When discussing my stock-selection process for the Income Builder Portfolio, I give a lot of lip service to “quality.”

Yes, I use Dividend Growth Investing as my primary strategy, so metrics like yield and payout ratio matter; and yes, I want companies that have performed well on a total-return basis over time; and yes, I prefer to buy a stock when it’s fairly valued (or, even better, when it’s undervalued).

But as it says in the IBP Business Plan: “The perceived quality of the company is of utmost importance.”

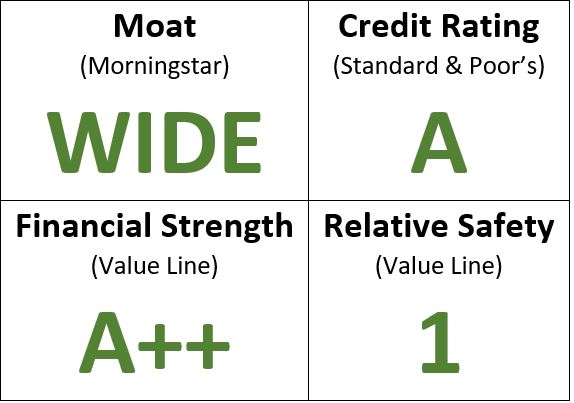

So I love seeing a quality profile like this for a company I’m considering:

That impressive profile belongs to Medtronic (MDT), the world’s largest stand-alone medical-device company, and that’s my next pick for the portfolio.

On Monday, Oct. 11, I plan to execute a purchase order for about $1,000 worth of MDT stock on behalf of this site’s co-founder (and IBP money man), Greg Patrick.

It will be the fourth time we will have added shares of Medtronic. We initiated the position with a $1,034 buy on June 23, 2020, and then made smaller purchases on Oct. 6, 2020, and May 7, 2021.

See the entire 44-stock portfolio, as well as links to every IBP-related article, HERE.

Why Medtronic?

As I said — and as I showed with my earlier graphic — the company is recognized as a quality leader in its industry.

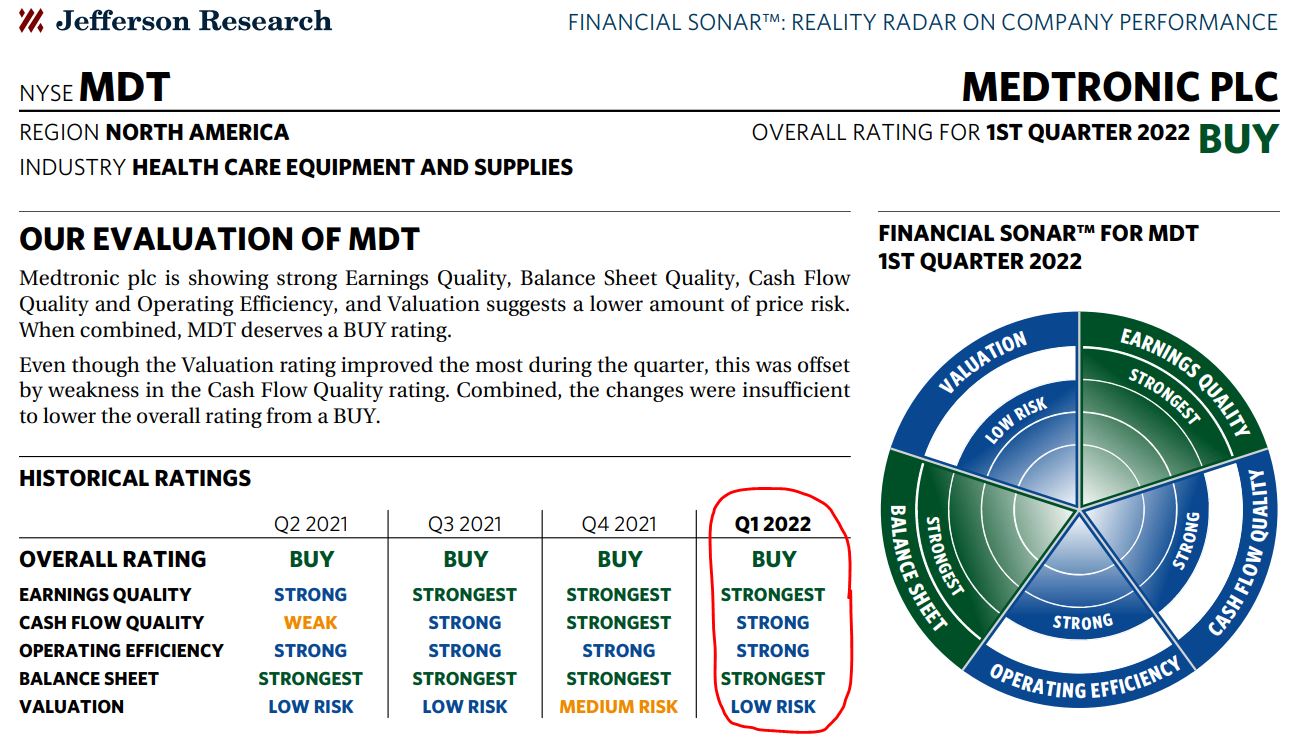

Continuing with that theme, here’s a look at Jefferson Research’s “Financal Sonar” for Medtronic:

Jefferson Research, via fidelity.com

When a company has the kind of balance sheet and earnings quality that the Jefferson Research graphic represents, it shouldn’t be surprising to see superb performance in various financial categories.

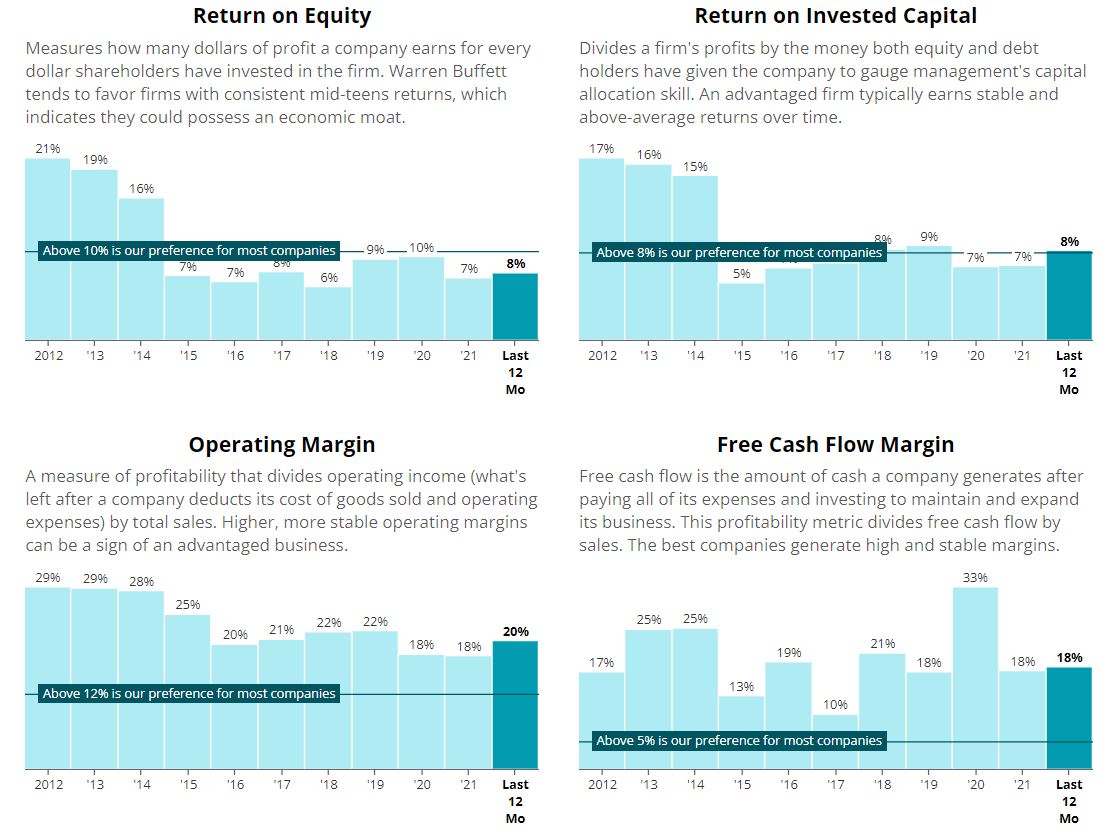

SimplySafeDividends.com

The COVID-19 pandemic has been rough on thousands of companies, and medical-device makers have not been immune.

During the first 12 months, and beyond, the coronavirus so occupied hospitals and medical personnel that non-emergency procedures were being postponed or canceled.

Thankfully, the vaccines have gradually improved the world’s collective health — which, in turn, has improved Medtronic’s bottom line.

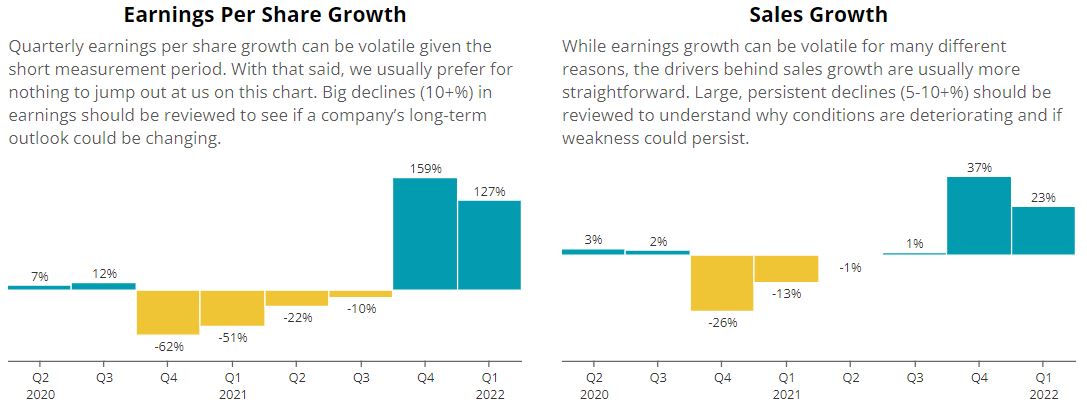

Check out the growth in the company’s earnings and sales the last couple of quarters after the pandemic-related declines.

SimplySafeDividends.com

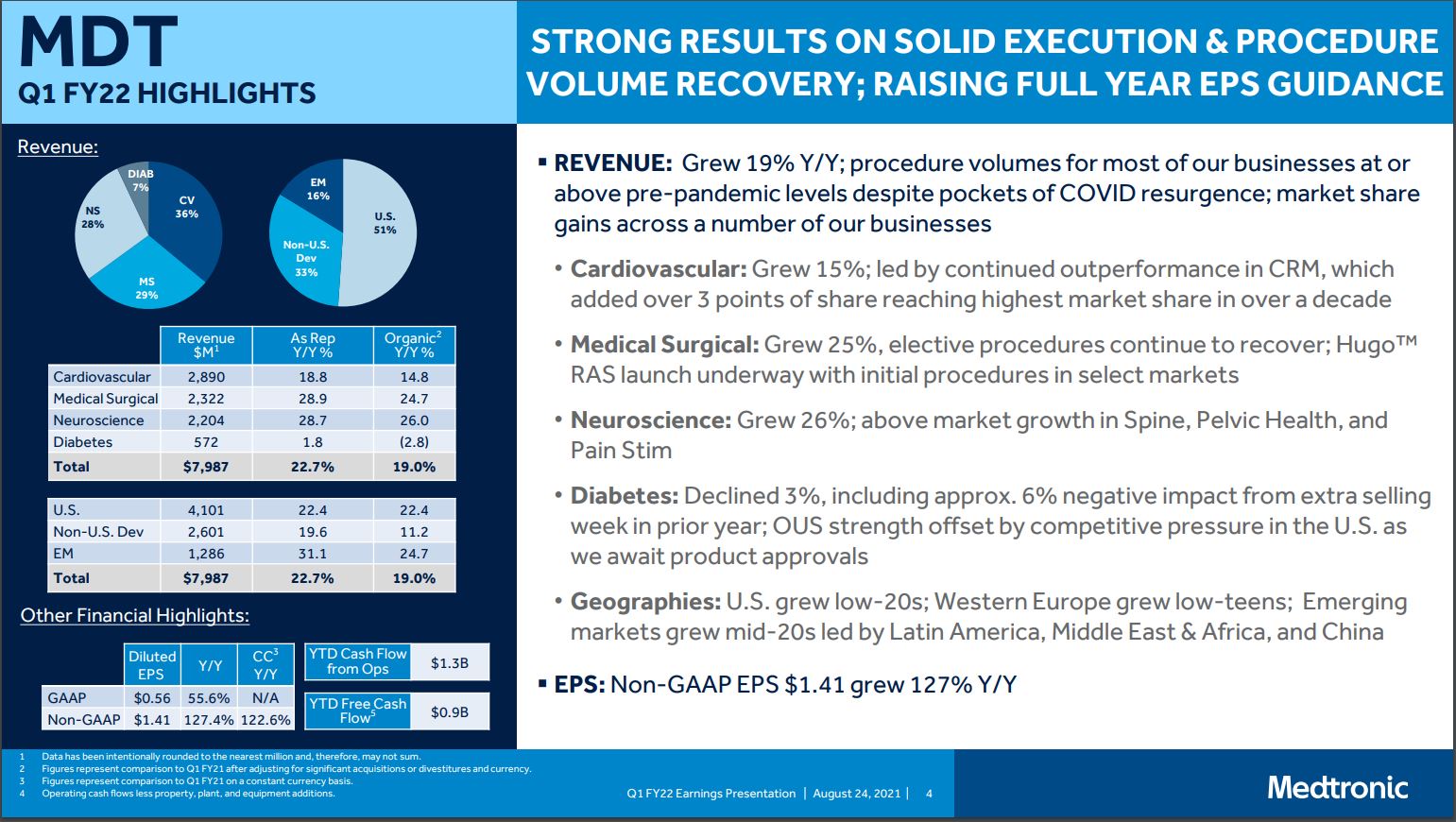

The following slide from Medtronic’s fiscal 2022 first quarter earnings presentation on Aug. 24 gives a nice snapshot into the performance of the company’s various divisions — Cardiovascular, Medical Surgical, Neuroscience and Diabetes. The first three experienced significant revenue growth, helping to offset a small organic loss for Diabetes devices.

Medtronic is known worldwide for its indispensable work in caring for the human heart, with devices such as implantable cardioverter-defibrillators, pacemakers, stents and valves.

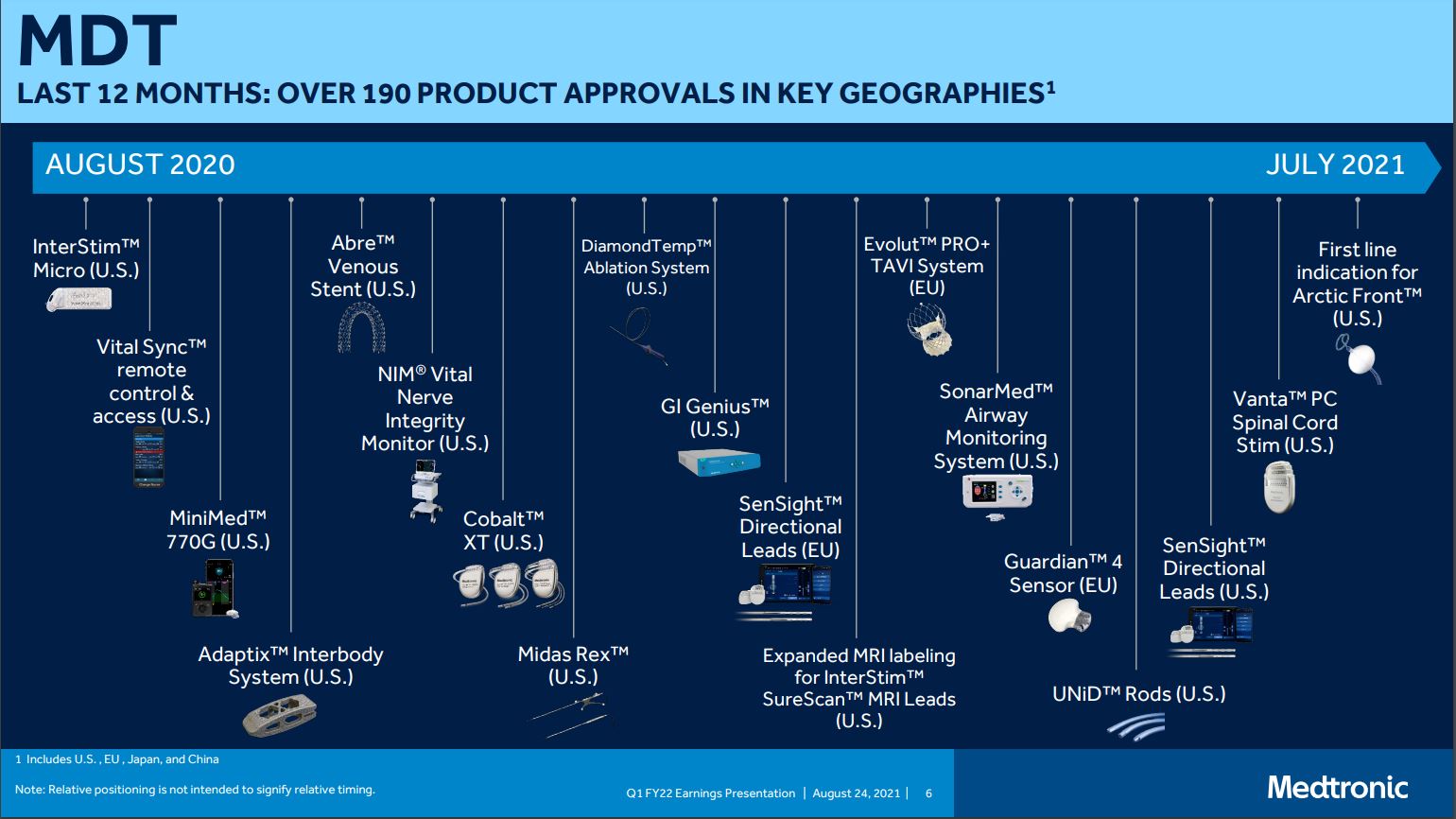

Its pipeline across all categories is strong, with nearly 200 products having been approved between August 2020 and July 2021.

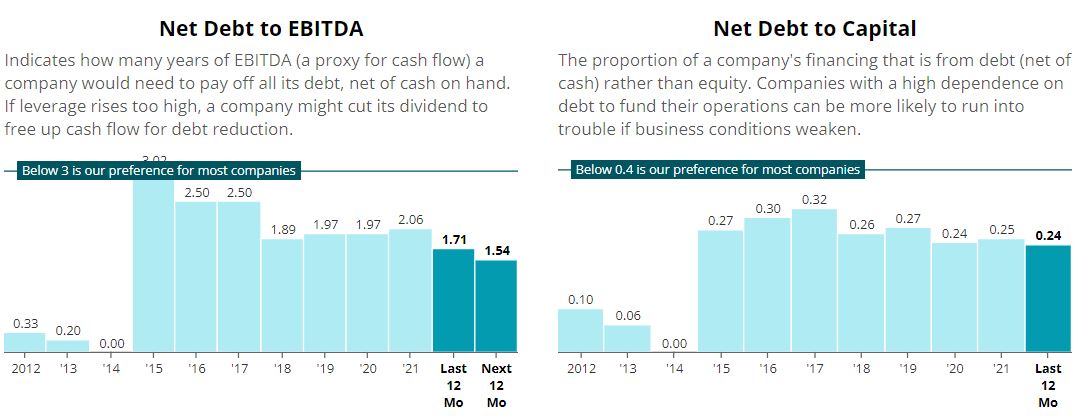

Despite the cost of innovation, research, development, and bringing products to market — and despite the lingering effects of the pandemic on Medtronic’s business — the company has managed to keep debt to a manageable level.

SimplySafeDividends.com

In the 16 months since we first bought Medtronic for the IBP, the stock has experienced total return of more than 40% — keeping with its long history of superb performance.

Investing is always a forward-looking pursuit, and Medtronic gave shareholders solid guidance during its Q1 earnings presentation. The company projected 2022 EPS of $5.65 to $5.75 — some 28% higher than the $4.44 of 2021 — as well as organic growth of 9%.

MDT = Many Dividend Thrills

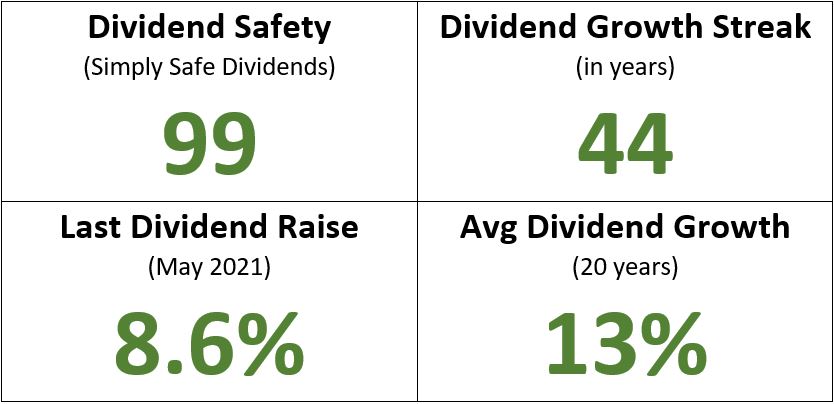

For DGI proponents, the quality of the dividend is very important … and Medtronic scores big there, too.

Obviously, any company that has been raising its distribution to shareholders annually for 44 years is committed to the dividend. But it’s still nice to hear any CEO say what Medtronic’s Geoff Martha said in announcing the latest 8.6% increase on May 27:

We’re pleased to be able to increase our dividend by 9% during the pandemic. Today’s dividend increase is a strong sign of our commitment to providing robust returns for our shareholders and of the confidence that our Board of Directors has in Medtronic’s financial strength and future growth opportunities.

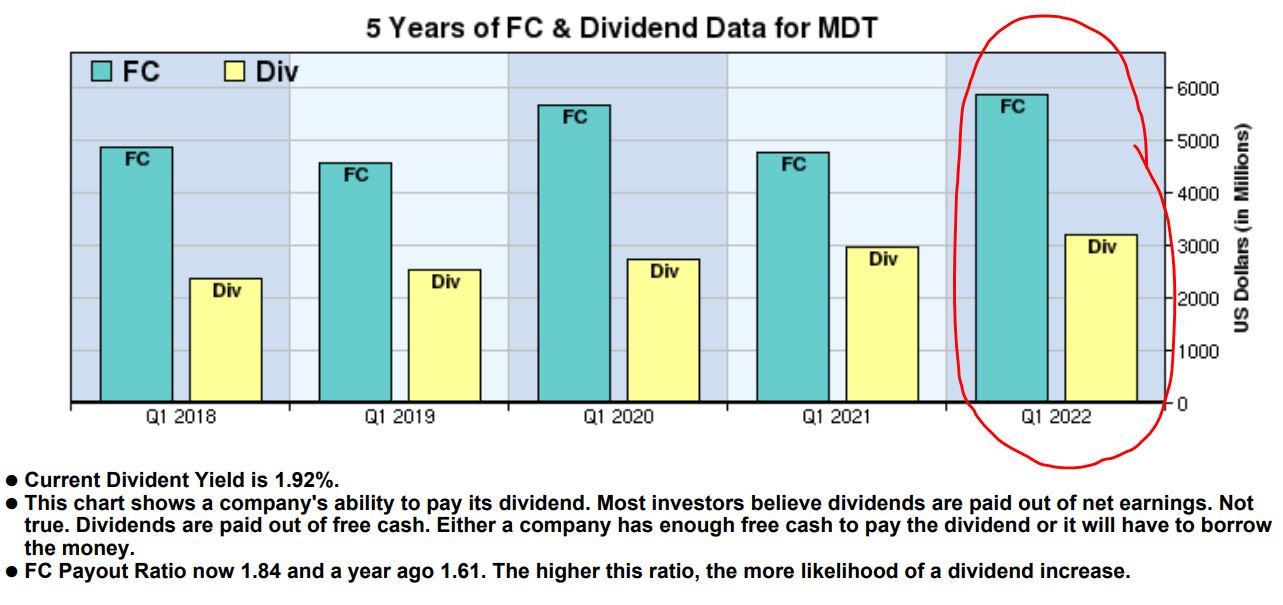

Medtronic’s dividend is well supported by the company’s consistently outstanding free-cash flow.

McLean Capital Research, via fidelity.com

The company’s FCF payout ratio is slightly higher than 50% — more than acceptable for a company that is expected to grow its free-cash flow by an average of 40% in 2022 and 2023.

Wrapping Things Up

Medtronic’s 2% yield might be a little lower than some DGI practitioners prefer, but it’s still significantly higher than the 1.3% of the S&P 500 Index.

Add in Medtronic’s four-plus decades of consistent dividend growth, its importance to medical science, and its overall high quality as a company … and we have the kind of stock we want in our Income Builder Portfolio.

I will take a thorough look at valuation and other pertinent information in my post-buy article, which is scheduled to be published Tuesday, Oct. 12.

As always, investors are urged to conduct their own due diligence before buying any stocks.

Note: I also manage the Growth & Income Portfolio for this site. Check out my most recent article HERE.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com