Everybody loves a good contest, right? As an investor, I certainly do — especially when I own both combatants, and both are big winners.

Last year, within the Income Builder Portfolio, I set up a friendly “competition” between Mastercard (MA) and Visa (V), the financial technology duopoly that dominates the credit-card industry.

We bought shares of both companies twice in 2020 — on April 21, and then a month later on May 21, the latter using proceeds from our Disney (DIS) divestment.

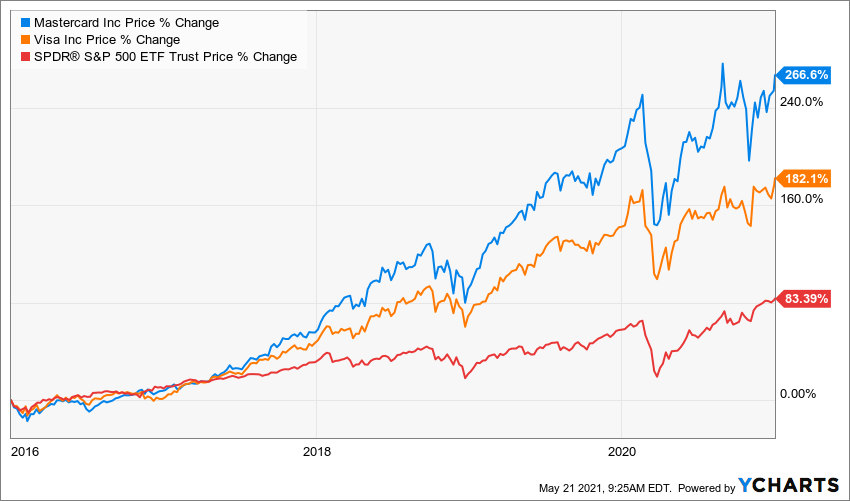

And now, exactly one year after that most recent purchase, the leader is …

As you can see, although Mastercard has been the winner so far, there has been no “loser.”

So let’s keep playing, kids!

Come Monday, May 24, I will split Daily Trade Alert’s $1,000 monthly IBP allocation between MA and V, executing purchase orders of each company’s stock on DTA’s behalf.

That Mastercard is ahead in the contest might surprise those who consider Visa the dominant company — which Visa is by market cap, total profits and total sales.

However, as a stock, MA outshined V from 2016-2020.

Indeed, Mastercard outgained Visa in every single one of those years, including 19.5% to 16.4% in 2020.

So why even bother owning Visa, then? Wouldn’t the Income Builder Portfolio have done even better had we invested all $2,000-plus in Mastercard last year?

Well sure, but it’s easy to make such calls using hindsight.

Additionally, just because something happened in the recent past doesn’t mean it always has been that way or that the trend necessarily will continue.

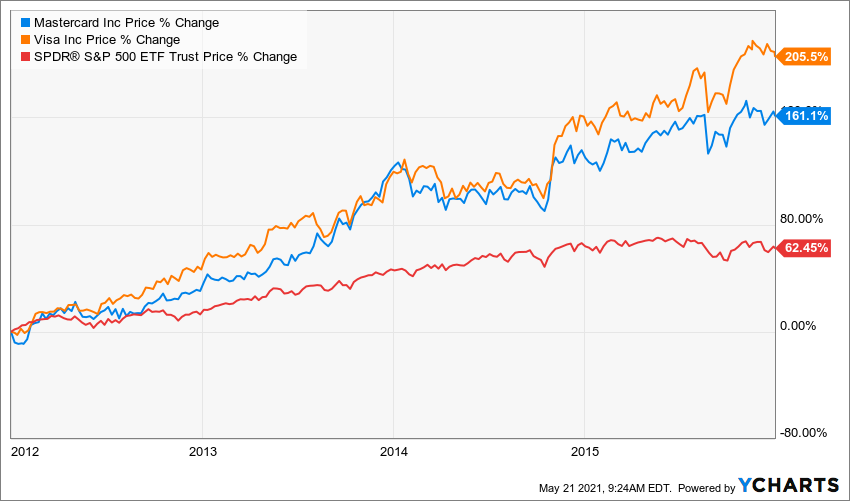

From 2012-15, in fact, it was Visa and not Mastercard that won the stock-performance showdown — so an investor who said, “This has to continue,” and ignored MA would have lost out on some sweet gains over the next 5 years.

And so far in 2021, Visa has the slight edge, with a 3.7% gain to Mastercard’s 3.0%.

When two fine companies rule an industry, I like owning both because it’s difficult to predict which will shine brightest in the future. (Disclosure: I own V and MA in my personal portfolio, too.)

All About Quality

I am all about picking outstanding businesses for the IBP, and it’s almost impossible to find companies with better “quality metrics” than Mastercard and Visa.

Furthermore, Morningstar includes both in its Hare Portfolio, which “seeks long-term capital appreciation by investing in companies with strong and growing competitive advantages” and which uses a “growth at a reasonable price strategy, looking for companies with above-average earnings-per-share growth whose stocks are trading at reasonable multiples of long-term earnings potential.”

Here are Morningstar’s capsules on MA and V:

- Few companies can match Mastercard’s record of consistent, rapid revenue and earnings growth. Mastercard benefits from consumers spending more on their credit, debit, and prepaid cards without taking on any consumer credit risk. The company has done an excellent job of adapting to new trends, such as mobile payments and virtual cards, while pursuing new opportunities such as business-to-business and fast ACH transactions. We’re still in the very early innings for these latter opportunities.

- Visa’s story is similar to Mastercard’s, with a very strong competitive position, secular growth tailwinds, and significant operating leverage owing to fixed costs. The EBITDA margin is around 70%—an almost unheard-of level of profitability. Still, Visa’s management has been less aggressive than Mastercard’s in pursuing new opportunities (like business-to-business transactions), and the company’s greater size and less favorable business mix results in somewhat slower (though still impressive) growth.

Meanwhile, Value Line lists both MA and V among its 100 Highest Growth Stocks, stating: “To be included, a company’s annual growth of sales, cash flow, earnings, dividends and book value must together have averaged 9% or more over the past 10 years and be expected to average at least 9% in the coming 3-5 years.”

Only 13 of the 100 receive VL’s highest “safety” score, a group that includes not only Mastercard and Visa but also fellow IBP components Apple (AAPL), Microsoft (MSFT), Sherwin-Williams (SHW) and UnitedHealth Group (UNH).

Value Line also features Mastercard on its list of stocks with High Returns Earned on Total Capital, while including Visa in its model portfolio of Stocks with Long-Term Price Growth Potential.

Given the financial strength of each company, it’s not surprising that MA and V appear on so many lists of top investments.

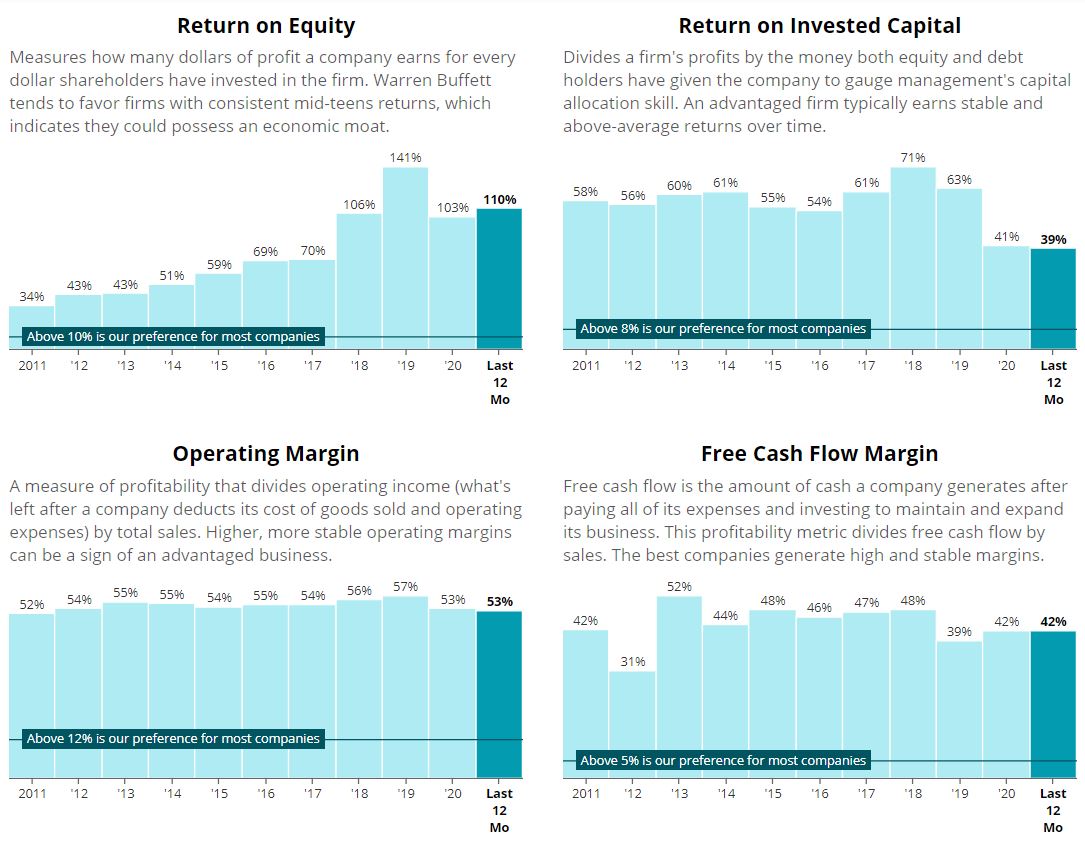

Over the last decade, Mastercard’s financial performance has been astonishingly good.

Simply Safe Dividends

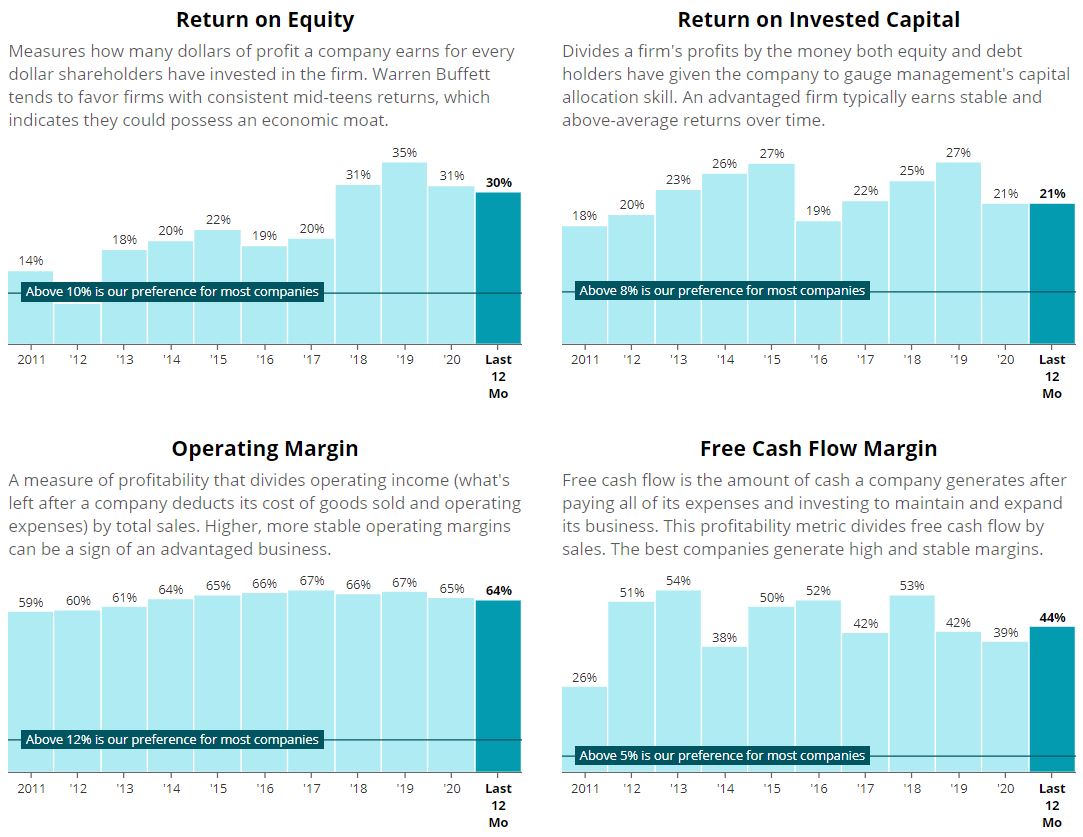

And Visa certainly has been no slouch, actually surpassing Mastercard in operating margin and FCF margin most years while also doing superbly in ROE and ROIC.

Simply Safe Dividends

The companies have similarly brilliant business models: Unlike American Express (AXP) and Discover (DFS), Mastercard and Visa issue credit cards through banks. So MA and V do not need to operate as banks, nor do they need to worry about lending money; they earn their profits through service and data processing fees.

Still, as wonderful businesses as they have been, both have been challenged during the COVID-19 pandemic.

As Morningstar said of Mastercard in its May post-earnings update:

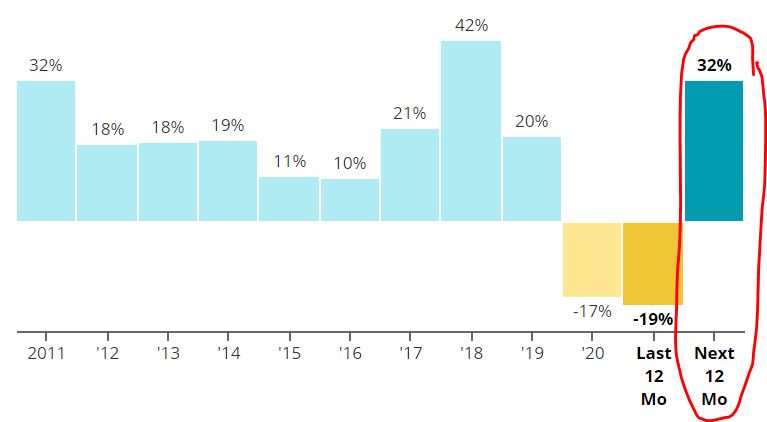

Mastercard continues to be weighed down by depressed cross-border transactions, which come with higher fees and margins. However, domestic spending has picked up nicely with gross dollar volume up 8% year over year. Constant-currency revenue was up 2%, while adjusted EPS declined 5%. Mastercard will need a recovery in international travel to truly return to form, but it seems like that’s only a matter of time, thanks to the global vaccination campaign.

The following graphic of the company’s year-over-year EPS growth illustrates this perfectly.

Simply Safe Dividends

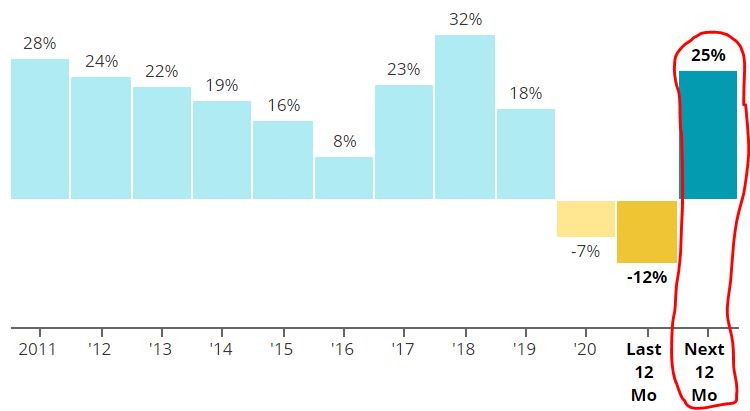

The red-circled area in the above graphic shows the expected earnings rebound to come, and we see a similar pattern in the Visa graphic below: sensational growth for most of a decade, a rough go during the pandemic, and a forecast of renewed growth in the coming year.

Wrapping Things Up

If I like Mastercard and Visa so much, why are they two of the smaller positions within the Income Builder Portfolio? (See all 41 IBP holdings HERE.)

Well, there are two reasons:

- They are always expensive, requiring investors to pay a steep premium.

- They have very low dividend yields — and “Income,” after all, is the first word in our portfolio’s name.

Despite those facts, however, I consider Mastercard and Visa to be such high-quality companies that I want to let them have their “contest” within the IBP.

I will go into great detail about valuations and dividends in my post-buy article, which is scheduled to be published on Tuesday, May 25.

As always, I remind investors to conduct their own due diligence before buying any stocks.

— Mike Nadel

Source: DividendsAndIncome.com

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.