The word “growth” is listed first in the name of my Growth & Income Portfolio because increasing the value of the portfolio is my main objective, and I have selected several traditionally high-growth companies to do it.

If income didn’t matter to me at all, however, I’d have called it the Growth & That’s All Portfolio.

I began this project in June 2020. Given that the purpose of the GIP is to help my now 2-year-old grand-twins, Logan and Jack (aka “LoJack”), with their college costs in the late 2030s and/or early 2040s, it’s a long-term project.

And over the coming years, income will be a material part of the process.

As it turns out, September offered a nice look at how income can play a role even in a growth-focused portfolio. It was enough to make me smile like … well … a couple of happy toddlers.

That’s Logan on the left, and Jack on the right

At the end of September, the GIP’s projected annual income stream was only about $55. That’s not even enough to buy a textbook for most college courses today.

But some of the month’s developments illustrated how the income stream has grown and will continue to grow.

Four of the companies held in the portfolio announced dividend raises: Texas Instruments (TXN), Microsoft (MSFT), Lockheed Martin (LMT) and McDonald’s (MCD). Those four increases will result in about 9% more income coming into the GIP over the next year.

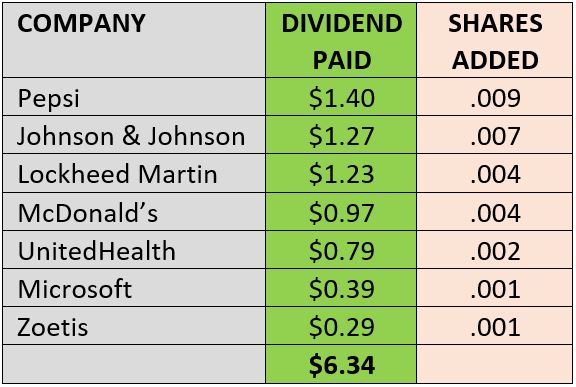

Seven positions paid dividends in September: Pepsi (PEP), Johnson & Johnson (JNJ), UnitedHealth Group (UNH), Zoetis (ZTS), Lockheed, McDonald’s and Microsoft. They generated a 14% increase in income from the $5.55 that same 7 stocks paid in June. All dividends were reinvested back into the stocks from which they came.

With those developments, LMT, MCD and MSFT demonstrated how dividend compounding works, especially when new money is constantly being dollar-cost-averaged into a portfolio. For example …

In June, the .403-share Lockheed Martin position produced $1.05 in income, which was reinvested to buy an additional fraction (.003) of a share. I bought about $25 more LMT in July and again in August, adding a total of .137 of a share.

In September, the position generated a $1.23 dividend that resulted in another share fraction coming into the GIP. And in December, the new higher dividend will be applied to .547 of a share, bringing $1.53 into the portfolio.

Over the space of two quarters, the income produced by the LMT position will have grown from $1.05 to $1.53 — 46% percent! — and that’s assuming I don’t buy more Lockheed stock between now and the Nov. 30 ex-dividend date.

Wow, what a ride! And it’s one that all of the Growth & Income Portfolio’s dividend-paying positions will experience over and over again, for years and years.

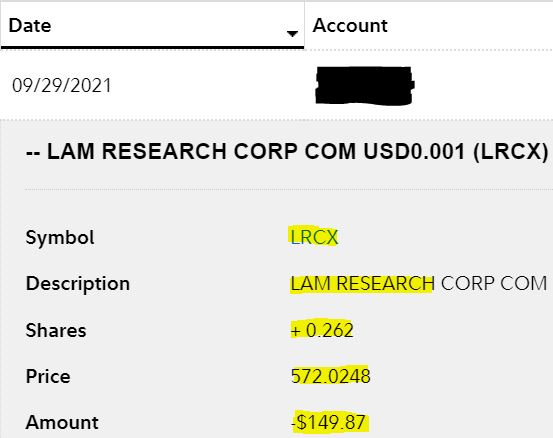

And lastly on the income front, September saw me add about $150 worth of a new business to the Growth & Income Portfolio: Lam Research (LRCX), which makes equipment for semiconductor companies. Not coincidentally, Lam had just announced a 15% dividend increase.

More on the GIP’s newest position in a minute. First, here are my six other September buys, all for much smaller dollar amounts:

The total spend on Apple (AAPL), Costco (COST), DraftKings (DKNG), Lam, McDonald’s, UnitedHealth and Microsoft was $286.98.

The purchases were made using my monthly $100 contribution and the remainder of the money that the boys’ other grandpa, Mickey, had chipped in for LoJack’s second birthday.

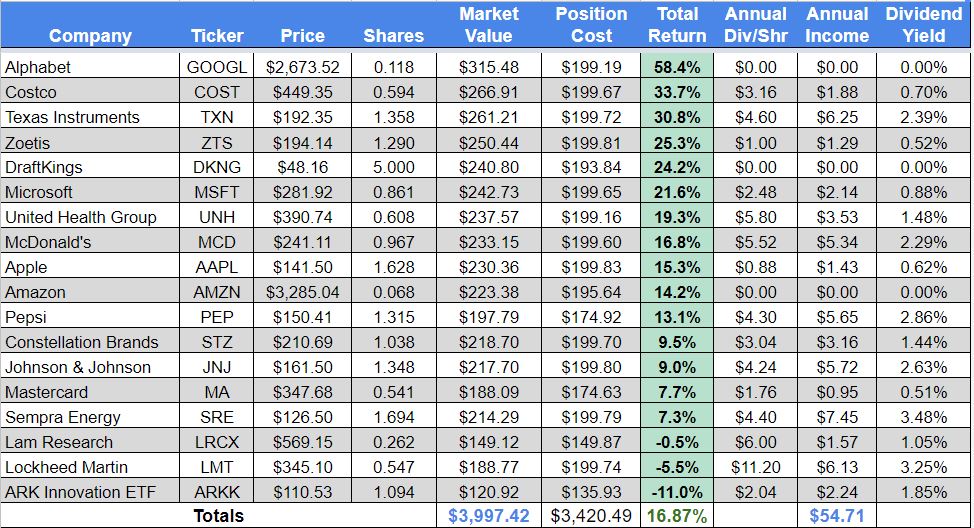

The portfolio now has 18 positions (17 stocks, one ETF), and here’s how it looked through the end of September:

That table is updated regularly and it, along with links to every article I’ve written about the GIP, can be found on the portfolio’s home page HERE.

Aside from DraftKings, a gambling-related business that just went public last year, the companies I bought during September have been considered high-quality operations for years.

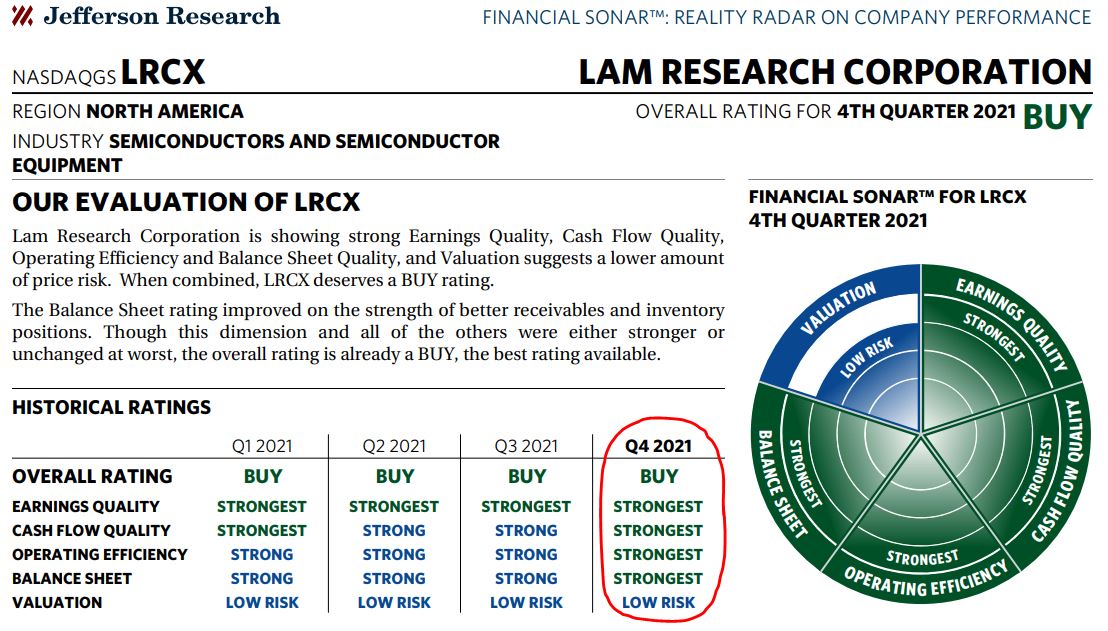

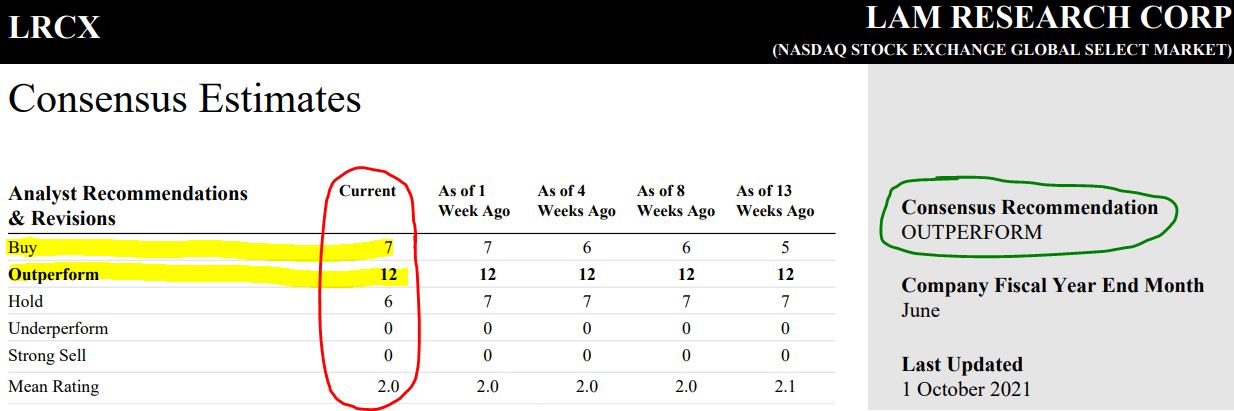

All About Lam

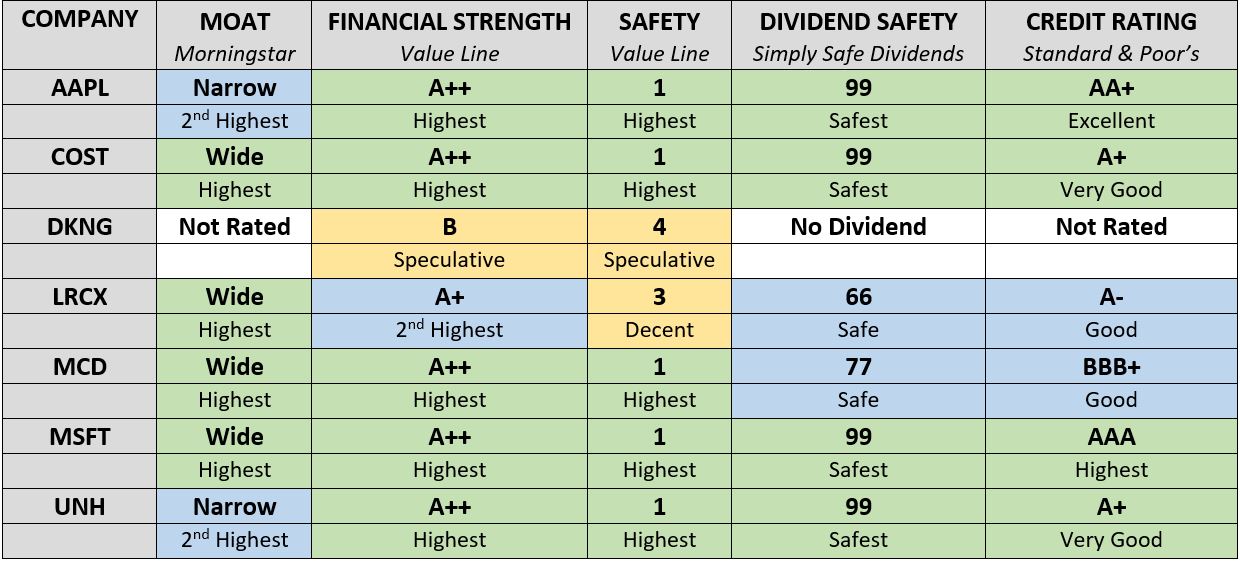

The GIP’s newest component received this very impressive assessment from analytical firm Jefferson Research:

Lam’s business can seem pretty complicated, and I don’t want to wander so far into the weeds that it will make our eyes glaze over, so I’ll start with the company’s own concise description of what it does:

Lam Research Corporation is a global supplier of innovative wafer fabrication equipment and services to the semiconductor industry. Lam’s equipment and services allow customers to build smaller and better performing devices. In fact, today, nearly every advanced chip is built with Lam technology.

The following description, by Morningstar, also keeps things simple (for simpletons like me):

Lam Research is a major vendor of semiconductor fabrication tools. The firm is the leader in dry etch, a critical step in the chipmaking process where material is selectively removed.

LRCX is a “pick and shovel company”: a business that, rather than making products for consumers, produces equipment and services for corporations.

Today’s world is run on semiconductors, and Lam’s products are absolutely essential to major chip-makers such as Micron Technology (MU) and Samsung (SSNLF).

For folks wanting still more details, here’s Reuters’ description of how LRCX makes money:

Lam Research Corporation is a supplier of wafer fabrication equipment and services to the semiconductor industry. The Company designs, manufactures, markets, refurbishes and services semiconductor processing equipment used in the fabrication of integrated circuits (ICs). It operates through manufacturing and servicing of wafer processing semiconductor manufacturing equipment segment. Its products and services are designed to help its customers build performing devices that are used in a variety of electronic products, including mobile phones, personal computers, servers, wearables, automotive vehicles, and data storage devices. Its customer base includes semiconductor memory, foundry, and integrated device manufacturers (IDMs) that make products such as non-volatile memory (NVM), dynamic random-access memory (DRAM), and logic devices. It offers its services in areas like nanoscale applications enablement, chemistry, plasma and fluidics and advanced systems engineering.

And here’s a snippet from the “Our Products” page on Lam’s website:

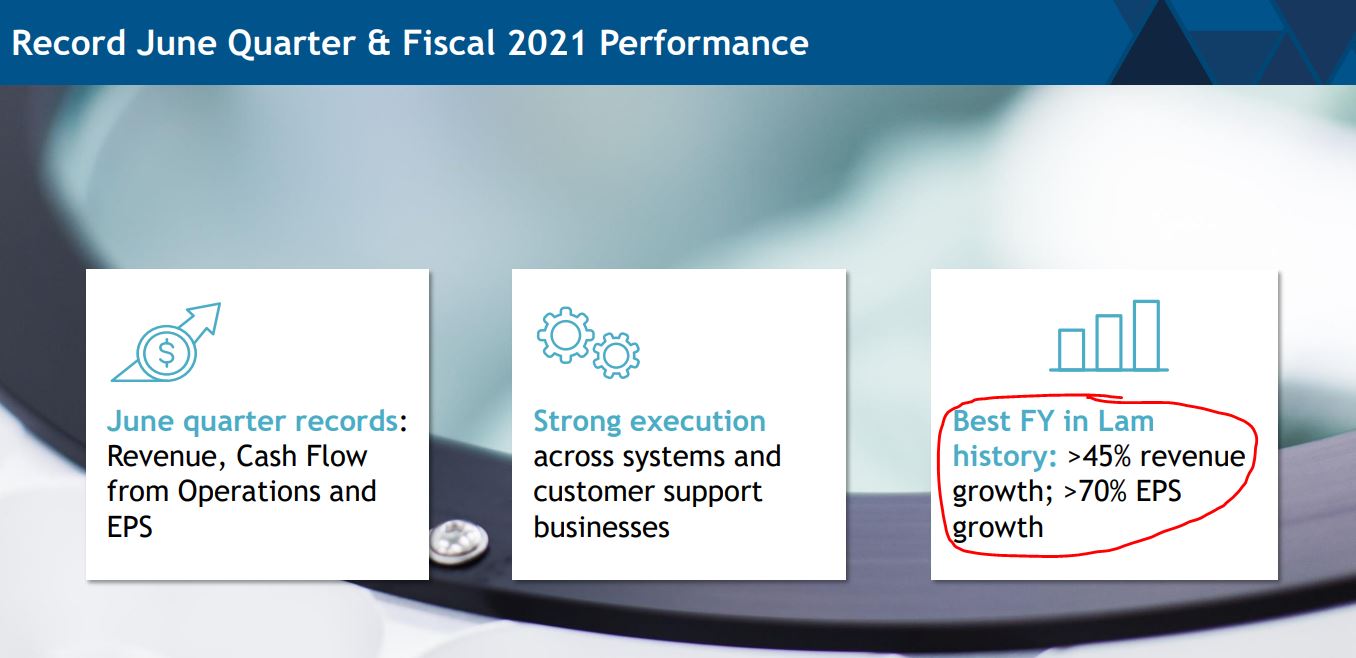

Lam reports quarterly earnings again in a couple of weeks, and that presentation should be interesting given some of the well-publicized challenges facing the semiconductor industry.

Despite those challenges, LRCX had a stellar earnings report last quarter.

lamresearch.com

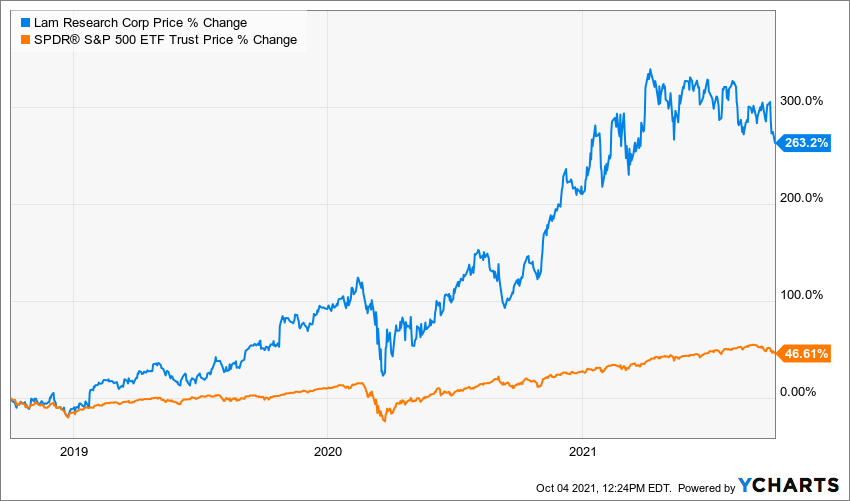

As a result of all that success, LRCX has crushed the market the last three years.

Valuation Station

So, after that run-up, is the stock still “buyable”? Most analysts say yes.

Reuters, via schwab.com

It’s worth noting that, with the overall market trending down the last few sessions, LRCX’s price has gotten a little more attractive: $550.14 at market close on Monday, Oct. 4.

Expanding the discussion beyond Lam Research, here’s a table showing analyst price targets and other valuation information for my seven September buys:

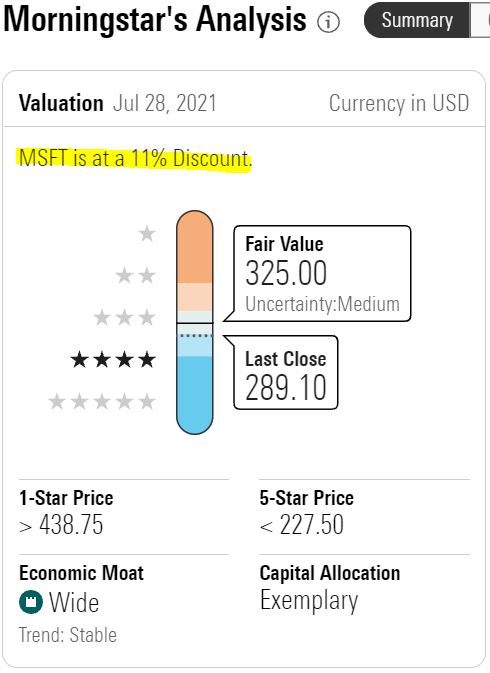

A quick look at forward price/earnings ratio suggests that Microsoft is extremely overvalued. But the rest of the MSFT row on the table shows that analysts disagree, with all of them saying there’s still plenty of room for the stock price to run over the next 6-18 months.

Morningstar, which often is conservative in its assessments, actually thinks MSFT is quite undervalued.

Others of this group I would consider attractively valued are Lam and DraftKings, though cases could be made for all of them.

Similarly, cases could be made that several are overvalued, so I strongly urge investors to conduct their own thorough due diligence.

Wrapping Things Up

I was going to use a groan-worthy play on words — something like, “For the Growth & Income Portfolio, September came in like a lion and went out with a Lam Research.”

LoJack, with Logan holding his prized lion “friend”

But that would have been a real shameless way to squeeze one more photo of my adorable grand-twins into this article, and I’d never do anything like that!

Lam’s dividend has increased some 400% since 2015, making it the GIP’s latest example of a company that rapidly grows earnings, revenue and income. Those things need not be mutually exclusive … and they certainly aren’t for this welcome addition to the portfolio.

Note: For more dividend-centric investors, I also manage the real-money Income Builder Portfolio; see the home page HERE. In addition, I regularly do YouTube videos about the IBP for our Dividends And Income Channel; check out my latest HERE.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com