In any portfolio, some stock positions are easy to manage and some require a little more work.

When it comes to the Income Builder Portfolio, the real-money project I’ve been putting together for nearly 4 years now, Medtronic (MDT) sits in the latter group.

Even though the world’s largest stand-alone medical device company spent almost 7 decades headquartered in Minnesota and is still primarily a U.S. operation, Medtronic is now based in Ireland — and that creates some tax-related implications for MDT shareholders.

Despite that, Medtronic has been a worthwhile holding for the IBP since June 2020, and I’m bullish on its future, too.

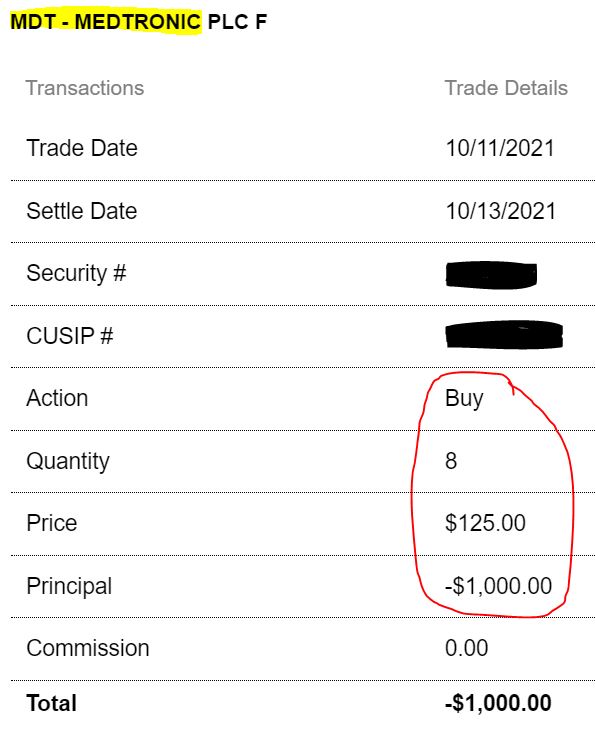

So on Monday, Oct. 11, I executed a limit buy order for $1,000 worth of MDT stock on behalf of this site’s co-founder, Greg Patrick.

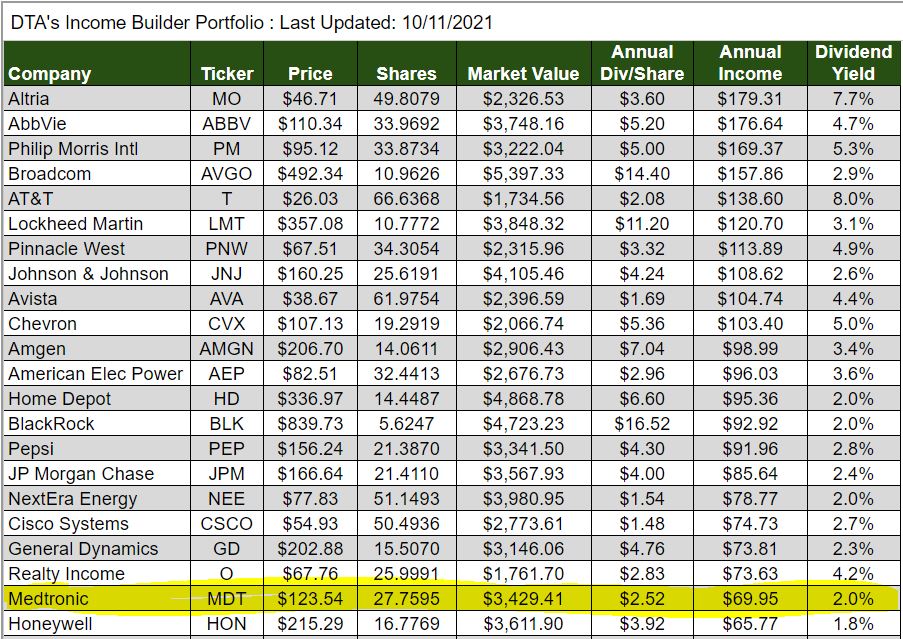

The IBP now has 27.7595 shares of Medtronic — which has jumped into the upper half of the 44-stock portfolio’s income-producers and the top 15 when ranked by market value.

(See the entire portfolio, as well as links to every IBP-related article, HERE.)

Taxing Issue?

As the above table shows, MDT is projected to generate about $70 in income for the IBP over the next year. How will Greg and other shareholders be taxed on those dividends? It depends on where they live.

Here is what Medtronic says about the subject on its website:

Medtronic plc has established tax residence in Ireland, and as such, dividends are considered Irish source income and Irish dividend withholding tax (“DWT”) rules apply. … Payments will be subject to an Irish withholding tax unless the shareholder that is beneficially entitled to the dividend is a resident of the United States or a resident of a country listed as a “relevant territory,” and has ensured that the required information is on file with their broker, bank, qualifying intermediary or transfer agent. … With these rules, the vast majority of Medtronic shareholders and beneficial owners are entitled to an exemption from DWT.

In other words, U.S. residents like Greg are not subject to Irish withholding tax on their MDT dividends as long as they have filed the proper paperwork with their brokers.

Because Greg didn’t want to deal with the hassle of foreign withholding taxes, I have avoided selecting non-U.S.-based companies for the IBP unless they have these kinds of tax truces with the United States.

No Automatic Drip

Even with this arrangement between the countries, some brokers do not allow dividends from foreign countries to be reinvested automatically — aka “dripped.” And Schwab, where the Income Builder Portfolio is held, happens to be one of those brokerage houses.

The IBP Business Plan mandates dripping, so I have gotten around Schwab’s silliness by what I call “backdoor reinvesting.”

While it won’t let me drip MDT divvies, Schwab does include Medtronic among the hundreds of companies in which an investor can buy fractional shares through the brokerage’s “Stock Slices” platform.

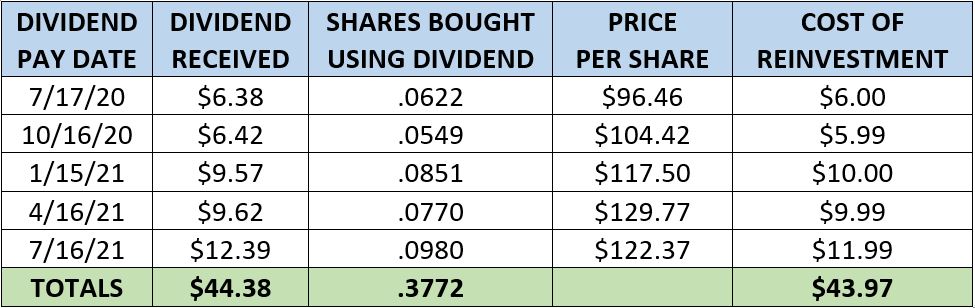

So after the Medtronic dividend has hit the IBP account each quarter, I have turned right around and used those funds to buy more MDT.

Over the course of the IBP’s ownership of MDT, about $44 has been paid out in dividends over five quarters, and all but a few pennies of it has been reinvested, buying .3772 of a share in all.

The end result is the same as if dripping had been done automatically; I just have to do a tiny bit more work with MDT than I do with the portfolio’s other 43 positions.

That table also gives an interesting look at dollar-cost averaging in action.

We sometimes paid a pretty low per-share price when reinvesting the Medtronic dividends. But we also paid $129.77/share — more than MDT trades for now — for the “slice” bought with the 4/16/21 distribution. The average price per share for the five drips was $116.57.

As much fun as it can be to see our stocks appreciate in price, investors who build positions over time actually benefit if prices stay low.

More Income Info

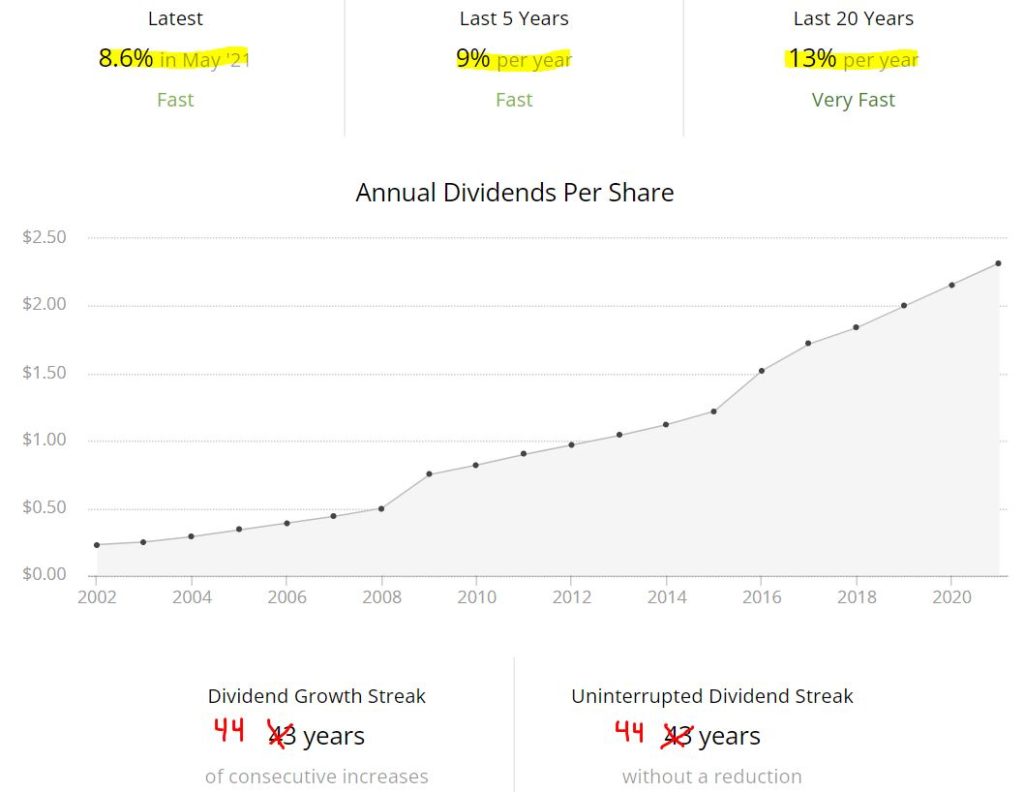

As mentioned prominently in my previous article, in which I made my case for adding to our position in this high-quality company, Medtronic has increased its annual dividend for 44 straight years.

SimplySafeDividends.com

MDT’s ex-dividend date was only a few weeks ago, so the 8 shares we just bought won’t generate any income until the mid-January distribution.

Nevertheless, the IBP’s Medtronic position soon will increase in size, as the 17.7595 shares we already held will produce $11.19 in income on Friday, Oct. 15. Once again, I’ll quickly invest that into another “slice” of MDT — adding about .09 of a share.

Then, once the mid-January dividend arrives, it will apply to 25.85 shares … and the ensuing $16.29 payout will be used to buy yet another slice.

Lather, rinse, repeat … over and over again … not just with MDT but with all 44 positions. And that’s how an income stream gets built for our appropriately-named endeavor.

Valuation Station

Most analysts are extremely bullish on Medtronic, which has a forward price/earnings ratio of about 22.

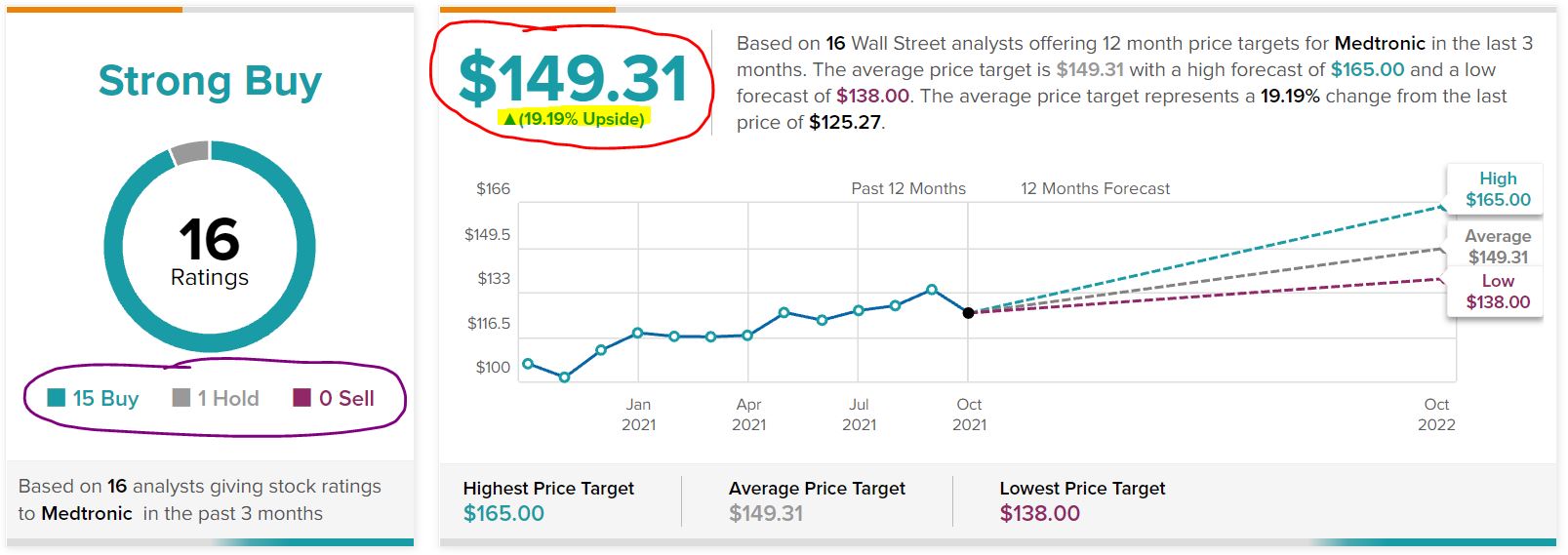

For example, 15 of the 16 tracked by TipRanks call it a “buy,” and their average 12-month price target suggests an upside of almost 20%.

TipRanks.com

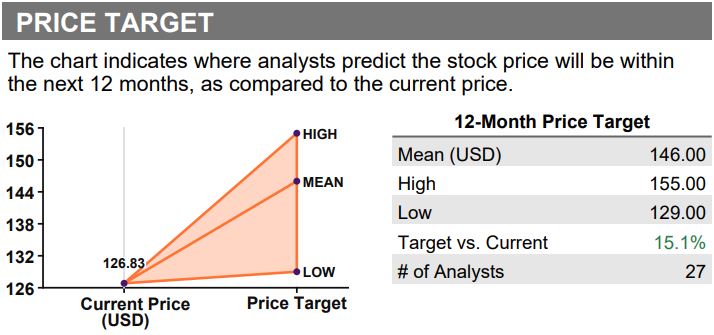

The results are similar in the Thomson Reuters survey, with 23 of 30 analysts rating MDT either a “strong buy” or “buy.”

Thompson Reuters, via fidelity.com

The mean price target put forth by those analysts is $146 — about 17% higher than we just paid for our latest tranche of MDT.

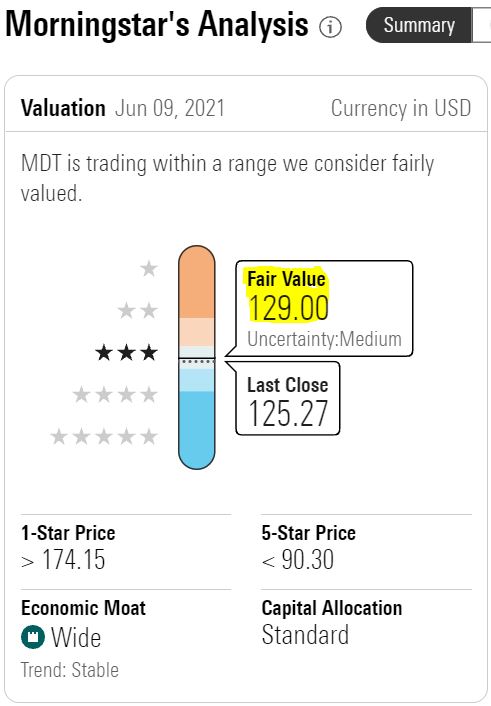

Morningstar recently increased its fair value estimate for Medtronic from $118 to $129, suggesting the stock’s price is reasonable here.

morningstar.com

Morningstar analyst Debbie Wang said the estimate was raised “after adjusting our expectations for the resumption of pre-pandemic procedure volume in fiscal 2022, the anticipated launch of renal denervation in early 2023, and cash flow realized since our last update. We continue to hold fairly optimistic expectations for innovation in the structural heart, diabetes, and neurovascular units, as well as gradual margin expansion to account for efficiency programs and higher-margin new products.”

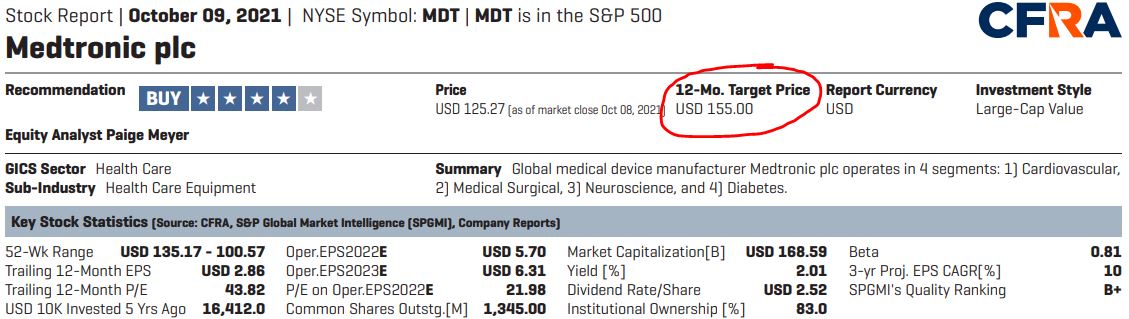

CFRA has set a $155 year-ahead price target for MDT, with analyst Paige Meyer forecasting 10.3% sales growth for the 2022 fiscal year.

CFRA, via schwab.com

Meyer added:

We believe that MDT’s shares, trading at 23.3x our FY 22 EPS estimate, have room for appreciation. Given MDT’s broad lineup of new products and its high exposure to elective procedures, we expect the company to generate strong results as health care systems recover from the impact of Covid-19. MDT also stands out from medical device peers because of its strong financial position (e.g., leverage ratio of 1.8x as of July 2021), which has probably helped the company capture market share during the pandemic. In our opinion, new product growth should support continued share capture in the near future. One product that we’re particularly looking forward to is MDT’s robotic assisted surgery platform, a key future growth driver, which could see European regulatory approval by September 2021.

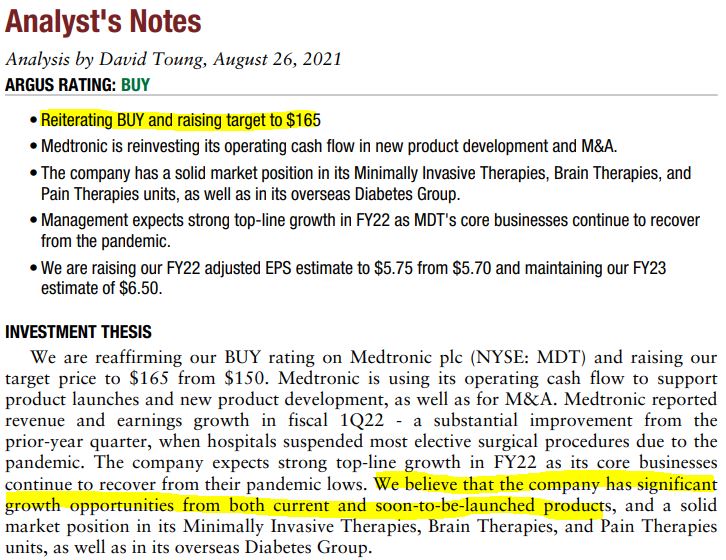

Citing “significant growth opportunities from both current and soon-to-be-launched products,” Argus raised its target price from $150 to $165.

Argus, via schwab.com

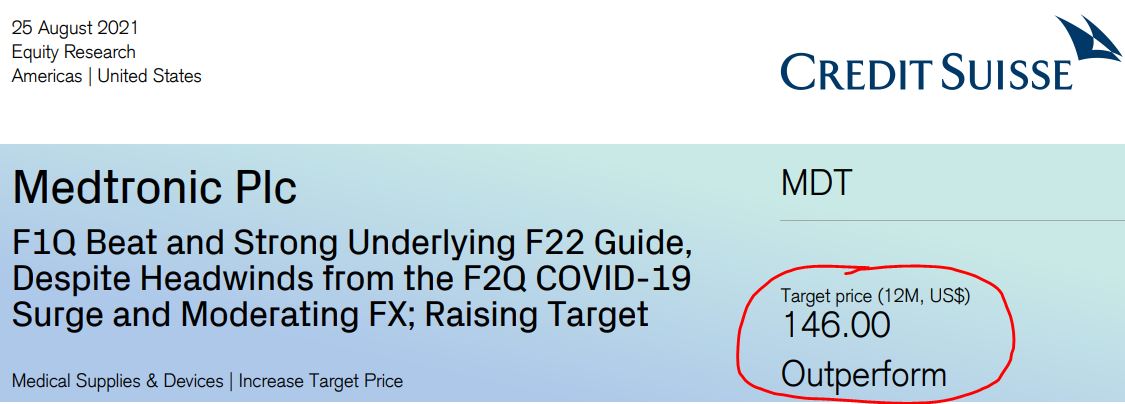

Impressed that Medtronic management raised the company’s earnings guidance for 2022, Credit Suisse established a $146 target price.

Credit Suisse, via schwab.com

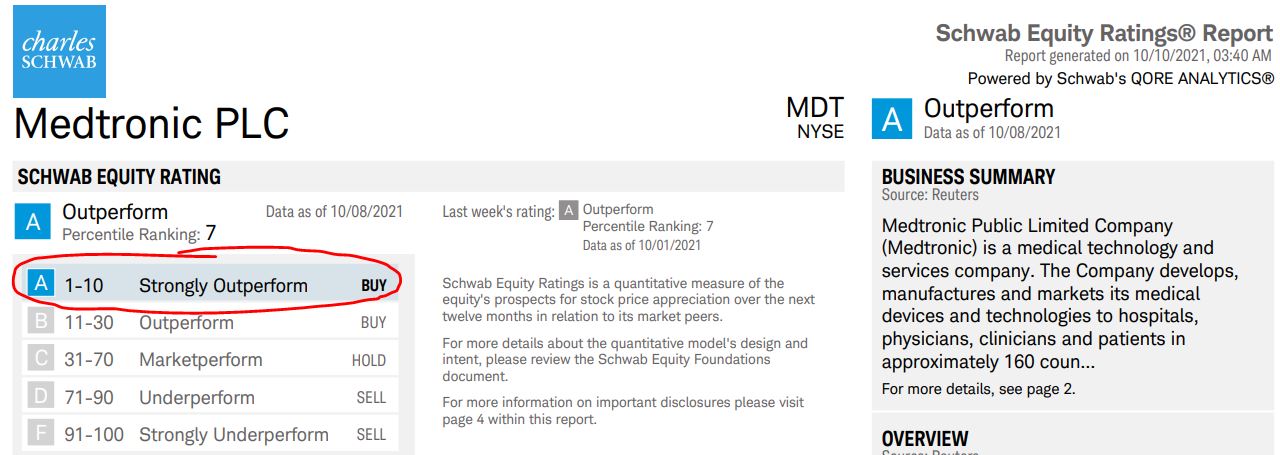

Schwab doesn’t give target prices, but its analytics forecast strong outperformance for MDT stock in the coming year.

schwab.com

Value Line said the stock could appreciate by 20% over the next 18 months (yellow highlights in the following graphic) but not by much more than that over the longer term (red-circled area).

valueline.com

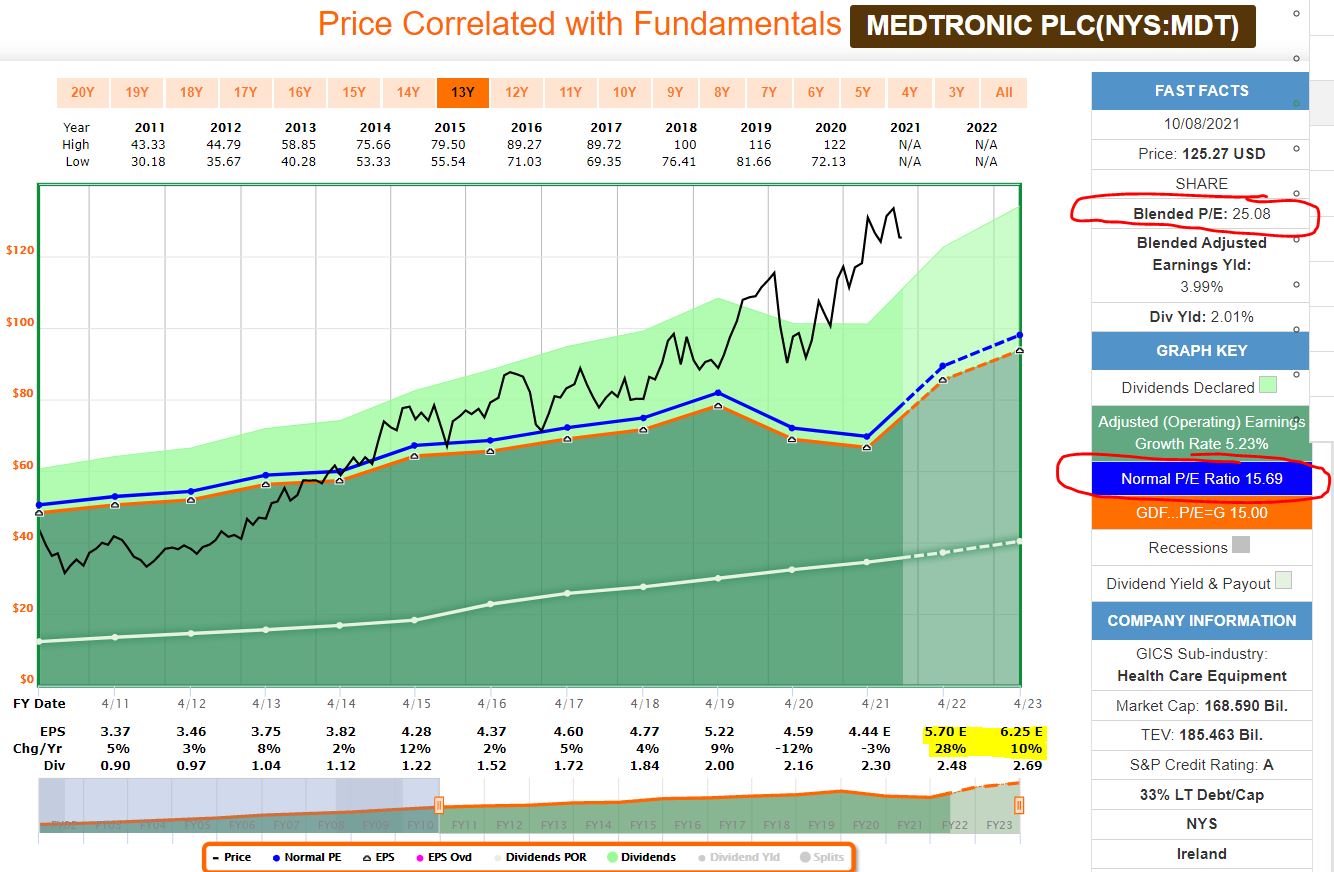

A look at a FAST Graphs illustration shows that the current “blended P/E ratio” is considerably higher than Medtronic’s 10-year norm (red-circled areas below). Nevertheless, expected earnings growth (as indicated by the yellow highlight) gives an idea why so many analysts are bullish on MDT.

fastgraphs.com

Wrapping Things Up

Medtronic has been making products that improve the lives of human beings since Harry Truman was in the White House, and it has been growing its dividend since Jimmy Carter was shelling peanuts in the Oval Office.

The company continues to innovate and grow and perform. Its balance sheet is strong, its dividend is safe and its fundamentals are sound.

Medtronic’s move to Ireland for tax reasons has added a step for some investors … but that hasn’t made MDT any less appealing for the Income Builder Portfolio.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com