Stocks are pricey, but we closed-end fund (CEF) investors aren’t sweating it: we’ve got an edge that lets us buy at a discount, with dividends that are double—and sometimes triple—the typical S&P 500 payout!

That would be our ability to buy CEFs that trade at discounts to net asset value (NAV, or the value of their underlying portfolios). This simple move lets us “rewind the clock” and essentially buy the stocks our CEFs hold at levels we could a few months ago on the open market.

(And there are many bargain-priced CEFs to be had out there, including one trading at a 10% discount and paying more than double the average stock’s dividend—more on that below.)

The One Thing About Today’s Market Everyone Overlooks

Yes, there are plenty of reasons to buy into this market, not the least of which is the fact that investors are focusing solely on valuation measures like the S&P 500’s price-to-earnings (P/E) ratio, which stands at 27 as I write this, well above its level of 22 at the end of 2019.

Trouble is, most folks stop there and overlook the fact that the economy is growing strongly and is set to keep doing so. That will inflate corporate earnings and narrow the gap between the “P” and the “E” in our ratio—setting the stage for more gains as it does.

Let’s dive into the latest numbers to see how this is likely to play out, before we swing back around and talk more about CEFs, including the one I mentioned a second ago.

Earnings Pop—But From a Low Base

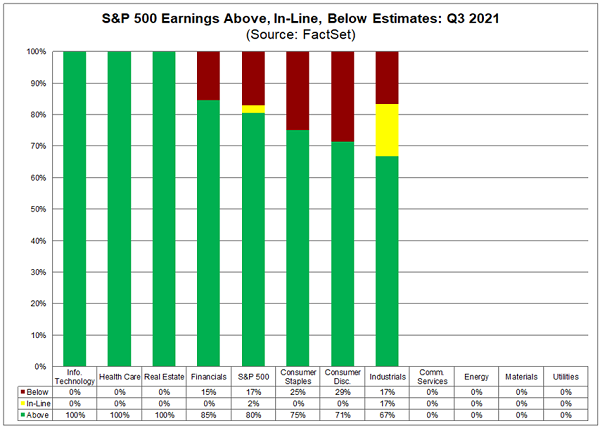

To be sure, today’s higher P/E ratio is at least partially justified by the latest earnings coming out of S&P 500 companies. So far, 80% of firms that have reported their third-quarter results have posted profits above analysts’ expectations. And overall earnings have grown by an average of 30% year over year.

Earnings Surge Past Estimates

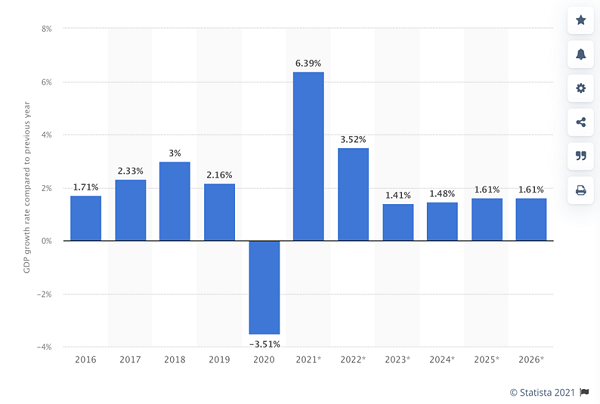

Bear in mind, too, that earnings season has only just started: estimates call for 40% higher profits for all of 2021 as they bounce from the low floor of 2020, when lockdowns and tight pandemic restrictions battered corporate bottom lines.

The low 2020 floor meant this big earnings jump was expected, and it got started in March, so it’s no surprise that stock prices have been rising. But have stocks gone too far, hence the dip in recent weeks? In other words, has all of 2021’s earnings growth been priced into the market?

The real issue here is whether we can expect earnings to keep rising strongly in the next few years, thus justifying that higher P/E ratio. GDP growth—the factor that most P/E ratio–obsessed investors overlook—helps answer that question.

Rising Wealth for the Foreseeable Future

The IMF estimates expect 3.5% economic growth in the US next year, meaning we’re not just buying the strong earnings growth of 2021 but also the strong earnings growth of next year, too. And if the economy stays out of recession for the next few years—as current estimates predict—earnings will keep rising, justifying current market prices and eventually lifting them.

Good Time to Buy Stocks—But We CEF Investors Never Pay Retail

Add it all up and you’ve got a nice opportunity to buy stocks here, especially if you’re holding for the long run and/or are investing mainly for income. But we don’t have to hurry, either. And, as mentioned, you’ll be in an even better position if you buy CEFs at a discount, as we always aim to do in my CEF Insider service.

For example, a large cap stock investor would be better off with a CEF like Tri-Continental Corporation (TY) than buying stocks individually or through an ETF. (Don’t be surprised if you haven’t heard of TY, which is managed by Columbia Threadneedle Investments; as we’ve discussed before, the CEF world is small, and within that world there’s a fair amount of concentration among bigger players like Nuveen, PIMCO and BlackRock.)

Despite its obscure name, TY is a sizeable CEF, with nearly $2 billion in assets invested in strong US large cap stocks: Apple (AAPL), Alphabet (GOOGL), Microsoft (MSFT), Facebook (FB) and Broadcom (AVGO) are its top holdings. Those names might make you think TY is a tech fund, but that’s not the case. It also holds companies like Pfizer (PFE) and Dow Inc. (DOW), so you’re getting broad diversification here, as well.

But as a CEF, TY gives us two other advantages: a discount on these stocks’ market prices (the fund trades at a 10% discount to NAV, so you’re essentially getting its portfolio of strong US large caps for 90 cents on the dollar) and a dividend that’s more than double what the typical S&P 500 stock pays: TY’s shares yield around 3.5% as I write this.

Even so, I have to admit that TY is a bit dull in the world of CEFs, because there are dozens of other funds that hold these companies while trading at discounts and paying higher dividends. CEF Insider members, of course, know this well—our portfolio yields a tidy 6.5% today, and our equity-focused CEFs, which total five in all, do better, with an average 7.2% yield between them.

— Michael Foster

Urgent Buy: A CEF With a “Hidden” 9% Yield (and 20% Price Upside) [sponsor]

I especially want to let you in on one of our equity CEFs: it holds many of the same large cap companies as TY, but with a huge difference: this one drops a huge special dividend on us yearly—so big that I expect its yield for 2021 to top 9%!

That big special payout comes our way in December, by the way, so the time to buy is now. That’s because, when this big payout is announced, it almost always takes investors by surprise (even though it really shouldn’t), driving a big bounce in the share price.

This amazing dividend play is one of my top 5 CEFs to buy now. Taken together, these 5 stout income plays boast a safe average yield of 7.1%. And they’re so undervalued (even in today’s pricey market!) that I fully expect them to surge 20% or more in the next 12 months.

I’ve got everything you need to know about these 5 CEFs right here, including their names, tickers, current yields, my complete analysis of management and more.

Source: Contrarian Outlook