With momentum and growth investing dominating, value investing has been out of favor for quite some time … so I’ll be very interested in seeing how my latest pick for the Income Builder Portfolio fares in the months and years to come.

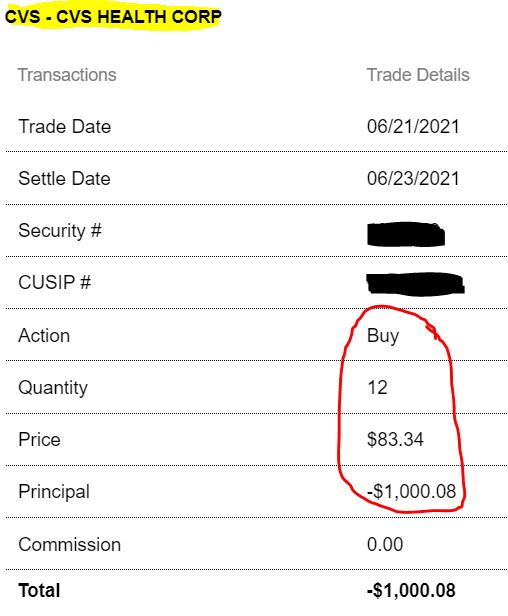

On Monday, June 21, I executed a limit order on behalf of this website for 12 shares of CVS Health (CVS) at $83.34 apiece.

CVS stock looks like a bargain. That makes it different from most of our recent buys — and, given the trend, most recent buys by most investors.

When I formulated the IBP Business Plan some 3 1/2 years ago, I included this passage:

A stock’s valuation will be strongly considered before each purchase, but the perceived quality of the company is of utmost importance.

An investor making sizable additions to a large, established portfolio might be primarily concerned with valuation. The IBP, however, is a DGI (Dividend Growth Investing) portfolio that will be built over time through regular $1,000 purchases – similar to the concept of dollar-cost averaging.

In following that plan, I sometimes have had to acknowledge how difficult it’s been to find high-quality companies at appealing valuations.

Just a month ago, for example, I opted to add to our positions in credit-card twins Visa (V) and Mastercard (MA) — despite the fact that they were trading at 40 to 50 times projected earnings.

Good Company, Good Buy

CVS becomes the portfolio’s 42nd company, and the sixth from the Health Care sector.

In addition to operating a well-known chain of drug stores, CVS is a leading health-insurance provider and a major pharmacy benefit manager.

In my previous article, I explained why I consider it a high-quality business. Now, let’s take examine why it looks like a good value.

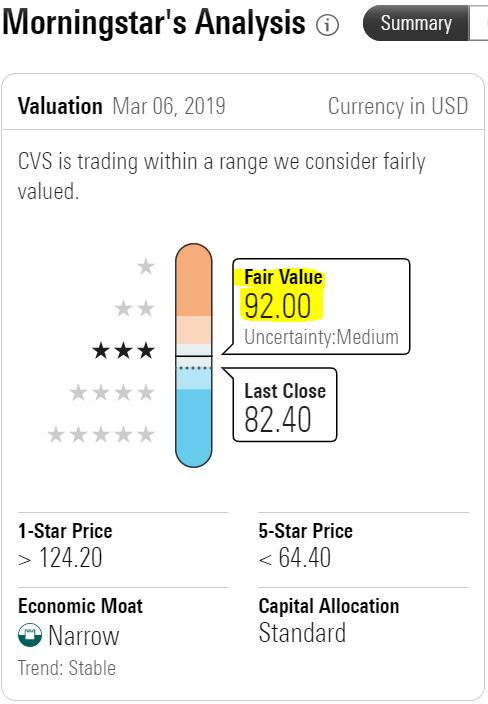

Morningstar Investment Research Center says the stock’s fair value is more than 10% higher than the price we just paid for our stake.

morningstar.com

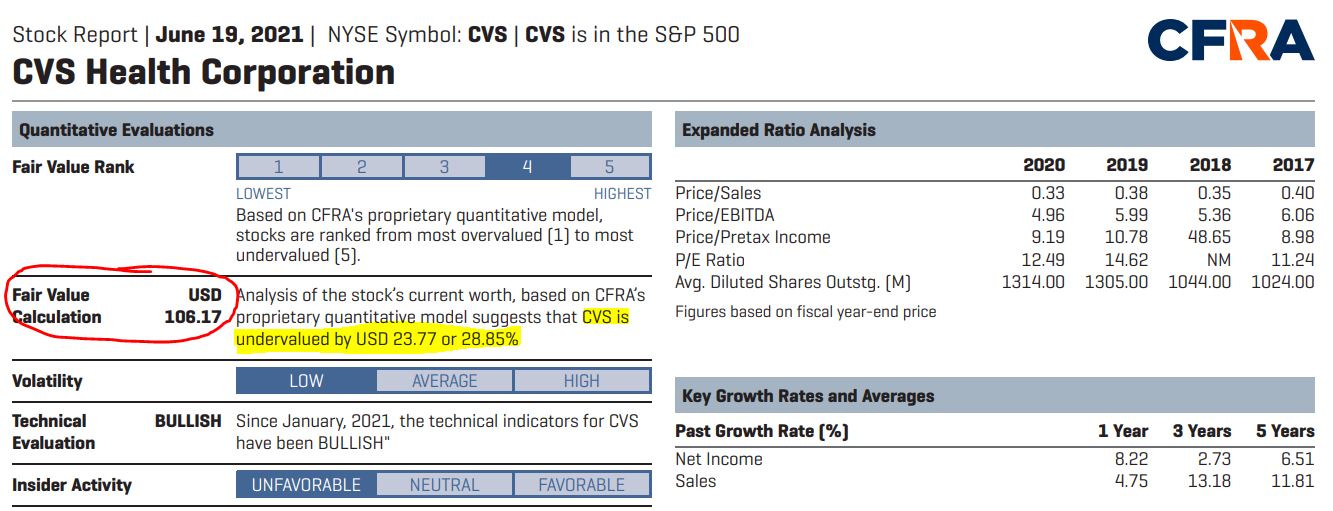

Another analytical firm, CFRA, calculates CVS Health’s fair value at about $106 share; so they think we bought the stock for the IBP at nearly a 30% discount.

CFRA, via schwab.com

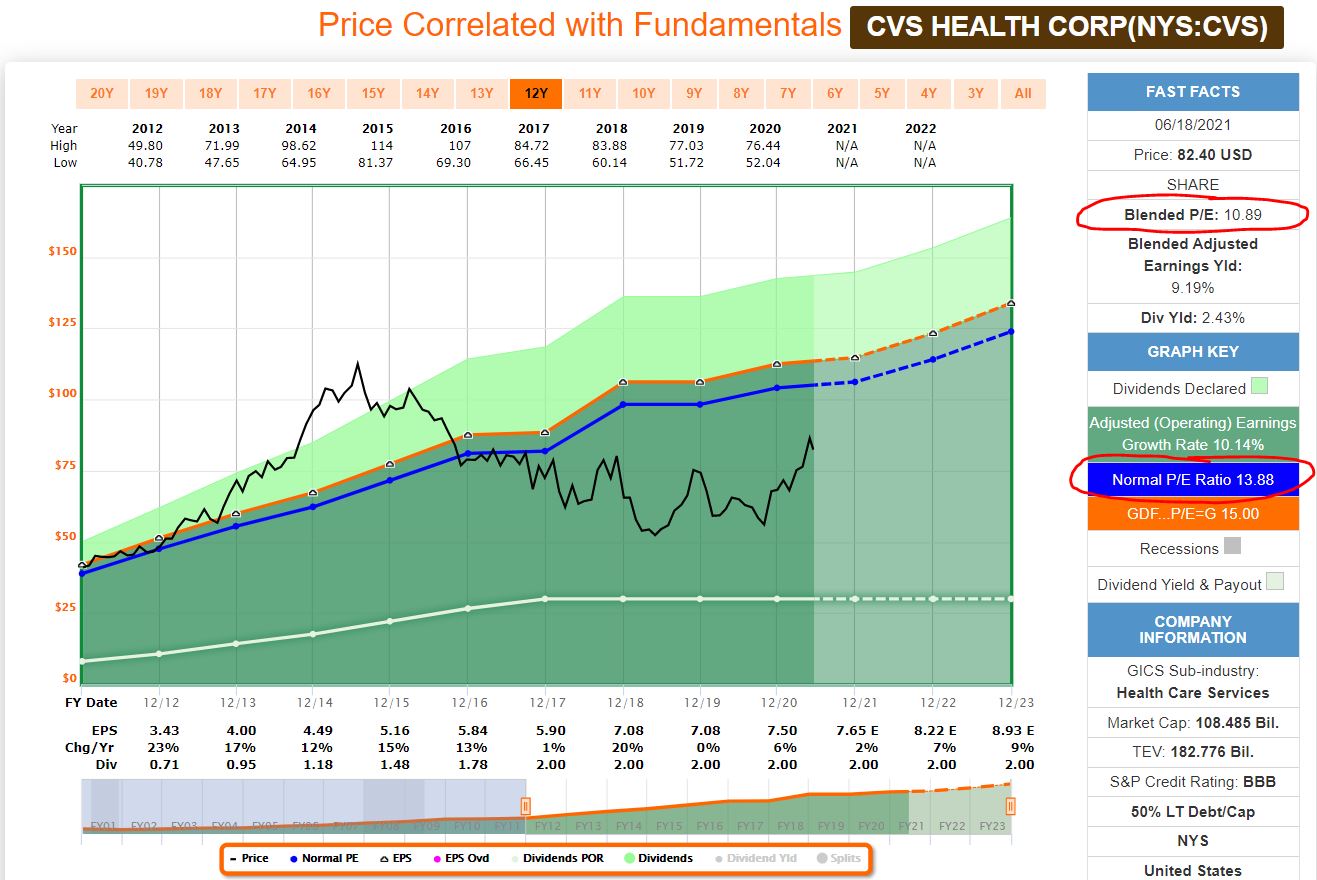

According to FAST Graphs, CVS has a “blended price/earnings ratio” of about 11; that’s significantly lower than its 14-ish norm over the last decade or so.

Furthermore, the end of the black price line on the FAST Graphs illustration — representing the company’s closing price of Friday, June 18 — sits well below the blue normal P/E ratio line.

fastgraphs.com

CVS is poised for steady earnings growth as it emerges from the pandemic — with a 2% estimated EPS increase this year, followed by 7% in 2022 and 9% in 2023.

That’s not turbo-charged growth by any means, but it’s acceptable for a large company that is paying down debt from recent major acquisitions.

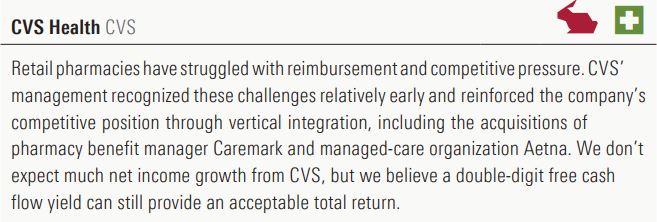

Morningstar thinks enough of CVS Health’s growth prospects to have included the company in its “Hare Portfolio.” Here is the accompanying capsule:

morningstar.com

Analyze This!

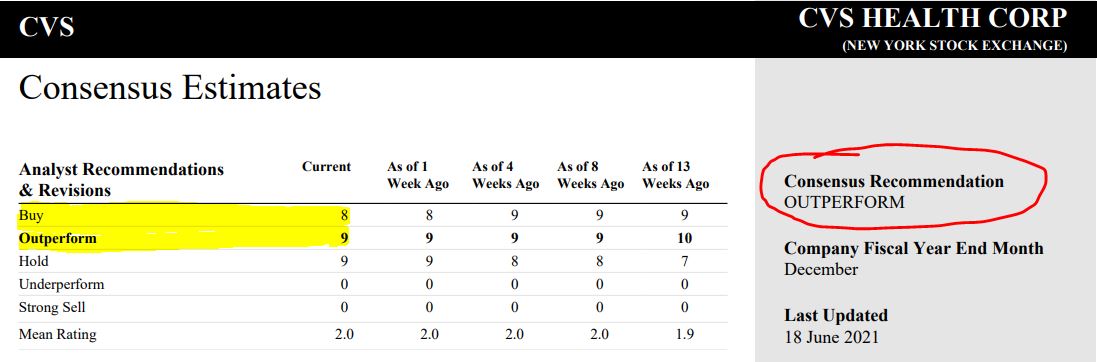

The majority of market-watchers who follow CVS are bullish on the business.

Of the 18 analysts surveyed by TipRanks, 14 say CVS is a buy, and their average target price suggests a 13% upside.

tipranks.com

There’s a similar story with the analysts surveyed by Reuters, with 17 of 26 giving CVS either a buy or outperform rating.

Reuters, via schwab.com

Specific analysts’ target prices include: RBC, $101; Credit Suisse, $100; Barclays, $100; Deutsche Bank, $99; Mizuho Securities, $98; BMO, $96; Jefferies, $95; DA Davidson, $95; Argus, $95; Raymond James, $95; Wolfe Research, $93; CFRA, $91; RBC, $91; UBS, $90; Zacks $90; Wells Fargo, $89.

Most of those targets were the results of upgrades after CVS announced May 4 that it had beaten Q1 earnings estimates and that it was raising full-year guidance.

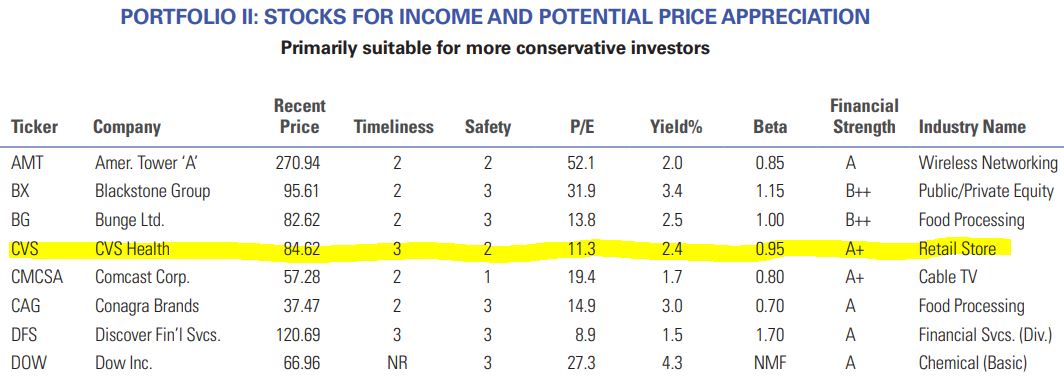

Value Line has a 3-5 year target price ranging from $95 to $130, and it has included CVS in its model portfolio of Stocks for Income and Potential Price Appreciation.

valueline.com

And Speaking of Income …

Referring again to the IBP Business Plan, the stated goal was simple:

Build a reliable, growing income stream by making regular investments in high-quality, dividend-paying companies.

So far, so great … as the projected annual income stream has grown to almost $3,000.

The IBP’s Income Target is $5,000 within 7 years … so at the exact halfway point, the portfolio is just about 60% of the way there. Nice!

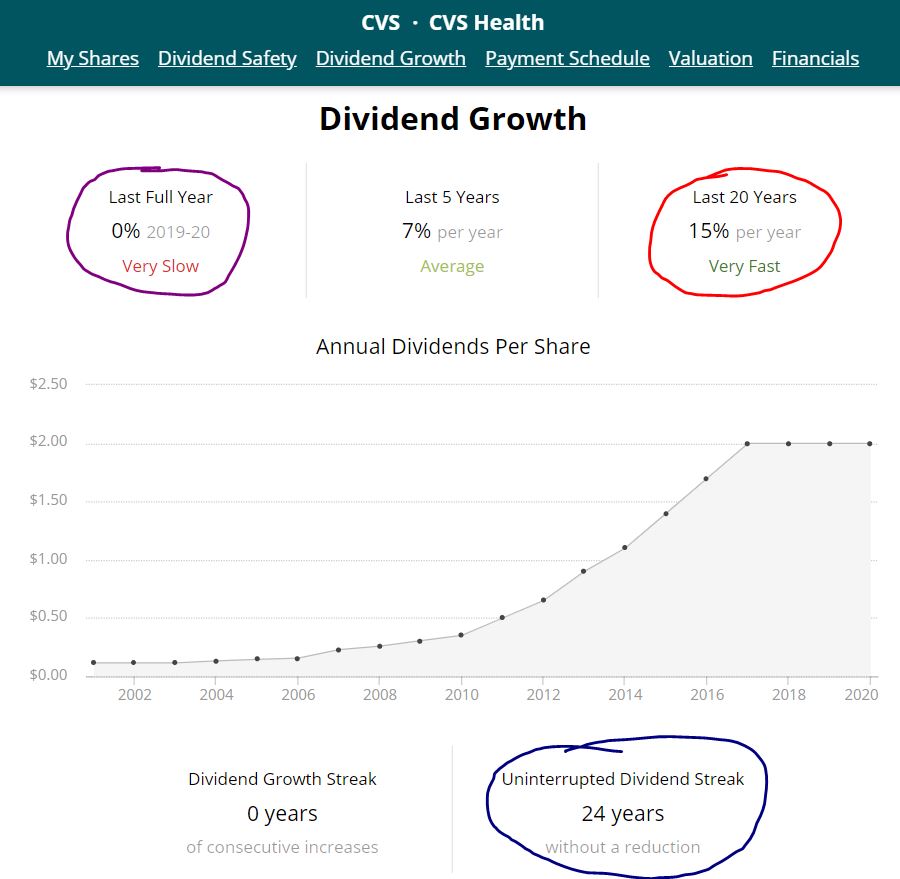

CVS has been a reliable dividend-payer, with a 24-year streak of never having reduced its payout. But the company’s dividend growth has stalled the last few years, as it has been using excess cash to pay down debt.

SimplySafeDividends.com

Simply Safe Dividends says CVS Health’s dividend is “safe,” assessing a score of 67 on a 1-to-100 scale. That’s a little lower than I prefer, but still adequate.

As the company’s financial picture improves, specifically as it rapidly pays down debt, I’m optimistic that dividend growth (and improved “safety”) will follow.

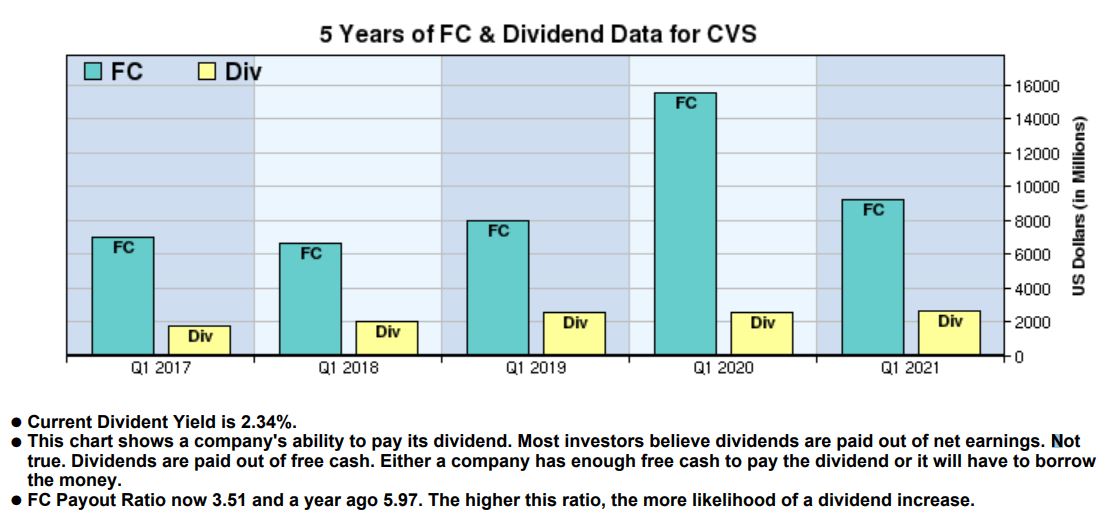

Year after year, CVS has generated plenty of free cash flow to cover its dividend.

McLean Capital Research, via fidelity.com

CVS pays a $2/share annual dividend, so our position is expected to generate $24 during the next year.

The IBP will receive a $6 quarterly dividend in early August. That will be reinvested back into the company, as per portfolio rules, bringing in about .07 of a share more CVS stock.

Then, three months later, the new higher share total will generate slightly more income — a process that will be repeated over and over again, not only with CVS but with all 42 IBP positions.

And that’s why we gave this endeavor the name we did.

Wrapping Things Up

Eight months ago, CVS was more than just a garden-variety value investment. It was trading at about $56, and it could have been called a deep-value or “turnaround” play.

It would be easy to say that I should’ve selected it for the IBP back then … but it’s always easy to say such things in hindsight.

I was concerned that the stock might be a “falling knife,” so I went with proven performers BlackRock (BLK) and UnitedHealth Group (UNH) instead — and they have continued to excel.

Fundamentally, CVS appears to be on solid ground now, and the stock’s valuation suggests that it still has plenty of room to run.

Throw in a dependable dividend that very well could start growing again, and we have a company we’re glad to have added to the Income Builder Portfolio.

Note: I also manage my Grand-Twins College Fund, a “growth-and-income” portfolio that includes the likes of Alphabet (GOOGL), DraftKings (DKNG), Texas Instruments (TXN) and Costco (COST). I plan to write a GTCF update in early July; until then, check out the home page HERE. I also have been making videos about the GTCF and IBP for Dividend And Income’s YouTube channel; see the most recent video HERE.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com