When commercial toolmaker Snap-on (SNA) recently announced a 15.4% dividend increase, it got my attention.

When I took a closer look and learned that the raise wasn’t anything out of the ordinary — that it was, in fact, right in line with Snap-on’s annual dividend hikes of the past decade — my interest was really piqued.

And then when my research led me to discover a high-quality company that’s been in business for more than a century, one whose products will be in even greater demand during the upcoming infrastructure boom, and one whose stock is fairly valued … well hello, Snap-on, come on down!

In this article, I’ll talk about what makes this company tick, why I felt it was a good addition to our Income Builder Portfolio, and how it might appeal to Dividend Growth Investing proponents.

History in a Snap

In 1920, as the automobile was becoming recognized as the future of American transportation, there was a growing need to make tools to fix cars … and Milwaukee engineer Joseph Johnson created a wrench set with five handles and 10 sockets that could be interchanged quickly and easily.

Operating under the credo, “Five do the work of Fifty,” Johnson and his co-worker, William Seidemann, used demo sets and brochures to secure orders for 500 socket sets, and the Snap-on Wrench Company was born.

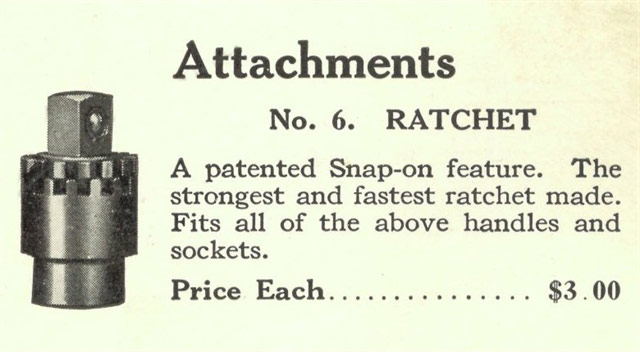

They opened a manufacturing facility in Milwaukee and launched an advertising campaign, secured their first patent (for “No. 6 Ratchet”), and worked to expand the company’s reach.

snapon.com

By 1925, there were 17 branches and 165 salesmen selling Snap-on hand tools directly to mechanics. International expansion began in Canada.

In 1929, the company moved its operations to Kenosha, Wis., a smaller town located between Milwaukee and Chicago.

Innovation came quickly. The company developed tool kits unique to specific car models, and then also branched out into heavier duty socket lines for working on trucks, airplanes, farm equipment, road machinery, mills, mines and power plants.

During the Great Depression, when money was tight, Snap-on became the first tool company to let its industrial clients use credit.

Snap-on became a preferred provider to the U.S. government and was heavily involved in the World War II effort. The military upgraded the material specifications, with nickel alloy steel ultimately becoming a Snap-on standard.

snapon.com

In the decades after the war, Snap-on continued to innovate and expand. There were wheel-alignment products for cars, a new railroad division, salesmen taking tools directly to smaller customers, aerospace products, and expansion into Central and South America.

As air travel boomed, reducing weight became essential. The Navy asked Snap-on to help develop tools that could handle lighter, stronger fasteners. The result was the Flank Drive Wrenching System, which quickly proved so popular that it spread throughout the product line.

snapon.com

The company built new and larger factories in the 1970s and ’80s, and created a manufacturing breakthrough called “cold forming” that made sockets stronger and more specialized.

In February 1978, Snap-on began trading on the New York Stock Exchange under the ticker SNA.

The sky literally was not the limit for Snap-on, which developed equipment for NASA to service its Lunar Rover, Space Shuttle and Space Station projects.

In more recent decades, Snap-on established relationships with auto racing and other sports, expanded into Australia and Japan, went on an acquisition spree to bring more brands under its umbrella, partnered with schools for aspiring mechanics, and increased the size of its credit operations.

Although Snap-on continues to emphasize tools for auto repair and maintenance — mostly distributed by franchisees through well-stocked vans that travel to technicians’ places of business — the company’s reach is broad and multi-faceted.

Here is the official description of Snap-on’s current operations:

Snap-on Incorporated manufactures and markets tools, equipment, diagnostics, and repair information and systems solutions for professional users worldwide. It operates through Commercial & Industrial Group, Snap-on Tools Group, Repair Systems & Information Group, and Financial Services segments. The company offers hand tools, including wrenches, sockets, ratchet wrenches, pliers, screwdrivers, punches and chisels, saws and cutting tools, pruning tools, torque measuring instruments, and other products; power tools, such as cordless, pneumatic, hydraulic, and corded tools; and tool storage products comprising tool chests, roll cabinets, and other products. It also provides handheld and PC-based diagnostic products, service and repair information products, diagnostic software solutions, electronic parts catalogs, business management systems and services, point-of-sale systems, integrated systems for vehicle service shops, original equipment manufacturer purchasing facilitation services, and warranty management systems and analytics. In addition, the company offers solutions for the service of vehicles and industrial equipment that include wheel alignment equipment, wheel balancers, tire changers, vehicle lifts, test lane equipment, collision repair equipment, vehicle air conditioning service equipment, brake service equipment, fluid exchange equipment, transmission troubleshooting equipment, safety testing equipment, battery chargers, and hoists. Further, it provides financing programs to facilitate the sales of its products and support its franchise business. The company serves the aviation and aerospace, agriculture, construction, government and military, mining, natural resources, power generation, and technical education industries, as well as vehicle dealerships and repair centers.

snapon.com

Financial Picture

Like so many companies, Snap-on was hurt by the sudden impact of the COVID-19 pandemic in early 2020.

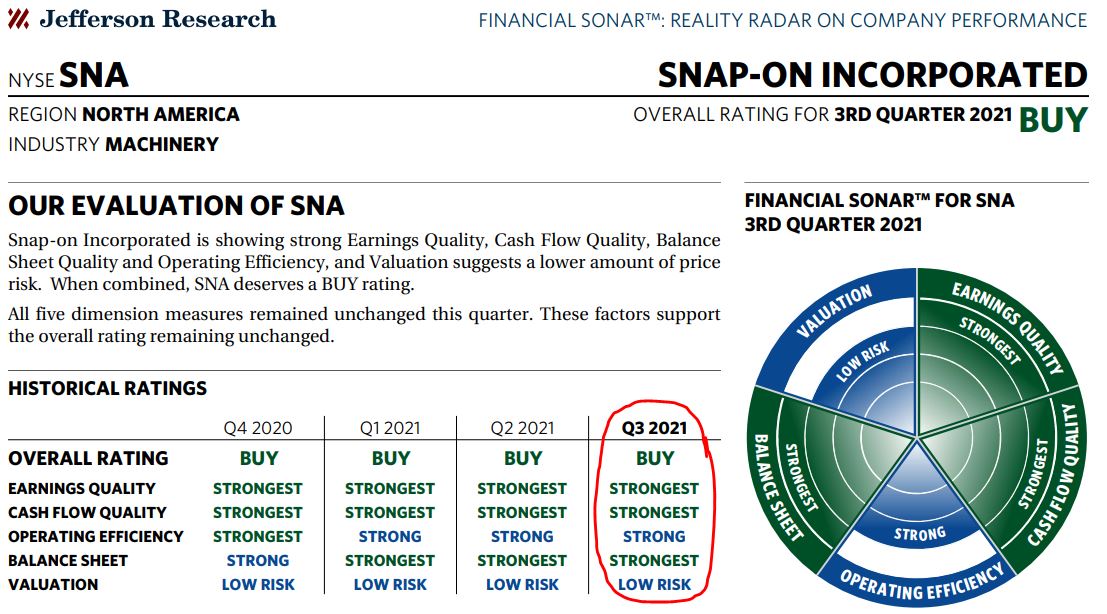

But the business has rebounded strongly, and its balance sheet couldn’t have received a much better “Financial Sonar” picture from Jefferson Research.

fidelity.com

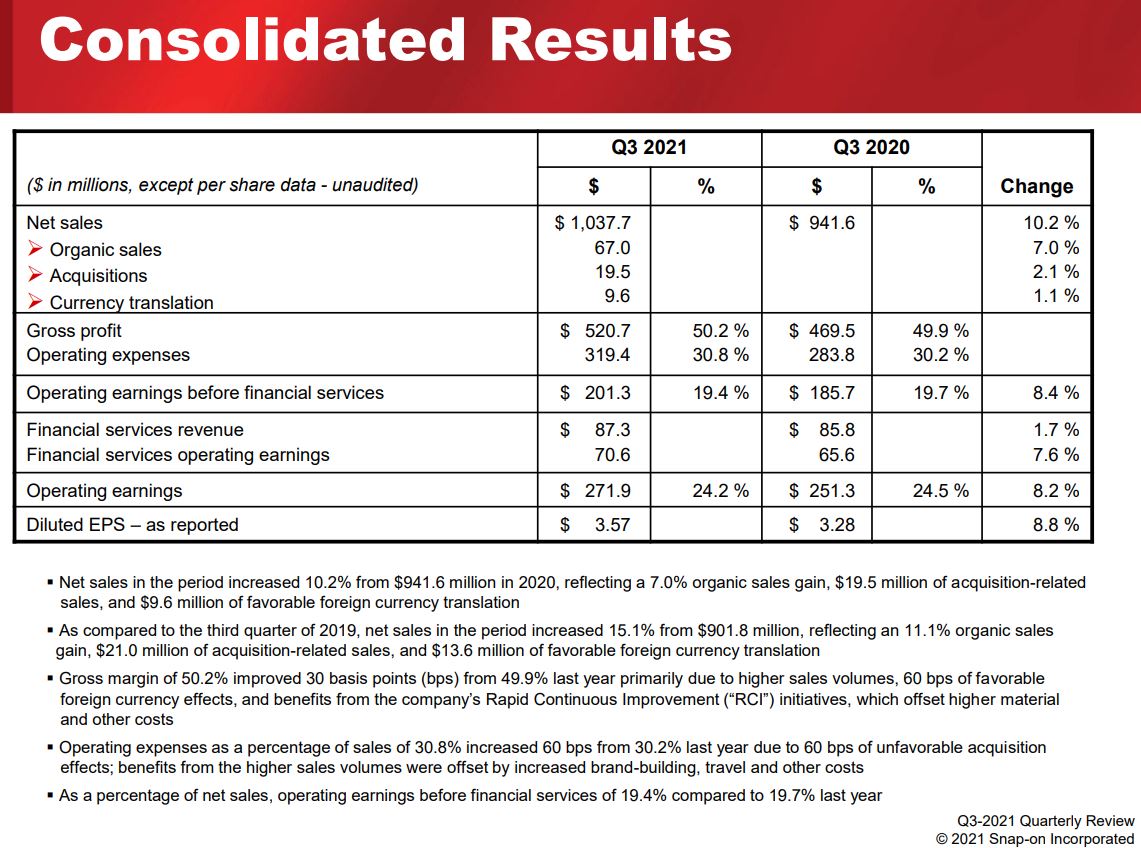

Snap-on reported its third-quarter 2021 earnings on Oct. 21, and the results easily beat estimates.

The company experienced significant year-over-year growth in sales, earnings and profit margin.

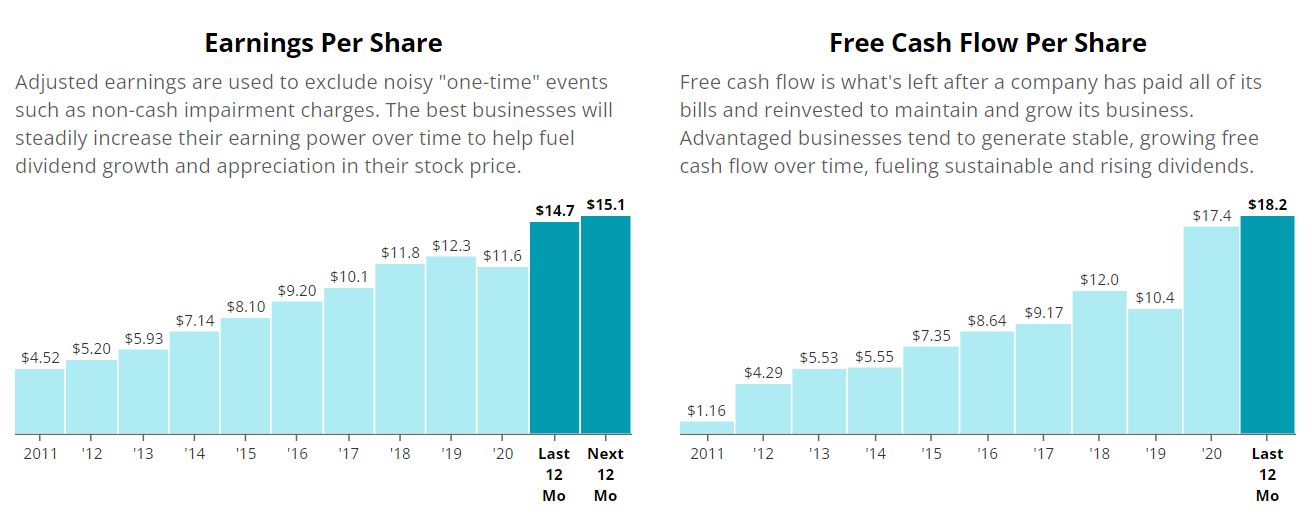

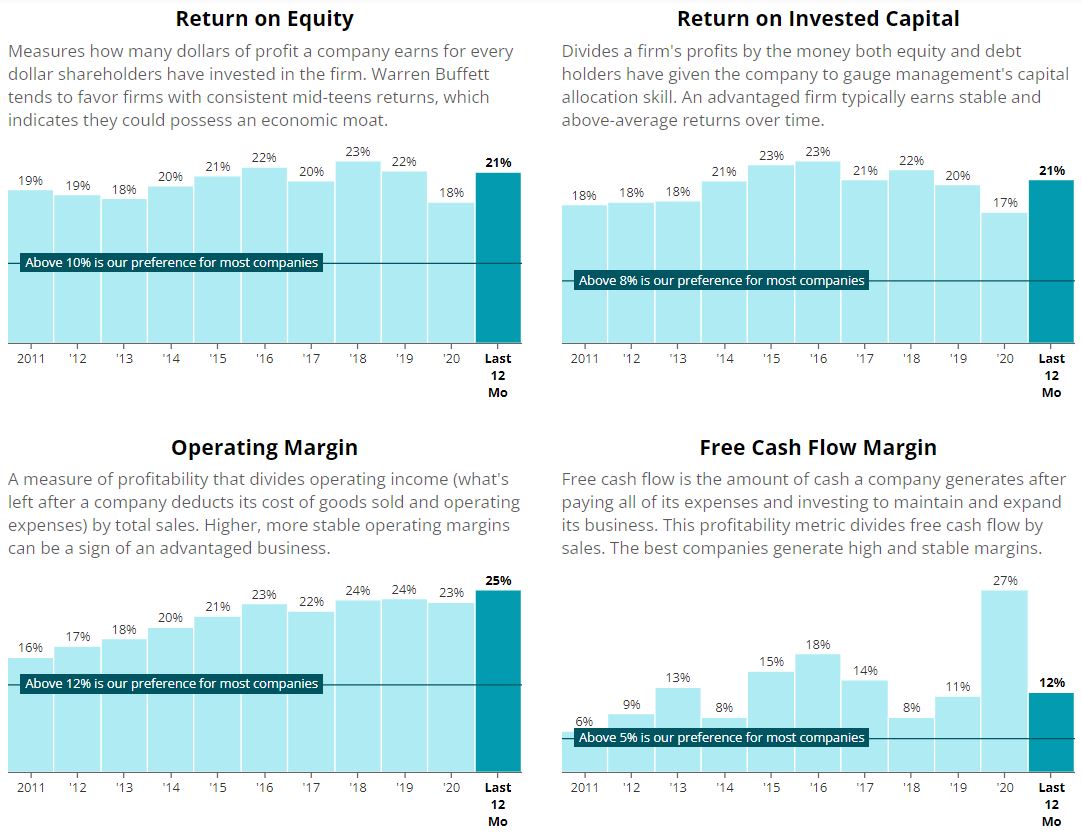

You name the metric, and Snap-on has excelled. (The graphics in the rest of this section are from Simply Safe Dividends.)

Earnings per share have risen well above the pre-pandemic level, and free cash flow is also very strong.

Return on equity, return on invested capital and operating margin each eclipsed the 20% mark over the last 12 months … and that’s nothing new for SNA. Free cash flow margin also has been at a healthy level.

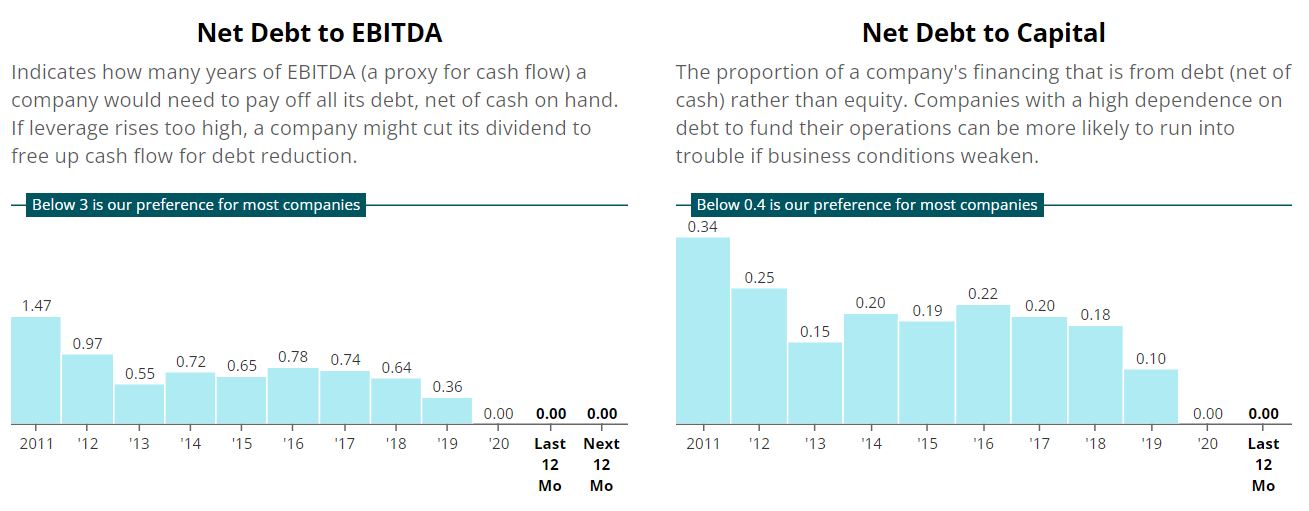

What’s especially nice is that Snap-on has been able to achieve so much growth without taking on significant debt.

Snap-on has received a solid A- credit rating from Standard & Poor’s, an A+ financial strength grade from Value Line, and a “narrow” (2nd-highest) moat designation from Morningstar.

Looking ahead, the $1.2 trillion infrastructure bill that President Biden is about to sign can only help Snap-on. All that construction equipment will need servicing and repair, workers will need the best tools to fix bridges, and so on.

Even the gradual shift to electric vehicles could be a boon. As Morningstar said: “We believe Snap-on will thrive as auto manufacturers are already tapping the company to develop new tools to service new EV models. … We think repair work will shift away from engines to batteries, sensors, wiring, and advanced driver assistance systems. In our view, this will lead to new tools being developed

and increased sales of diagnostic equipment.”

Let’s Talk About Dividends

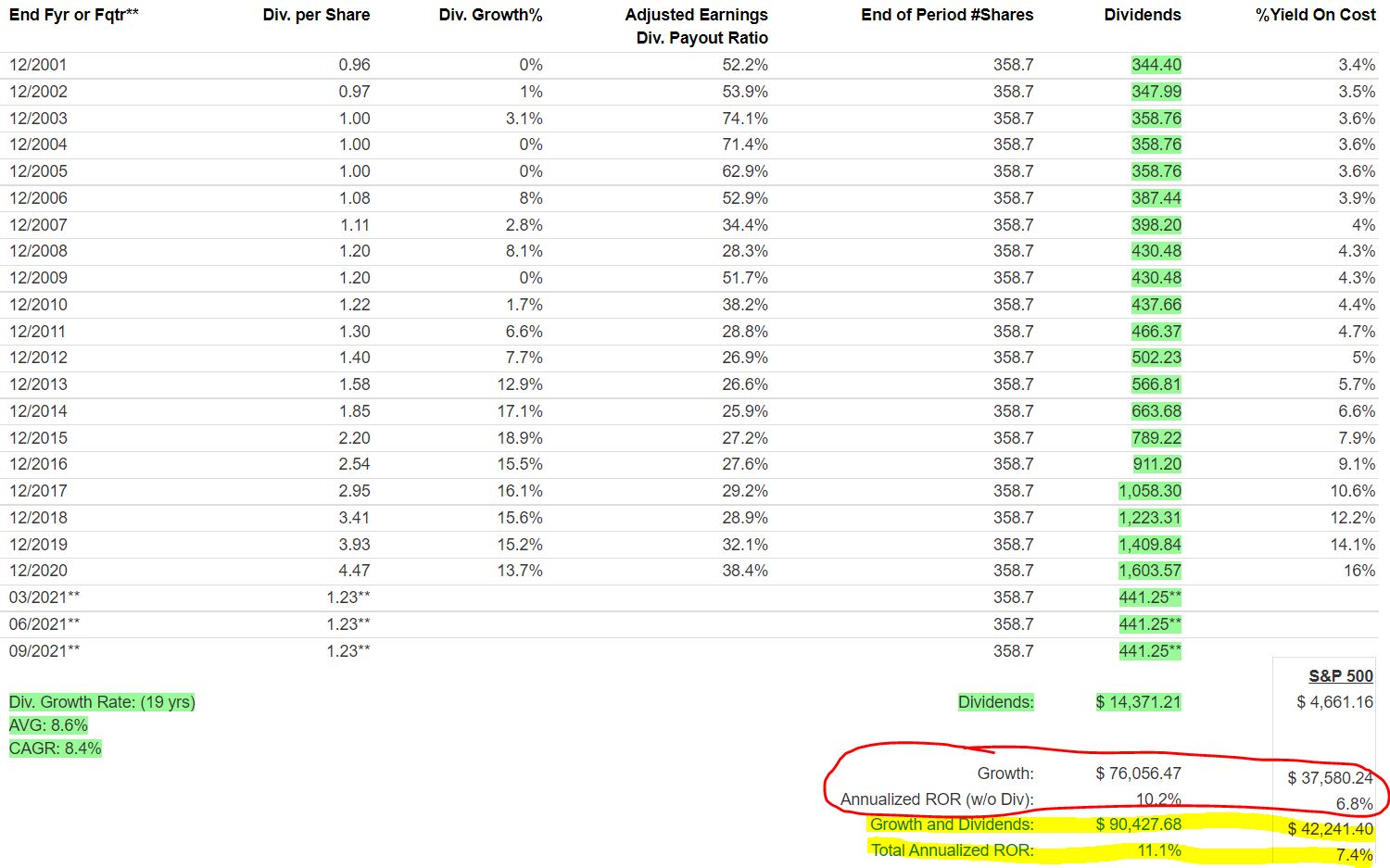

SNA has beaten the S&P 500 Index over the last 10 and 20 years. As the following FAST Graphs illustration shows, a big chunk of the 20-year outperformance is attributable to Snap-on’s reliable, ever-growing dividend.

The red-circled area shows how Snap-on crushed the S&P 500 even without dividends being included in the calculations. The yellow-highlighted area indicates how much the dividend added to the outperformance — with the end result being an outstanding 11.1% annual rate of return over a 20-year span.

SNA has paid a dividend every quarter, without reduction or interruption, since 1939.

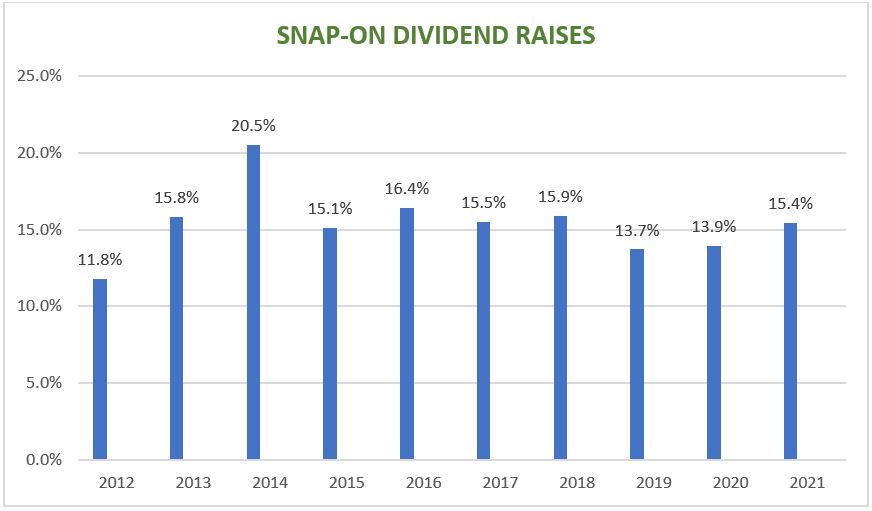

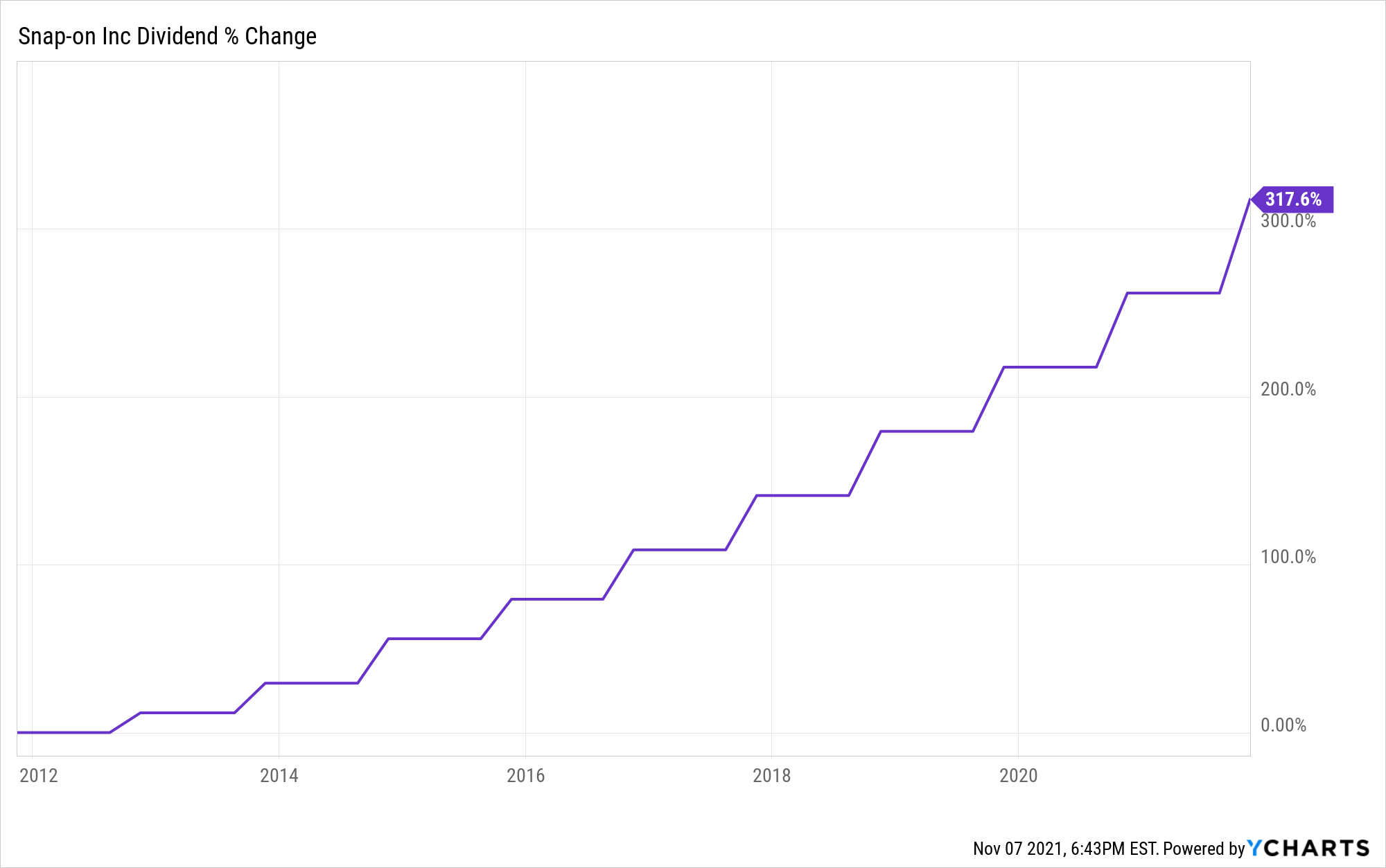

It has had some freezes over the years, so it isn’t a Dividend Aristocrat. But as the very first graphic I used in this article shows, Snap-on has been aggressively raising its dividend for many years — it’s grown more than 300% since 2012 alone.

Snap-on declared its most recent 15.4% raise on Nov. 4, lifting the quarterly payout from $1.23 to $1.42.

The ex-dividend date is Nov. 18, so investors must own shares of SNA by Nov. 17 to receive the next distribution.

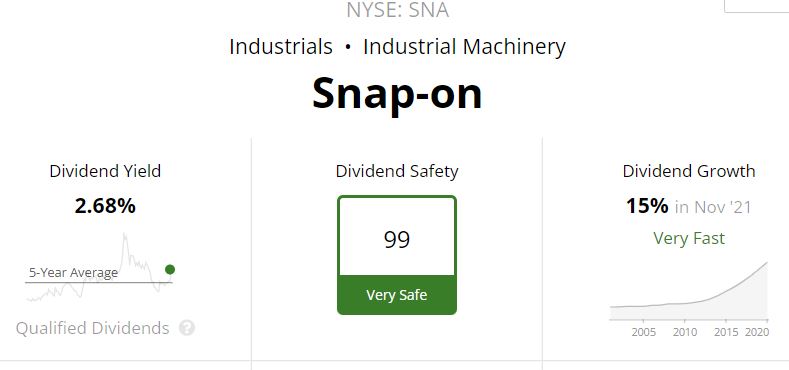

The dividend increase pushed SNA’s forward yield to 2.7%. That, combined with the top safety score of 99 that Simply Safe Dividends bestows upon SNA, could make the stock attractive to DGI practitioners who value income-production, dependability and consistency.

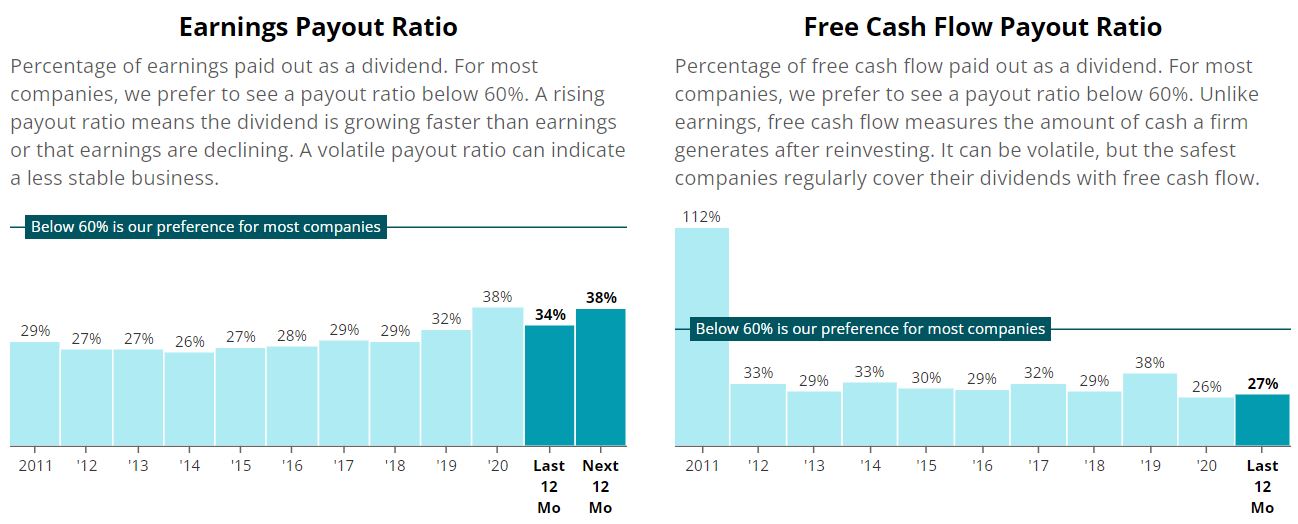

With healthy payout ratios, there is every reason to believe that SNA will continue offering generous dividend raises for years to come.

The company also has been reducing its share total through buybacks, and a new $500 million share-repurchase program has been authorized by the board of directors.

Said CEO Nick Pinchuk:

The dividend increase and the new share repurchase program demonstrate our steadfast commitment to create long-term value for our shareholders and our ongoing belief that we’re well-positioned for the future. This 12th consecutive annual dividend increase confirms the resilience and strength of our business — as evidenced by our payment of consecutive quarterly cash dividends, without interruption or reduction, since 1939, even during times of substantial turbulence. Our strong financial position and robust cash generation enables both our return of capital to shareholders and our support of ongoing strategic investment, organically and through acquisitions, along our defined runways for growth and improvement.

Such words are music to the ears of anybody who does the DGI thing.

Valuation Station

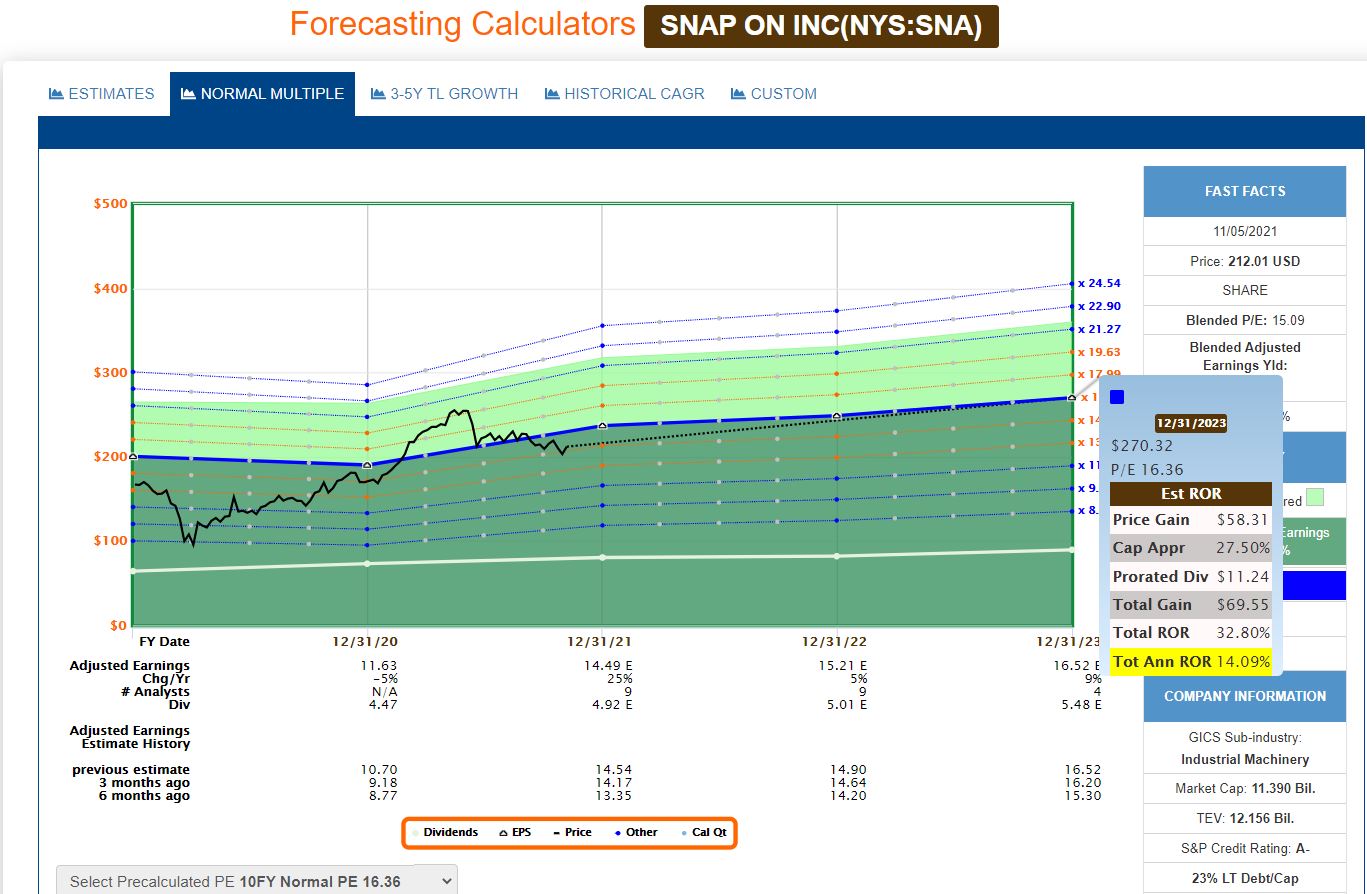

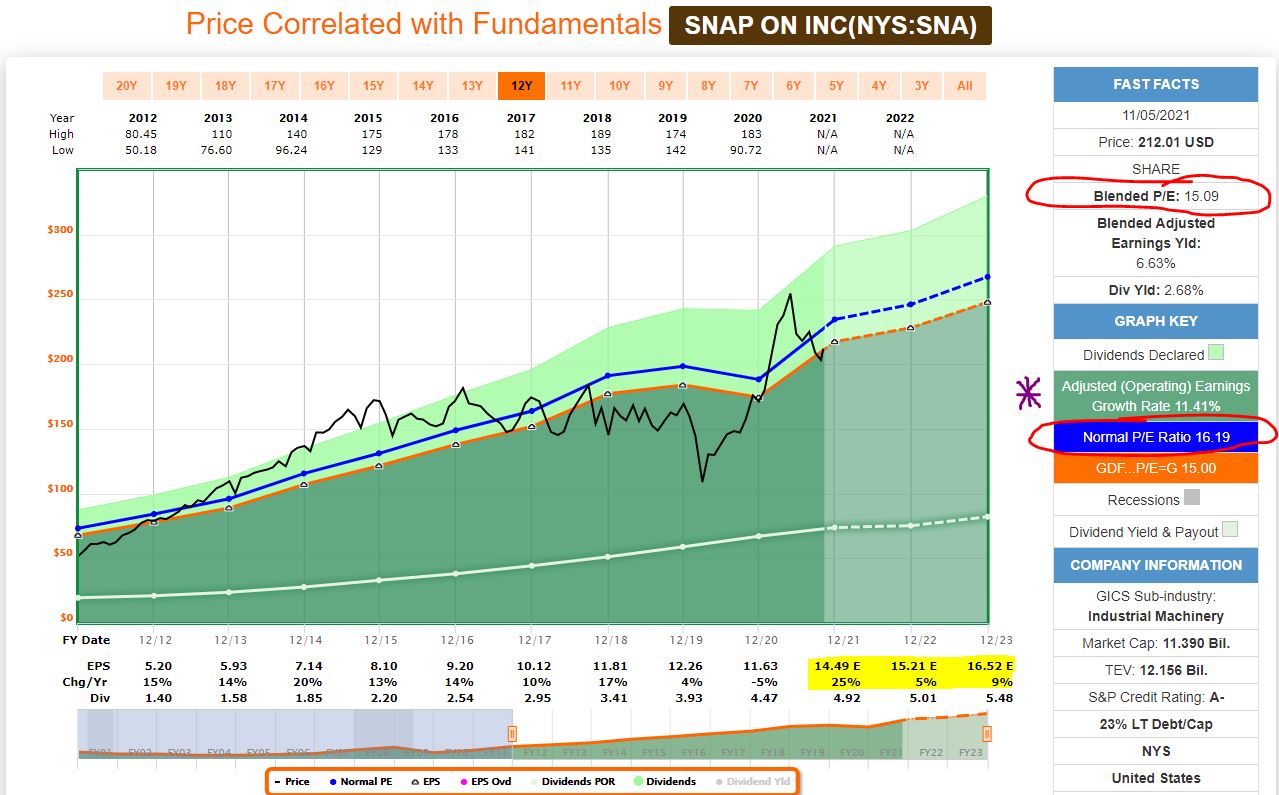

Using FAST Graphs’ forecasting calculator, if I take SNA’s normal price/earnings ratio over the last 10 years and extrapolate it into the future, it suggests a potential 14% annual rate of return through 2023.

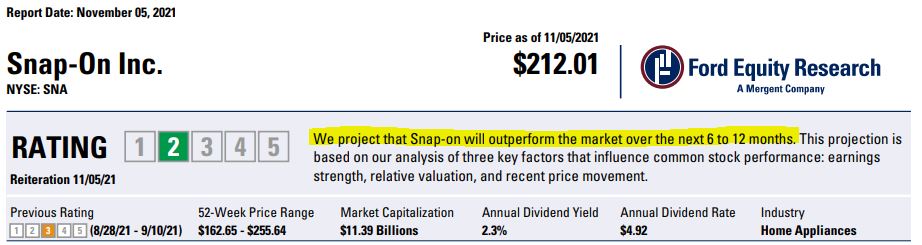

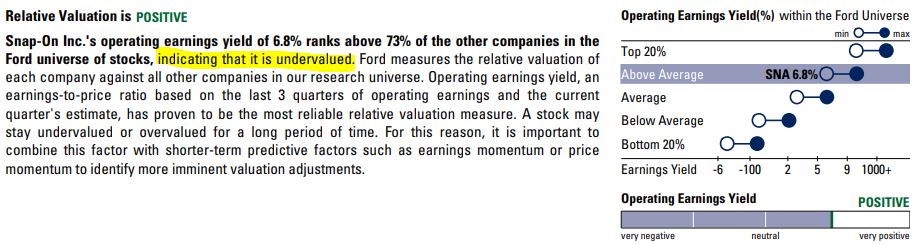

Ford Equity Research believes Snap-on will outperform the market over the next year or so and considers the stock to be undervalued.

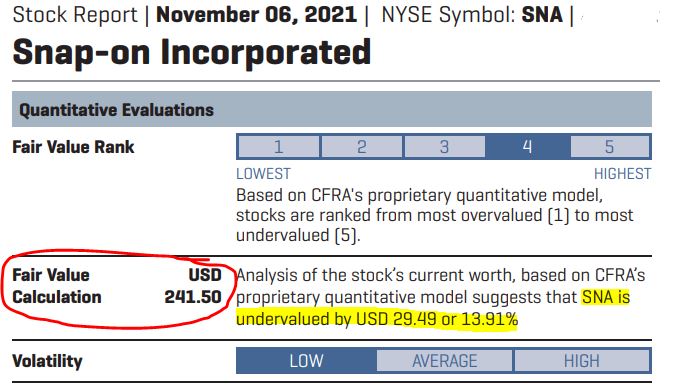

CFRA projects a 12-month target price of $246. It also values the stock currently at $241.50 per share, suggesting SNA is undervalued by about 14%.

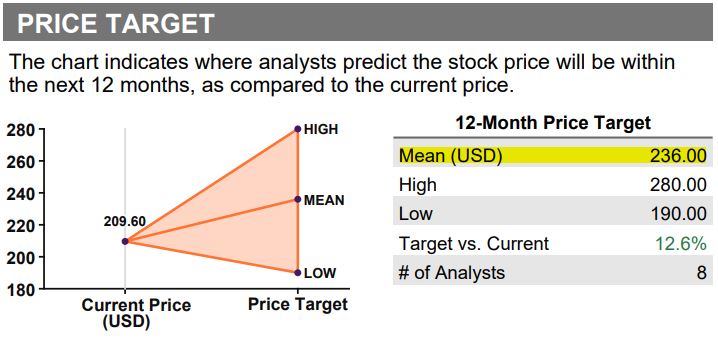

Refinitiv compiled numerous analysts’ projections, showing an average 12-month price target of $236.

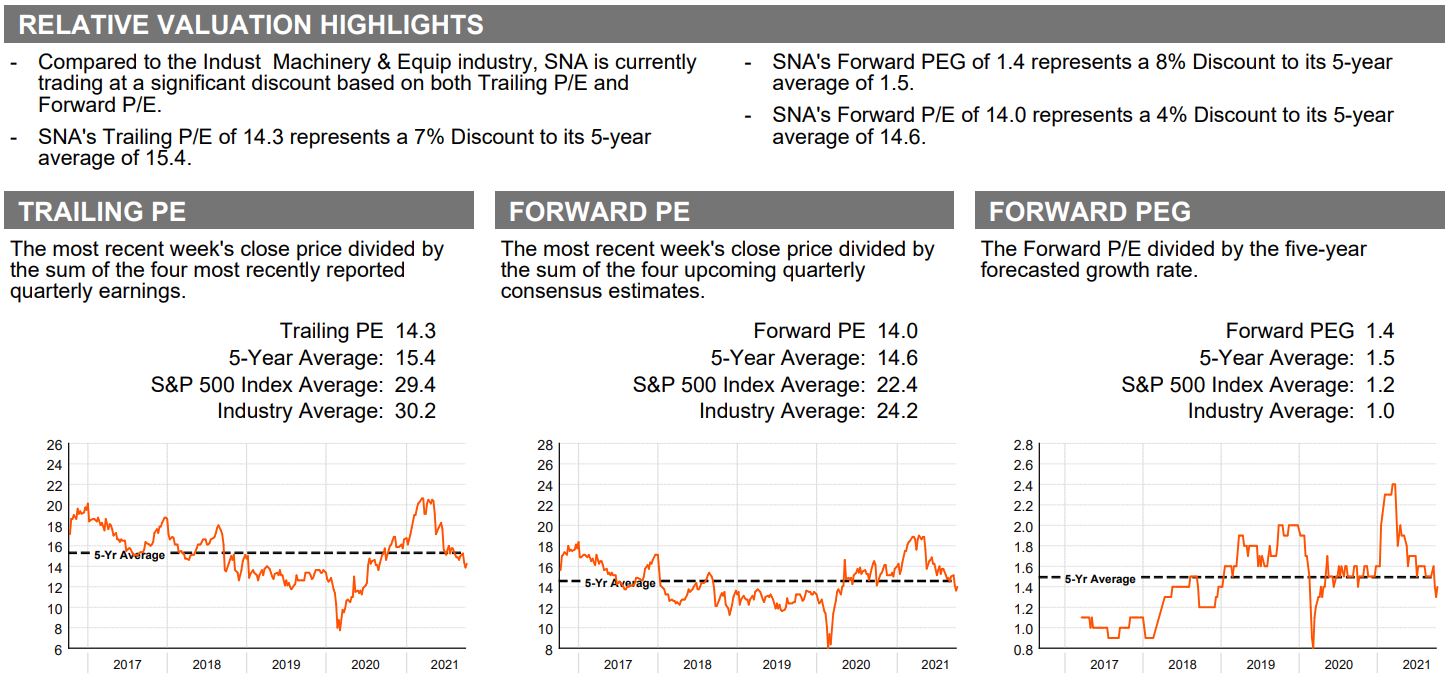

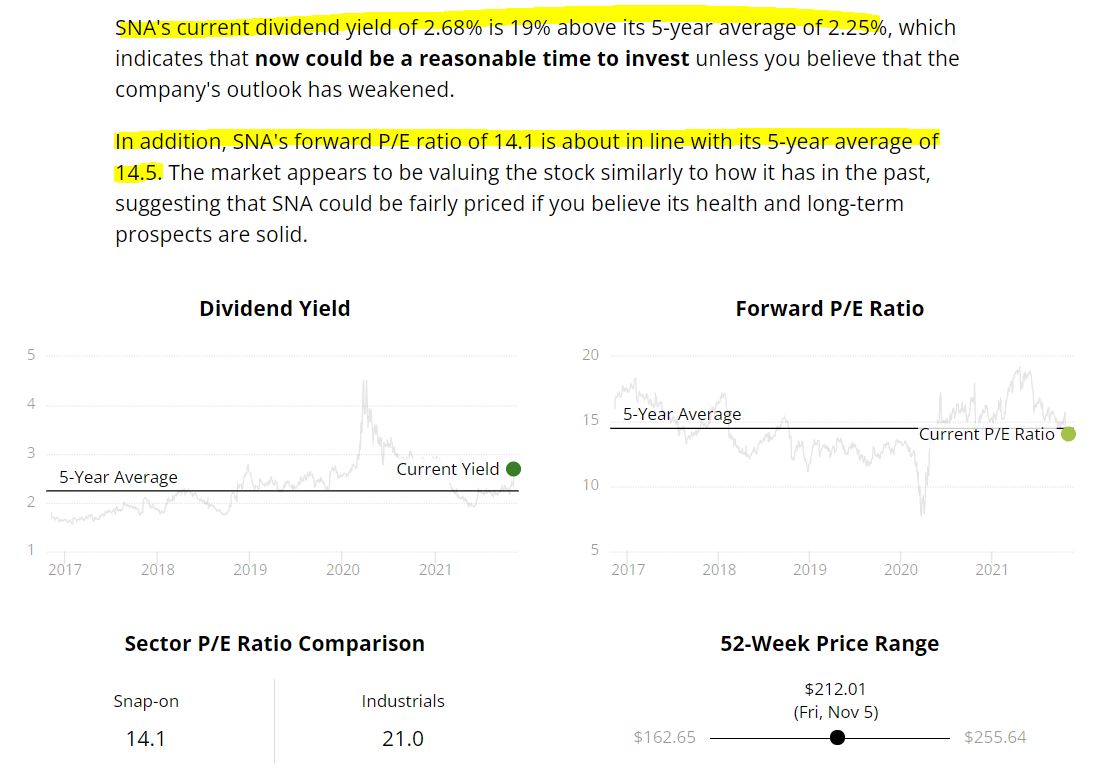

Here is some other valuation-related material from Refinitiv that potential investors might find interesting. Notably, Snap-on is trading at a discount to its 5-year averages in forward P/E ratio, trailing P/E ratio and PEG ratio.

Simply Safe Dividends says Snap-on is undervalued if one compares its current dividend yield to its 5-year average.

And finally, FAST Graphs also shows Snap-on to be at least slightly undervalued, as its “blended” P/E ratio of 15 is lower than the 10-year norm (red-circled areas).

Also of note on the above graphic: The yellow-highlighted area indicates Snap-on’s expected future EPS growth, and the purple star points to the fine 11.41% annual EPS growth rate over the last decade.

Wrapping Things Up

With all of that research completed, I selected Snap-on to be the Income Builder Portfolio’s 45th company.

I was drawn to its proven business model, its probability of future success and, of course, its growing, dependable dividend.

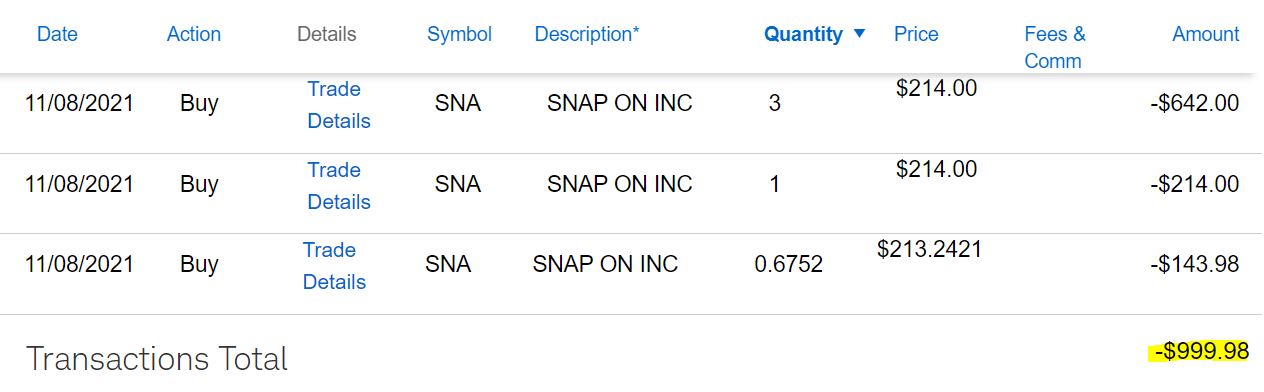

On Monday, Nov. 8, I executed purchase orders for about $1,000 worth of SNA stock on behalf of this site’s co-founder (and IBP money man) Greg Patrick.

Whole shares were bought via a limit order that executed in two transactions a split-second apart; the fractional share was bought using Schwab Stock Slices.

The average price of the 4.6752-share purchase was $213.89. At market close Monday, SNA’s price was $214.11.

Investors are strongly encouraged to conduct their own thorough due diligence before buying any stock.

NOTE: For more on the IBP, see the home page HERE. We also recently published a video recapping the IBP’s October activity; check it out HERE. And for those who can’t get enough of this stuff, I just did an update on the other real-money endeavor I manage, the Growth & Income Portfolio — HERE.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com