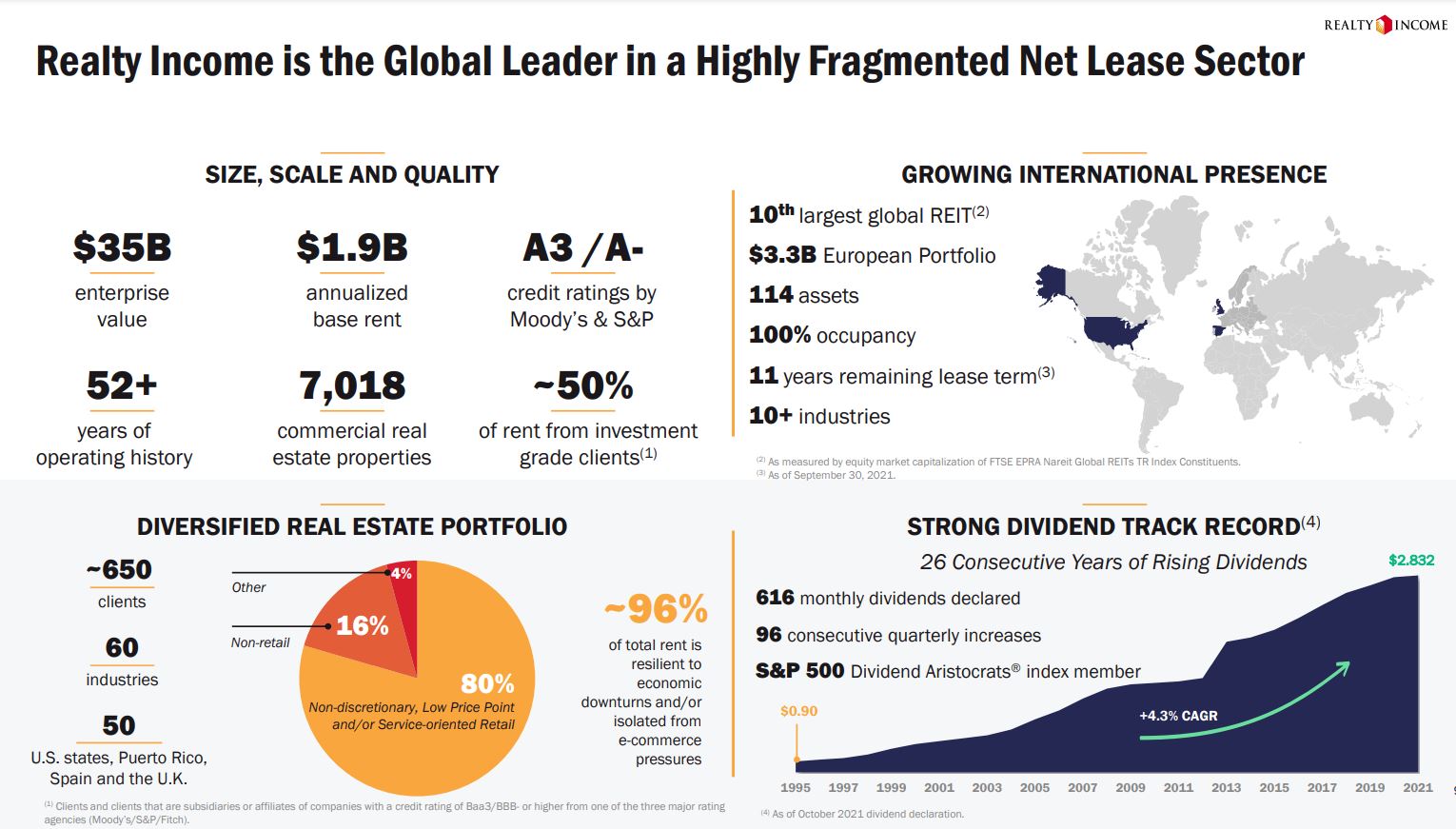

Realty Income owns more than 7,000 properties, with about 650 clients operating in 60 industries. It has properties in every state, as well as in Puerto Rico, the United Kingdom and Spain. Most of those properties are freestanding buildings in prime locations.

realtyincome.com

Realty Income has grown by being a serial acquirer.

The company’s management team gets high marks from analytical firm Morningstar, which said:

We give Realty Income an Exemplary capital allocation rating. In our opinion, the company’s balance sheet is sound, its capital investment decisions are fair, and its capital return strategy is appropriate. …

We attribute most of Realty Income’s growth to the skill of its management team. Even though the company’s business drives only 1% internal growth per year, the company has quintupled in size and produced a total return on its common equity well above the U.S. REIT average since the end of 2009. This growth is a result of management’s ability to consistently deliver accretive acquisitions. …

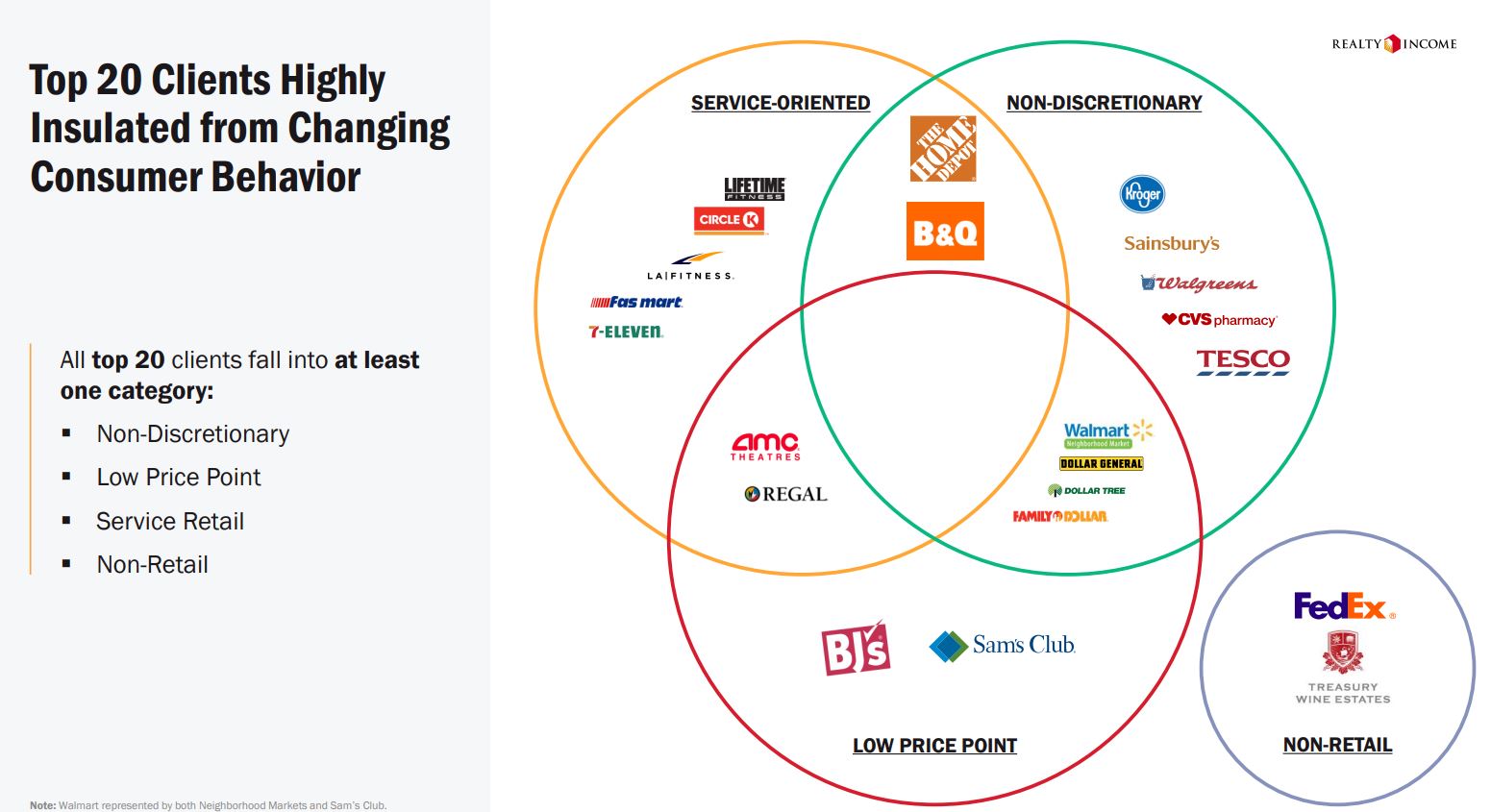

What also impresses us is management’s ability to significantly increase the portfolio’s quality over the past decade. … Realty Income has shifted its exposure away from economically sensitive retail segments like full-service restaurants, which represented over 21% of its rent in 2009, to retail segments that are much more insulated from economic downturns and e-commerce.

Very few of Realty Income’s tenants are at risk from the “Amazonification” of things.

realtyincome.com

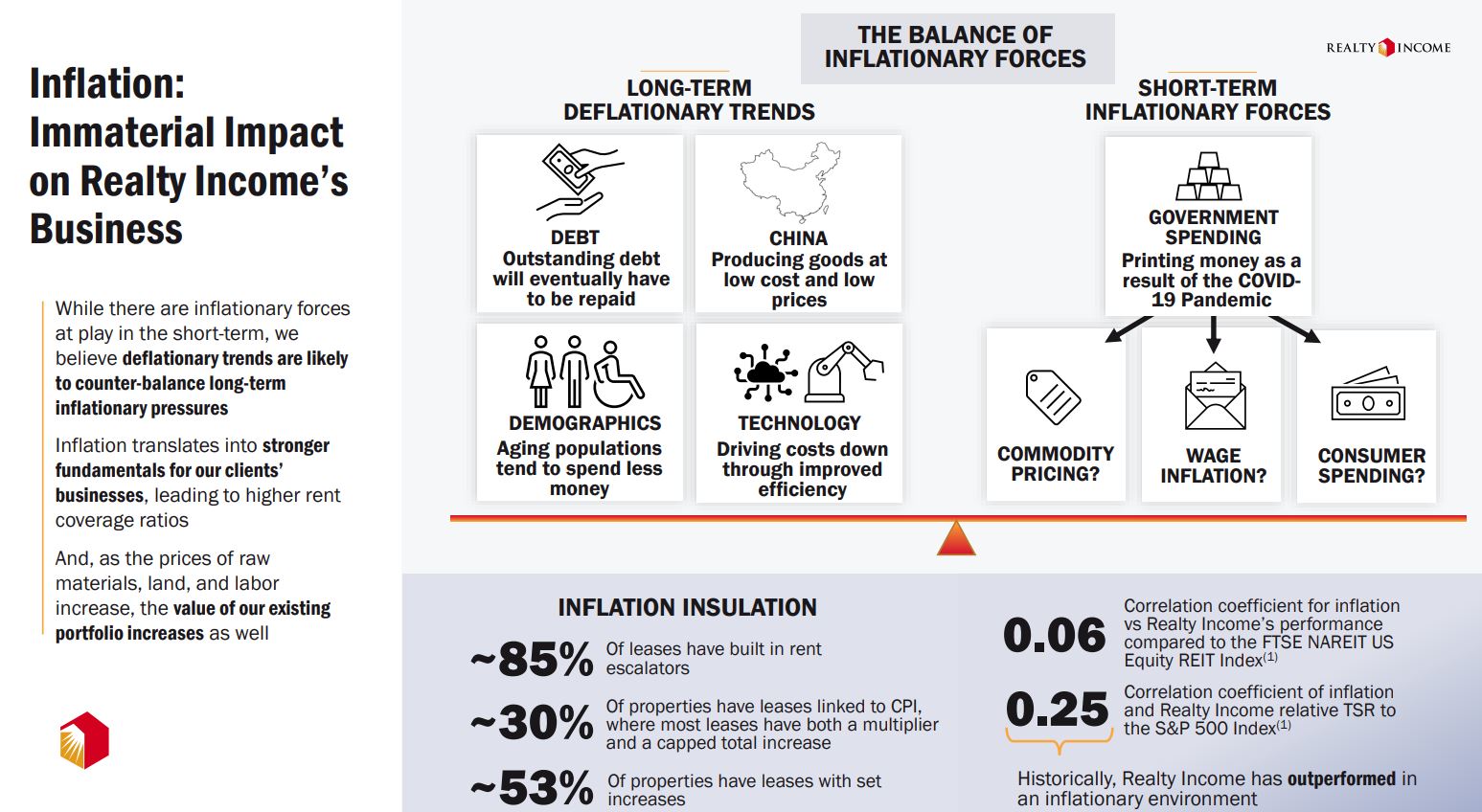

In addition to being less affected by e-commerce than most other REITs, Realty Income makes a convincing argument that it will be less affected by one of today’s economic buzzwords: Inflation.

Historically, the stock has performed well during inflationary times, in great part because the company’s leases have built-in rent escalators.

realtyincome.com

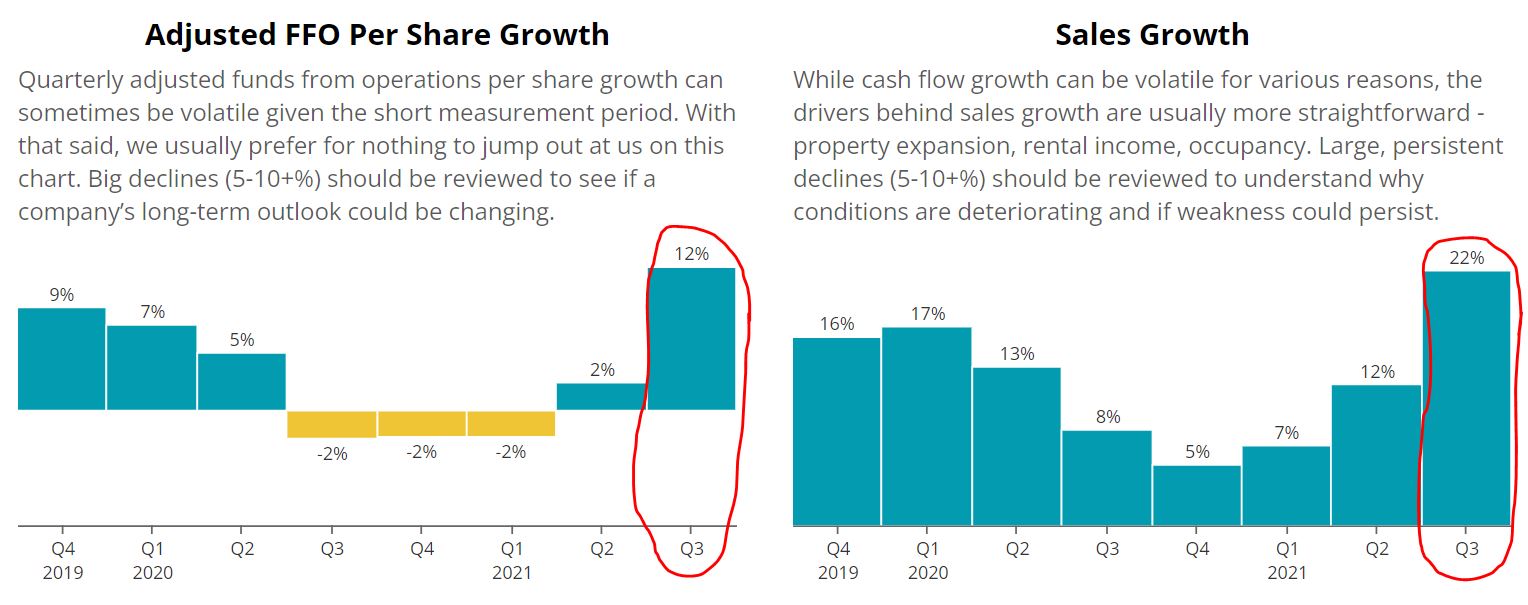

Realty Income’s main trouble spots the last couple of years were its theater tenants, which were severely hurt by shutdowns during the COVID-19 pandemic. During its third-quarter earnings report on Nov. 1, however, O reported that those tenants were able to pay 99.6% of the rent they owed.

As a result, overall rent collection saw significant quarter-over-quarter improvement and is now at almost 100%.

Rather than earnings, a REIT’s performance is measured by adjusted funds from operations … and Realty Income had a stellar third quarter, with 12% growth. At 22%, sales growth also was outstanding.

SimplySafeDividends.com

Robust growth is expected to continue into next year.

SimplySafeDividends.com

From a quality standpoint, Realty Income checks so many boxes.

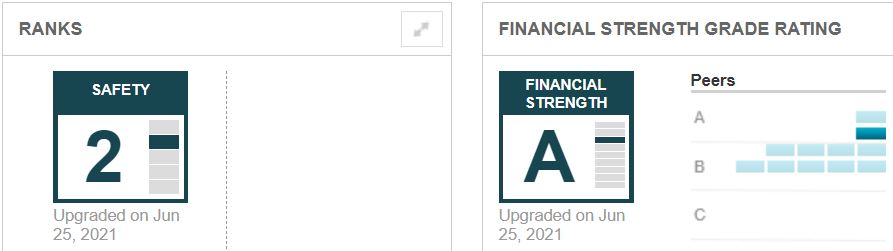

In addition to the Exemplary mark that O gets from Morningstar for capital allocation strategy, the company has received a solid A- credit rating from Standard & Poor’s, and good grades from Value Line for relative safety (2) and financial strength (A).

valueline.com

Let’s Talk About Dividends

Like all REITs, Realty Income is required by U.S. law to pay at least 90% of its taxable income in the form of dividends every year. That mandate has made REITs quite popular among Dividend Growth investors.

Realty Income wears that commitment like a badge of honor.

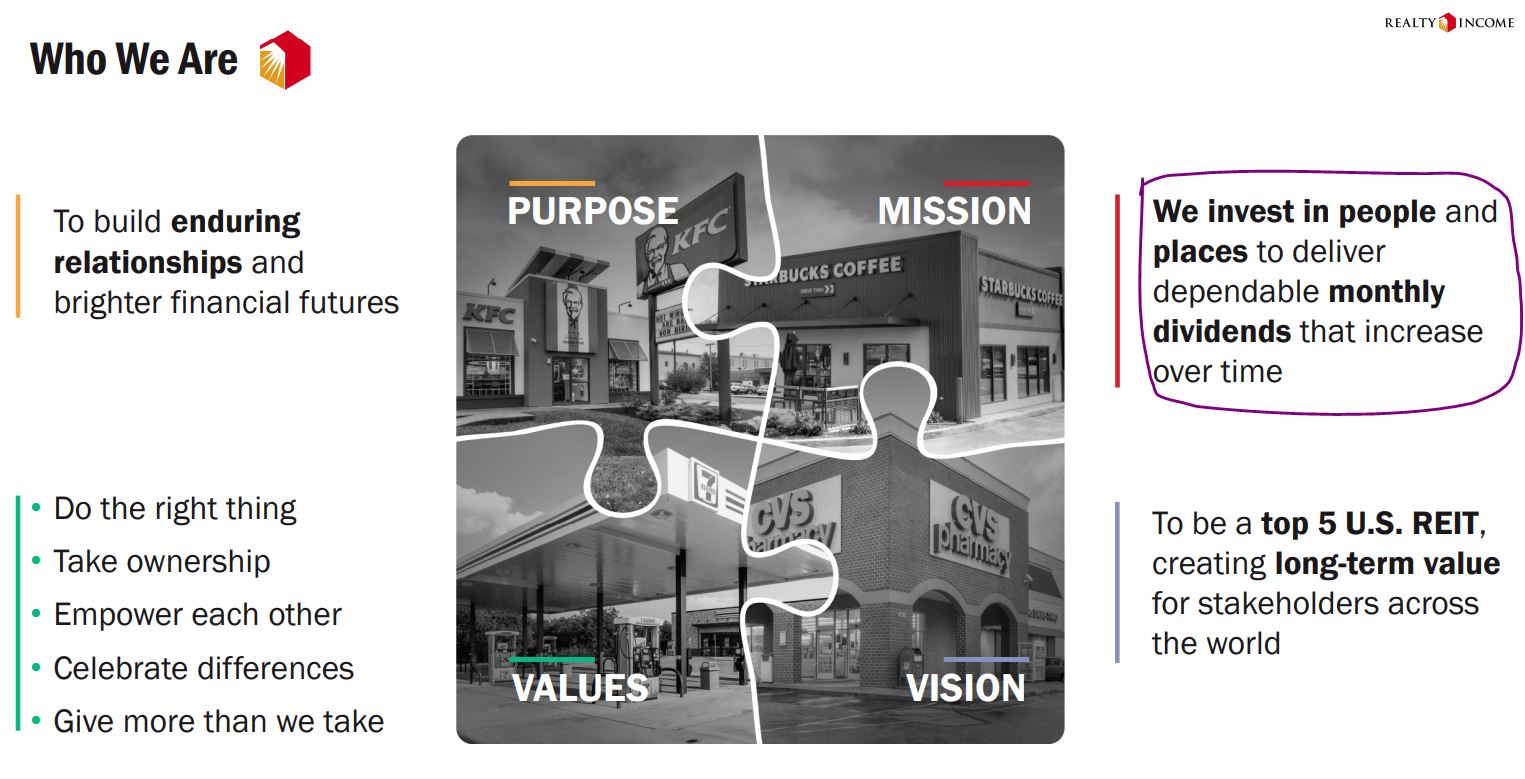

For example, in its November investor presentation, the word “dividend” was mentioned 25 times. The “Who We Are” page included the statement: “We invest in people and places to deliver dependable monthly dividends that increase over time.”

realtyincome.com

And the next page described the commitment to the dividend as “sacrosanct” — a word whose synonyms include “holy,” “hallowed,” “sacred,” and “untouchable.”

realtyincome.com

I have learned to never say never, so I won’t claim Realty Income will never cut its dividend. I’ll just say I’m very confident that the company is highly unlikely to reduce or eliminate the payout for as long as I own shares of the stock.

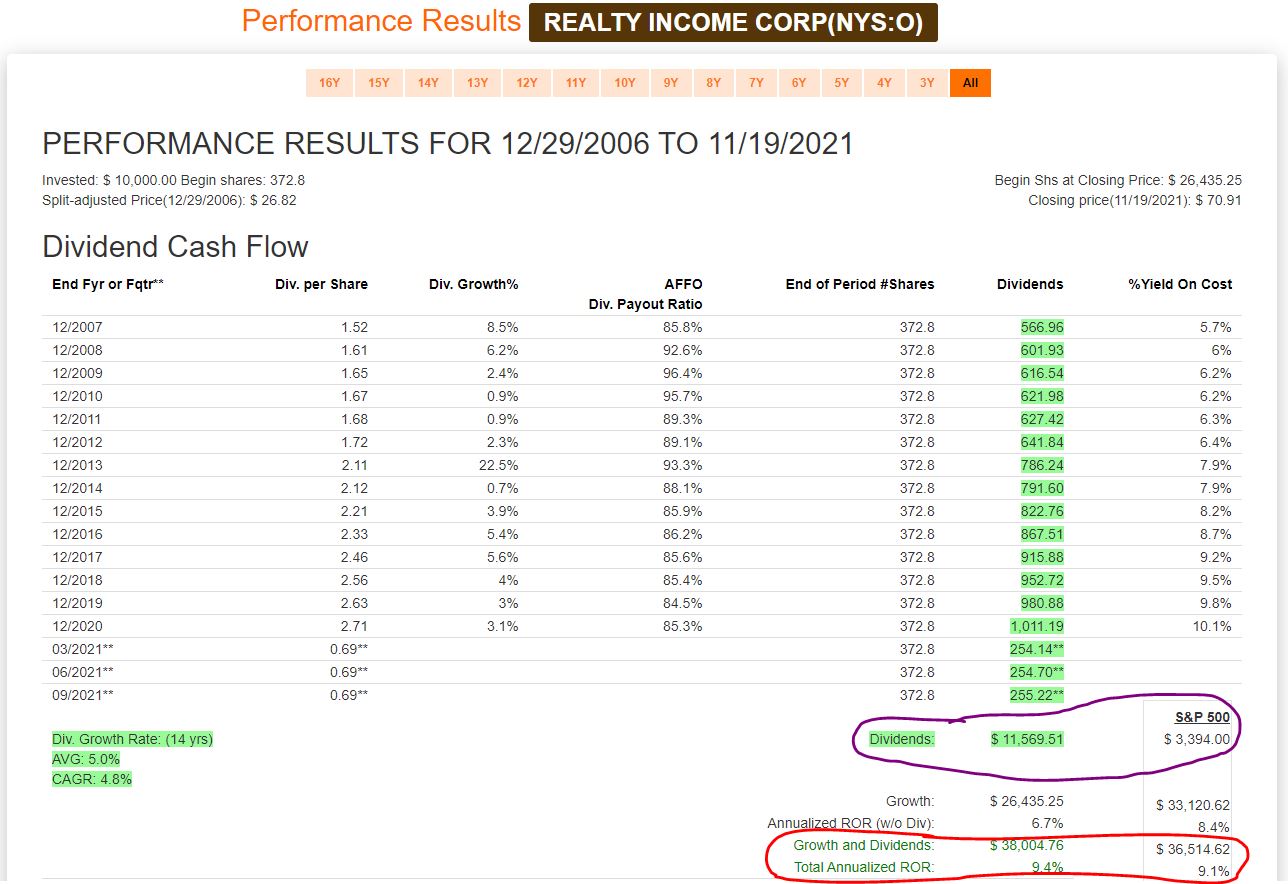

The dividend has made it possible for O outperform the S&P 500 Index over the long term, as this FAST Graphs image shows:

fastgraphs.com

From its marketing campaign to its logo to just about every discussion it has, Realty Income makes sure everybody knows it pays its dividend monthly.

Some DGI proponents love monthly payers, but it’s not really a factor for me. I would own Realty Income in my portfolio and would have selected it for the IBP even if its dividend was paid quarterly, as is the case with all of our other positions.

Realty Income has been a slow and steady dividend grower — averaging 4% annual growth the last 5 years, 5% the last 10, and 5% the last 20. Its dividend gets a “safe” 70 score from Simply Safe Dividends.

SimplySafeDividends.com

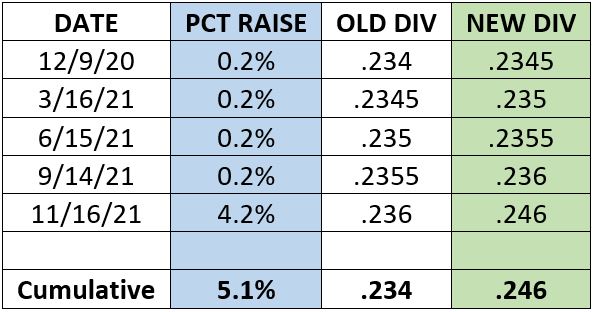

The company tends to issue small raises every few months for several consecutive quarters before making a much larger increase — as illustrated in this table of the past year’s dividend hikes:

At the new annual dividend amount of $2.952 per share (.246/month times 12), Realty Income’s yield has moved above the 4% mark.

Valuation Station

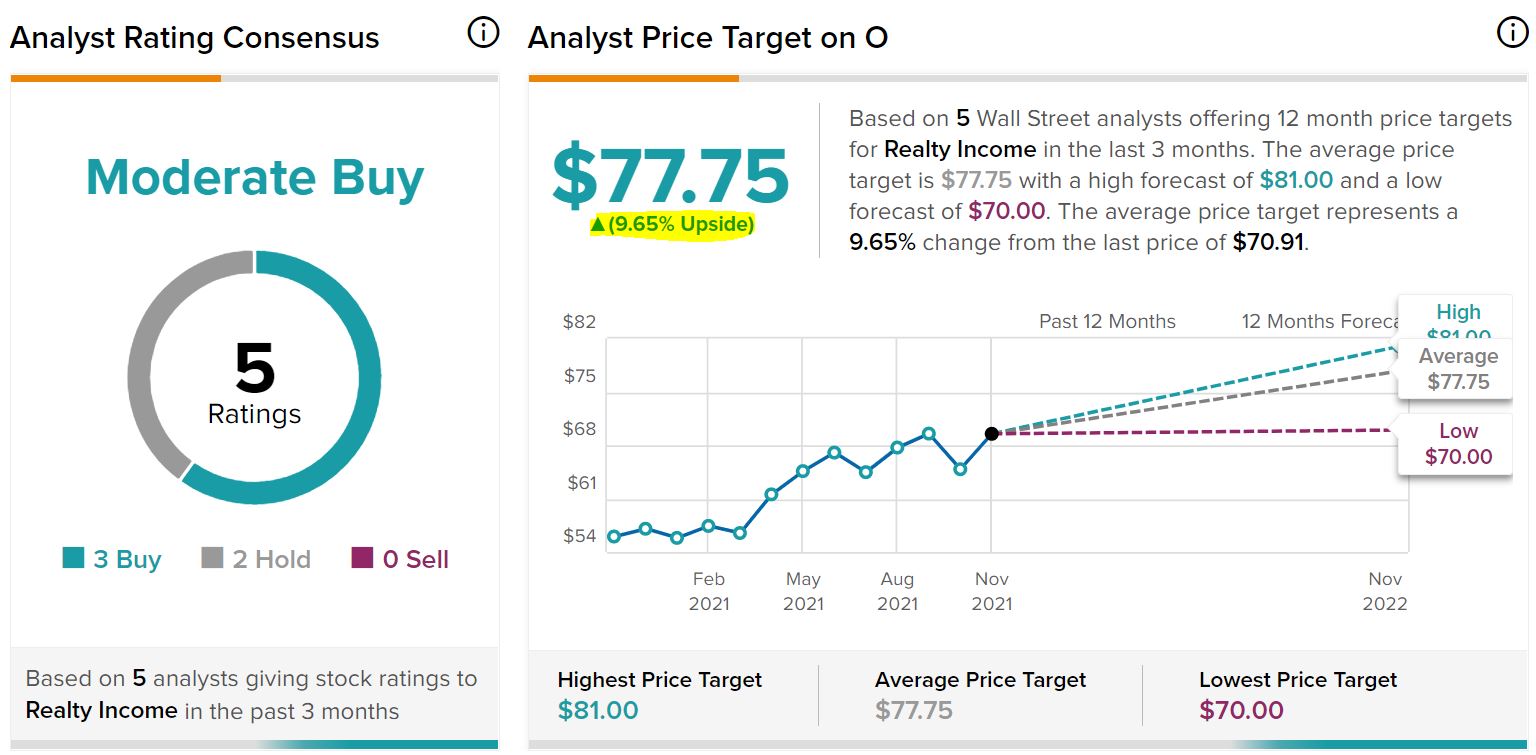

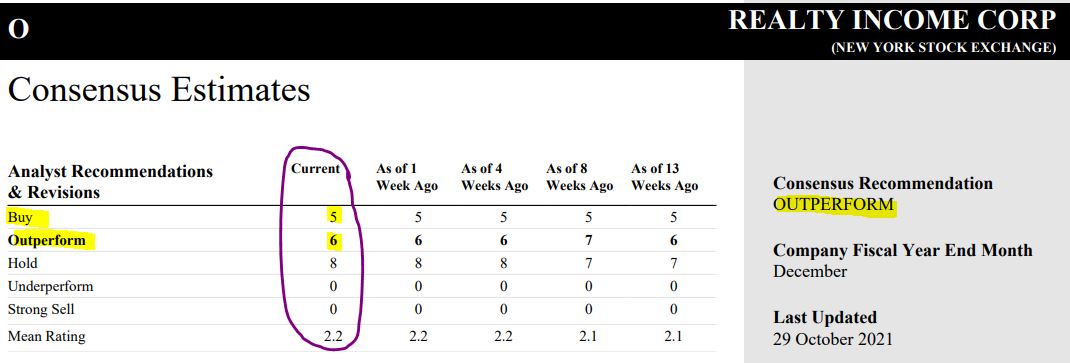

Analysts tracked by TipRanks consider O to be a “moderate buy,” with a price target that offers an upside of about 10%.

tipranks.com

Reuters surveyed 19 analysts, with 11 giving O either a “buy” or “outperform” rating.

Reuters, via schwab.com

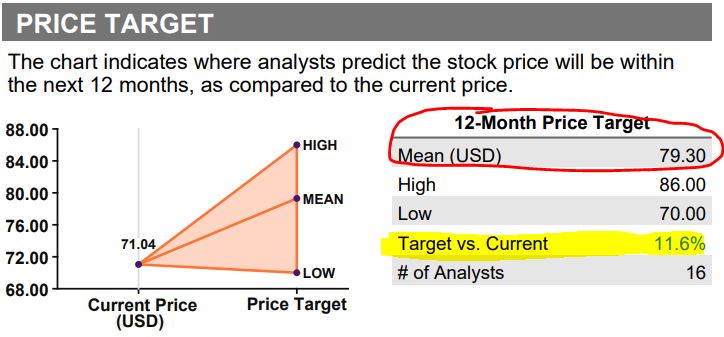

Refinitive collected data from numerous analysts, whose mean price target is more than $79.

Refinitiv, via fidelity.com

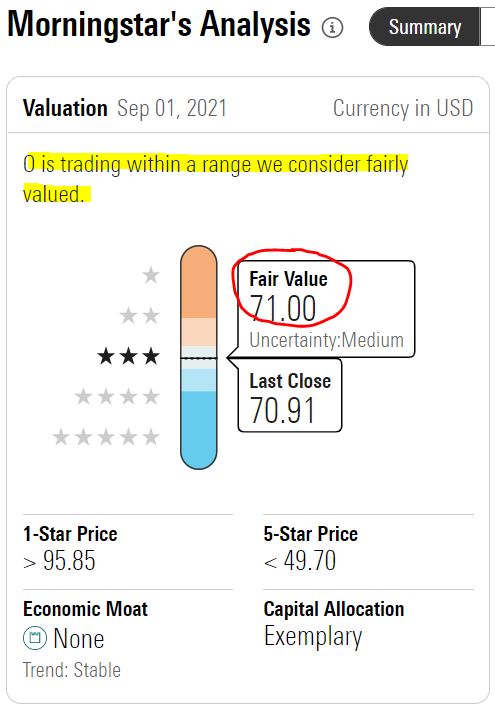

Morningstar considers Realty Income to be fairly valued.

morningstar.com

Value Line says O could see more than 50% price appreciation over the next 3-5 years, but Value Line’s shorter-term forecast doesn’t envision much of a gain.

valueline.com

Citing expected continued high occupancy, the quality of Realty Income’s properties and the consistency of its rent collections, CFRA calls O a “buy” with a $78 target price.

CFRA, via schwab.com

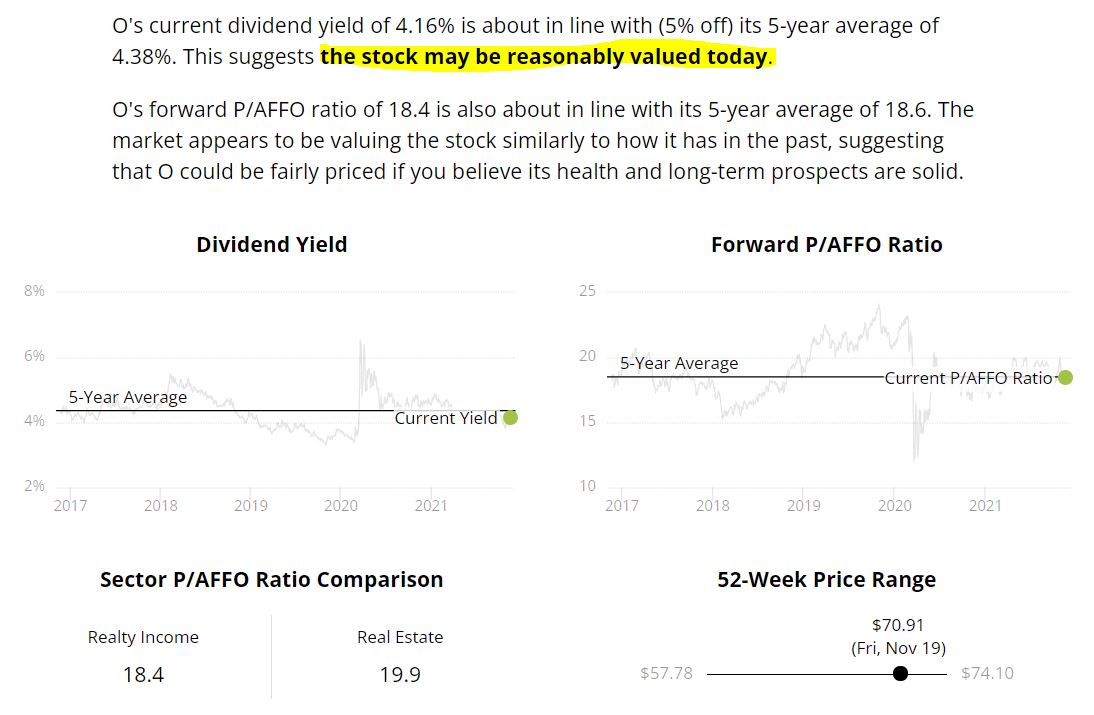

Simply Safe Dividends likes to use current and historic yield to determine a company’s valuation. By that measure, as well as price/AFFO, SSD believes O is reasonably valued.

SimplySafeDividends.com

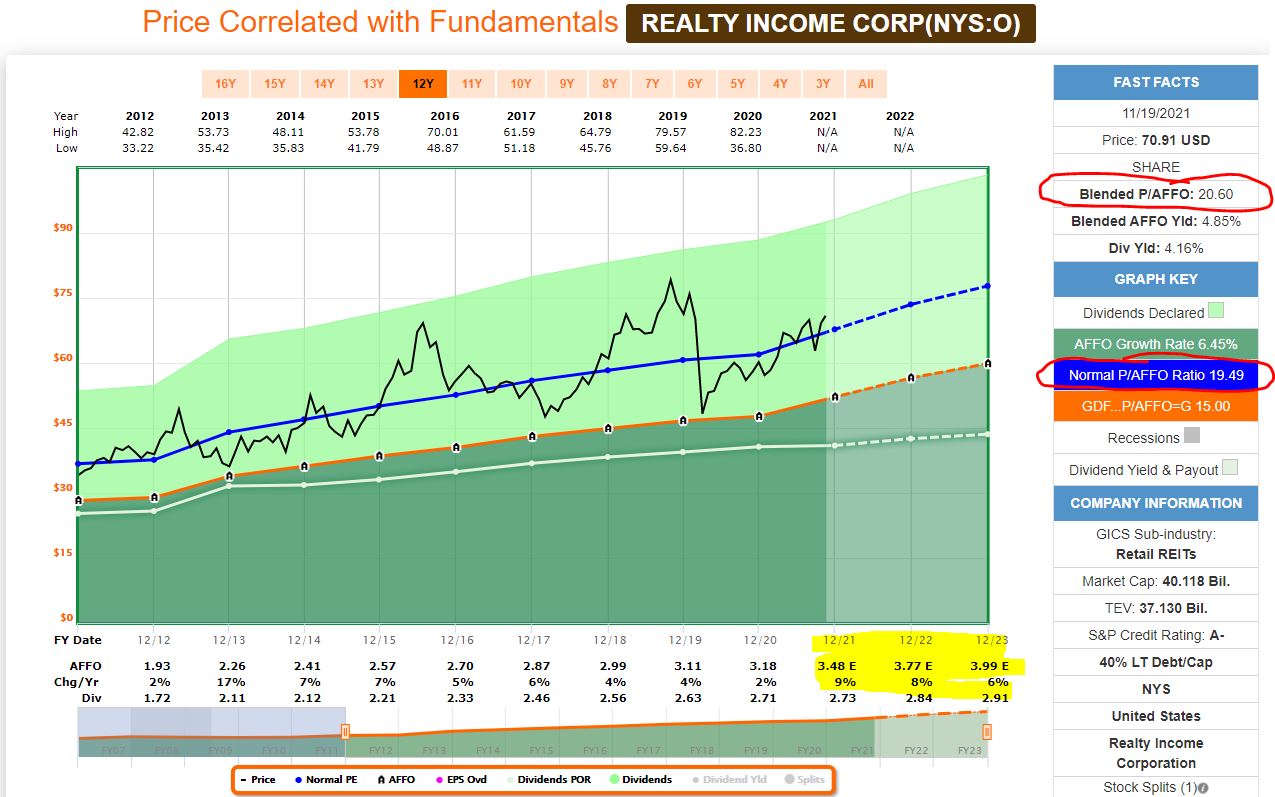

Looking at FAST Graphs, Realty Income’s current “blended P/AFFO” is just a little higher than its 10-year norm, suggesting the stock is fairly valued to slightly overvalued.

fastgraphs.com

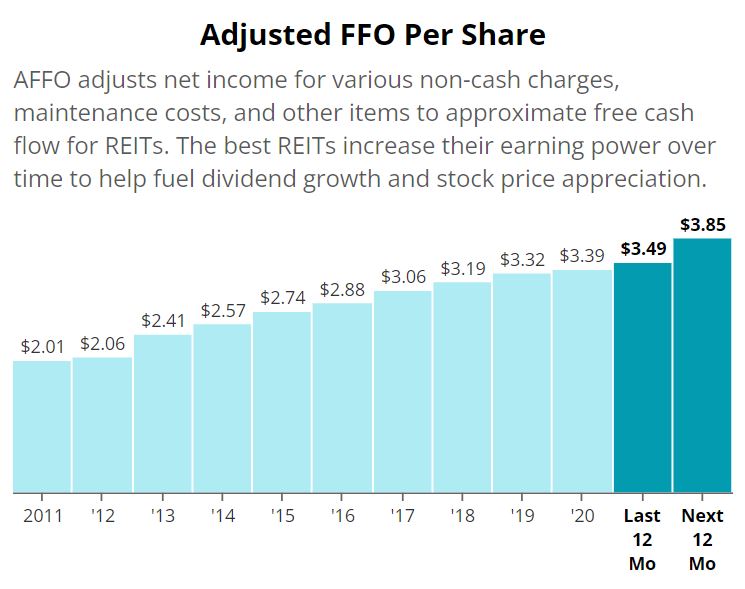

The yellow highlighted area of the above graphic indicates Realty Income’s expected AFFO growth for the next three years. The annual average of 7.7% is quite good for a slow-and-steady REIT.

The IBP Buys

On Monday, Nov. 22, I executed a purchase order for about $497 worth of Realty Income on behalf of this site’s co-founder (and Income Builder Portfolio money man) Greg Patrick.

I split the rest of Greg’s $1,000 semi-monthly allocation between two of the IBP’s smaller positions: defense contractor Northrop Grumman (NOC); and health-care conglomerate CVS Health (CVS).

I wrote about CVS and NOC earlier this year when I initiated the positions; investors interested in more information about those high-quality, dividend-growing companies should check out my February article about Northrop HERE, and my June piece about CVS Health HERE.

Here is some updated valuation-related material on the two companies, both of which look fairly valued to somewhat undervalued:

In addition, I sold the 2 shares of Orion Office REIT that the IBP received as part of Realty Income’s spin-off, and I used the $44 proceeds to buy another .6233 of a share of O. I felt the quality of Orion’s holdings wasn’t up to Realty Income’s standards, and I decided I’d rather the portfolio simply have more O.

The portfolio also received $13.02 cash in conjunction with the spin-off, and I invested that in Realty Income, too, buying .1836 of a share.

After all of those transactions, the IBP now owns 33.9803 shares of O, which is expected to bring about $100 in annual income into the portfolio. We also own 14.8224 shares of CVS and 4.8313 shares of NOC, with each position projected to generate about $30 of income over the next year.

Wrapping Things Up

The table showing all 45 Income Builder Portfolio positions can be seen on our home page HERE.

We regularly present videos about all of our IBP buys. Check out the one about my first November selection, toolmaker Snap-on (SNA) — HERE.

I also manage another real-money, public project for this site, the Growth & Income Portfolio; see the home page HERE. And a just-released video about Bank of Nova Scotia (BNS), which I bought as an adjunct to the GIP, can be viewed HERE.

As always, investors are strongly urged to conduct their own thorough due diligence before buying any stocks.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com