I don’t know if the folks running McCormick (MKC) can sing like Led Zeppelin, but the spice-maker’s version of “Stairway to Dividend Heaven” is sweet music to many income investors.

As a Dividend Growth Investing proponent, I love it when a company’s distribution history has that kind of long, gradual, beautiful staircase pattern.

Such dividend reliability was a big reason I decided to add to the Income Builder Portfolio’s MKC stake … and on Monday, July 26, I executed a limit purchase order on this site’s behalf for 12 shares at $85.25 apiece.

(As can happen with limit orders, the buy executed via two transactions a split-second apart.)

With MKC paying a dividend of $1.36/year, these 12 new shares will generate $16.32 in annual income for the IBP.

That pushes the overall portfolio’s annual income stream past the $3,000 level. Woo-hoo!

The IBP’s “Income Target,” as outlined in the Business Plan, is to “build a portfolio that will produce at least $5,000 in annual dividends within 7 years of the IBP’s (January 2018) inception.”

That means we are some 60% of the way to the target even though we are only about halfway through the designated time period.

Why $5,000 in 7 years? Well, we needed something to shoot for, and a target that assumes 5% annual dividend growth and a 2.5% yield seemed both realistic and ambitious enough.

As we say in the Business Plan:

Many investors will have (and should have) a longer time frame in mind. Indeed, DGI is a long-term strategy that truly bears fruit after years (or better yet, decades) of compounding.

Nevertheless, we are realistic enough to know that this project might not last for multiple decades, so we are choosing a shorter time frame as the Income Target.

So $3,000 is a major milestone … and it’s fitting that one of the portfolio’s most dependable dividend growers put us over the top.

![]()

McCashin’ In

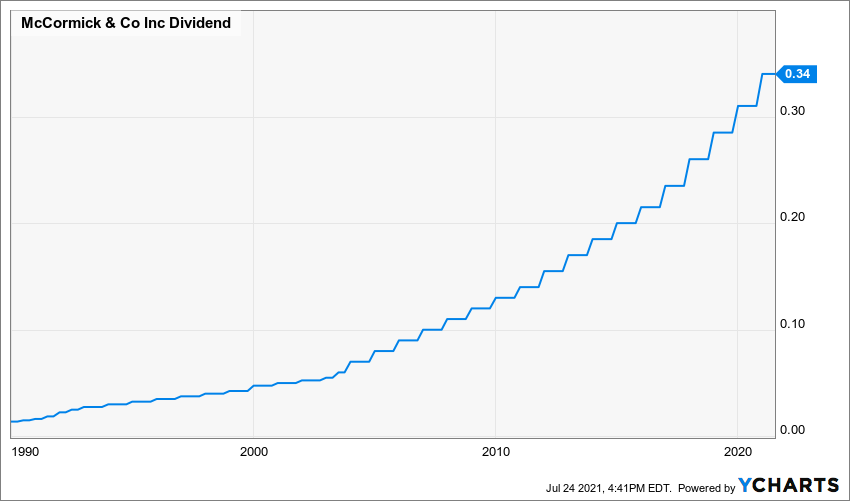

As the Stairway to Dividend Heaven chart at the top of the article indicates, McCormick is a Dividend Aristocrat that has been growing its payments to shareholders for 34 years.

The consistency of management’s commitment to increasing investors’ income has been particularly impressive, as MKC has averaged 10% dividend growth over 20 years … 9% over 10 years … 9.2% over 5 years … and 9.7% over 3 years.

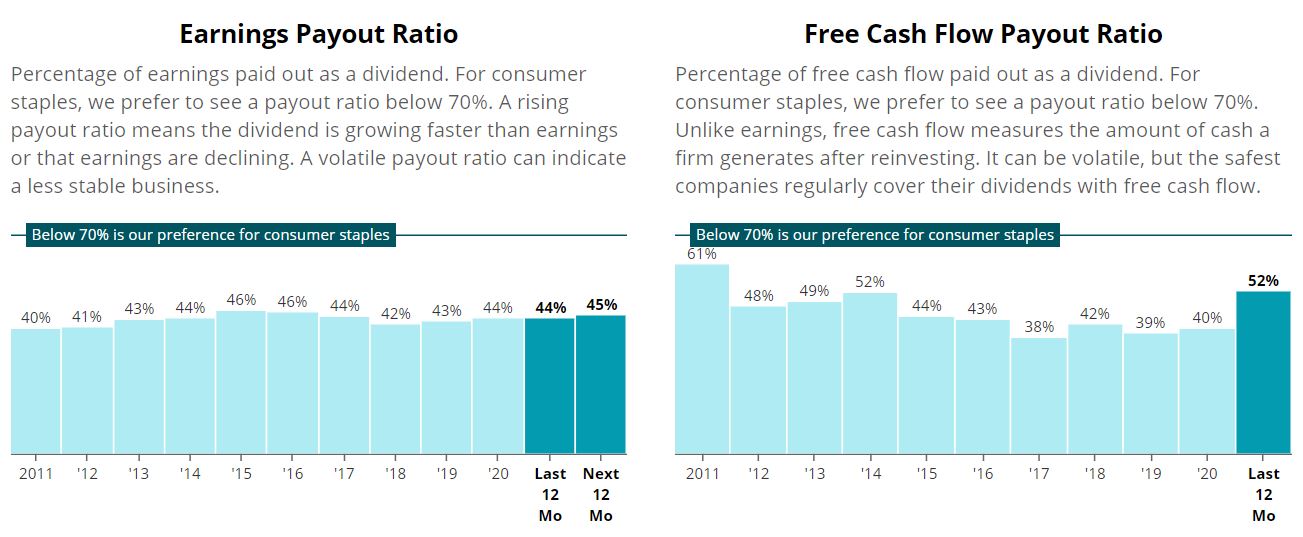

And with McCormick’s leaders keeping close tabs on the company’s payout ratios, there is every reason to be confident that many more years of dividend hikes are in the offing.

SimplySafeDividends.com

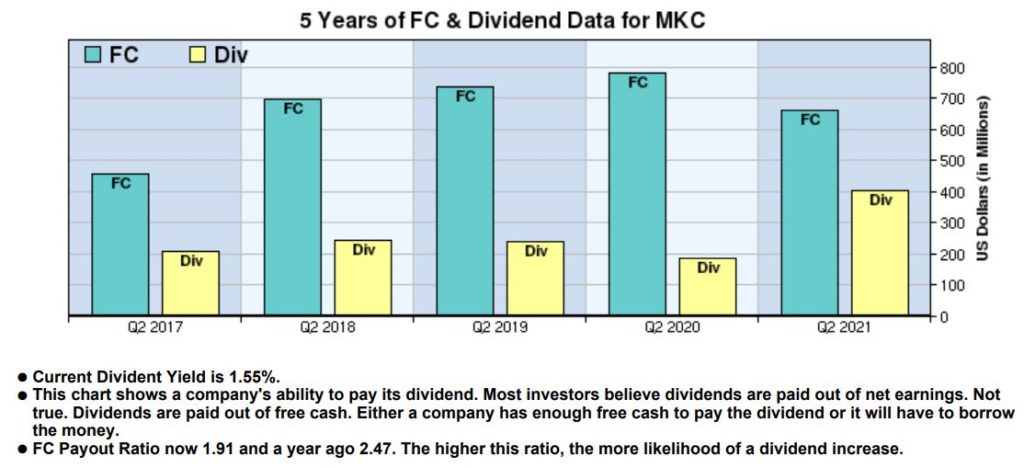

Year after year, McCormick has easily generated enough free cash flow to cover its dividend … so even though its 1.6% yield is a little low for some DGI practitioners, they can feel secure that the raises will keep coming.

McLean Capital Research, via fidelity.com

The IBP just received McCormick’s second-quarter payout, with our then-20.912 share position generating $7.11 in income. That was reinvested right back into the company — a process informally called “dripping” — adding about .083 of a share.

Including Monday’s purchase, the IBP now has approximately 32.995 shares of MKC. In October, that will produce $11.22 in dividends, which again will be dripped, buying an additional fraction of a share.

And if history is any guide, McCormick will announce its 35th annual dividend raise around Thanksgiving.

Invest … drip … grow. That’s what McCormick does, and that could be this project’s mantra as we build a predictable, rising income stream.

Valuation Station

As I mentioned in my previous article, MKC has been one of the IBP’s total-return leaders since we first bought it in May 2018. But as I also said, I hadn’t chosen McCormick again for the portfolio because “it almost always seemed overvalued.”

Over the last 11 months or so, MKC’s price has fallen almost 20%, a drop I believe has a lot to do with the stock having been so overvalued.

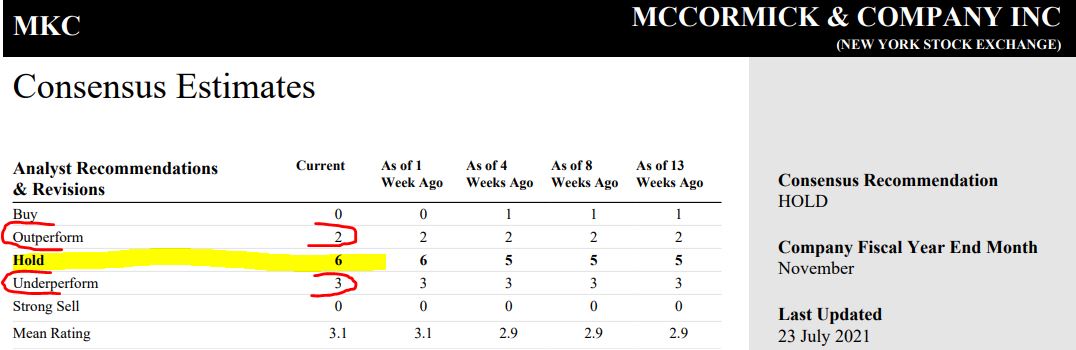

Even at the $85.25 we paid Monday, McCormick’s forward P/E ratio of about 28 indicates it still isn’t exactly in the bargain bin … and that’s reflected in what some analysts say about the stock.

For example, the consensus of 11 analysts surveyed by Reuters is that MKC is a “hold” — with only 2 expecting it to outperform the market over the next year, compared to 3 who say it will underperform.

Reuters, via schwab.com

Morningstar’s analysts like the well-run, wide-moat company but say it remains extremely overvalued.

morningstar.com

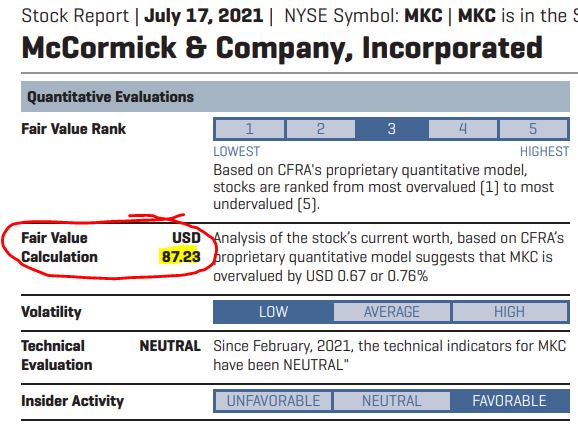

CFRA, on the other hand, says MKC is fairly valued to slightly undervalued.

CFRA, via schwab.com

In calling MKC a low-risk investment, CFRA’s Arun Sundaram said:

Our risk assessment is low as MKC competes in the relatively stable operating environment that is the packaged foods industry. Additionally, MKC has a strong balance sheet and proven track record of generating strong free cash flow. Its margin profile is in the top quartile of its packaged food peers, and MKC is the industry leader in the spices category.

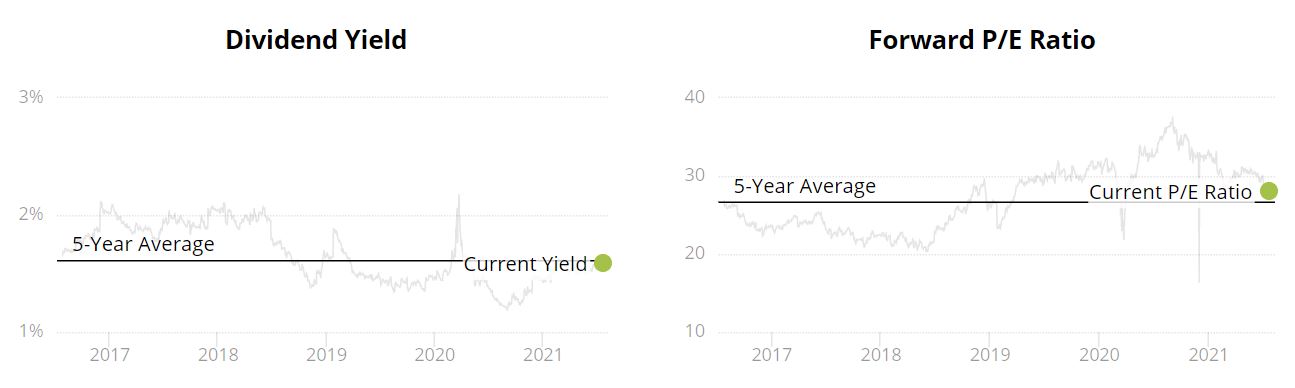

Simply Safe Dividends agrees that McCormick is fairly valued, saying the yield and forward P/E are in line with the firm’s 5-year averages.

SimplySafeDividends.com

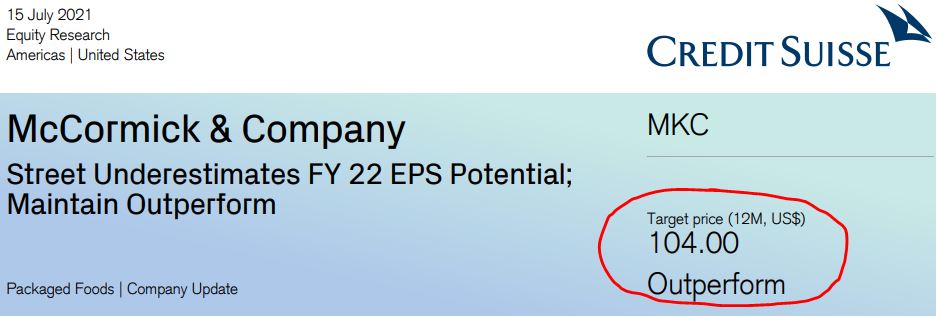

Meanwhile, Credit Suisse’s analytical team is bullish on the company and expects its price to appreciate by more than 20% over the next 12 months.

Credit Suisse, via schwab.com

In establishing that target price, Credit Suisse said:

What does the market need to see to re-embrace this stock? We think the … pullback in the stock this year reflects concerns that McCormick will face tough comparisons just like every other food company once consumers return to pre-COVID consumption patterns and that operating margins will contract due to cost inflation. … We think the stock will regain momentum after management articulates these tailwinds and provides more visibility into next year’s outlook. … Our target price of $104/share assumes a 28x P/E multiple against our 2023 EPS estimate. This is roughly in-line with stocks that have leadership position in attractive niche markets.

Value Line has an 18-month target price for MKC that reflects a 35% gain, which is similar to the top of its 3-5 year range.

valueline.com

In addition to giving MKC its top “Safety” score (1) and a high Financial Strength rating (A+), Value Line assigns McCormick excellent scores within its 1-100 scales for Earnings Predictability (100), Price Stability (95) and Price Growth Persistence (85).

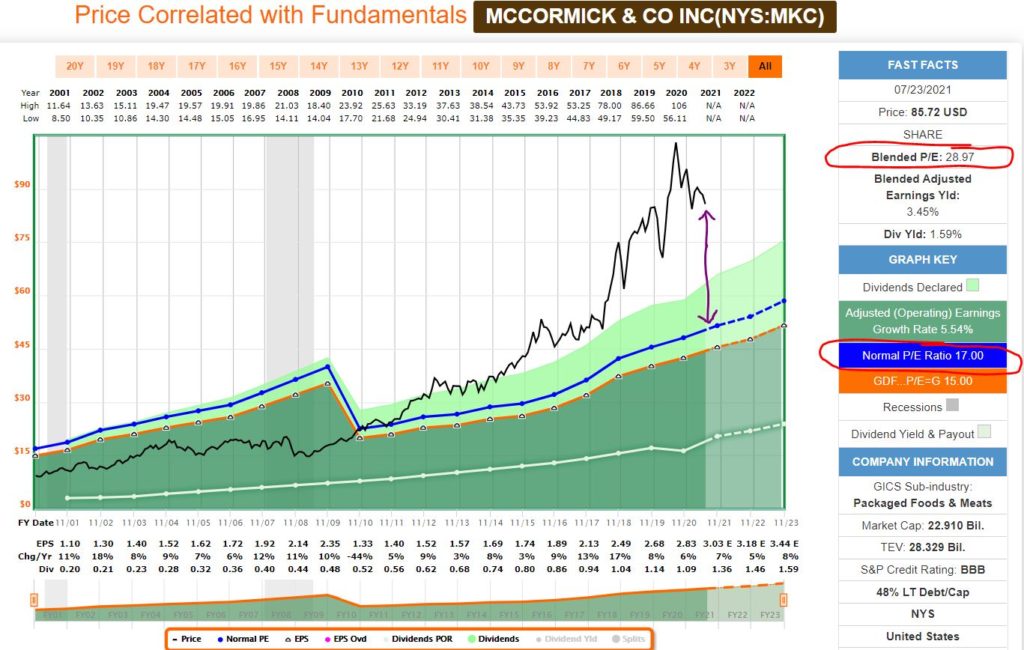

Finally, let’s take a look at what a couple of FAST Graphs illustrations suggest.

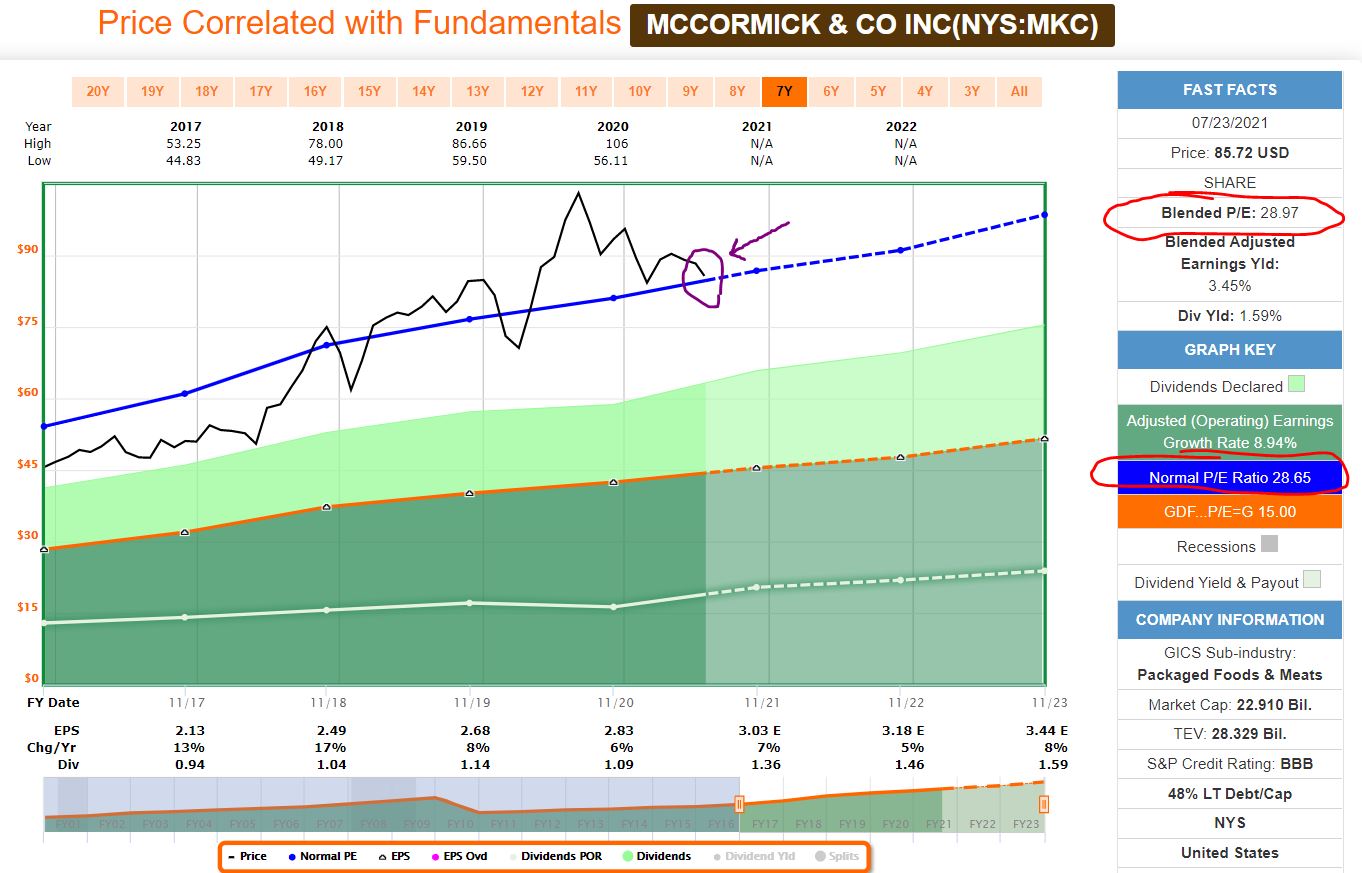

If you use McCormick’s two-decade history, there is little doubt the stock is overvalued now — its blended P/E ratio is significantly higher than its norm (red circles), and the end of the black price line sits much higher than the blue line that represents the average valuation over the period (purple arrow).

fastgraphs.com

However, if we focus on the most recent 5 years, when prices have been spicy for not just McCormick but for the entire market, we see that the price and normal valuation lines are almost touching (purple circle) and the current P/E ratio and 5-year norm are almost identical (red circles).

fastgraphs.com

Wrapping Things Up

When I look at all of the valuation information presented above, I can’t sit here and claim that McCormick is a great buy. Nevertheless, I can see why Value Line analyst William Ferguson came to the following conclusion in his July 16 write-up about the company:

High-quality McCormick stock remains an appealing option for those with an 18-month investment horizon. And even with the neutrally ranked issue recently trading at 29 times our 12-month forward-looking earnings estimate … MKC’s high Price Stability score may provide some comfort for those considering a commitment.

As such, I feel good about increasing the size of the Income Builder Portfolio’s MKC position, and I look forward to watching as it continues to climb the Stairway to Dividend Heaven.

Note: See all 43 IBP positions on the portfolio’s home page HERE. Also, take a look at the other real-money project I manage for this site, the Grand-Twins College Fund, HERE. And for even more about IBP and GTCF holdings, as well as discussions about the portfolio-building process, please check out my YouTube videos on our Dividends And Income Channel; the most recent video is HERE.

— Mike Nadel

Source: DividendsAndIncome.com

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.